Author: Magicdhz, Blockworks; Compilation: Baishui, Bitchain Vision

summary

-

The Lido protocol is managed by Lido DAO and is an open source middleware that routes ETH, stETH, and Ethereum rewards between a set of validators and ETH stakers.

-

stETH is the most liquid LST and the most widely used form of on-chain collateral.

-

stETH liquidity and stETH as collateral are also growing on CEX, indicating an institution’s interest in trading and holding stETH as an alternative to ETH.

-

stETH is staked in a powerful validator collection with lower risk and offers higher probability adjustment rewards.

-

Since TradFi seeks staking ETH rewards, this may mean developing a “tradfiETH” product, stETH can serve as a coordination tool against centralization.

Introduction: stETH > tradfiETH (ETF)

On May 20, 2024, Eric Balchunas and James Seyffart changed the odds of spot ETH ETF approval from 25% to 75%.ETH rose by about 20% in a few hours.However, at the request of the SEC, the issuer modified the S-1 registration statement to cancel the ETF’s pledge reward.Therefore, investors holding spot ETH ETFs will not receive a staking reward from Ethereum, which may be due to the regulatory clarity required to provide staking ETH products.Anyway, at current interest rates, investors who choose to obtain spot ETH ETFs will lose consensus and an APR of about 3-4% of the execution layer rewards.Therefore, to alleviate dilution, there is an incentive to add pledges to ETF products.

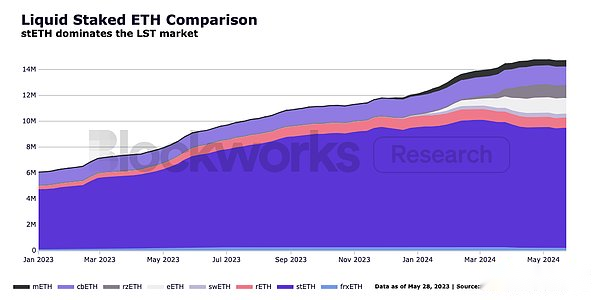

The Lido protocol is an open source middleware that automatically routes ETH in pools between validator sets according to delegate standards.Lido DAO is managed by an LDO holder and is responsible for managing some of the parameters of the above delegation standards, such as protocol fees and node operators and security requirements.However, the protocol is unmanaged and DAO cannot directly control the underlying validator.stETH, which accounts for approximately 29% of the total network equity (9.3 million ETH, or $35.8 billion), is a key infrastructure for the staking industry, maintaining high standards in performance, delegation and other staking practices.

ETH ETFs may be the most convenient option for TradFi investors to obtain ETH exposure at the moment, but these products cannot capture Ethereum’s issuance or crypto-economic activity.As more and more TradFi venues themselves join tokens, holding Lido’s liquid staking token stETH is arguably the best product to get exposure to ETH and Ethereum staking rewards, as it hasKey utility:

-

stETH is the most liquid and trading ETH pledged asset among decentralized exchanges (DEXes).

-

stETH is the most widely used form of collateral in DeFi, surpassing the largest stablecoins USDC and ETH itself.

-

stETH is the most liquid reward-based native L1 asset in centralized exchanges (CEXes)—both a replacement for spot ETH trading and a form of collateral.

With the advent of ETH ETFs, investors learn more about Ethereum and seek to get additional returns from consensus and execution layer rewards, stETH dominance may continue – which is beneficial for consolidating a stronger stETH market structure.Good wind.Going forward, Lido DAO governance and growth in stETH are essential to maintaining a sufficiently decentralized set of validators on Ethereum as TradFi institutions eventually add staking to their products (called “tradfiETH”).

Therefore, “stETH > tradfiETH” is because it provides better returns, releases more utility than adjacent products, and acts as a coordination tool for the fight against centralization.

Source: FINMA, Taurus

Lido protocol

The middleware of the Lido protocol is a set of smart contracts that programmatically assign users’ ETH to a group of censored Ethereum validators.This liquidity staking protocol (LSP) is designed to enhance Ethereum’s native staking capabilities.It mainly serves two parties: node operators and ETH stakers, and solves two problems: the threshold for entry of validators, and the loss of liquidity caused by locking ETH for staking.

Although the hardware requirements for running a validator on Ethereum are not as high as other chains, in order to reach a consensus, node operators need to stake exactly 32 ETH in the validator to get the reward of Ethereum.Raising so much money is not only not easy for potential validators, but allocating ETH within the limit of the 32 ETH interval can be very inefficient.

To simplify operations, Lido routes ETH from investors and delegates these ETHs to the validator set, effectively lowering the high economic threshold.In addition, Lido DAO reduces the risk of validator sets through rigorous evaluation, monitoring, and delegated strategies across node operators.Operator statistics and metrics containing data from the validator set are available inHereturn up.

In return for their ETH deposit, investors will receive stETH, and their value proposition is simple.Running a validator or staking ETH requires locking ETH in your account – instead, stETH is a liquid utility token that users can use in CeFi and DeFi.

stETH

stETH is a liquid staking token (LST), a practical token that represents the total amount of ETH deposited in Lido plus the staking reward (minus fees) and validator penalty.Fees include staking commissions collected from validators, DAOs and agreements.

When the user deposits an ETH into Lido, a stETH is cast and sent to the user, and the protocol records the user’s share of ETH in the protocol.This share is calculated daily.stETH is a receipt that the user can redeemed as a share of ETH in the pool.By holding stETH, users can automatically receive Ethereum rewards through a rebase mechanism—essentially, when the ETH rewards accumulate to the validator set, the protocol mints and allocates stETH based on the ETH share of the account in the protocol.

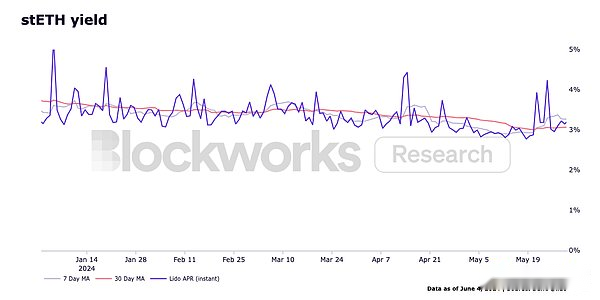

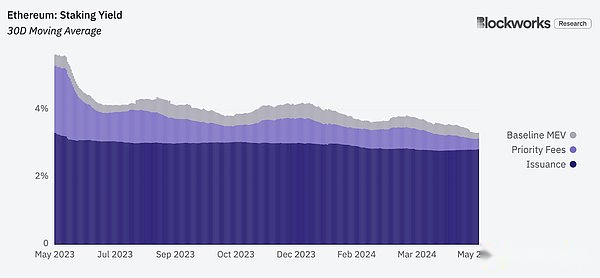

The rewards of stETH depend on ETH circulation, priority fees, and MEV rewards.ETH issuance is the reward for validators to participate in consensus and correctly propose blocks.Currently, the issuance rate is 917,000 ETH per year (and a change in this monetary policy is being discussed).Users pay a priority fee to prioritize transaction inclusion.MEV rewards are an additional source of revenue for running MEV-Boost, which facilitates the market for validators to earn some block rewards on Ethereum.This part of the reward depends on the demand for Ethereum block space.According to mevboost.pics, in 2023, validators achieved approximately 308,649 ETH through MEV-Boost ($704.3 million at the ETH price as of January 1, 2024).With these factors in mind, investors can earn a variable annual interest rate of 3-4% for the full year of 2024 by simply holding stETH.

All in all, unlike spot ETH ETFs, stETH is a liquid product through which investors can own ETH assets and earn cash flow from Ethereum.In addition, stETH is also one of the most used assets in various environments in DeFi.

stETH utility

The main utility of stETH makes it an ideal asset, which includes liquidity and the ability to use it as collateral.Typically, it takes several days to withdraw the pledged ETH because the time the pledger must wait depends on the size of the exit queue.This increases the likelihood of a maturity mismatch, in which case the value of ETH changes dramatically between withdrawal requests and redemptions.

The core value proposition of stETH is its liquidity.Stakers do not have to wait to exit the queue, they simply exit their pledged position by selling stETH on the market for DEX or CEX.Savvy readers will realize that eliminating the risk of maturity mismatch will shift the risk to the secondary market’s willingness and ability to accept stETH inventory.That being said, given the approval of spot ETH ETFs and the properties and underlying market structure trends of stETH, there are greater precedents that predict further adoption of stETH and deeper liquidity.

stETH liquidity

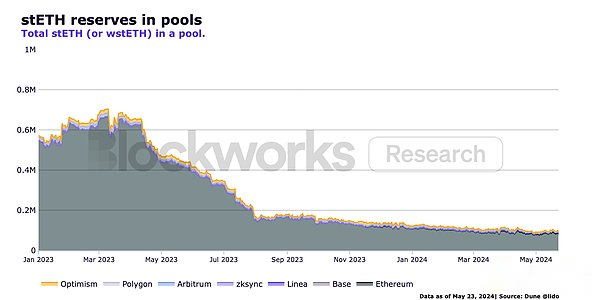

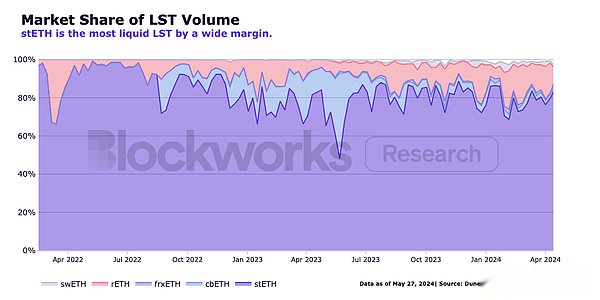

It is worth noting that the stETH reserves in Ethereum and rollup pools were declining throughout 2023.This is due to the DAO eased incentive spending on on-chain stETH LPs, which meant that LPs had withdrawn their reserves from the pool.In 2024, reserves will reach a stable level.From subsidized LPs (who are usually more inclined to withdraw reserves when they need it most) to a genuine, non-subsidized stETH LP, it is much healthier for the on-chain liquidity profile of stETH.Despite these market adjustment forces, stETH remains one of the most liquid assets in DeFi and ranks in the top 10 in Uniswap’s TVL.

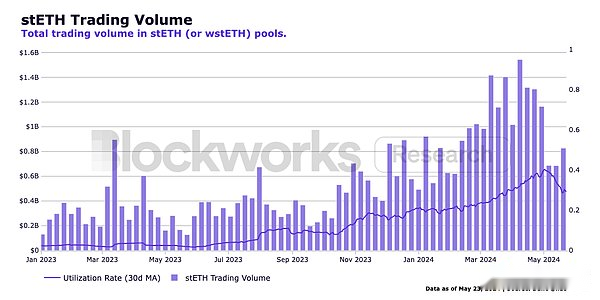

During the same period, both the transaction volume of stETH and the usage of stETH in these pools increased.The trends in the figure below show that: (1) LP has higher viscosity and consistency, (2) the market is close to a more stable balance of stETH liquidity, and (3) more and more participants are more willing to trade stETH.These market structures are a stronger and more organic basis for expansion than overinvesting LDO incentives on seasonal LP.As shown in the figure below, stETH is far ahead in trading volume and liquidity compared to other LSTs.

Liquidity is really important (ICYMI)

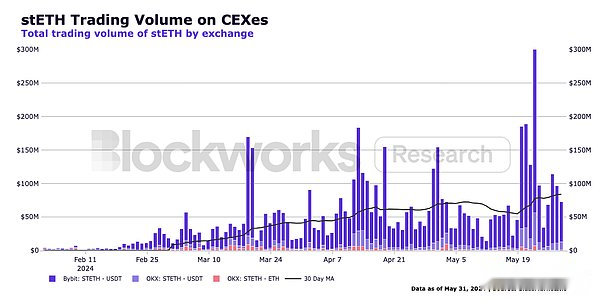

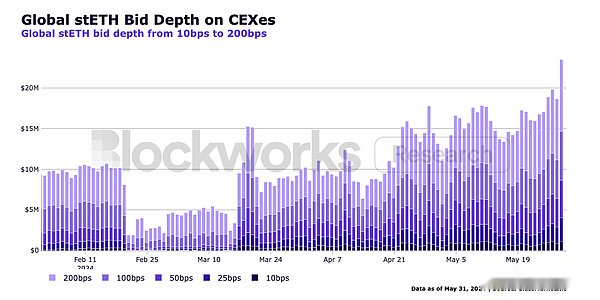

Liquidity can be said to be the biggest determinant of risk management in financial markets.The liquidity status of an asset greatly affects its risk-adjusted returns, which in turn affects its attractiveness to investors.This makes stETH the best choice for investors and traders looking to receive Ethereum rewards, as confirmed at a seminar between Blockworks with large crypto-native institutions including Hashnote, Copper, Deribit and Cumberland.The following figure shows the trends adopted by crypto native institutions on CEX: More crypto native institutions and market makers are more willing to hold and trade stETH.Note: Global bid data were incomplete during parts of February and March because the exchange changed the exchange rate limits for order data.

stETH as collateral

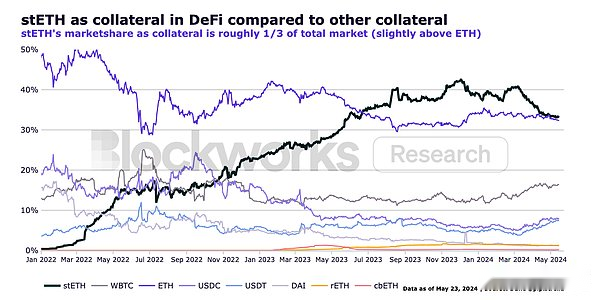

stETH is also the preferred form of collateral in DeFi – it surpasses ETH and popular stablecoins such as USDC, USDT and DAI.The figure below shows that since its establishment, it has gradually climbed to this position, accounting for about 1/3 of the total market share.

Using stETH as a premium collateral option can improve its capital efficiency and may help exchanges and lending platforms generate more transaction volume.In February this year, ByBit announced that it would increase the collateral value of stETH from 75% to 90%.Since then, stETH trading volume on ByBit has increased nearly 10 times.

It seems that the on-chain market structure of stETH has reached a more stable balance, which may lay a solid foundation for the long-term gradual growth trend.Off-chain, we can observe sparks adopted by more institutions, as investors will prefer to stake ETH over regular ETH.While we also expect other LSTs (possibly including LRTs) to gain market share, stETH’s existing market structure and dominance, as well as its first-mover advantage, should maintain its strong position in the market.In addition, Lido and stETH have many advantages over other staking options.Compared with other staking mechanisms, Lido’s mechanism has three key features: non-managed, decentralized, and transparent.

stETH compared to other stakes

Compared with other staking mechanisms, Lido’s mechanism has three key features: non-managed, decentralized, and transparent.

-

Unmanaged:Neither Lido nor node operators escrow users’ deposits.This feature mitigates counterparty risk – node operators will never host user-staked ETH.

-

Decentralization:There is no organizational verification protocol—technical risks are evenly distributed among a group of node operators, thereby improving resilience, uptime and rewards.

-

Open Source:Anyone can review, audit and/or recommend improvements to the code that runs the protocol.

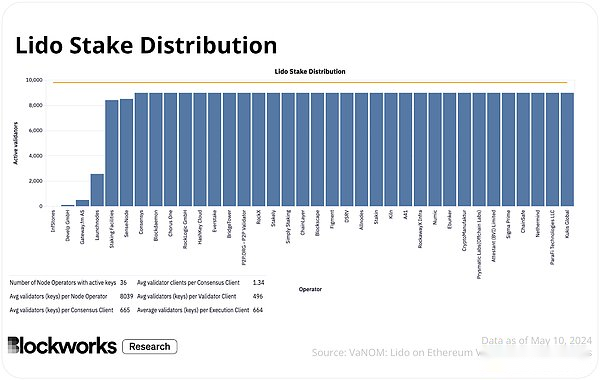

When comparing stETH with other LSTs and staking providers, based on Rated data, the reward difference between top node operators is small, ranging from 3.3-3.5%.However, taking into account the factors of operating nodes (including devops, cloud infrastructure, hardware, maintenance code, client type, geographic distribution, etc.), a small difference in rewards contains a great risk.

stETH is less risky because it ensures access to a different set of operators running different machines, code, and clients in different locations on many teams.Therefore, the possibility of downtime is lower, and the risks are diversified by default; while other staking providers have more concentrated operations and more potential central failure points.For more information on the field, Blockworks Research analyst 0xpibblez wrote an in-depthResearch Report.

stETH probability of receiving excess reward

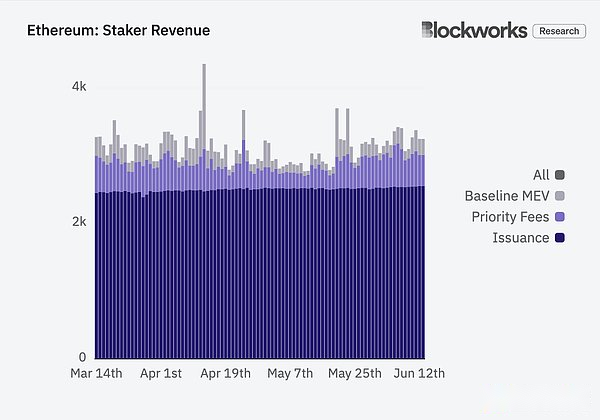

Referring to the first graph below, we can observe that the execution layer reward (priority fee + baseline MEV) is more variable than the consensus layer reward (issuance).The second image below shows a magnified view of this change over the past month.This is due to the periodicity of on-chain activities, that is, in some periods, the increase in activity levels coincides with more valuable blocks, so the execution layer reward is higher; while the consensus layer reward is constant.This means that the implemented staking ETH reward is a function of the probability of the validator proposing the next block, capturing the changes in the execution layer reward.

Since stETH stakes are in the hands of many different operators, accounting for 29% of the total staked ETH, the probability of stETH capturing changes in block rewards is much higher than that of a single validator, smaller operator, or less staked validator set.This means it continues to produce higher returns on average.

In other words, at an extreme, when a separate validator proposes a very valuable block, even if the total return is much higher (e.g., staking 32 ETH to earn 10 ETH in a block), thisThe chances of this happening are also very low, about one in a million (32/32,400,000).They will basically win the lottery.At the other extreme, Lido’s validator set is more likely to capture valuable blocks, about 29% of the time.Therefore, by holding stETH, users can choose and increase their chances of sharing more rewards.

In short, another reason stETH is a better choice to get a staking ETH reward is that it produces highly competitive rewards based on probability and risk adjustments.

Lido Governance: stETH’s growing importance to decentralization

The approval of the spot ETH ETF brings expectations for more products—most notably pledged ETH products.During the bull market cycle, the native legend of cryptocurrency DegenSpartan wrote an article titledHow many Trojan horses can we launch?》Articles.In this short blog post, DegenSpartan wrote: “After spot ETFs, more access can still be expected in terms of [TradFi]. Options, funds included in funds, mutual funds, retirement accounts, DCA plans,Structured products, dual currencies, Lombardy loans, etc. ”

While U.S. capital markets will have more opportunities to reach ETH, bringing more permanent (structural) tailwinds, it is unclear how TradFi will integrate other digital assets or derivatives and what side effects they may have on decentralization.

tradfiETH and stETH

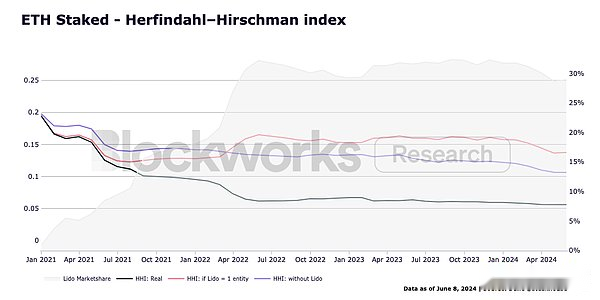

Philosophically, we think LST is the best way to maintain a sufficiently decentralized, secure and well-performed validator set.Grandjean et al. calculated the HHI of Ethereum (an indicator used to assess market concentration and competition) and found that Lido has improved the degree of decentralization (lower HHI readings shown in the figure below).

Although considering Lido as an entity results in higher HHI (i.e., less decentralized networks), we do not believe that this description of Lido accurately reflects Lido’s existence in the market, because the protocol is not made by aAn organization or entity managed or controlled by a validator set consists of a variety of different independent entities.While large LSPs are at risk, implementing appropriate governance mechanisms and protocol oversight (e.g. dual governance) should reduce the severity of the risk.In addition, the addition of DVT is expected to further decentralize operators.

That being said, it is reasonable for TradFi to eventually launch a pledged ETH product, given the economic incentives for pledged ETH (or holding native ETH will dilute its equity).Here are some possible (pure) hypotheses results: (1) TradFi explicitly adopts stETH and all its advantages; (2) TradFi works closely with Coinbase or other large institutional staking providers to build this framework, in which case,cbETH or tradfiETH will become the standardized staking ETH products of TradFi; or (3) TradFi develops its own practices, invests in proprietary node operations, hosts its own staking ETH, and issues tradfiETH products.

“While this is good for BTC [and ETH], the next direction is an unknown area.” — DegenSpartan

We believe, and there is evidence that hypothesis (1) is a better solution for the network, because in either case, if the staking ETH tends to tradfiETH, then the chain is at risk of staking centralization.Therefore, in a state where existing enterprises with strong capital develop centralized pledged products, as long as Lido remains sufficiently decentralized, stETH and DAO are important components in maintaining Ethereum consistency, and more broadly, because DAO manages stETHdelegate, and in turn have a significant impact on the performance, security and decentralization of the network.

risk

-

Volatility and liquidity:When ETH volatility soars, investors will be more willing to sell stETH in the open market than to wait in the withdrawal queue.In the case of insufficient liquidity, the occurrence of high volatility periods and high selling volumes may cause the price of stETH to deviate from its 1:1 ETH price linkage, which will bring subsequent risks until market conditions recover.

-

Circular risk:A popular way to earn rewards (such as farming for airdrop or liquidity mining incentives), users take leveraged positions, lend stETH, borrow ETH, buy stETH, lend extra stETH, and repeat the loop until theyMake full use of the leverage ratio to achieve maximum capacity.During periods of volatility, cyclers face the risk of being liquidated, which may trigger amplified risks associated with volatility and liquidity.

-

Agreement and Governance:There are risks associated with LSP occupying a large market share.The agreement delegated by stETH is managed by DAO.While DAO is taking steps to achieve dual governance, which will reduce these risks, if stETH accounts for the majority of staking ETH, then there is reason to worry that ETH staking will be concentrated in LDO governance.

-

Smart Contract:The Lido protocol is executed by a set of smart contracts.This includes deposits, withdrawals, entrusted pledges, cuts and key management.Unforeseen errors or malicious escalations associated with smart contracts exist in these systems.

-

Competitors:The LST market is huge and other re-staking agreements are entering the field.TradFi is also able to develop its own pledged products, which may be easier to obtain for some investors given the current market structure.

-

Supervision:While spot ETH ETF approvals may make staking providers more secure on average, staking ETH will remain under regulatory scrutiny.Public legal discussions include, but are not limited to, the role of a staking provider, the difference between “management” and “administrative” (according to the Howie Test), and whether the LSP is a “issuer” (Reve test).

Summarize

By today’s standards, stETH is arguably the best product to get a pledged ETH exposure.It is the most liquid LST on the chain; it is the most widely used form of collateral in DeFi; these market structures are expanding rapidly off-chain, and the continuous growth of transaction volume on CEX is proof (the most notable are ByBit and OKX).While there are risks in holding stETH, these powerful market structures may continue to exist, and may even surge, given the properties of stETH, Lido’s protocol, the growing need to align with Ethereum, and the upcoming catalyst.These catalysts on the roadmap include distributed validator technology (DVT), dual governance, support for pre-confirmation and allocating additional resources for restaking stETH, and improved governance structures that contribute to Ethereum research.More importantly, if TradFi develops staking ETH products, stETH and Lido DAO will play an increasingly important role in Ethereum.