Author: Frank

The market plunge on October 11 not only broke through the price defense line of crypto assets, but also triggered a “tens of billions migration” on the stablecoin track.

Data shows that since October, the total market value of stablecoins has shrunk from US$308.7 billion to US$302.8 billion, and nearly US$6 billion of funds have left the market.In this ebb, the leading compliant stablecoin USDC was the first to bear the brunt, and its supply on the Solana chain fell off a cliff.USDe, the “rising star” that had been in the limelight before, also saw a sharp decline in issuance due to the liquidation of revolving loan leverage.

However, this is not a simple capital flight, but a cruel competition.When we get rid of the fog of data, we will find that this is a change from “speculation” to “rationality”. Funds are flowing from highly leveraged on-chain gaming fields to safe havens with stronger compliance, smoother legal currency channels, and real RWA returns.

Solana Ecosystem and USDC’s “Double Spiral”

In this wave of shrinking market value, USDC has become the biggest “blood loss point”.Data shows that USDC accounted for half of the nearly 6 billion US dollars flowing out, and its total market value fell from 76.3 billion US dollars to 73.5 billion US dollars, a drop of 2.8 billion US dollars.

Behind the decline of USDC, the main reason is that the USDC issuance of the Solana chain has dropped by 18.24% in the past month. On October 11, the total amount of USDC issued on the Solana chain was approximately 12.8 billion US dollars. By November 23, it dropped to 8.7 billion US dollars, and the total amount decreased by 4.1 billion.

During the same period, TVL on the Solana chain also dropped from $12.9 billion to $8.79 billion, a decrease similar to the supply of USDC.Solana’s top-ranked DeFi protocol also experienced a significant decline in TVL during this stage.From this perspective, after the market plunge on October 11, a large number of funds on the Solana chain chose to redeem stablecoins directly to avoid market risks.

Take Pump.fun as an example. According to monitoring by on-chain analyst Ember, in the past week, the Pump.fun project team transferred 405 million USDC to Kraken.Then during the same period, 466 million USDC were transferred from Kraken to Circle, which was probably a withdrawal.These are the funds Pump.fun received from selling PUMP to institutions in a private placement in June.However, Sapijiju, co-founder of Pump.fun, responded: “This is completely untrue news. Pump.fun has never cashed out.” He also said that this was just a step in fund management.

Not just Solana, Hyperliquid, known for its highly leveraged derivatives trading, also suffered a drop in liquidity, with its stablecoin issuance falling by 25% from $6 billion to $4.4 billion.This all-round contraction has directly impacted the performance of the publisher Circle in the US stock market.Affected by the double blow of poor revenue expectations and a sharp decline in USDC supply, Circle’s stock price fell from a high of $240 all the way below the issue price to $71.3. The once highly anticipated myth of “compliant stablecoin unicorn” seems to be suffering its first crisis after listing.

USDe Crisis and Sui’s Stablecoin Data Mistake

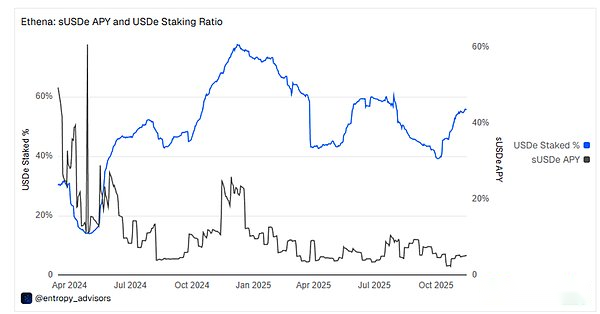

If the decline of USDC is a cyclical deleveraging, then the crisis of USDe has exposed the structural vulnerability of algorithmic stablecoins in a bear market.

Since October 10, the supply of USDe has halved from US$14.6 billion to US$7.38 billion, and the price on Binance once detached to US$0.65 due to a lack of short-term liquidity.The main reason for the de-anchoring was the collective withdrawal of liquidity providers from centralized exchanges during the panic, resulting in extremely thin order books.At the same time, although USDe’s official redemption mechanism operates normally, there is a delay of several hours in the “off-exchange settlement” behind it.This delay makes it impossible for arbitrageurs to quickly arbitrage within a few minutes of the flash crash, thus unable to bring the discount on CEX back to the $1 anchor, amplifying the magnitude of the de-anchoring.

As for the reason for the sudden drop in issuance, it is actually because the market crash caused the perpetual contract funding rate to plummet and even turn negative. This caused the “revolving loan” leverage strategy that had been widely deployed on lending platforms such as Aave and Morpho to lose its economic foundation.With yields lower than borrowing costs, traders were forced to deleverage and close positions on a large scale, triggering a shrinking supply of USDe.Afterwards, OKX CEO Star posted on the X platform: “USDe should not be regarded as a stable currency anchored 1:1 with the US dollar. It is a tokenized hedge fund.”

Even though Ethena set a record of $151 million in fee capture in Q3 this year, it was still unable to withstand the loss of market confidence caused by the sharp drop in yields.Although the current yield of USDe has risen to above 5%, the overall supply and trading volume are in decline.

When the market is extremely anxious and eager to find the next growth point, a data oolong about the Sui public chain has become an episode.On November 24, Artemis data showed that the stablecoin supply on the Sui chain increased by $2.4 billion.Social media believes that this may be some institutions or smart money actively deploying certain assets of Sui Chain.Even Sui officials participated in the interaction with this news and replied: “stablesmaxxing” (stablecoins are full).

However, after investigation, it was found that this may just be an own incident. After careful comparison of multiple data panels, USDC is indeed the most issued stable currency on Sui, with the current issuance market value of approximately US$480 million.The issuance volume of other stablecoins on Sui is tens of millions of dollars.According to data from Defillama, the current total amount of stablecoins in the Sui ecosystem is approximately US$653 million.If US$2.5 billion flows in or is issued in a single day, it means that the supply of stablecoins on Sui will increase by about 4 times.

The information on the chain also shows that the issuance of USDC in Sui is 482 million US dollars, and the address with the largest holdings is approximately 148 million on the Binance exchange.Subsequently, Artemis also updated this data, and the stablecoin supply on Sui in the past seven days increased by US$117 million.

A new direction for risk aversion, embracing gains

When funds are withdrawn from high-risk areas, they do not disappear completely, but flow to safer and more functional assets.

During the market decline, USDT once again proved its dominance as the “big brother” of the stable currency. Not only was the total market value unaffected, but it repeatedly broke new highs reaching $184.7 billion.

Compared with the decline of USDC, other compliant stablecoins have experienced significant growth. Since the market plummeted on October 11, the issuance volume of PYUSD has bucked the trend and increased from US$2.5 billion to US$3.6 billion, an increase of nearly 50%.Among the public chain segments, the growth of PYUSD mainly comes from the growth of the Ethereum mainnet, which has increased by 57% in the past month.

Data released by Token Terminal on November 9 showed that PYUSD has become one of the fastest-growing tokenized assets with a market value of more than US$1 billion.Compared with other stablecoins, the core advantage of PYUSD may lie in its convenient fiat currency exchange channel and relatively stable rate of return.PYUSD has previously maintained more than 10% APY on the Solana chain by subsidizing earnings.In addition, the compliance of PYUSD is also one of the key considerations for many institutional investors.

In addition, the issuance of USYC, an income-based stablecoin also issued by Circle, has also achieved a 45% increase in the past month, with the total issuance increasing by approximately US$500 million.This shows that during periods of market turmoil, institutional investors are no longer satisfied with holding zero-interest cash and are unwilling to take on the high risks of DeFi. Instead, they prefer the stable returns of anchoring RWAs such as U.S. bonds.

Data from RWA.xyz also shows that the recent issuance of RWA assets has not been affected by the market decline and is still growing steadily.It grew to $36 billion from $33 billion on October 11, an increase of 10%.

A market turmoil has become a touchstone for the stablecoin market at this moment.Not only does it allow the market to distinguish which stablecoins are mainly used in high-leverage transactions, but which ones are used as financial management targets for large institutions.At the same time, it also reflects that the encryption market has officially bid farewell to the “reckless era” of relying solely on on-chain leverage to drive scale.

On the other hand, PYUSD’s breakout against the trend and the steady growth of RWA assets prove that funds have begun to vote with their feet.In turbulent times, more convenient fiat currency channels, more transparent compliance endorsements, and real returns based on U.S. debt are the core competitiveness for retaining funds.

The outflow of US$6 billion may give us an opportunity to think. The second half of the stablecoin war is no longer a competition of money printing speed, but a competition of scenarios, trust and underlying asset quality.For issuers, how to evolve from a “fuel” serving on-chain speculation to a “bridge” in finance and trade will be the only ticket to the next bull market.