Friends in the currency circle should still remember that in July 2025, Trump signed the GENIUS Act.Not long after, the US Treasury Department launched the ANPRM solicitation of opinions, which suddenly sparked heated discussions in the circle.

I believe everyone is eager to understand the latest situation. This article by Sister Sa’s team is still the same. Let’s first take you to review the history of the development of the US stablecoin, and then dismantle the core focus of the GENIUS Act and ANPRM.

01History of the Development of US Stablecoins ——About the GENIUS Act

Old friends all know that the early years of US crypto regulation was a “coin melee”: the SEC said cryptocurrency was “securities”, the CFTC said it was “commodity”, and different states were different. The BitLicense in New York was so strict that it persuaded companies to withdraw, but Wyoming gave crypto companies a green light.In 2025, the situation began to change. The GENIUS Act and the STABLE Act launched by the Senate and the House of Representatives have been implemented one after another, marking the entry of the “Gemini” era of US stablecoin regulation. Therefore, if everyone wants to understand the current situation of US stablecoins and the role of soliciting opinions on the GENIUS Act, these two bills need to be put together first.

These two bills can be called “Gemini” in the US stablecoin legislation, and their paths are similar.

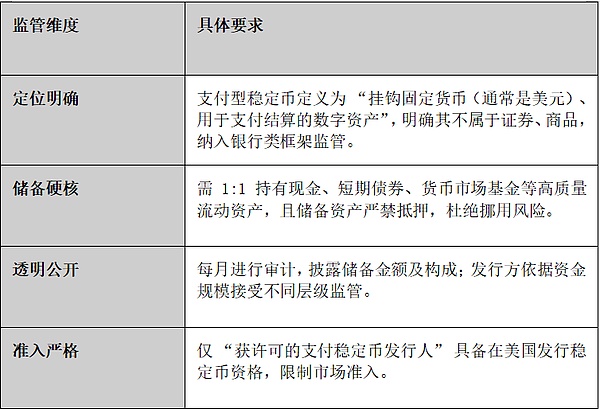

Let’s first look at the GENIUS Act (full name “2025 National Innovation Act to Guide and Establish U.S. Stablecoins”), which was proposed by the Senator in February 2025. The core is to tailor the development path for “payment-type stablecoins”.Its key content can be summarized in one table:

Let’s look at the STABLE Act (full name “The Ledger Economic Act for Stablecoin Transparency and Accountability in 2025”), which is consistent with the core logic of the GENIUS Act, but the details vary.First, the positioning focuses differently.Payment-type stablecoins are also defined, but it is particularly emphasized that “the issuer must promise to be exchanged, redeemed or repurchased in fixed currency”, and highlights the guaranteed property;Second, the core rules are the same: It is also 1:1 to maintain high-quality current assets, regular audit disclosure, and license issuance, but the requirements of international issuers and the upper limit of state-level regulatory authority.

In general, these two bills have no substantial conflict, but are more like “complementary partners”: the GENIUS Act sets up a framework to clarify the regulatory ownership and development direction of stablecoins; the STABLE Act completes transparency and accountability details, and focuses on the safety of user funds.

02ANPRM Six major issues and public opinion focus

After understanding the development history of US stablecoins, old friends can change their perspective and comment on the ANPRM recently issued by the US Treasury Department to officially promote the implementation of the GENIUS Act.This opinion collection covers almost the entire stablecoin ecosystem, with the core focus on six major issues: one is the definition of issuer qualifications (including the “equivalent supervision” recognition of overseas issuers), the second is the rules for holding and disclosure of reserve assets, the third is the scope of extraterritorial application (compliance requirements of overseas institutions for US services), the fourth is the restrictions on anti-money laundering and marketing, the fifth is the characterization of federal income tax, and the sixth is the ban on interest payments (including indirect payment disputes).The opinions are still being collected. Although the conclusions are still difficult to form, there are several core topics in it, Sister Sa wants to talk to you.

First, who is eligible to issue stablecoins is a key issue in determining whether USDT can stay in the US market.The GENIUS Act stipulates that only “payment stablecoin issuing agencies” that have obtained official permission can issue coins in the United States.So the US Treasury Department is in this inquiry,A core issue is “Who can issue payment stablecoins in the United States”.According to the GENIUS Act, only licensed payment stablecoin issuers (PPSIs) can issue such stablecoins in the United States.In ANPRM, the public also requires feedback on whether additional definitions are needed and whether a “green channel” is opened for small transactions.

In this regard, for Tether, which issues USDT, if these new requirements are not met, there may be only three ways to go: either rectify according to the new regulations, withdraw from the US market, or launch new currencies that meet the regulations.Tether announced the launch of a USAT designed specifically for the United States, which is actually trying to meet regulatory conditions by “splitting the business”.It has a more profound impact on the determination of regulatory standards of foreign issuing institutions. By asking whether the regulatory systems of other countries meet the standards and how institutional compliance capabilities are, the United States is actually competing for the right to formulate global stablecoin rules. In the future, foreign stablecoins that do not meet the US standards may be difficult to enter the US market.

Second, can stablecoins send revenue to users?This question is also very quarrel.Although the bill prohibits issuers from directly paying interest from users, it does not stop exchanges and other platforms from rewarding in disguise.For example, if the Coinbase platform gives users a 4% stablecoin holding reward, the bank quits, accusing it of secretly attracting deposits and keeps lobbying the government to change the rules.The regulatory authorities asked whether it is considered a violation of the rules? Behind it is the traditional finance and crypto industries that are competing for the cake.

Written at the end

After all, the GENIUS Act and ANPRM are essentially the United States wants to encircle stable currency into the hegemony of the US dollar.The bill can protect the advantages of the US dollar stablecoin by binding US debt and setting a framework, but it is too optimistic to say that “hegemony is realized” is decentralized, and global supervision is competing. Coupled with the rise of Hong Kong and the advancement of offshore RMB stablecoins, Sa Jie believes that the United States cannot dominate at all.

Finally, I would like to give my old friends some practical suggestions. First, we must keep a close eye on the feedback results of ANPRM, especially the reserve custody and interest payment rules, which directly affect the cost and liquidity of USDT and USDC; second, we must focus on the Hong Kong market. Offshore RMB stablecoins have valuation depressions, and early layout may have opportunities.Now, supervision and innovation are playing every day, and only by understanding the rules and choosing the right track can we not capsize in the wave of stablecoins.