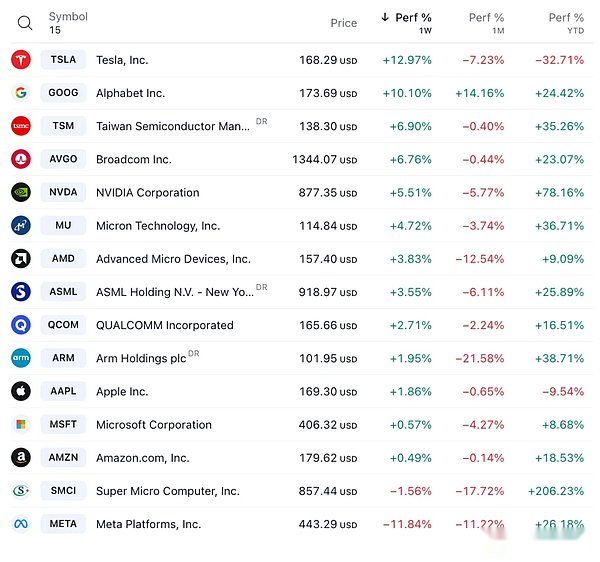

Last week, there were many financial reports of large companies, GDP data, and economic information such as inflation indicators that the Federal Reserve is concerned about. Investors are facing a massive influx of information and need to constantly reprice their assets. The market has also shown large fluctuations. Overall,The N-shaped trend finally closed higher, especially driven by technology stocks (Microsoft and Google’s financial reports), the stock market has recovered half of its decline in April.After falling 5.4% last week, the Nasdaq 100 rebounded 4% this week, with the S&P small-cap Russell 2000 rising more than 2%, and the Dow Jones Industrial Average rose less than 1%

We found that the main narrative of the market did not change fundamentally—the pace of economic growth slowed slightly, the pressure of inflation was high, geopolitical tensions continued, and interest rates rose slightly.but

-

Job market data continues to be strong

-

The current market environment is in a reinflation process rather than a recession

-

There is still a foundation for the recovery of global manufacturing

-

In the GDP data just released, personal consumption expenditure is still growing at a relatively healthy rate of 2.5%.

-

Enterprise equipment spending has increased for the first time in nearly a year, with the fastest growth rate of residential investment in more than three years

Therefore, in the medium term, the overall environment is still beneficial for risk asset investment.

Figure: All S&P sectors closed higher last week

The Big Seven’s profits are expected to grow 47% year-on-year in the first quarter, easily surpassing the S&P 500’s expected 2% earnings growth.Among the four companies that announced their results last week, three of them rose in stocks (Tesla, Alphabet, Microsoft), among which Alphabet performed outstandingly and announced dividends for the first time.But Meta, which has been strong before, fell as the company released lower-than-expected revenue forecasts while targeting higher capital expenditures to support AI.

From the trend of Meta, investors are more concerned about the future investment and expenditure plans of large technology companies, not just their current profitability.Meta announced that it would increase investment in AI infrastructure this year to as much as $10 billion, so big spending scares investors and makes the stock price plunge by 15%.

Meta, Microsoft, Tesla and Google had a total cash balance of up to $275 billion at the end of the first quarter.If a company uses its huge amount of cash to make strategic acquisitions, it will make investors happy.They don’t want to see companies spend a lot of money on projects that don’t know when they will be profitable.It feels like investors are limited in patience with high-valuation technology stocks now, and they look forward to quick returns.

One episode is that ByteDance’s insider reported that if the case is ultimately lost, the company is more inclined to shut down the entire software in the United States.On the one hand, TikTok is still a loss for Bytes, with a small proportion of revenue, and the closure has little impact on the company’s performance.On the other hand, the underlying algorithm in the APP is a trade secret of bytes and cannot be sold.If TikTok is finally turned off, the biggest beneficiary will definitely be Meta. However, such news has not prevented Meta from plummeting after the market, but if it happens, we are likely to see Meta jump.

Chinese stock market becomes a hot commodity

Recently, overseas investment banks such as Morgan Stanley, UBS, and Goldman Sachs have raised the ratings of China’s stock market. Policymakers suggest that PBoC may gradually increase its active trading in the secondary market of bonds, which may enhance market liquidity and increase investor sentiment..

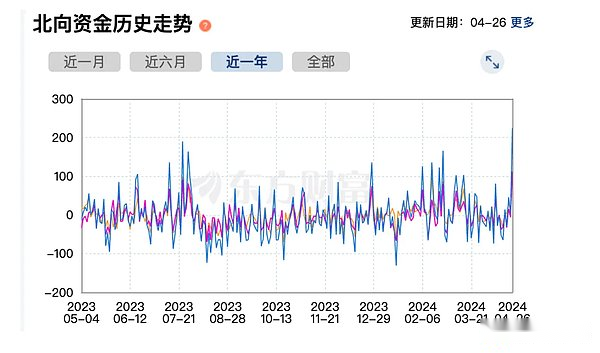

Net inflows from northbound funds hit record highs last week, with the CSI300 rising 1.2%, and the MXCN (MSCI China Concept Stock Index) and the Hang Seng Index up 8.0% and 8.8%, respectively, which are the best weekly returns since December 2022,The technology sector led the rise (+13.4%).Analysts believe that the attractiveness of low valuations in the A-share market is gradually emerging. With the continuous implementation of domestic economic growth policies, the numerator-side profitability levels and denominator-side liquidity factors that affect A-share market pricing are expected to be marginally improved. Foreign capitalNet inflow momentum may further increase.

Another positive sign is the real estate market. For example, the hot sales of luxury homes in Shanghai have led to the rise in the new housing price index, and the Shenzhen real estate market also showed signs of recovery, and the number of second-hand houses sold has increased significantly.John Lam, the first analyst who gave a “sell” rating to China Evergrande in early 2021, said that after the adjustment, the Chinese real estate industry is preparing to recover slowly, and it is expected that China’s real estate industry sales and prices will not beRises, but the decline will ease.He believes that domestic residential sales may fall by area by area, down from a record 27% drop in 2022.The new home operating rate may fall by 7%, narrowing from the 39% drop in 2022.Once house prices stabilize, pent-up demand will return as the decline in real estate prices over the past three years has led to delays in buying.

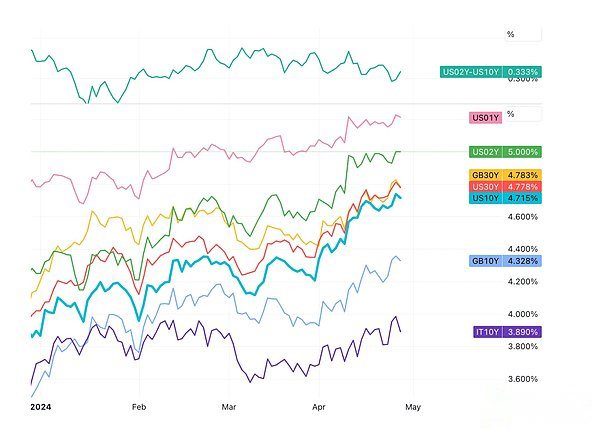

In terms of interest rates, the 10-year treasury bond interest rate closed at 4.66% last week, gradually approaching 5%, and the 2-year treasury bond interest rate closed at 5%. This week, the market absorbed a total of US$183 billion in new treasury bonds.Demand for issuance of 2-year Treasury bonds is strong, and 5-year and 7-year Treasury bonds are not bad either.

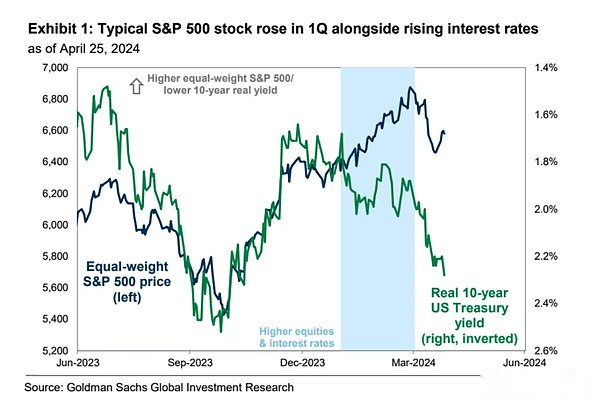

High interest rates are usually not conducive to the strengthening of the stock market:

Oil rebounded last week, up 1.92%.WTI crude oil closed at US$83.64, and the US dollar basically flattened DXY closed at 106.09.Gold fell 2% to close at $2,337 as fears of escalating conflict in the Middle East faded.The Industrial Metals Index fell slightly by 1.2%.

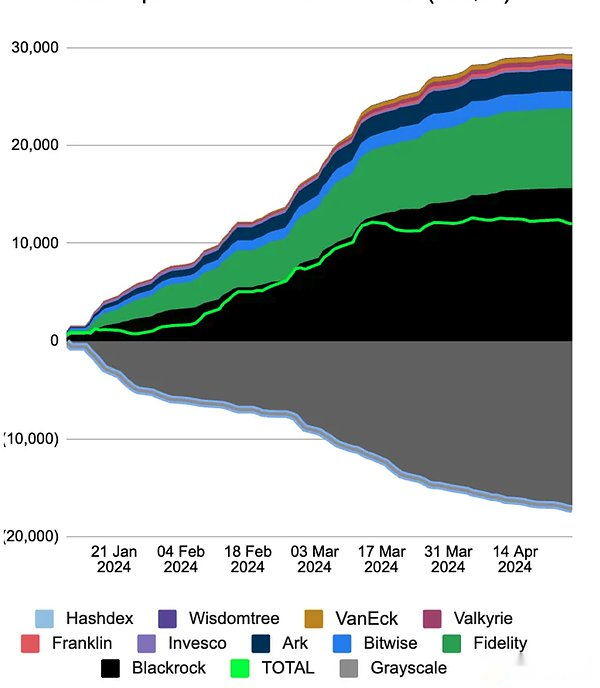

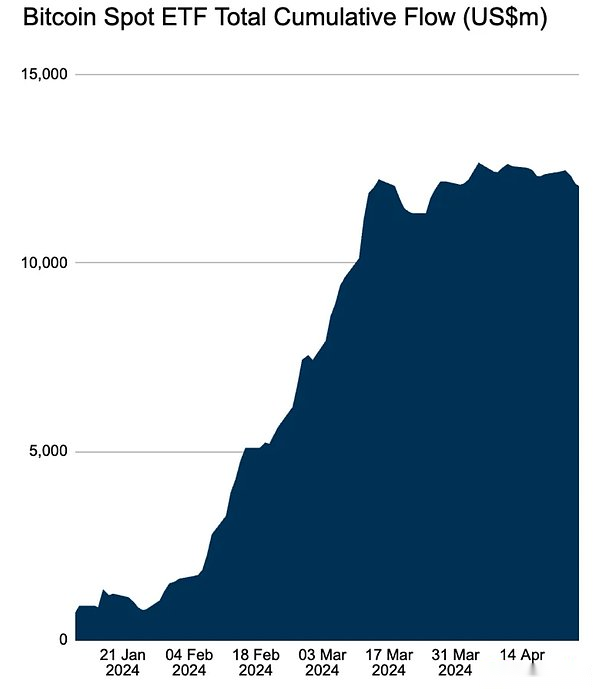

Cryptocurrencies lack new catalysts

Due to its lack of new catalysts, the favorable rebound in macro-market sentiment failed to drive cryptocurrencies. BTC spot ETFs have net outflows for the third consecutive week (-328 million), and IBIT has inflows of 0 in three consecutive trading days, the first time since its release.

After the conflict between Iran and Israel improved and Bitcoin successfully halved, the crypto market rebounded, and BTC once rose to more than $67,000.With the first spot ETH ETF in Hong Kong about to be listed on Tuesday, ETH rose by 7%+ over the weekend.In addition, Ethereum development company Consensys filed a lawsuit against the SEC on the grounds of regulatory overreach in order to counter the Wells notice received on April 10 (indicating that the SEC is working hard to file a case). As crypto companies suing regulatory victory is not uncommon, this is a good matchEthereum has also hedged regulatory pressure.

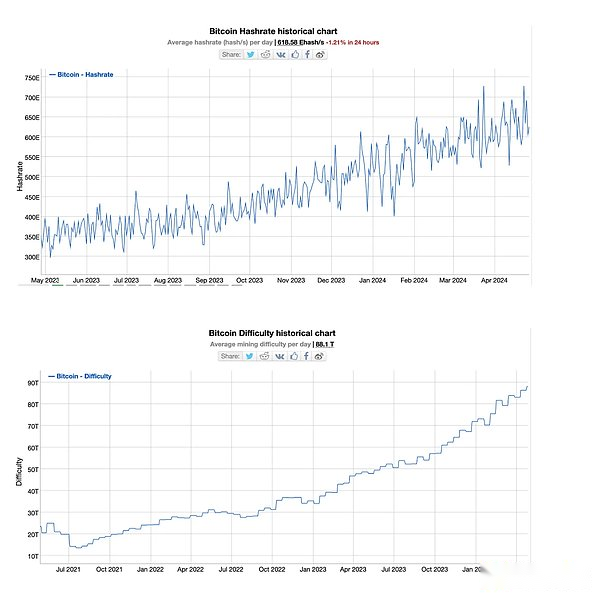

After the reduction of the version, the computing power of BTC network remained high and did not decrease significantly, but the difficulty of mining increased:

Trump is closer to loose monetary policy

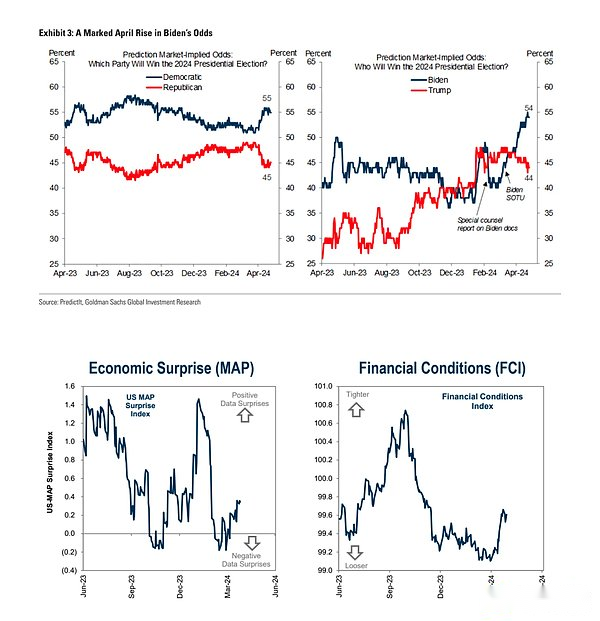

Politically, the Wall Street Journal published a heavy article about the Trump team plotting to manipulate the Federal Reserve after taking office. The plans they proposed include making interest rate policies negotiate with the president and letting the Treasury Department review the Federal Reserve’s regulatory measures.Trump hopes the Fed chairman can communicate with him and promote monetary policies that match his wishes.Despite concerns, there are obstacles in Trump’s impact on the Fed in actual operation, such as the FOMC has no space, and the market’s confidence in the Fed’s independence is crucial.These discussions and plans are worth further consideration only after Trump is re-elected, but from this can strengthen a market confidence — that is, the probability of Trump winning is rising = looser monetary policy, higher long-term inflation.

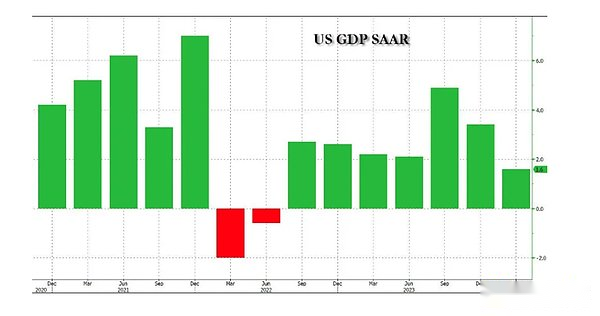

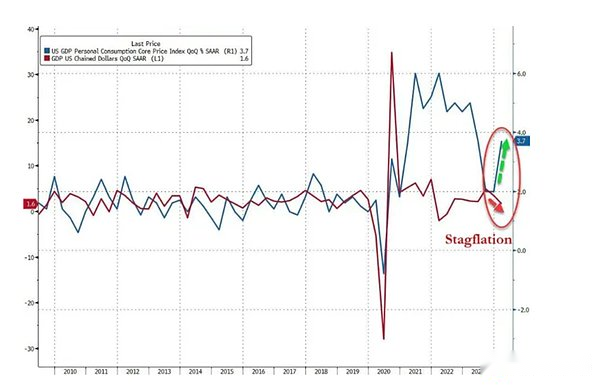

Signs of stagflation

The annualized quarterly initial value of the US real GDP in the first quarter increased by 1.6%, far below the market expectations of 2.5%, and a sharp slowdown from 3.4% in the fourth quarter of last year.But the GDP-weighted price index in the first quarter was 3.1%, higher than expected 3.0%, almost double the 1.6% in the fourth quarter.

Personal consumption expenditure (PCE) increased by 2.5% on the previous quarter-on-month basis, a sharp slowdown from the previous value of 3.3%, also lower than the expected 3%; the core PCE price index, excluding food and energy, increased by 3.7% on the annual quarter-on-month basis,It exceeded expectations by 3.4%, almost double the previous 2%, and was the first quarterly growth in a year.It shows that core inflation is still stubborn.

Signs of stagflation are the core logic of the market plunge on Thursday.

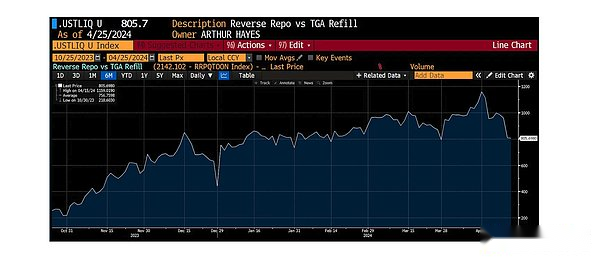

Moderate bond issuance plans may bring optimism

The current U.S. Treasury Department’s cash level is far beyond the previous forecast ceiling.As of yesterday, the Ministry of Finance had about $955 billion in its general account, $205 billion more than expected.The cash level of the Ministry of Finance increased significantly mainly due to the unexpected high income of capital gains tax on April 15.

Against the backdrop of “with surplus grain in hand”, the Ministry of Finance does not urgently need to issue short-term bills, resulting in the need to drop the RRP balance to close to 0.In other words, the systemic liquidity in the United States will not drop to a level that triggers market panic in the short term.

The U.S. Treasury Department has been accelerating its bond issuance over the past year, but now it seems that this momentum is about to be suspended.Compared with fiscal year 2023, the federal budget deficit narrowed in fiscal year 2024, mainly due to strong revenue growth and basically flat spending.

Therefore, lower debt issuance expectations will be a general benefit to the market for risky assets.

With less than seven months left before the 2024 US presidential election, U.S. fiscal policy may undergo major changes.The Ministry of Finance may sooner or later need to expand the bidding scale again to meet future deficit demand, and the market may also need to adjust.

A small bank that is easy to mess up

After the closing of Friday, media reported that the US Republic First Bank was taken over by the FDIC, but after careful look at the FDIC data, Republic First had about $6 billion in assets and $4 billion in deposits in January. The bank is very small, compared with last year’s violentLei’s Silicon Valley Bank has 200 billion assets, Signature Bank has 110 billion US dollars, and First Republic Bank’s 230 billion assets are incomparable, and it was delisted by the exchange last year.Therefore, it failed to cause the market to “explode” the digital currency in the same way last year.

Fund flow

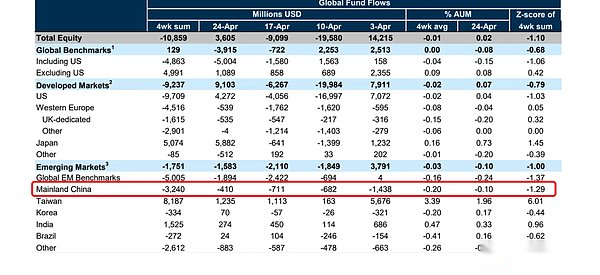

China’s concept funds flow out for seven consecutive weeks under the EPFR caliber, in contrast to the record inflow of northbound funds

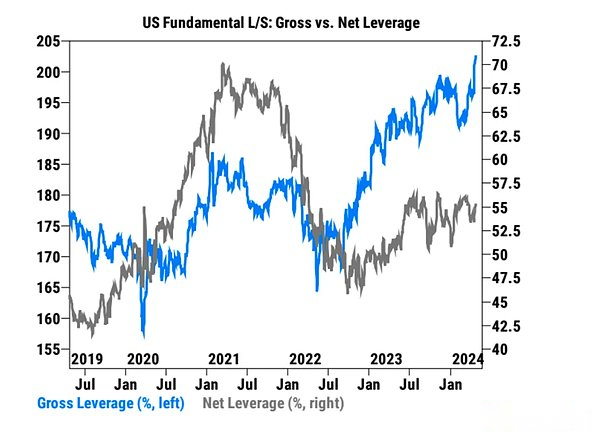

The net exposure of Goldman Sachs fundamental long-short strategy funds rose to 55%, at the 97th quarter in one year, with a total leverage ratio hitting a five-year high.

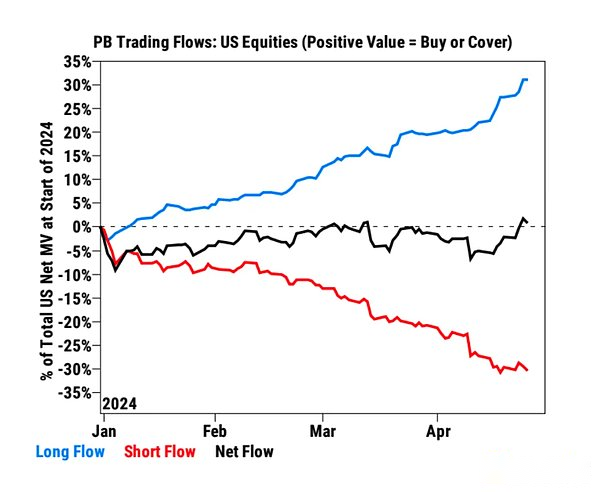

Hedge funds have net purchases of U.S. stocks for the second straight week, the fastest in five months, driven mainly by long buys and short cover (7-to-1 ratio).It is mainly concentrated in the information technology and healthcare industries, and consumer goods, energy, etc. are sold.

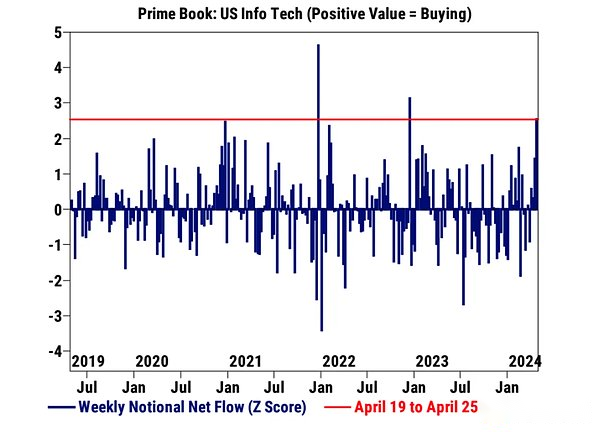

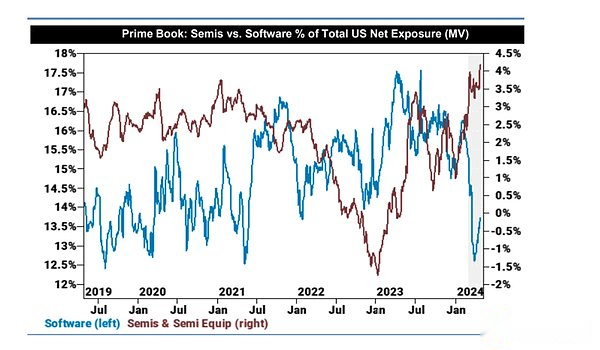

The allocation of funds to semiconductor stocks has reached the highest level in five years.

Goldman Sachs strategists believe that rising inflation and policy risks may put pressure on short-term stock markets.After the interest rate market adjustment is over and inflation data improves, it may be a good time to increase stock bulls.High-quality and non-U.S. stocks may perform better.(As US stock risks accumulate, some funds have begun to allocate high-quality stocks with lower valuations and more stable performance, as well as non-US markets with improved fundamentals to balance portfolio risks. These markets may be in the easing cycle or earlier than the United States.)

Institutional perspective

[JP Morgan Chase: TSMC’s technological breakthroughs, the key engine in the AI era]

JPMorgan Chase rating of TSMC is “upper holdings” with a target price of NT$900.The report highlights TSMC’s leading position in technological innovation and advanced packaging, and its key role in the AI era.Through a series of technological breakthroughs, including the launch of the latest A16 process node, the debut of the advanced packaging technology SoW, and further innovation in silicon photonic technology.TSMC is expected to continue its leading position in the semiconductor industry in the next few years.

[French Xing: Before the yen bottoms, there may be a final and sharp decline]

Kit Juckes, Forex strategist at Societe Generale: The yen has become disordered, indicating that there may be a final sharp decline before the bottoming out.Currently, U.S. yields are rising, while Japanese yields are still supported by very low short-term rates that provide positive returns for shorting yen trading, keeping the leveraged trading community optimistic over the past few months.However, the USD/JPY yield gap will narrow significantly in the next few quarters.If the PPP parity of USD/JPY is now at the mid-90 level, the fair value will still be about 110 even after being adjusted for the US exceptionalism and Japaneseization.

Added: Most institutions believe that the central bank will send hawkish signals by adjusting bond purchases to support the yen.As a result, the Bank of Japan’s resolution last week only said it would maintain its scale in March, and it did not say anything about reducing bond purchases.BOJ seems to have a little bit of abstaining from the exchange rate. Such a dovish move will require the yen to fall further, and in fact it will directly fall below the 158 mark.

Follow this week

In the coming days, investors will turn their attention to the performance of his members.Amazon is scheduled to release its earnings report next Tuesday, Apple will announce it on Thursday, and Nvidia will announce it on May 22.

The U.S. Treasury Department will announce plans for the next quarter of Treasury bond issuance on Monday and Wednesday.After increasing the scale of financing for three consecutive quarters, the market closely monitors this quarter’s financing, buyback plans, and further explanations of the long-term financing strategy provided by Finance Minister Yellen.

However, a series of interesting data may suggest that the U.S. Treasury Department may unexpectedly lower financing expectations – which will squeeze bond shorts.

In addition, attention needs to be paid to the Fed’s policy decision on Wednesday and Chairman Powell’s press conference to assess the possibility of a rate cut in the short term.The market expects that FOMC’s post-meeting statement will not change much, and there will be no new dot map release.

Chairman Powell is not expected to change his current monetary policy stance in the near term.He may reiterate recent comments that recent data have not strengthened his confidence that inflation will fall.Considering that the latest federal funds futures implicit interest rate is expected to cut interest rates for the whole year only 1.3 times/34bps, it is very extreme, if Powell does not give a significantly more hawkish speech, there is more room for yields to fall than the room for upside.

In addition, it is necessary to pay attention to whether the Fed will issue a statement on slowing down the balance sheet to warm up the tape QT, while preparing for the possible sudden tightening of liquidity in the money market and slowing down the recent rapid upward rate of US Treasury bond interest rates.There is a high possibility that the market will rise sharply.