1. Introduction: The key turning point in the SEC new policy and the DeFi regulatory landscape

Decentralized Finance (DeFi) has developed rapidly since 2018 and has become one of the core pillars of the global crypto asset system.Through an open and licenseless financial agreement, DeFi provides rich financial functions including asset trading, lending, derivatives, stablecoins, asset management, etc. It relies on smart contracts, on-chain settlement, decentralized oracles and governance mechanisms at the technical level, realizing in-depth simulation and reconstruction of the traditional financial structure.Especially since “DeFi Summer” in 2020, the total lock-in volume of DeFi protocol (TVL) once exceeded US$180 billion, marking that the scalability and market recognition in this field have reached an unprecedented level.

However, the rapid expansion in this field continues to be accompanied by problems such as scale blur, systemic risks and regulatory vacuum.Under the leadership of Gary Gensler, former chairman of the Securities and Exchange Commission (SEC), U.S. regulators have adopted a stricter and centralized law enforcement regulatory strategy for the overall crypto industry. Among them, DeFi protocols, DEX platforms, DAO governance structures, etc. have been included in the scope of possible illegal securities transactions, unregistered brokers or clearing agents.From 2022 to 2024, Uniswap Labs, Coinbase, Kraken, Balancer Labs and other projects have been investigated and enforced by the SEC or CFTC in different forms.At the same time, the long-term lack of criteria for determining “whether it is fully decentralized”, “whether there are public financing behaviors”, and “whether it constitutes a securities trading platform”, has caused the entire DeFi industry to fall into multiple difficulties such as restricted technological evolution, shrinking capital investment, and leaving developers in amid policy uncertainty.

This regulatory context has undergone significant changes in the second quarter of 2025.In early June, Paul Atkins, the new SEC chairman, proposed the path to actively regulate DeFi for the first time at a Congressional FinTech hearing, and clarified three policy directions: First, establish an “Innovation Exemption” for agreements with high degree of decentralization, and suspended some registration obligations within a specific pilot scope; second, promote the “Functional Categorization Framework” to classify supervision based on the business logic of the agreement and on-chain operations, rather than identifying it as a securities platform with one-size-fits-all “whether to use Tokens”; third, incorporate the DAO governance structure and the actual asset on-chain (RWA) project into the open financial regulatory sandbox, and connect with the rapidly developing technology prototypes with low-risk and traceable regulatory tools.This policy shift echoes the White Paper on Systemic Risks of Digital Assets issued by the U.S. Treasury Department’s Financial Stability Regulatory Commission (FSOC) in May of the same year. The latter proposed for the first time to pass a regulatory sandbox and functional testing mechanism to avoid “stifling innovation” while protecting investors’ rights and interests.

2. Evolution of the US regulatory path: Transformation logic from “default illegal” to “functional adaptation”

The US regulatory evolution of decentralized finance (DeFi) is not only a microcosm of its financial compliance framework responding to emerging technologies, but also a profound reflection of the trade-off mechanism between “financial innovation” and “risk prevention”.The current SEC policy attitude towards DeFi is not an isolated incident, but a product of the gradual evolution of multiple inter-agency games and regulatory logic in the past five years.Understanding its transformational foundation requires a backbone of the roots of regulatory attitudes in the early days of the rise of DeFi, feedback loops of major law enforcement events, and systematic tensions in the application of laws at the federal and state levels.

Since the DeFi ecosystem gradually took shape in 2019, the SEC’s core regulatory logic has relied on the securities judgment framework of Howey Test in 1946, that is, any contractual arrangement involving capital investment, common enterprises, profit expectations and relying on others’ efforts to obtain profits can be regarded as securities transactions and included in the scope of supervision.Under this standard, the vast majority of tokens issued by DeFi protocols (especially with governance weights or profit distribution powers) are presumed to be unregistered securities, posing potential compliance risks.In addition, under the provisions of the Securities Exchange Act and the Investment Company Act, any act of matching, liquidating, holding or recommending digital assets without explicit exemption may constitute an illegal act of an unregistered securities broker or liquidation agency.

During 2021 and 2022, the SEC has taken a series of high-profile law enforcement actions.Representative cases include whether Uniswap Labs is investigated to constitute an “unregistered securities platform operator”, agreements such as Balancer and dYdX face allegations of “illegal marketing promotion”. Even privacy agreements such as Tornado Cash have been included in the sanctions list by the Office of Foreign Assets Control (OFAC) of the Ministry of Finance, showing that the regulatory authorities have adopted a law enforcement strategy of wide coverage, strong crackdowns and blurred boundaries in the DeFi field.The regulatory tone of this stage can be summarized as “presumption of illegality”, that is, the project party must prove that its agreement design does not constitute securities transactions or is not subject to US jurisdiction, otherwise it will face compliance risks.

However, this regulatory strategy of “law enforcement first and rules lag” quickly encountered challenges at the legislative and judicial levels.First, the results of many litigation cases have gradually exposed the limitations of regulatory judgments being applicable under decentralized conditions.For example, the US court ruled in SEC v. Ripple that XRP does not constitute securities in some secondary market transactions, effectively weakening the SEC’s position on “all tokens are securities.”Meanwhile, the ongoing legal dispute between Coinbase and the SEC has made “regulatory clarity” the core issue of the industry and Congress pushing for crypto legislation.Secondly, the SEC faces fundamental difficulties in the application of legal structures such as DAO.Since DAO’s operations do not have a legal entity or beneficiary center in the traditional sense, its on-chain autonomy mechanism is difficult to classify as the traditional securities logic of “producing returns from the efforts of others.”Correspondingly, regulatory authorities also lack sufficient legal tools to implement effective subpoenas, fines or injunctions on DAO, thus creating an idle dilemma for law enforcement to be implemented.

It is against the background of the gradual accumulation of institutional consensus that the SEC made strategic adjustments after personnel changes in early 2025.The new chairman Paul Atkins has long advocated the use of “technological neutrality” as the bottom line of regulation, emphasizing that financial compliance should design regulatory boundaries based on functions rather than technology implementation.Under its presidency, the SEC established a “DeFi Strategy Research Group” within and jointly organized a “Digital Finance Interaction Forum” with the Ministry of Finance to build a risk classification and governance assessment system for the main DeFi protocols through data modeling, protocol testing, on-chain tracking and other means.This technology-oriented and risk-hierarchical regulatory method represents the transition from traditional securities law logic to “functionally adaptive regulation”, that is, the actual financial functions and behavioral patterns of the DeFi protocol are used as the basis for policy design, so as to achieve an organic combination of compliance requirements and technical flexibility.

It should be pointed out that the SEC has not given up its regulatory claims in the DeFi field, but is trying to build a more resilient and iterable regulatory strategy.For example, for DeFi projects with obvious centralized components (such as front-end interface operation, governance multi-signature control, and agreement upgrade authority), they will be required to fulfill their registration and disclosure obligations; for highly decentralized and purely executed protocols, an exemption mechanism of “technical testing + governance audit” may be introduced.In addition, by guiding project parties to voluntarily enter the regulatory sandbox, the SEC plans to cultivate a “middle zone” of the compliant DeFi ecosystem while ensuring market stability and user rights and interests to avoid spillover losses caused by one-size-fits-all policies.

Overall, the US DeFi regulatory path is gradually evolving from the early strong application of law and law enforcement suppression to institutional negotiation, functional identification, and risk guidance.This shift not only reflects a deepening understanding of technological heterogeneity, but also represents the attempt of regulators to introduce new governance paradigms in the face of open financial systems.In the future policy implementation, how to reach a dynamic balance between protecting investors’ interests, ensuring system stability and promoting technological development will become the core challenge of the sustainability of the DeFi regulatory system in the United States and even the world.

3. Three major wealth codes: value revaluation under institutional logic

With the official implementation of the new SEC regulatory policy, the overall attitude of the US regulatory environment towards decentralized finance has undergone a substantial change, from “post-law enforcement” to “pre-compliance” and then to “functional adaptation”, bringing long-lost institutional positive incentives to the DeFi sector.Against the background of the gradual clarification of the new regulatory framework, market participants began to reevaluate the underlying value of the DeFi protocol, and several tracks and projects that were originally suppressed by “compliance uncertainty” began to show significant revaluation potential and allocation value.Starting from the institutional logic, the current main line of value revaluation in the DeFi field is mainly concentrated in three core directions: the institutional premium of the compliant intermediary structure, the strategic position of on-chain liquidity infrastructure, and the credit reconstruction space of high-endogenic income model protocols. These three main lines constitute the key starting point of the next round of DeFi’s “wealth code”.

First, as the SEC emphasizes the “function-oriented” regulatory logic and proposes to include some front-end operations and service layer agreements in the registration exemption or regulatory sandbox testing mechanism, on-chain compliance intermediaries are becoming a new value depression.Unlike the ultimate pursuit of “de-mediation” in the early DeFi ecosystem, the current regulatory and market have created structural demands for “compliant intermediary services”, especially at key nodes such as identity verification (KYC), on-chain anti-money laundering (AML), risk disclosure, agreement governance and custody, project parties with clear corporate governance structure and service licenses will become a necessary channel for compliance paths.This trend will enable DID protocols, compliant custodian service providers, and front-end operating platforms with high governance transparency to gain higher policy tolerance and favor by investors, thereby promoting the transformation of its valuation system from “technical tool attributes” to “institutional infrastructure”.It is worth pointing out that the “compliance chain” modules that are rapidly developing in some Layer2 solutions (such as Rollup with a whitelisting mechanism) will also play a key role in the rise of this compliance intermediary structure, providing a credible execution basis for traditional financial capital to participate in DeFi.

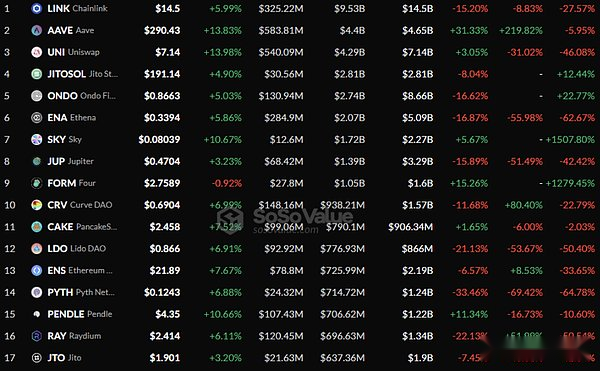

Secondly, as the underlying resource allocation engine of the DeFi ecosystem, on-chain liquidity infrastructure has regained strategic valuation support due to the clarity of the system.Although liquidity aggregation platforms represented by decentralized trading protocols such as Uniswap, Curve, and Balancer have faced multiple challenges such as liquidity exhaustion, token incentive failure, and regulatory uncertainty suppression in the past year, driven by the new policy, platforms with protocol neutrality, high composability and governance transparency will once again become the first choice for the inflow of funds in DeFi ecological structure.Especially under the principle of “separating the protocol and front-end supervision”, the underlying AMM protocol, as an on-chain code execution tool, will significantly alleviate its legal risks. Combined with the continuous enrichment of RWA (real-world assets) and on-chain asset bridges, the depth of on-chain transactions and capital efficiency are expected to be systematically repaired.In addition, the on-chain oracle and price feed infrastructure represented by Chainlink have become the key “risk controllable neutral node” in institutional-level DeFi deployment because it does not constitute a direct financial intermediary in regulatory classification, and bears important responsibilities for system liquidity and price discovery within the compliance framework.

Again, the DeFi protocol with high endogenous yields and stable cash flow will usher in a credit recovery cycle after institutional pressure is released, becoming the focus of risk funds again.In the first few cycles of DeFi development, lending agreements such as Compound, Aave, and MakerDAO have become the credit foundation of the entire ecosystem with their robust mortgage models and clearing mechanisms.However, as the crypto credit crisis spreads between 2022 and 2023, the assets and liabilities of DeFi protocols are under pressure to liquidate, and frequent incidents such as stablecoin deans and liquidity depletion occur. In addition, the security concerns of asset security caused by the gray area of regulatory have made these protocols generally face structural risks of weakened market trust and sluggish token prices.Nowadays, after supervision has gradually clarified and built a systematic recognition path for protocol revenue, governance model, and audit mechanisms, these protocols have the potential to become a “stable cash flow carrier on-chain” with their quantifiable and verifiable on-chain real income model and low operating leverage.Especially under the evolution of the DeFi stablecoin model to “multi-collateralization + real asset anchoring”, on-chain stablecoins represented by DAI, GHO, and sUSD will build an institutional moat against centralized stablecoins (such as USDC, USDT) under a clearer regulatory positioning, enhancing their systematic attractiveness in institutional fund allocation.

It is worth noting that the common logic behind these three main lines is the rebalancing process of transforming the “policy cognitive dividend” brought by the new SEC policy into the “market capital pricing weight”.The past DeFi valuation system relied heavily on speculative momentum and expectations, and lacked stable institutional moats and fundamental support, resulting in its strong vulnerability in the market countercyclical period.Now, after the regulatory risks are alleviated and the legal paths are confirmed, the DeFi agreement can establish a valuation anchoring mechanism for institutional capital through real on-chain revenue, compliance service capabilities and systematic participation thresholds.The establishment of this mechanism not only gives the DeFi protocol the ability to rebuild the “risk premium-return model”, but also means that DeFi will have the credit pricing logic of financial companies for the first time, creating a system prerequisite for it to access the traditional financial system, RWA docking channels and on-chain bond issuance.

4. Market Echo: From TVL Soaring to Revaluation of Asset Prices

The release of the new SEC regulatory policy not only sends a positive signal of prudent acceptance and functional supervision in the DeFi field at the policy level, but also quickly triggers a chain reaction at the market level, forming an efficient positive feedback mechanism of “institutional expectations – capital return – asset revaluation”.The most direct reflection is the significant rebound in the total lock-in volume of DeFi (TVL).Within a week after the release of the new policy, according to the tracking of mainstream data platforms such as DefiLlama, DeFi TVL on the Ethereum chain quickly jumped from about $46 billion to nearly $54 billion, with a single-week increase of more than 17%, setting the largest weekly increase since the FTX crisis in 2022.At the same time, the locked positions of multiple mainstream protocols such as Uniswap, Aave, Lido, Synthetix, etc. have increased simultaneously, and indicators such as on-chain transaction activity, Gas usage, and DEX transaction volume have also rebounded in full swing.This broad-spectrum market response shows that clear signals at the regulatory level have effectively alleviated institutional and retail investors’ concerns about the potential legal risks of DeFi in the short term, thereby promoting over-the-counter funds to re-enter the sector and forming a structural incremental liquidity injection.

Driven by the rapid return of funds, multiple leading DeFi assets have experienced price revaluation.Taking UNI, AAVE, MKR and other governance tokens as examples, within one week after the new policy was implemented, the average price increase was between 25% and 60%, far exceeding the increase in BTC and ETH during the same period.This round of price rebound is not simply driven by emotions, but reflects the market’s new round of valuation modeling of the future cash flow capabilities and institutional legitimacy of the DeFi protocol.Previously, due to compliance uncertainty, the valuation system of DeFi governance tokens was often given a large discount by the market, and the real revenue of the agreement, the value of governance rights and future growth space were not effectively reflected in the market value.At present, with the gradual clear institutional path and policy tolerance for operational legitimacy, the market has begun to revalue the DeFi protocol based on traditional financial indicators such as the protocol profit multiple (P/E), unit TVL valuation (TVL multiple) and on-chain active user growth model.This return to valuation methodology not only enhances the investment attractiveness of DeFi assets as a “cash flow asset”, but also marks the beginning of evolution of the DeFi market to a more mature and quantifiable capital pricing stage.

Not only that, the on-chain data also shows a changing trend in the distribution structure of funds.After the release of the new policy, the number of on-chain deposit transactions, number of users and average transaction volume of multiple protocols have all increased significantly, especially in protocols with high integration with RWA (such as Maple Finance, Ondo Finance, Centrifuge), the proportion of institutional wallets has increased rapidly.Take Ondo as an example. The short-term US Treasury token OUSG launched, the issuance scale has increased by more than 40% since the release of the New Deal, indicating that some institutional funds seeking compliance paths are using the DeFi platform to allocate on-chain fixed income assets.Meanwhile, stablecoin inflows on centralized exchanges have shown a downward trend, while net stablecoin inflows in DeFi protocols have begun to rebound, a change that shows that investors’ confidence in the security of on-chain assets is recovering.The trend of the decentralized financial system regaining the pricing power of funds has begun to emerge. TVL is no longer just a short-term traffic indicator for speculative behavior, but has gradually transformed into a weather vane for asset allocation and fund trust.

It is worth noting that although the market is currently resounding significantly, the revaluation of asset prices is still in the initial stage, and the space for realizing the institutional premium is far from being completed.Compared with traditional financial assets, DeFi protocols still face higher regulatory trial and error costs, governance efficiency issues and on-chain data auditing difficulties, resulting in the market still maintaining a certain cautious attitude after the risk preference turns.But it is this resonant situation of “institutional risk contraction + value expectation repair” that has opened up space for valuation to expand again for the medium-term market of the DeFi sector in the future.The current P/S (market-to-market sales ratio) of multiple head agreements is still far lower than the mid-term level of the 2021 bull market, and under the premise that real income continues to grow, regulatory certainty will enable its valuation center to gain upward movement.At the same time, the revaluation of asset prices will also be transmitted to token design and distribution mechanisms. For example, some protocols are restarting governance token repurchases, increasing the proportion of agreement surplus dividends, or promoting the reform of the staking model that is linked to the agreement revenue, further incorporating “value capture” into the market pricing logic.

5. Future Outlook: Institutional Reconstruction and New Cycle of DeFi

Looking ahead, the new SEC policy is not only a compliance-level policy adjustment, but also a key turning point for the DeFi industry to move towards institutionalized reconstruction and sustainable and healthy development.This policy clarifies regulatory boundaries and market operation rules, laying the foundation for the DeFi industry to move from a “wild growth” stage to a mature market with “compliant and orderly”.Against this background, DeFi not only faces a significant reduction in compliance risks, but also ushers in a new stage of development in value discovery, business innovation and ecological expansion.

First of all, starting from the institutional logic, the institutionalized reconstruction of DeFi will have a profound impact on its design paradigm and business model.Traditional DeFi protocols mostly focus on the automated execution of “code is law” and rarely consider compatibility with the actual legal system, causing potential legal gray areas and operational risks.Through the clarification and refinement of compliance requirements, the new SEC policy prompts DeFi projects to design a dual identity system that has both technical advantages and compliance attributes.For example, the balance between compliance identity verification (KYC/AML) and on-chain anonymity, the legal responsibility of protocol governance, and the compliance data reporting mechanism have become important issues in the design of DeFi protocols in the future.By embedding compliance mechanisms into smart contracts and governance frameworks, DeFi will gradually form a new paradigm of “embedded compliance”, realizing the deep integration of technology and laws, thereby reducing the uncertainty and potential penalties brought about by regulatory conflicts.

Secondly, institutional reconstruction will inevitably promote the diversification and deepening of DeFi business models.In the past, the DeFi ecosystem relied too much on short-term incentives such as liquidity mining and transaction fees, making it difficult to continuously create stable cash flow and profitability.Under the guidance of the new policy, the project party will pay more attention to building a sustainable profit model, such as gradually forming a closed loop of returns comparable to traditional financial assets through protocol-level income sharing, asset management services, compliant bonds and collateral issuance, and RWA (Real-World Asset) on-chain.Especially in RWA integration, compliance signals have greatly enhanced institutions’ trust in DeFi products, allowing diversified asset types including supply chain finance, real estate asset securitization, bill financing, etc. to enter the on-chain ecosystem.In the future, DeFi will no longer be a purely decentralized trading venue, but will also become an institutionalized financial infrastructure for on-chain asset issuance and management.

Third, the institutional reconstruction of the governance mechanism will also become the core driving force for DeFi to move towards a new cycle.In the past, DeFi governance mostly relied on token voting, which had problems such as excessive decentralization of governance power, low turnout, and low governance efficiency, and lacked connection with the traditional legal system.The governance norms proposed by the SEC new policy prompt the agreement designer to explore more legally effective governance frameworks, such as improving the legitimacy and execution of governance through the registration of DAO legal identity, legal confirmation of governance behavior, and the introduction of multi-party compliance supervision mechanisms.In the future, DeFi governance may adopt a hybrid governance model, combining on-chain voting, off-chain agreements and legal frameworks to form a transparent, compliant and efficient decision-making system.This not only helps alleviate the risks of power concentration and manipulation in the governance process, but also enhances the agreement’s trust in external regulators and investors, becoming an important cornerstone of DeFi’s sustainable development.

Fourth, with the improvement of compliance and governance system, the DeFi ecosystem will usher in a richer transformation of participants and capital structure.The new policy greatly lowers the threshold for institutional investors and traditional financial institutions to enter DeFi.Traditional capital such as large asset management companies, pension funds, family offices, etc. are actively seeking compliant on-chain asset allocation solutions, which will give rise to more customized DeFi products and services for institutions.At the same time, the insurance, credit and derivatives markets under a compliance environment will also usher in explosive growth, promoting the full coverage of on-chain financial services.In addition, the project party will also optimize the token economic model, strengthen the inherent rationality of tokens as governance tools and value carriers, attract long-term holdings and value investments, reduce short-term speculative fluctuations, and inject sustained impetus into the stable development of the ecosystem.

Fifth, technological innovation and cross-chain integration are the technical support and development engines for DeFi institutional reconstruction.Compliance needs promote technological innovation in protocols in privacy protection, identity authentication, contract security, etc., and give rise to the widespread application of privacy protection technologies such as zero-knowledge proof, homomorphic encryption, and multi-party computing.At the same time, cross-chain protocol and Layer 2 expansion solutions will realize the seamless flow of assets and information between multi-chain ecosystems, breaking the on-chain island effect, and improving the overall liquidity and user experience of DeFi.In the future, the multi-chain integration ecosystem under the compliance base will provide a solid foundation for DeFi’s business innovation, promote the deep integration of DeFi and the traditional financial system, and realize a new form of “on-chain + off-chain” hybrid finance.

Finally, it is worth pointing out that although the DeFi institutionalization process has opened a new chapter, the challenges still exist.The stability of policy implementation and international regulatory coordination, the control of compliance costs, the improvement of project parties’ compliance awareness and technical capabilities, and the balance of user privacy protection and transparency are all key issues in the healthy development of DeFi in the future.All parties in the industry need to work together to promote the formulation of standards and the construction of self-discipline mechanisms, and use industry alliances and third-party audit institutions to form a multi-level compliance ecosystem to continuously improve the overall institutionalization level and market trust of the industry.

6. Conclusion: DeFi’s wealth new frontier has just begun

As the forefront of blockchain financial innovation, DeFi is at a critical node of institutional reconstruction and technological upgrading. The new SEC policy has brought it an environment where norms and opportunities coexist, promoting the industry from wild growth to compliant development; in the future, with continuous breakthroughs in technology and increasing ecology, DeFi is expected to achieve broader financial inclusiveness and value reshaping, becoming an important cornerstone of the digital economy. However, the industry still needs to continue to work in compliance risks, technical security and user education to truly open up the long-term prosperity of the new frontier of wealth.With the new SEC policy, from “innovation exemption” to “on-chain finance” may lead to a full explosion, the summer of DeFi may reappear, and the blue-chip tokens in the DeFi sector may usher in a revaluation of value.