Author: QW, Alibaba DAO Customer Support Source: X, @QwQiao Translation: Shan Oppa, Bitchain Vision

At Alliance Dao, we receive approximately 3,000 applications to join the cryptocurrency startup accelerator each year.The data we collect includes information on the blockchain network they build, product type, region and other information.Due to the huge sample size and our relatively unblinded attitude towards these factors, we are able to draw unique insights into the direction of the industry.

Blockchain network

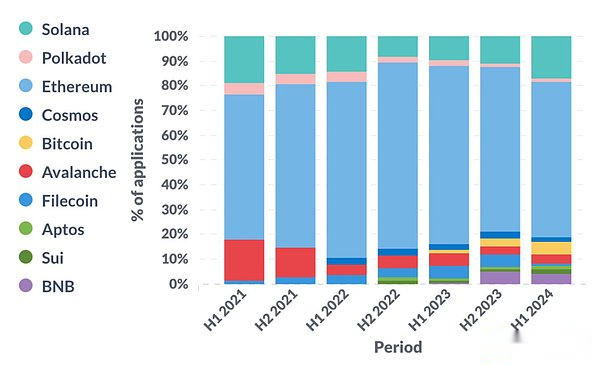

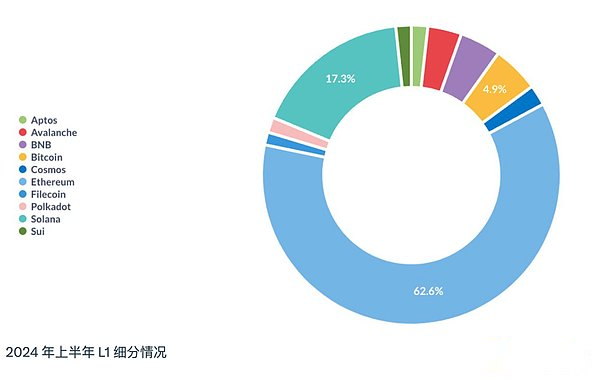

Layer 1

Ethereum remains the dominant ecosystem.However, after bottoming out in the second half of 2022, Solana is backing strongly.This is no coincidence, as FTX also collapsed in the second half of 2022.Bitcoin has experienced a revival with excitement surrounding the inscriptions (ordinals), runes (runes), and Bitcoin Layer 2.

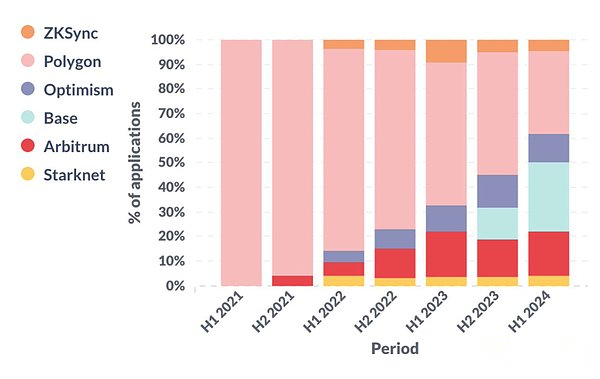

Ethereum Layer 2

Deep into Ethereum Layer 2 (and sidechain).Optimistic rollups have steadily occupied market share in the past 3 years.It is worth noting that in the first half of 2024, more than a quarter of the startups built on Ethereum Layer 2 chose the Base network.

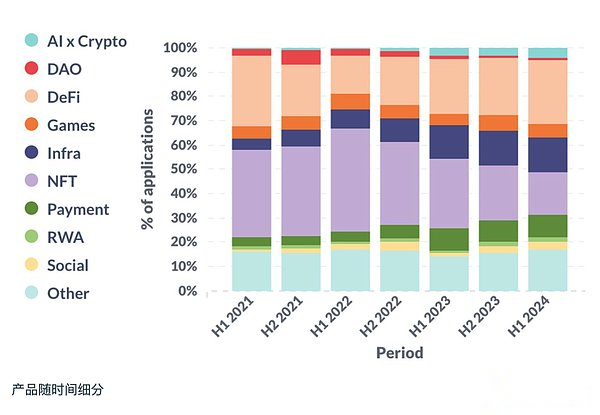

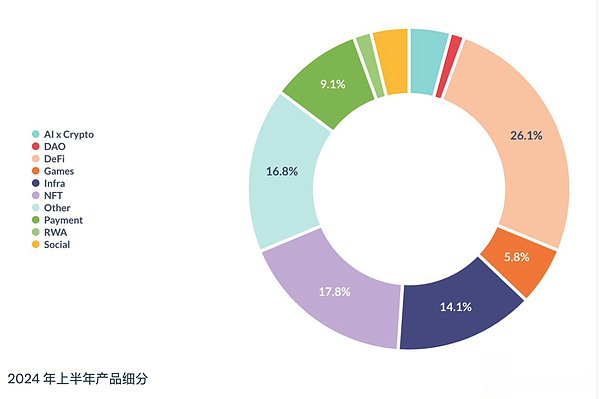

Product Type

The number of startups used to integrate infrastructure, DeFi, payments and AI with blockchain technology is increasing, mainly at the expense of NFTs.Among them, infrastructure and AI are in line with the hot topics of public discussion.But the rise of DeFi and payments may surprise most people because the public isn’t very enthusiastic about it.Coincidentally, we believe that this is also the only two verticals in the cryptocurrency space that have found undeniable product market fit (PMF).

Note that this is an imperfect attempt to make product categories, as these categories are obviously not mutually exclusive.For example, a startup might be involved in both gaming and NFT, in which case we would assign weights of 0.5 to gaming and NFT respectively.

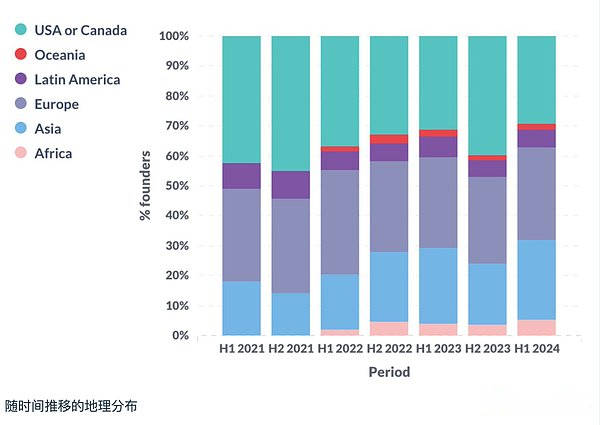

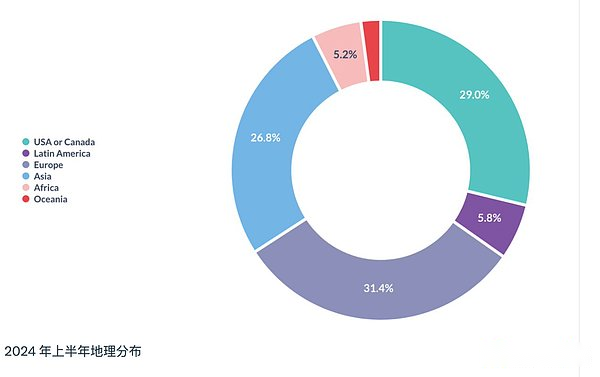

Regional distribution

In the first half of 2024, the proportion of startups from the United States and Canada fell to an all-time low, while the proportion of startups from Asia and Africa hit a record high.This may be due to 1) uncertainty in U.S. regulation, and 2) the practical application of cryptocurrencies in emerging markets.

All in all, North America, Europe and Asia remain the three major regions, with startups contributing in each region accounting for one-quarter to one-third of the overall.

The following sections may be for the founderand venture capital institutionsMore attractive, the general public can skip it.

Founder background

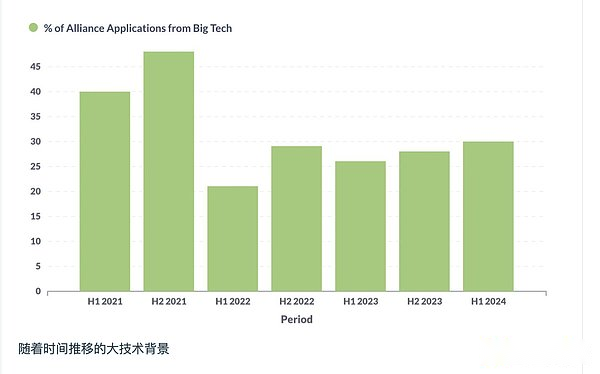

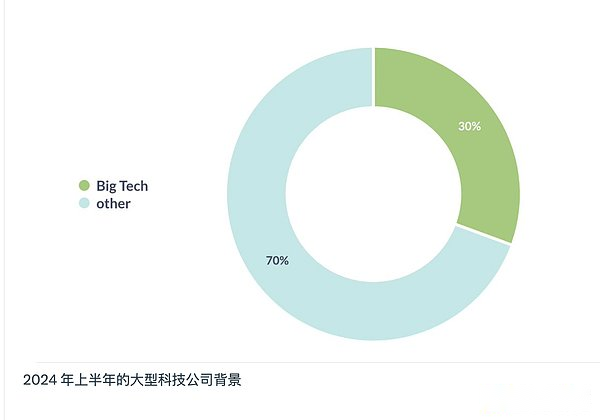

Large tech companies

The proportion of founders from the background of “large tech companies” peaked in 2021 and is currently stable at around 30%.We define tech companies in the S&P 500 as large tech companies.The exact definition is not important, it is important to observe trends over time.

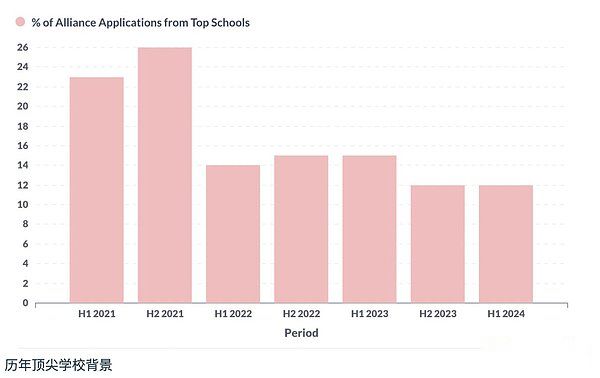

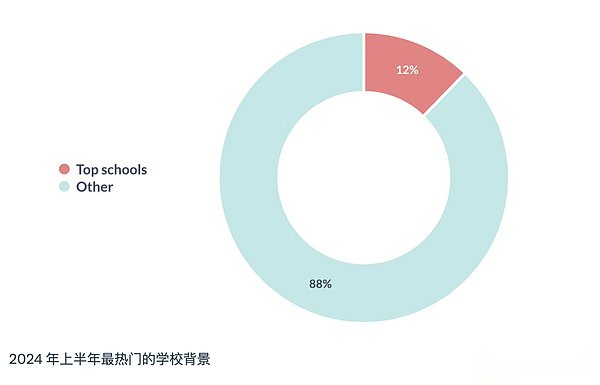

Top universities

Similarly, the proportion of founders who graduated from “top universities” will also peak in 2021.We define QS’s top 100 universities as top universities.

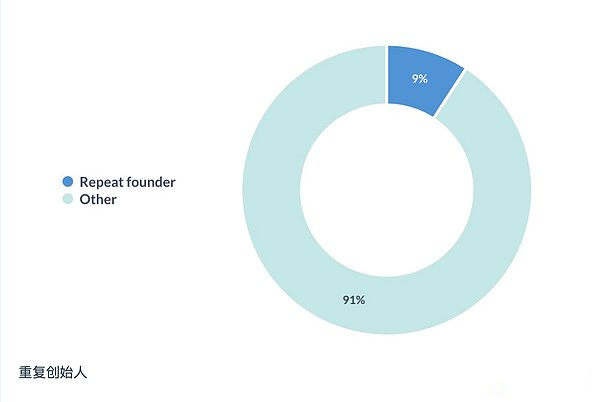

Serial entrepreneurs

About one in 10 founders have previously started a startup.

Team composition

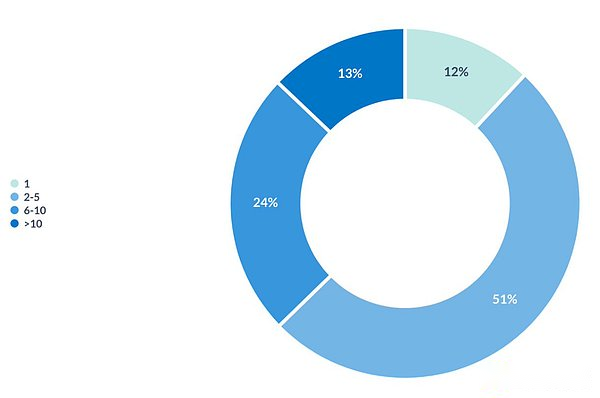

Team size

More than half of the startup teams are between 2-5 people.We also think this is the best scale for startups that have not yet found a product market fit (PMF).

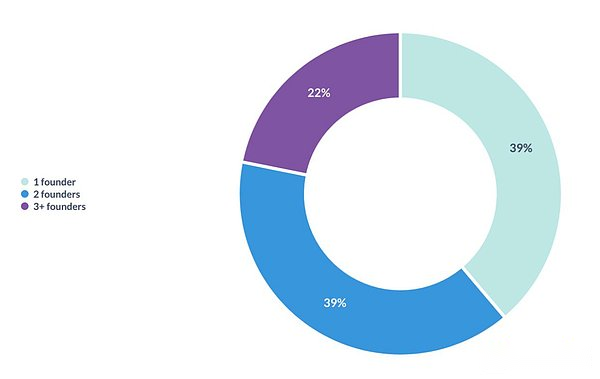

Number of co-founders

Less than 40% of startups are founded by a single founder.For reference, some studies show that 20-30% of unicorn companies are founded by a single founder.

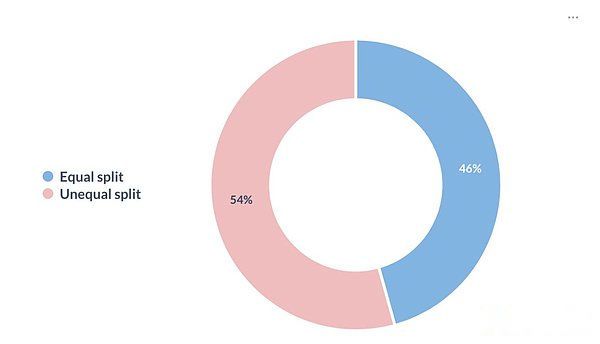

Equity distribution

Among startups with two or more co-founders, about half will choose to split the equity, while the other half will choose to split the equity.

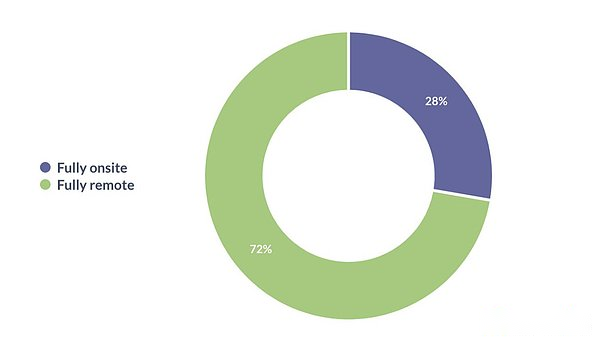

telecommute

Nearly three-quarters of startups implement a full remote work system.