Source: Web3 Xiaolu

Recently, Binance Research released a research report on Web3 payment, which well sorted out the current situation of traditional payments and blockchain Web3 payments, and looked forward to the future of Web3 payment by combining the advantages brought by blockchain.The research report system is complete and the arguments are sufficient, which is worth learning from.

What inspired me the most is that the author Joshua Wong, based on the background of a macro analyst, can place Web3 payment more in the entire huge traditional financial payment system rather than being trapped in a pure pursuit chain.The obsession with technology.

Therefore, this article compiled the research report of Binance Research and studied its index article in depth. Only through the comparison of cold data can we better clarify our own positioning and gaps, as well as the direction of our future path.

Below, Enjoy:

Blockchain Payments:

A Fresh Start

1. Report core points

Although the payments industry is one of the largest and fastest growing industries in the world, it still relies primarily on outdated, 50-year-old banking infrastructure.Modern payment fintechs and card organization networks such as Stripe, Mastercard and Visa bring a more convenient end-user experience to consumers and merchants.However, the traditional costs involving up to six intermediaries (e.g. card organizations, issuers, processors, POS systems, payment aggregations, digital wallets) in each transaction remain.Blockchain technology provides a whole new global infrastructure track for payments, and this is a new beginning.

Blockchain and its range of innovative applications it supports have the potential to significantly reduce the cost of cross-border payments and improve its efficiency.This has been achieved at the institutional level, with participants such as Visa running pilots to enable settlement of institutional-level global payments on public blockchains.It is also being adopted at the individual level, and products like Binance Pay are being used in faster and cheaper ways for peer-to-peer payments and cross-border transfers, as well as direct use of cryptocurrencies at merchants, without paying Gas fees, and automatically adjusting currency exchanges.and real-time settlement.

The payments industry is huge, which means that adopting revolutionary technologies such as blockchain may be slow and cautious.This also gives the blockchain industry itself the necessary time to grow and build the necessary payment tools and payment infrastructure.

2. Background introduction

The use of cash for face-to-face payment methods gives the currency a unique sense of freedom.Unfortunately, modern digital payment systems simply cannot provide this ability to directly transaction without third-party intervention.This is mainly because we need a third party to custody funds for us, which is different from blockchain technology that can achieve self-custody of funds.

Worse, the modern global payment infrastructure stack still relies on banks and other intermediaries to handle any transaction.Today’s payment technology stack is in desperate need of a fresh start, and blockchain technology can do that.

When the guy named Satoshi Nakamoto launched Bitcoin in 2009, it was conceived as a revolutionary form of peer-to-peer electronic cash payment.The goal is to create a decentralized currency that provides the same freedom as in-person cash transactions, but for digital payments.It does this by facilitating direct transactions between individuals without the need for financial intermediaries such as banks.This vision promises to usher in a new era of financial freedom, transparency and lower transaction costs.

Since its inception in 2009, the modern crypto industry has undergone significant changes.The emergence of stablecoins has introduced a stable value yardstick that can be used as a medium for value exchange and payment, while taking advantage of blockchain technology to eliminate the problem of asset fluctuations.In addition, the development of Layer 1 and Layer2 solutions has increased transaction speed and reduced costs, effectively reducing the previous bottlenecks that have hindered the adoption of distributed ledgers as a bottleneck for handling large-scale payment transactions.

This report will outline the current traditional payment landscape and its key issues.Then, it will be discussed how blockchain technology solves these problems, the current status of blockchain payments, and how the payment industry can make progress through blockchain.

3. Current status of traditional payment industry

When global payment systems such as SWIFT were first created in the 1970s, achieving global remittances was a groundbreaking achievement and an important milestone in the financial sector.

However, today’s global payment infrastructure can only be described as outdated, simulated and fragmented.It is a costly and inefficient system that operates within limited banking hours and relies on numerous intermediaries.The modern financial system relies on many banks around the world, and each bank maintains its own books.The lack of unified global standards among these banks hinders seamless international transactions and complicates building consistent cooperation.

The shortcomings of modern payment systems make cross-border interbank transactions expensive and inefficient, as a single transaction may require multiple proxy banks to reach its intended destination.Sometimes it is more like a black box, where the sender and receiver cannot track the flow of funds and can only wait in the dark.

According to the World Bank, cross-border remittances usually take up to five business days to settle, with an average fee of 6.25% of the transaction amount.Despite these obvious challenges, the business-to-business (“B2B”) cross-border payment market is huge and continues to expand.In 2023, the total market size of B2B cross-border payments is US$39 trillion and is expected to grow 43% by 2030 to US$53 trillion.

3.1 Current traditional payment industry structure

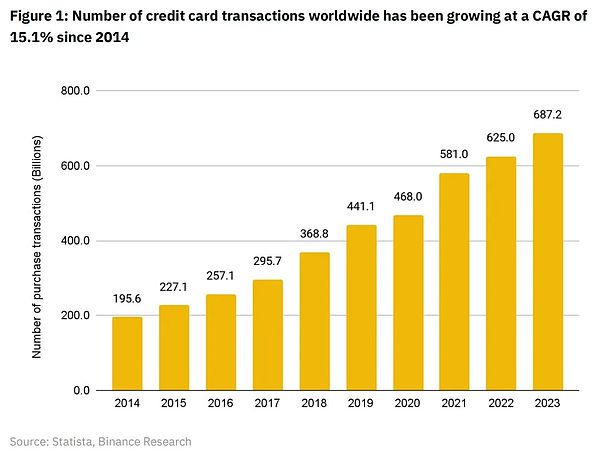

The payments industry does not seem to be affected by inefficiency, but has grown into one of the world’s largest industries, with revenues currently estimated to reach $2.83 trillion by 2024.It is also one of the fastest growing industries, with a projected $4.7 trillion by 2029, with a compound annual growth rate (CAGR) of 10.8%.The global payment funding scale reached approximately US$150 trillion in 2022, an increase of 13% over 2021.

The situation is similar in terms of the growth in the number of purchase transactions for global card organization brands (American Express, Discover, JCB, Mastercard, Visa and UnionPay) over the past nine years.Purchase transactions have been growing steadily since 2014, with a CAGR of about 15.1%.

Although the payments industry is one of the largest and fastest growing industries in the world, most of its business is still using the technology track from 50 years ago.The global payment landscape has evolved into a rent collection agency group filled with numerous middlemen who stand between merchants and consumers and collect rent from each transaction.

Over the past five years, innovation in the payment fintech field has created miracles for merchants and consumers’ experiences.However, this cannot protect them from the high costs caused by the inefficiency of traditional systems, and even the most advanced fintech solutions still rely on these traditional payment systems.

Broadly speaking, there are two types of payment systems in the modern payment industry: open-loop payment system and closed-loop payment system.

3.2 Open Loop Payments

Card organizations like Visa and Mastercard support open payment infrastructure around the world.They enable numerous acquiring banks and issuing banks from around the world to access the card organization network and allow funds to flow from one bank to another through clearing and settlement of the card organization network.

Card organization networks are priceless innovations that enable fast communication between banks around the world.This is an extremely consumer-friendly system that allows the use of a Visa/Mastercard to pay for goods and services around the world.Therefore, they have become the main means of digital payment in today’s world.Visa and Mastercard are two of the most valuable publicly traded companies in the world today, ranking 18th and 20th respectively.

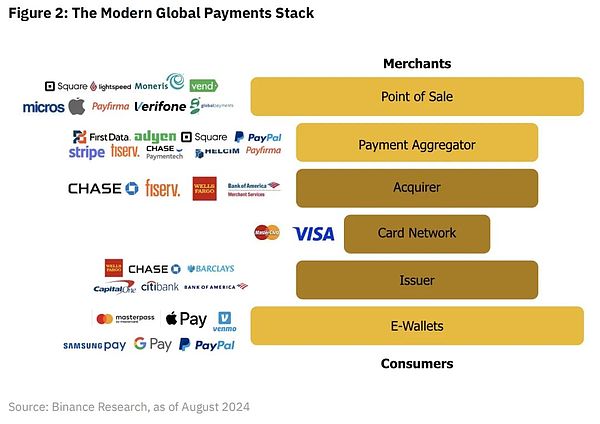

In a typical open-loop payment system supported by card organization networks such as Visa and Mastercard, there are up to 6 middlemen between merchants and consumers.

1. POS service is a physical or digital terminal that initiates transactions.It captures payment details and sends them for processing.For example, Square is one of the most important POS service providers, which charges merchants 2.6% + $0.10 per transaction.The fee is then allocated to the remaining four intermediaries in the payment stack that charge rent (e-wallets like Apple Pay and Google Pay currently do not charge any per-transaction fee).

2. Payment Aggregators integrate transactions from multiple merchants and simplifies the process of receiving payments.They provide a single point of integration for a variety of payment methods.Most payment aggregators such as Stripe also screen transactions to detect fraud to protect their merchant customers.

3. Acquirers are financial institutions that handle credit or debit card payments on behalf of merchants.It ensures that the transaction is authorized and transfers funds from the issuing agency to the merchant’s account.

4. Card Networks promote the transmission of transaction information between the acquiring agency and the issuing agency.They set the rules and standards for card transactions.

5. Card Issuers are banks or financial institutions that provide credit or debit cards to cardholders.It authorizes transactions and deducts from the cardholder’s account.Credit card networks such as Visa and Mastercard also monitor transactions to detect fraud, thus protecting their banking customers.

6. E-Wallets are digital wallets that store payment information and facilitate online and in-store transactions.They provide users with a convenient way to pay without using a credit card directly.

In short, blockchain can serve as an alternative, global, decentralized payment network—a new open system that is free from the current global payment system and slow and expensive traditional banks that are full of middlemen.The constraints of the system.

3.3 Close Loop Payments

Closed-loop payments is a growing trend in the payments industry, promoted by companies such as PayPal and Starbucks.

In the closed payment loop, consumers only interact with the PayPal application because various merchants are stored by PayPal and are able to accept payments through the PayPal network.As far as Starbucks is concerned, customers can only use funds stored in Starbucks digital wallets in their stores.More and more merchants are beginning to follow Starbucks and implement their own closed payment loop.The main purpose of this is to deepen customer stickiness by running your own loyalty program and bypass the high fees imposed by existing open payment stacks.

However, the closed payment loop currently exists is a highly decentralized system that remains closely linked to slow and expensive traditional banking systems.To transfer funds to and from Starbucks closed loop, users still need a bank account.In addition, closed-loop systems dedicated to many merchants (such as Starbucks) do not allow transfers between customers and cannot be used seamlessly in many countries around the world.Blockchain technology provides an alternative to future payment fintechs, allowing them to choose to completely avoid traditional, decentralized banking systems, ultimately reducing fees for merchants and consumers.

Binance Pay is an example of this kind of payment fintech.It supports instant, low-cost point-to-point transfers and direct merchant payments within closed-loop payment systems.As a closed-loop model, the latest generation of fintechs like Binance Pay can provide merchants and consumers with a familiar, sophisticated and customizable fintech experience, facilitating the transition from traditional banking tracks to blockchain tracks.

3.4 New options for cross-border payments

When cross-border transactions and remittances are involved, the cost increases exponentially.According to the International Monetary Fund, workers or immigration remittances mean that “immigrants send part of their income back to the country in the form of cash or goods to support their families.”This is a specific area of cross-border payments, and blockchain technology can have a direct impact on it.

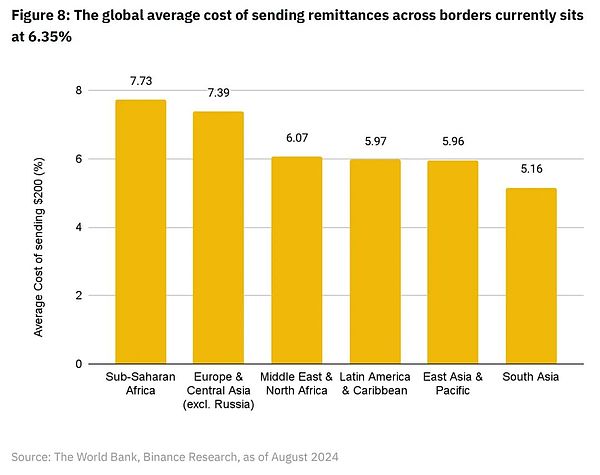

It is estimated that global remittance funds increased by 1.6% from $843 billion in 2022 to $857 billion in 2023.Growth is expected to reach 3% in 2024.In 2023, in current US dollars, the top five low- and middle-income countries receiving remittance inflows are India (US$120 billion), Mexico (US$66 billion), China (US$50 billion), Philippines (US$39 billion) and Pakistan($27 billion).According to World Bank data as of the first quarter of 2024, the average cost of remittances of $200 worldwide is still 6.35% of the amount of transfers, with a total annual fee charged at $54 billion.

Due to the extremely high costs, cross-border remittances are a key area of the payments industry, and blockchain can truly make a huge impact.

Cross-border remittances involve cross-border remittances through a range of banks located in different countries, and the entire process can take several days, so it is slow and expensive.

1) The process begins when the remitter initiates the remittance at the local bank or remittance service, where the remitter provides the recipient’s details and the amount to be remitted.

2) Because the remitter and the payee’s bank may not have a direct relationship, an intermediary bank (called an agent bank) facilitates transactions.The remitter’s bank sends the funds to its agent bank, which may transfer the funds to other agent banks, and each agent bank charges a fee.In this process, the SWIFT network is often used to send such payment instructions.

3) If different currencies are involved, funds are usually exchanged at one of the agent banks, and the exchange rate is usually lower.

4) Every bank must comply with anti-money laundering (AML) and understanding customer (KYC) regulations, verify identity and ensure the legality of the transaction.Transactions are also screened based on the international sanctions list.

5) After processing and completing the compliance inspection, the funds will be transferred to the recipient’s bank, and the bank will record the funds to the recipient’s account.The sender will receive a confirmation that the transaction is completed.

The above-mentioned traditional payment system is not only costly and inefficient, but also cannot cover a considerable portion of the world’s population at present.

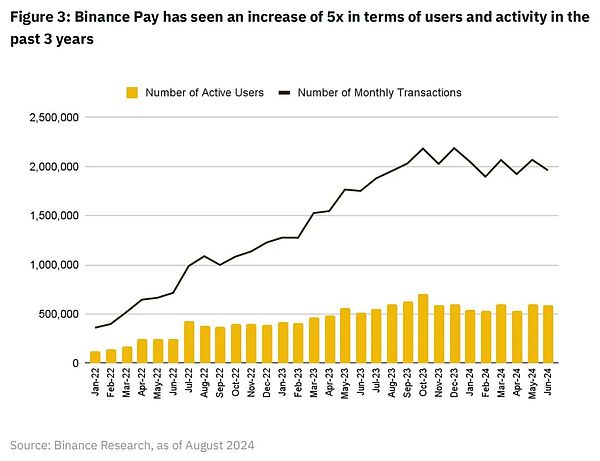

Today, as many as 1.4 billion adults worldwide do not have bank accounts.For these reasons, we have seen users around the world switch to blockchain solutions such as Binance Pay as a cheaper and faster way to transfer money across borders.Since 2022, Binance Pay’s monthly active users and monthly transactions have increased by nearly 5 times, with the global number of users being about 13.5 million and the monthly transactions being about 1.96 million.

Blockchain and distributed ledger technology (DLT) have the potential to disrupt many existing players in the payment industry as it provides a unified, global, transparent payment environment that can be accessed with just a smartphone and internet connection..This means there will be a more direct communication channel between merchants and consumers, driven by distributed ledgers and eliminate the need for agency banks.Liberating future fintech from traditional banking systems may be the key to achieving cheaper and faster payments worldwide.”Ultimately, we want to achieve the ability to settle any payments in any currency anytime, anywhere, and this may require the use of blockchain technology,” said Jason Clinton, head of sales at JPMorgan European Financial Institutions Group.

Four,Current status of blockchain-based payment

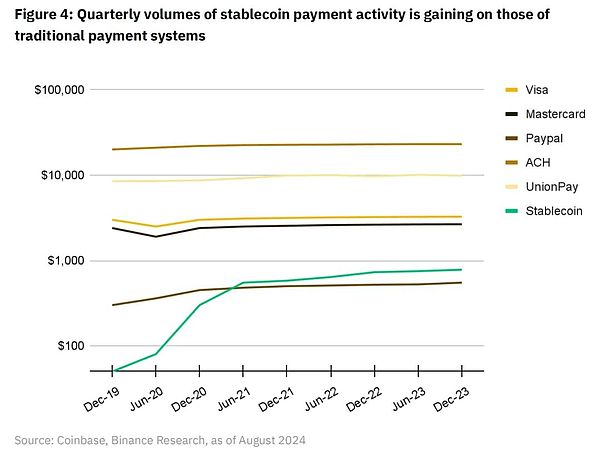

Because of its high cash equivalence, stablecoins have become a key component of blockchain payments.In 2023, stablecoins processed transactions of more than $10.8 trillion, excluding activities such as machines or automatic trading, which is $2.3 trillion.

Comparing stablecoin payments with traditional payments, we can see that they have been catching up with traditional payments in terms of quarterly transaction volume.

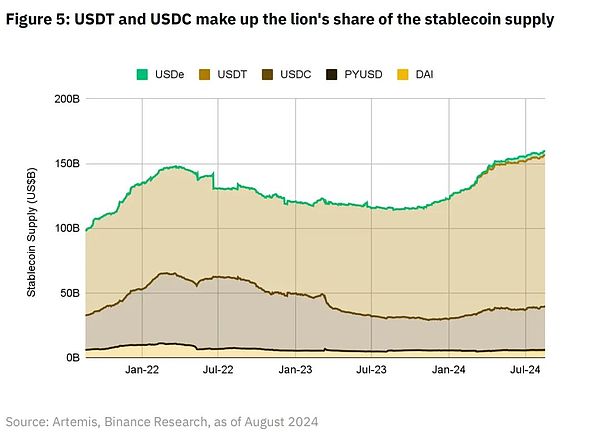

The total supply of stablecoins has also been increasing since mid-2023, indicating a steady increase in demand.The total market value of major stablecoins exceeds US$160 billion, with USDT and USDC accounting for the largest share, with market share of 73% and 21% respectively.

Taking advantage of the low volatility provided by stablecoins, the blockchain payment ecosystem and its associated infrastructure have made great progress since 2009.

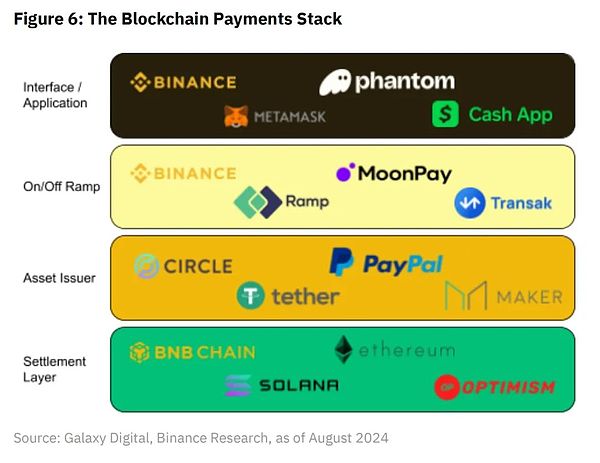

4.1 Infrastructure based on blockchain payments

Settlement layer(Settlement Layer)

Blockchain infrastructure responsible for transaction settlement, such as Bitcoin, Ethereum, and Solana, are all Layer1 blockchains, as well as multi-functional Layer2 solutions such as Optimism and Arbitrum, which are essentially in the sales block space.

These platforms compete in various aspects such as speed, cost, scalability, security and distribution.Over time, payment use cases may become important consumers of the block space.

We can imagine the settlement layer as a banking network that constitutes the current traditional payment system.Instead of storing funds in centrally managed bank accounts, consumers and merchants can store assets in either an on-chain external-owned account (EOA) or smart contract account.

It is worth noting that in modern payment stacks, authorization and settlement are processed separately.Visa and Mastercard’s card organizations provide payment authorization services; card issuing banks and acquiring banks are responsible for handling actual payment settlements.For blockchain, authorization and settlement can theoretically be synchronized.Consumers can send a 100 USDT transaction directly from their EOA to the merchant’s EOA by signing a transaction authorization, and the validator will immutably process and settle the transaction on the blockchain.

It is worth noting, however, that relying solely on blockchain for settlement and authorization of P2P payment transactions may mean bypassing clearing, transaction monitoring and fraud detection service systems used by payment aggregators such as Stripe and credit card networks such as Visa.

Visa itself has been the leader in piloting blockchain for payment use cases over the past few years, and the company envisions the future “Visa’s network involves not only multiple currencies and bank settlement channels, but also multiple blockchain networks, stablecoins and CBDC or tokenized deposits.”

Asset Issuer Layer(Asset Issuer)

An asset issuer is the organization responsible for creating, managing, and redeeming stablecoins—a stablecoin that is a crypto asset designed to maintain stable value relative to a reference asset or a basket of assets (most often in the US dollar).These issuers often adopt a balance sheet-driven business model similar to banks.They accept customer deposits, invest these funds in higher-yield assets such as U.S. Treasuries, and issue stablecoins as liabilities to profit from interest spreads or net interest spreads.

Asset issuers are a new type of “intermediary” that exists in crypto payment stacks, and there is no direct equivalent in traditional payment stacks.Perhaps the closest equivalent is the government that issues fiat currency used to conduct transactions.

Unlike intermediaries in traditional payments, asset issuers do not charge fees from every transaction using their stablecoins.Once the stablecoin is issued on-chain, it can be self-custodial and transferred without paying any additional fees to the asset issuer.

On/Off Ramp Layer

The acceptance of deposits and exits is crucial to improve the availability and adoption of stablecoins in financial transactions.Fundamentally, they act as a technical bridge connecting stablecoins on the blockchain with fiat systems and bank accounts.Their business model is usually traffic-driven, accounting for only a small percentage of the total dollar transaction volume through their platform.

Currently, the upper/downhill layer is usually the most expensive part of the crypto payment stack.Service providers such as Moonpay charge up to 1.5% to transfer assets from blockchain to bank accounts.

The transaction from fiat currency held by consumer banks to on-chain stablecoins and then to fiat currency held by merchant banks, which may cost up to 3%.In terms of cost, this aspect may be the biggest barrier to widespread adoption of blockchain payments, especially for merchants and consumers who may still need fiat currencies in bank accounts for daily transactions.To solve this problem, products such as Binance Pay are building their own merchant network where users can use cryptocurrencies directly without the user’s cost.

Interface/application layer(Interface/Application Layer)

Front-end applications are customer-facing software in the crypto payment ecosystem that provides a user interface for crypto-enabled transactions and leverage other components of the stack to facilitate these payments.Their business model usually includes platform fees and transaction-based fees, earning revenue based on the transaction volume processed through its interface.

4.2 Take advantage of blockchain-based payment

Nearly instant settlement

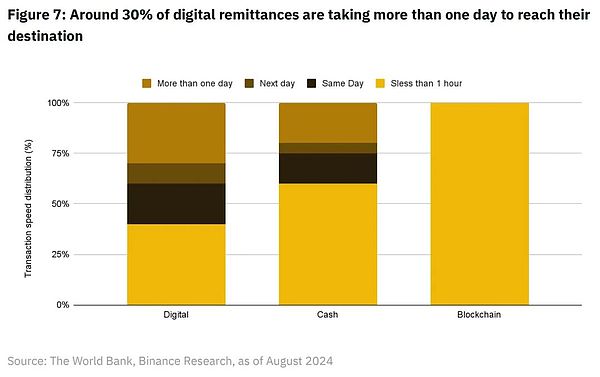

When trading with a Visa or Mastercard card, consumers can experience the convenience of near-instant payment authorization.However, the actual settlement of the transaction, where funds are transferred from the client’s bank account (issuing bank) to the merchant’s bank account (acquisition bank), usually takes at least one day to happen.While card organizations allow consumers to make digital payments in seconds, merchants usually don’t receive funds for the purchase until the next day or later.When funds need to be transferred across borders, the settlement time will be longer because this requires communication between banks in different countries.

Judging from the remittance transaction time, the inefficiency of the cross-border interbank communication system is obvious.It’s a bit counterintuitive that about 30% of remittances take more than a day to reach their destination; this is higher than 20% of cash remittances required for the same time.

The World Bank attributes this to two reasons:

(1) Remittances cover traditional banking services, i.e. bank account to bank account services, which are slower.

(2) Most non-bank remittance service providers may provide funds for transactions in advance, providing fast services to end users using cash.

For example, among the three payment media (digital, cash and blockchain), blockchain is significantly ahead in speed, with 100% of transactions being completed in less than an hour.

In 2021, Visa conducted a pilot with Crypto.com to leverage USDC and Ethereum blockchain to process cross-border transaction payments made on Australia’s real-time card plans.Currently, Crypto.com uses USDC to meet its Visa card settlement obligations in Australia and plans to expand this feature to other markets.

Prior to this pilot, cross-border purchase settlement using the Crypto.com Visa card involved a long currency exchange process and expensive international wire transfers.

Crypto.com can now send USDC directly across borders to Circle-managed Visa financial accounts via the Ethereum blockchain, greatly reducing the time and complexity associated with international wire transfers.

At the individual user level, services such as Binance Pay allow users to instantly transfer cryptocurrencies across borders.

Cost reduction

According to the World Bank, the average cost of cross-border remittances has dropped from 6.39% in the fourth quarter of 2023 to 6.35% in the first quarter of 2024.According to their breakdown of average costs across the world, Sub-Saharan Africa is the region with the highest remittance costs, with an average cost of 7.73%.

For comparison, the average cost of sending $200 worth of stablecoins (or any number of stablecoins, as most blockchains charge a fixed Gas fee, regardless of the amount of transfer) through a high-performance blockchain like SolanaAbout $0.00025.Products like Binance Pay allow users to make borderless peer-to-peer stablecoin transfers at relatively low fees, as long as the transfer amount is less than USDT.A USD fee of $1 will be charged for value exceeding that amount.

It is worth noting that, at present, inbound and outbound currency exchange is the most expensive part of any transaction involving on-chain assets.CryptoConvert, which Binance partnered with in the fourth quarter of 2023, provides services that allow South African consumers to purchase goods using their digital assets.This eliminates the need for in-and-out currency exchange and is the beginning of incorporating merchant networks into the encrypted native closed payment cycle.

Transparent and trustless network

In an era when traditional payment systems such as SWIFT are used for geopolitical purposes, blockchain technology provides a revolutionary alternative.With its inherent transparency, every transaction on the blockchain is recorded on an immutable ledger that can be seen by all network participants.This openness promotes trust and consensus, and prevents fraud and manipulation.

Decentralization is another key advantage.Unlike centralized systems, blockchain disperses control over a large network, reducing the risk of single point of failure and abuse of power.No one can impose sanctions or restrictions, ensuring that the global payment system is neutral and accessible.The decentralized nature of blockchain enhances its security and enables it to resist attacks.Invasion of blockchain networks requires huge computing power, far exceeding traditional systems.

In addition, blockchain simplifies transactions by enabling peer-to-peer payments, reducing intermediaries and reducing fees.Cross-border payments that once took several days can now be completed in minutes, facilitating real-time global trade.Blockchain provides an existing decentralized banking system with a viable global unified alternative system for storing and transferring digital value.

five,Current Dilemma of Blockchain-based Payment

Scalability andperformance

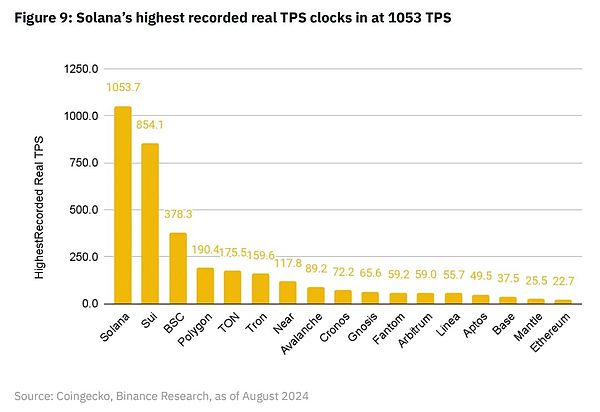

The globally usable payment network must be able to support cheap, fast transactions and operate 24/7.Because payment networks are required to be able to process thousands of transactions per second, even momentary delays can have a significant impact on global business operations.For example, Visa can process over 65,000 transactions per second.

Solana is the blockchain with the highest number of user-generated transactions per second (TPS) recorded to date, with a maximum daily average of just over 1,000.Sui reportedly followed closely behind with an actual maximum TPS of over 850.BNB Chain ranks third in this metric with 378.3 TPS.

In 2023, Visa processed about 720 million transactions per day, which means an average daily TPS of about 8,300 in 2023.

This is still nearly 8 times the largest user-generated TPS recorded by Solana.

In addition to the TPS issue, Solana also showed performance issues.Solana has experienced seven major disruptions since the launch of the mainnet in 2020, causing block production to come to a halt, the most recent in February 2024.This serious accident has led to organizations being cautious about relying on blockchain for critical business operations (such as payments).

However, despite these issues, Solana is still adopted by numerous pioneer agencies.Because of its “proven level of throughput”, Visa describes it as a “viable test and pilot payment use case.”

PayPal also chose Solana as the second chain to launch its PYUSD stablecoin after Ethereum.At the time of writing, despite launching nearly a year later, PYUSD supply on Solana ($377 million) has surpassed Ethereum ($356 million).

Complexity on the chain

Blockchain is largely complex due to its decentralized nature, which makes it more inconvenient for consumers and merchants to adopt them than for centralized systems.The requirements for end users (such as private key management, payment of Gas fees and the lack of a unified front-end) make the adoption of blockchain technology a major problem for ordinary consumers and merchants.

Meanwhile, payment fintech companies such as Square and Stripe have taken the payment experience for merchants and consumers to a very high level in the past five years.Overall, it does this by abstracting all the underlying complexity of middlemen, agency banks and other third parties.So, from the perspective of the traditional global payment stack, from the consumer and merchant perspective, what we now have is a highly refined system that forms a traditional payment system at a cost of up to 3% per transaction.

Fortunately, with the rise of faster and cheaper blockchain infrastructure, the UI/UX of blockchain applications has also been improved a lot.Binance Pay provides users with a familiar centralized fintech experience without being bound by traditional banking systems.This gives users the freedom to send cryptocurrencies to each other at low fees worldwide, while also having the option to easily withdraw crypto assets into self-custody (if they choose to do so).

Regulatory uncertainty

The current regulatory environment for cryptocurrency and blockchain technology is still evolving, bringing uncertainty to businesses and consumers.Regulations vary widely in different countries, complicating global operations and cross-border transactions.

Countries such as Switzerland and Singapore are developing clear regulatory frameworks to provide guidance and promote innovation in the blockchain space.The EU’s Crypto Asset Market (MiCA) regulations are another example of a coordinated regulatory environment.The blockchain industry is also developing compliance solutions to help businesses cope with the regulatory environment.Providing individuals and businesses with the necessary tools to monitor and ensure compliance with Anti-Money Laundering (AML) and Understand Customer (KYC) regulations is key to adoption.

six,Future payments based on blockchain

Blockchain provides a unified technological infrastructure, simplifies the payment landscape, and transcends the fragmented nature of modern banking systems.As a globally decentralized ledger, traditional banks rely on maintaining and synchronizing multiple centrally managed bank accounts, and blockchain eliminates the inherent inefficiencies of traditional banks.Therefore, blockchain provides a new medium that has the potential to reduce costs and increase global payment speeds.

As mentioned earlier in this report, payment giant Visa is trying to use blockchain as a cheaper and faster global settlement method for its institutional customers.Today, Crypto.com, one of Visa’s customers, can send USDC across borders directly to Visa’s financially managed Circle account through the Ethereum blockchain.This reduces the time and complexity of international wire transfers, which previously took several days to process.As companies become more familiar with blockchain technology, many companies may choose to use on-chain stablecoins to trade instead of slower, more expensive fiat banking systems.

On smaller peer-to-peer scales, blockchain could have a faster and more significant impact on the global payment industry, especially in the cross-border remittance sector.Many remittance recipients do not have a bank account or have insufficient bank account.Blockchain technology provides the possibility of a “leapfrog” traditional banking system so that anyone with an internet connection and a smartphone can quickly start receiving payments from anywhere in the world.

Blockchain essentially provides a new, decentralized medium through which payments can be made more seamlessly around the world.As the modern payments industry continues to experiment with this new technology and integrate it into various parts of the global payment system, the ultimate goal we should always bear in mind is to create a cheaper, faster, and more efficient free currency world for everyone.