Author: danny; Source: X, @agintender

Boros creates a capital-efficient on-chain derivatives market for perpetual contract funding rates.By “tokenizing” the capital rates of off-chain exchanges into tradable “yield Units, YUs”, a market that is functionally similar to Interest Rate Swaps (IRS) in traditional finance was essentially built – a trading category that “bets” for Maosan Wang durian fruit farmers.

The agreement not only provides traders with new tools to hedge and speculate on capital rate fluctuations, but also provides a critical risk management infrastructure for Delta neutral strategy protocols such as Ethena that rely on capital rate.

In the short term, the better Ethena develops, the greater the trading volume of Boros.

1. The rise of on-chain interest rate derivatives

1.1 Perpetual Contract Fund Rate: A Crypto-Native Interest Rate Benchmark

A perpetual contract is different from a traditional futures contract, and it has no expiration date.In order to keep its price anchored to the spot price of the underlying asset, a core mechanism of capital fee rate was introduced.Funding rates are the fees for regular exchanges between long and short positions.

Its economic significance lies in that the capital rate not only reflects market sentiment and leverage demand, but also reflects the difference in capital cost between the base currency and the denominated currency.Positive rates (long pay shorts) usually indicate strong bullish sentiment in the market or strong leverage demand; negative rates (short pay longs) are the opposite.The perpetual contract market processes hundreds of billions of dollars in transaction volume every day, making the capital rate a huge source of returns and risks that could not be traded directly before, creating a broad market space for derivatives agreements built around it.

1.2 Similarities and similarities with traditional interest rate swap (IRS)

Interest rate swap (IRS) is a derivatives contract where both parties agree to exchange a series of interest payment streams based on a nominal principal for a period of time, usually one party pays a fixed interest rate and the other party pays a floating interest rate.The global interest rate swap market is huge, with daily clearance exceeding US$1.2 trillion.

The Boros protocol implements a functionally similar fixed-change floating protocol.Users can choose to pay a fixed interest rate (i.e., an implicit annualized rate of return) in exchange for a floating interest rate (i.e., a basic annualized rate of return from a centralized exchange) and vice versa.

However, there are key differences between the two:

-

Bottom interest rate: Traditional IRS usually use benchmark interest rates such as SOFR or ESTR.Boros uses perpetual contract funding rates.

-

Infrastructure: Traditional IRS is an over-the-counter trading (OTC) market, usually intermediary by banks and increasingly cleared by central counterparties (CCPs).Boros builds an order book on the chain.

-

Opponent risk: In traditional finance, counterparty risk is a major issue, which is mitigated through legal agreements and collateral.In Boros, counterparty risks are managed algorithmically through an on-chain mortgage, margin and liquidation system.

1.3 Boros Introduction: Pendle enters leveraged income trading

Boros expanded “earnings trading” to “funding rate” and introduced margin and leverage mechanisms.

For many years, traders have been able to passively bear the capital rate as a transaction cost or source of income, and cannot trade it as an independent risk factor.Hedging operations are indirect and inefficient.Boros has achieved direct transactions on capital rate risks for the first time by providing a direct, capital-efficient tool (YU) and trading venue (on-chain order book).This is similar to the birth of Credit Default Swap (CDS) in financial history, which allows banks to separate credit risks from underlying loans for transactions.Boros is doing the same for the crypto world’s funding rate risk.

The most core and most powerful application scenario at this stage is to provide institutional-level hedging tools for Delta neutral strategies like Ethena that manages billions of dollars of assets.Whether Ethena can provide stable fixed income for its stablecoin USDe may depend in part on its ability to hedge capital rate risks on Boros.

1.4 An analogy: Maosan King Durian Futures Market

To better understand Boros’ core philosophy, we can compare it to a hypothetical “Maoshanwang durian futures market”.

Imagine there is a Maoshanwang durian tree.This tree represents a base asset that generates profits, just like the perpetual contract market on Binance.

-

Future durian harvest: How many durians will be produced in the future and their quality are uncertain.This uncertain future harvest is like the future generation of the perpetual contract marketFunding rate.Sometimes the harvest is good (the capital rate is positive and high), and sometimes the harvest is different (the capital rate is negative).

-

Durian futures contract: Fruit farmers and fruit vendors hope to lock in future durian prices in advance to hedge the uncertainty of harvest.So they created a market that specializes in the contract for “durian delivered on a specific date in the future.”This contract is equivalent to the Boros agreementIncome Unit (YU).

-

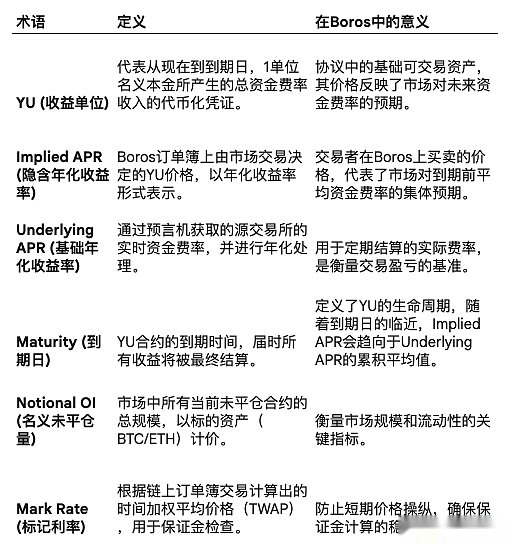

Prices in the futures market: In this market, durian futures contracts have a price formed by bidding between buyers and sellers.This price reflects the market’s collective expectations for future durian harvests.This price is in BorosImplicit annualized rate of return (Implied APR).

-

Actual harvest value: When the durian is ripe and picked, its actual value in the spot market will be determined.This ultimate, real value is theUnderlying APR.

In this analogy, the Boros Agreement plays the role of this durian futures market.It does not trade the durian tree itself (i.e., does not trade BTC or ETH spot), but provides people with a platform to specifically trade expectations of the “fruits” (fund rate) produced by this “tree” (perpetual contract market).Traders can buy and sell expectations of future capital rates on Boros, just as fruit merchants buy and sell expectations of future durian harvests, thus achieving speculation or hedging.

2. Architecture in-depth analysis: the operating mechanism of the Boros protocol

This chapter will disassemble Boros’ technical components in detail, explaining how it converts an abstract off-chain rate into a financial instrument that can be traded on-chain.

2.1 Tokenization of off-chain income: connecting CEX rates with on-chain assets

Boros relies on oracles to import real-time fund rate data from data sources such as Binance/Hyperliquidi.This is a key centralized node and a potential manipulation vector, and the protocol addresses this problem through specific risk parameters.

The ingenious design of Boros is that it allows users to trade changes or spreads between market expectations and actual rates, rather than the rates themselves.This turns it into a powerful forecasting market.

2.2 Income Unit (YU): Basic Trading Tool

Yield Unit (YU) is the basic trading instrument in Boros, representing the total capital rate income that can be generated from a nominal principal (such as 1 BTC or 1 ETH) from the current to the expiration date of the contract.

Conceptually, Boros’ YU is similar to the earnings tokens (YTs) of Pendle V2, as they both represent the tokenized future earnings stream.However, unlike V2, Boros does not have a corresponding principal token (PT), which makes it a pure return-directional trading tool.Trading YU allows users to speculate or hedge the volatility of capital rates without taking direct price risks to the underlying assets (such as BTC or ETH).

2.3 Rate duality: Deconstructing implicit APR and basic APR

The core dynamics of Boros transactions stem from the interaction between two rates:

-

Implicit annualized rate of return (Implied APR): This is the YU price determined by market transactions on the Boros order book, representing the market’s collective expectations of the average capital rate before maturity.Traders are actually long or shorting this implicit interest rate.

-

Underlying APR: This is the annualized real-time funding rate obtained by the oracle from the source exchange.It is the basis for regular settlement of positions.

The profitability of a position depends on the difference between the Underlying APR at settlement and the Implied APR at the time of entry by traders (in plain words: you bet on Implied apr):

Do long YU: If Underlying APR > Implied APR, then profitable.

Short selling YU: If Underlying APR < Implied APR, then profitable.

2.4 Transaction infrastructure: on-chain order book and settlement engine

Boros uses a fully-winded public order book for peer-to-peer transactions at YU.This design provides transparency, but also presents challenges related to Gas costs and potential jump-start deals.At the same time, the agreement also has an automatic market maker (AMM) to provide basic liquidity.

The settlement process (also known as Rebase) is performed regularly according to the funding rate cycle of the source exchange (e.g. Binance is every 8 hours).At each settlement, the system calculates profit and loss (i.e. the difference between Underlying APR and Implied APR) and directly adjusts the user’s collateral balance.

The existence of this periodic settlement mechanism and arbitrage opportunity ensures that as the expiration date approaches, the Implied APR will naturally converge to the cumulative average of the Underlying APR.This is because the shorter the remaining time, the less uncertainty of future rates will be.

2.5 Capital Management: Cross-margin and Clearing System

Boros supports leveraged trading (the initial cap is 1.2 times, but it can support higher leverage by design), and provides independent and cross margin account models.Its margin system is designed to achieve capital efficiency, matching collateral requirements with expected payment risks (i.e. spread fluctuations) rather than being tied to full nominal exposure.

For margin checks, position value is determined by Mark Rate, a time-weighted average price (TWAP) derived from on-chain order book transactions.This is a key defense mechanism against short-term price manipulation.If the margin level of the account is below the maintenance margin requirement, the account will face liquidation to prevent bad debts from accumulating.

Boros’ architecture creates an ecosystem that is self-referential but is anchored by externally.The transaction price (Implied APR) is determined endogenously by participants on the Boros Order Book.However, the value and profit and loss of the system are ultimately settled based on an exogenous, objective (oracle) data source.This binary structure of internal pricing and external anchoring is the core engine of the protocol.The 8-hour settlement mechanism plays the role of “reality testing”, and forces speculative prices to reconcile with off-chain actual fees.

3. Application and Market Trends

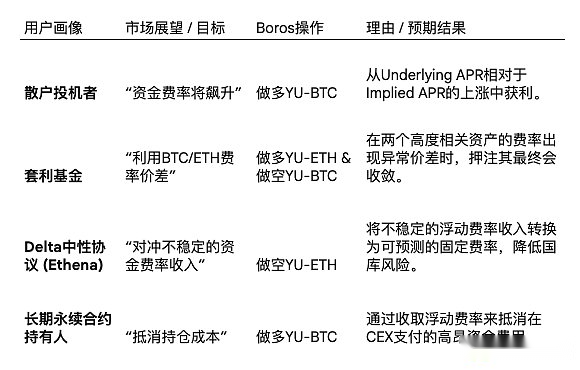

3.1 Boros Trading Strategy Framework 3.1 Boros Trading Strategy Framework

In addition to the strategies in the table above, traders can also use the cyclical rules of capital rates (such as low weekend rates)Cyclic trading, or when the rate deviates from the historical averageMean regression trading.In addition, before major market events (such as regulatory decisions) occur,Event-driven transactionsIt is also a common strategy.

3.2 Institutional Utility: Ethena Case Study and Delta Neutral Hedging

Agreements such as Ethena create benefits for its stablecoins (USDe) by holding spot ETH/BTC and shorting the equivalent perpetual contract position.Its main source of income is the rate of funds obtained as short holders.However, this part of the revenue is extremely unstable; once the capital rate turns negative, Ethena will face significant losses.

Boros provides a solution for this.By shorting YU on Boros, Ethena can pay for (unstable) floating Underlying APR while charging (predictable) fixed Implied APR.This effectively converts its unstable revenue stream into fixed, predictable revenue, allowing it to reduce treasury risks and even provide fixed income products to its users.This hedging capability is crucial for any entity that runs “spot-futures arbitrage” or basis transactions, including miners, pledgers and arbitrage funds, allowing them to lock in costs or revenues and improve operational stability.

3.3 Evaluation of capital efficiency claims

Boros claims to provide extremely high capital efficiency, allowing users to hedge large-scale nominal positions with a small amount of collateral (up to 1,000 times as mentioned in the official publicity).This efficiency stems from its margin model.In Boros, margin is calculated based on potential fluctuations in interest rate payments, rather than based on the full nominal value of the underlying position.

However, theoretically 1000 times efficiency is an extreme marketing figure.Actual leverage ratio and capital efficiency are strictly limited by agreement risk parameters, margin requirements and initial leverage caps (e.g., 1.2 times the initial stage of the online launch).True capital efficiency is dynamic and depends on market volatility.

4. Thinking

The emergence of Boros creates a “meta game” and new one on the existing perpetual contract market.It allows traders not only to speculate on asset prices, but also to counter (investment) the behavior and sentiment of other traders in the underlying perpetual contract market – capital rates.

Because the capital fee rate is the direct result of the imbalanced game of long and short positions on CEX.So trading YU on Boros is actually a leveraged bet on the positions and sentiment of traders in markets like Binance or Hyperliquid.A trader who is long in YU is essentially the leverage long demand on Binance will increase/decrease.This adds a new dimension of complexity and opportunity, turning the market structure and trader psychology itself into a directly tradeable asset.

Interestingly, the existence of a sound capital rate hedging market may in turn suppress the volatility it relies on.Extreme capital rates are often caused by crowded unilateral transactions.Large participants often dare not increase their positions due to their high holding costs (capital rates).With Boros, a large trader can now leverage long on CEX (which pushes up positive rates) while doing long on Boros YU to hedge this cost.This reduces the negative incentive to participate in crowded transactions.As Boros liquidity deepens, it may play a stable role like the mature IRS market in traditional finance stabilizing lending rates, compressing the extreme peaks and valleys of capital rates, or pushing crowded transactions to the other extreme?