Author: Lianping Source: Wall Street See

Today’s meeting of the Political Bureau of the Central Committee of the Communist Party of China pointed out that moderate and loose monetary policies should be implemented.

In September, Lian Ping, Chief Economist of the Chief Industrial Research Institute and the chairman of the China Chief Economist Forum, issued an article entitled “Suggestion Monetary Policy Tone to” Moderate Loose “.Lian Ping suggested that a more scientific and reasonable definition of monetary policy tone.Adjust the tone of monetary policy to “moderate loosening” to create a suitable policy environment for the implementation of greater efforts and reducing interest rate cuts.

Lian Ping reviewed the practice of my country’s monetary policy in the past 30 years. The central bank only implemented a “moderate loose” monetary policy during the 2009-2010 period.

>

The following is the full text of Lianping’s article:

Since 2011, my country has implemented a “stable” monetary policy tone for 14 years.At present, major changes in the economic situation at home and abroad have undergone major changes, especially in China facing more severe demand, deflation and downward pressure, while US -European monetary policy is fully shifting to relax.In this context, should my country’s monetary policy continue to maintain the “stable” tone?Or should I adjust it in a timely manner to send a more positive and clear policy signal to the market, so that the monetary policy can better play the function of counter -cyclical adjustment?This article will be discussed and put forward views.

1. The flexible adjustment of monetary policy should be the norm

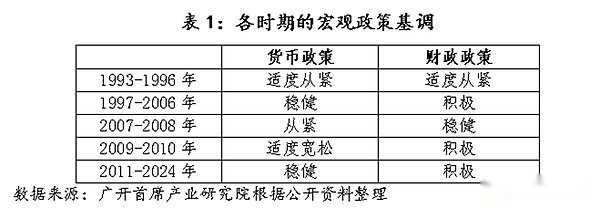

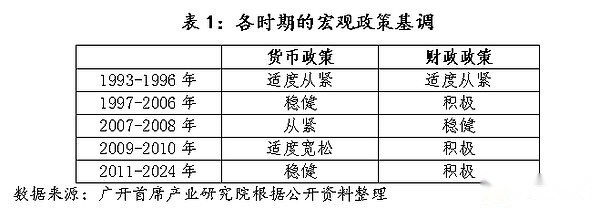

Looking back at the practice of my country’s monetary policy in the past 30 years, the tone of monetary policy is divided into “from tight”, “moderate”, “stable”, “moderate loose” and “loose”.Based on the objective situation of the objective situation, the currency authorities take “stable” as the center, and flexibly adjust between “tightness” and “loose” to achieve the purpose of stable economy and reverse cycle regulation.

In 1993, my country had an overheating and severe inflation phenomenon. The central government adopted a moderate and tight monetary policy. By the end of 1996, the inflation that lasted for three years fell sharply.In 1997, my country faced a situation of lack of domestic demand. The outbreak of the Asian financial crisis brought severe external impact, forming a tightening situation. In order to cope with the pressure of internal and external pressure, the tone of monetary policy shifted from “moderately tightening” to “steady”. Properly increase the amount of currency supply to maintain the stable renminbi value, and use credit leverage to promote expanding domestic demand and increase exports.At the end of 2007, in order to prevent economic growth from changing from fast to overheating, the Central Economic Work Conference set the 2008 monetary policy tone as “tight”.In September 2008, with the bankruptcy of the Lehman Brothers Bank of China, the US subprime mortgage crisis accelerated and upgraded. The Chinese economy was also affected by the financial crisis that had not been encountered for a century.Live until 2010.Since 2011, in order to prevent inflation, prevent asset -proof price bubbles, prevent “hot money” and prevent financial risks, my country has returned to the “stable” monetary policy tone.For about 14 years since then, my country’s monetary policy tone has not changed greatly, but it has a tendency to be loose or tight in actual operation.Among them, the steady monetary policy of 2011-2013 is generally tight, emphasizing the prevention of inflation; the steady monetary policy of 2014-2019 returns to “stable and neutral”, emphasizing not to relax; 2020-2024 steadyThe monetary policy is essentially loose, highlighting the flexibility and accuracy of the monetary policy.

>

Looking back, there are a few points of attention in practice in practice:

First, when the economy is facing a serious impact, the keynote tone of monetary policy will often make directional or large adjustments.From historical experience, under the threat of overheating or inflation, monetary policy tone usually adjusts quickly.For example, the “moderate obedience” in 1993, the “obsession” of 2008, etc.; And in the context of the shrinking impact, the tone of the monetary policy will make adjustments in the direction of pine in time. This adjustment may be a cross -gear, and it alsoIt may be two gear.For example, in 1997, monetary policy tone shifted from “moderate tightness” to “stable”. In 2009, it was “moderate” and “stable” from “tightness” and directly spanned to “moderate loose”.

>

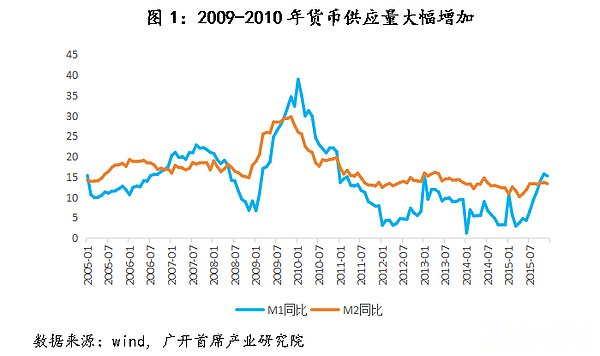

Second, the tone of monetary policy tone sometimes occurs in actual operation.In the five major tones, “tightness”, “moderate tightness”, “steady” and “moderate loose” all appeared in different times, but there was less “loose”.But this does not mean that the “loose” tone is really absent.From 2009 to 2010, my country’s currency credit increased at the rapid growth, especially from the end of 2009 to the beginning of 2010, the year-on-year growth rate of M1 was as high as 38.96%, the M2 growth rate was nearly 30%. ; Matching the high -speed growth of credit, local financing platforms have sprung up, and some areas have even established more than ten financing platforms in the short term.It can be seen that the tone of the monetary policy at that time was far from the nominal “moderate loose”, but the real “loose”.Similarly, “steady” sometimes real meaning is “moderate loose” (such as 1997), and sometimes “moderate compliance” (such as 2011-2013). Often, its expression and preliminary policy tone changes.Starting to grasp its relatively tight changes.

Third, in recent years, monetary policy keys have insufficient elasticity.Prior to 2011, according to the changes in the objective situation and the needs of the target of the objective situation and the needs of the target, the monetary policy tone was switched in a timely manner in timeThe staged obvious changes and fluctuations, but the elasticity of the currency policy tone is obviously insufficient, and the “stable” tone has continued to use for 14 years.In fact, the Chinese economy has experienced a series of fluctuations over the past 14 years.For example, the economic downturn and capital outflows from 2015-2016; the United States launched a trade war in China from 2018-2019; the impact of the epidemic from 2020-2022, and so on.However, the total tone of monetary policy has never changed.This is obviously not conducive to monetary policy to carry out counter -cyclical regulation according to the real economic needs.Of course, the Fed’s monetary policy overflow effect has brought certain restrictions on my country’s monetary policy, but the Fed’s monetary policy has gone through several rounds of major adjustments over the past 14 years.

2. The current monetary policy tone is necessary and conditional to be adjusted to “moderate loose”

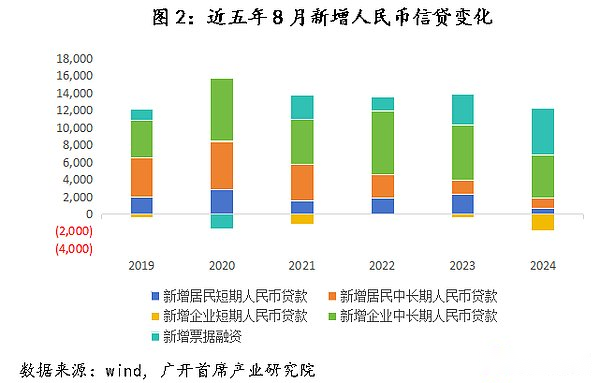

First of all, from the perspective of the domestic environment, the macroeconomic and financial indicators are relatively weak, and the need for further support for monetary policy.In August 2024, my country’s manufacturing procurement manager index (PMI) was 49.1%, a decrease of 0.3 percentage points from the previous month. The manufacturing prosperity continued to fall, and it was lower than the Rongku line for the fourth consecutive month.Since the beginning of this year, the manufacturing PMI has stood on the glory line for a short period of time in March and April, and the remaining 6 months are less than 50%. In 2023, it is only 4 months higher than the Rongku line, less than 50 months in 8 months, less than 50 months.%.In other words, in the past two years, my country’s manufacturing industry is in a state of downturn.From the perspective of financial data, the year -on -year growth rate of broad currency (M2) was 6.3%year -on -year, which was lower than 8%for five consecutive months; the balance of narrow currency (M1) decreased by 7.3%year -on -year.In July, RMB new loans were added only 260 billion yuan. If 558.6 billion notes financing was removed, the actual new loan was negative; although the new RMB increased loan in August rose to 900 billion yuan, it was 12200-from the same period of 2021-2023.Compared with 1360 billion yuan, there is still a small gap.From the perspective of sub -item data, the scale of residents and enterprises has a significant decline in the scale of short -term and medium- and long -term loans, and the factors that cause insufficient demand to cause credit to decline may exceed seasonal factors.In addition, prices, real estate, consumption and other indicators are also in a state of continuous downturn.

>

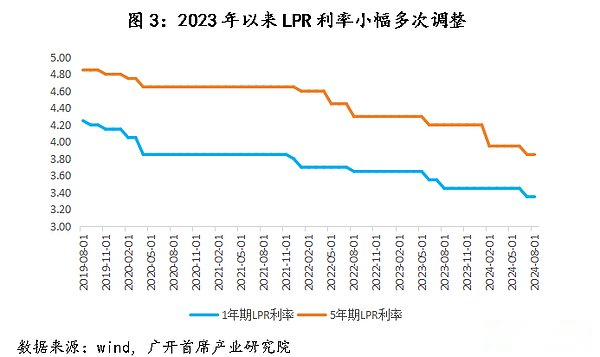

Secondly, there is a significant gap between the current “stable” monetary policy tone and market psychological expectations.Since 2020, even if facing major external impacts such as the new crown epidemic and insufficient domestic demand, the tone of monetary policy is just from the “stable and medium” tone to maintaining a stable monetary policy “flexible and moderate”, “flexible, accurate, reasonable and moderate”, “accurate and effective”, “accurate and effective””The direction of the pine is slightly adjusted, but the overall tone is still” stable “.Since 2023, the central bank has made many adjustments to LPR interest rates. For example10, 25, and 10 basis points were lowered in June, February 2024 and July 2024.Except for 5-year LPR interest rates, in February 2024, from 4.2%to 3.95%, the remaining interest rate cuts were small.Compared with the base point, its symbolic significance is more than practical significance, and there is a significant gap between market expectations. Therefore, it is difficult to have a significant impact on the market slightly.From the perspective of strengthening the expected management and effectively guiding market expectations, making a reasonable and appropriate adjustment of monetary policy tone as soon as possible will help boost market confidence and change the current market expectations of the current market.

>

Thirdly, from the perspective of policy coordination, in order to enhance the effects of adverse cycle regulation, monetary policy must better cooperate with fiscal policies and implement the “double pine” combination.In the process of reverse cycle adjustment, the government usually uses expansion fiscal policies to stimulate overall social needs by measures such as debt, deficit, tax reduction and expansion of government expenditure.However, due to the “crowding effect” of the expansion fiscal policy itself, when government expenditure increases, currency demand will increase accordingly. In the case of currency supply, interest rates will rise, resulting in inhibitory investment in private sector.At this time, it is often necessary to match the expansion monetary policy to suppress interest rates by increasing monetary supply.In recent years, my country’s fiscal policy tone has clearly settled in “positive fiscal policy” and proposed to “take effect” and expand the overall bias.In 2023, the national budget deficit was originally set at 3%. In October 2023, the budget was adjusted, an increase of 1 trillion yuan of high -long national debt, and the final fiscal deficit rate reached 3.8%.In 2024, my country’s budget deficit rate continued to be set to 3%. The amount of local government bonds was 39 trillion, which was further increased from last year. At the same time, it was decided to issue large -scale long -term special government bonds for several consecutive years.While the fiscal policy tone is significantly expanded, monetary policy is bound to give positive cooperation, including increasing liquidity supply and further reduced interest rates.At this time, the tone of monetary policy is necessary to make corresponding adjustments, and it is adjusted from “stable” to a substantial “moderate loose”.

>

Finally, the external environmental change provides a time window for the adjustment of my country’s monetary policy tone.On August 23, the Federal Reserve President Powell gave a speech at the Global Central Bank President Meeting, formally confirming that “the timing of policy adjustment has arrived.”The market generally believes that the Federal Reserve announced in September that interest rate cuts have become a foregone conclusion.We predict that the duration of the Federal Reserve ’s interest rate cut period is 14-16 months, 6-8 times of interest rate cuts, and a cumulative interest rate cut of 150-200 basis points.It is undeniable that in recent years, under the circumstances of the decline in economic downlink and the continuous increase in shrinkage pressure, my country’s monetary policy tone has not been adjusted. The important reason is that the high interest rate policy implemented by the Federal Reserve has the constraints on my country’s economic and financial.At present, the Fed’s new round of interest rate cuts have been arrowed on the string.In this context, my country’s monetary policy tone has obtained a rare adjustment time window, which has room for promoting a new round of reduction and interest rate cuts.

>

The “moderate loose” monetary policy tone is introduced between “stable” and “loose”, and the implementation of three positive significance in the current situation: First, the tone of the “stable” monetary policy tone is more aggressive.The use space, price, and structural monetary policy tools are used to inject sufficient liquidity into the market, and the actual interest rate is significantly lower.Second, compared to the “loose” monetary policy tone is relatively cautious.Due to the relatively moderate looseness, it can avoid sequelae and other sequelae of “large water drilling” and severe inflation.Third, compared with the current tone of monetary policy named “steady” but actually loose, its greatest positive significance is that it can send a clearer and clear policy signal to the market, so that all parties to the market can better understand the policies with policies.Loose intentions and actively expect consistency on subsequent policies to enhance their confidence in good economic recovery.Since the restriction rate reduction and structural tools have frequently adjusted in the direction of loosening in recent years, and in the future, the direction of continuing to continue to adjust the cycle will not be changed. So why can’t we make a “stable” tone in a timely manner to the “moderate loose” tone?Judging from all aspects, the monetary policy conditions that are currently implemented in the true “moderate easing” tone have matured.

3. Related policy recommendations

Suggestions 1: Make a more scientific and reasonable definition of monetary policy tone.Policy makers should comprehensively sort out and standardize the system tone system and related definitions of monetary policy, especially the boundaries between “loose” and “moderate loose”, “tight” and “moderate tightness”, and explain that under different policy tones, under different policy tones, under the tone of different policy,What specific changes will occur in monetary policy goals and operation tools, how to refine the trigger conditions of the entry and exit of various policy tones, and how to match the tone of monetary policy and fiscal policy.

Suggestions 2: Further strengthen the expected management and pass clear monetary policy signals to the market.While the establishment of the monetary policy tone system is established, it is recommended that the monetary authorities suggest that the policy tone that is more rigorous and accurate and better reflects the current demand, so that all parties to the market can better understand the orientation of monetary policy and form positive feedback with the same frequency resonance.As the central bank leaders have pointed out, “when the transparency of monetary policy is increased, the understanding and authority of the policy will be enhanced.”

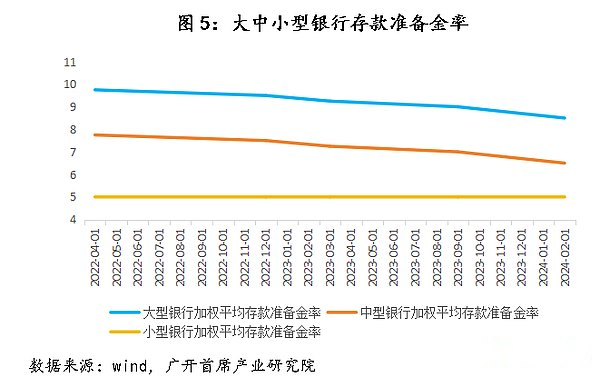

Suggestions 3: Adjust the tone of monetary policy to “moderate loose” to create a suitable policy environment for the implementation of greater efforts and reducing interest rate cuts.Judging from the possibility of downgrading, the weighted average deposit reserve rate of small banks in my country is currently as low as 5.0%, and the space is relatively small in the short term, but it does not mean that it cannot be further reduced; the weighted average deposit reserve ratio of medium -sized banks cannot be reduced. It is 6.5%, and the weighted average deposit reserve rate of large banks is 8.5%.For example, the implementation of a new round of rangers for monetary authorities can consider the targeted downside of large state -owned commercial banks and national joint -stock commercial banks.Given that the deposit of relevant banking institutions in my country’s banking industry accounts for 60 %, if its targeted reduction is 0.5 percentage points, it is expected to release the liquidity of more than 600 billion yuan to the market.In view of the current domestic actual interest rate is still high, it is necessary to further cut interest rates.It is recommended to concentrate policy resources, and a large increase in interest rate cuts around 50 base points will be implemented at the end of this year or early next year.At the same time, considering the structural monetary policy tools, carbon emission reduction support tools, inclusive micro -loan support tools, and inclusive pension special re -loan will expire at the end of this year.The tools are further added to the new quota and lowered 0.5 percentage points of supporting agricultural re -loans, small re -loans and re -discount rates to facilitate cooperation with green finance, inclusive finance, and pension finance.