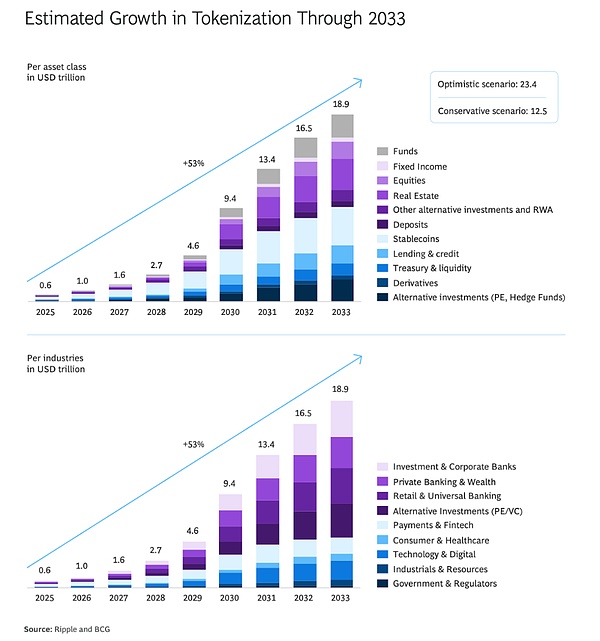

In 2025, the tokenized real-world assets (RWA) market size has reached nearly $300 billion, and some forecasts indicate that the market may reach $30 trillion by 2034.

This momentum is driven mainly by stablecoins.Ethereum chain stablecoin supply alone hit a record high of $165 billion this week.

But under the current situation of high handling fees, high friction coefficient and clumsy user experience, can blockchain infrastructure bear such huge demand?

Despite the many advances in the field of tokenized RWA, crypto innovators are clearly aware that truly seamless systems are still a mobile target.

“It’s still evolving,” said Aishwary Gupta, head of global payments at Polygon Labs.

Aishwary, who has a background in American Express Web2 payment and fund management (who was responsible for “cross-border capital flows”), believes that the problem is not the technology itself, and the underlying technology is evolving rapidly.

Aishwary stressed that the old expansion challenges are rapidly fading, but are quickly replaced by new obstacles, such as regulatory barriers and liquidity bottlenecks.

Four years of great changes: From dilemma to dawn

Aishwary joined in 2021 as the “first full-time employee in the Polygon DeFi business.”Comparing the development status of tokenized payments in the past and the past, he said that the difference is like day and night.According to his recollection, the handling fee was higher four years ago and the user’s entry experience was worse.

“Four years ago, users had to pay a 5% or even 10% on-chain entry fee. It may be possible to try five entry platforms to succeed. From that state to today, it has been much easier to complete transactions and fund entry operations. We have not yet fully evolved, but from a four-year perspective, the process has been much smoother.”

Aishwary pointed out that the core issue is that the cost structure is affected by the patchwork of market patterns and regional regulations: “Only one or two institutions in a specific market are licensed or in a liquidity sandbox.There are very few participants who are actually authorized to operate deposits and withdrawals, so you will see various arbitrage behaviors… The on-chain transfer of a billion dollars is only one cent of the cost, and the real bottleneck lies in regulatory arbitrage.”

Regulatory clarification: Who is leading the tokenization competition?

If stablecoin issuers and RWA providers are taking advantage of regulatory arbitrage, where are they going?Which regions are laying the groundwork for the trillion-dollar outbreak, truly embracing technology and promoting it with all their might?

Aishwary points to four core regions: the United States, Singapore, Europe and the Middle East.“These are the main markets we see high acceptance.”

He said the United States is moving from a long-term lag to a leading position, thanks to increased regulatory transparency.

As BitMEX CEO Stephan Lutz said a few weeks ago, the Trump administration turned the situation overnight through the GENIUS Act, which sets clear standards for stablecoin issuance and gives U.S. issuers long-awaited regulatory certainty.

Singapore is another pioneer in tokenized RWA (particularly stablecoins).

Its Payment Services Act and Financial Services and Markets Act have established a clear licensing system for digital token service providers, which are strictly regulated by the Monetary Authority of Singapore and comply with relevant international financing standards.

Large companies such as Nium, Zodia Custody and Crypto.com have all chosen Singapore for innovative payment channels and regulatory frameworks.

“In addition to the US dollar payment field, Singapore dollar trading volume ranks second.”

Europe is regarded by Aishwary as a typical example of “stable but slow”.Although MiCA regulations (the Crypto Asset Market Regulation) still need to be adjusted, he believes it has done “a lot of due diligence” for stablecoin issuers, and established companies such as Bitstamp and Fireblocks have provided regulated digital asset payment services under the MiCA system.

The Middle East has not lagged behind. Taking Abu Dhabi as an example, regulators have clarified the requirements for banks to issue stablecoins and established clear guidelines for reserve management and compliance.

Idle capital is eternally profitable

Given that Aishwary mentioned the GENIUS Act, we asked about its opinions on terms prohibiting stablecoin issuance from paying holders any form of interest or income.

“The problem is that idle capital in banks can get at least some interest (although not high, but still has profits).If the US dollar on the chain can provide higher returns than off-chain, users will naturally be willing to retain funds on the chain, which actually impacts the entire bank’s capital flow.”

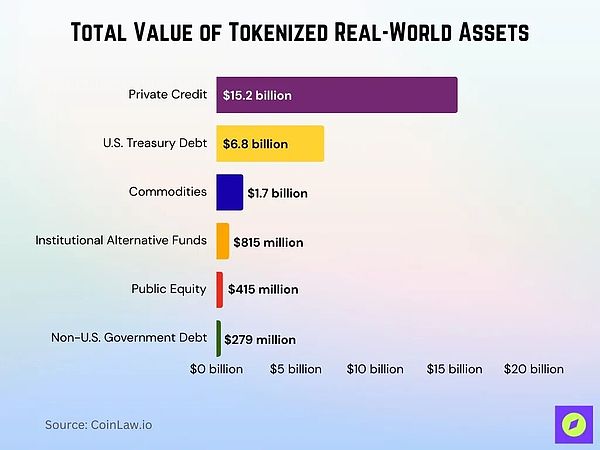

In fact, traditional financial institutions and crypto-native asset management companies are increasingly seeking on-chain product returns, such as tokenized U.S. Treasury bonds, private credit and regulated money market funds.

As of mid-2025, the scale of tokenized Treasury Debt Management (AUM) exceeded US$7.4 billion,Major institutions such as Goldman Sachs, Bank of New York Mellon and Securities actively allocate funds to these products to obtain higher returns, instant settlement and flexible mortgage advantages, and their performance is often better than traditional off-chain banking tools.

RWA Trends Beyond Stable Coins

We are shifting the topic from stablecoins to other trends in tokenized RWA.Although tokenized stocks are becoming the hot topic of centralized exchanges such as Kraken and Coinbase, as well as DeFi platforms such as Synthetix and Mirror Protocol, Aishwary keeps calm analysis:

“Everyone is pursuing tokenized stocks and thinks it’s the best direction, but Polygon tried to tokenized stocks a year and a half ago, and it doesn’t work and there is insufficient demand.”

Why are there little interest?He explained: “Unless you come from certain areas and have no access to Apple stock,Otherwise, users in any region around the world (including India and Dubai) have already held Apple shares through bank accounts, and tokenization has not reached people who really lack access channels.”

In addition, liquidity is still unsolved.”The current problems with on-chain liquidity are significant, and insufficient liquidity causes users to often get inferior quotes or exchange rates.” This is not a breakthrough that many people expect.

Commodity and non-USD stablecoins

Two major trends in Aishwary’s real potential in the tokenized currency world are: non-USD stablecoins and tokenized commodities, which have not been fully paid attention to.”

“Polygon accounts for 50%-60% of the total market share of non-USD stablecoins and is still growing rapidly. We are expanding this area vigorously. Commodity tokenization (such as gold and silver) is equally important, aiming to improve its accessibility and trading convenience.”

Globally, non-USD stablecoins have accounted for about 30% of the transaction volume of active cross-border channels outside the United States.

The global market size of tokenized commodities reached about US$25 billion in 2024, of which gold tokens are worth approximately US$1.7 billion, and the share of oil, silver and agricultural products tokens has grown steadily.

“Although these commodities or assets have been put on the chain, they have not yet developed into an independent ecosystem. This is a missing link at present.”

The road to $30 trillion

As tokenized RWA moves towards a trillion-level, it is worth paying attention to how the market structure will evolve.Against the backdrop of global governments accelerating the hoarding of hard assets, gold prices hit a record high in strategic reserves, and it is logical to follow the development of tokenized gold.

In just a few years,Tokenization has evolved from a proof-of-concept pilot to a global infrastructure,Billions of dollars are pouring into diversified real-world assets across continents.

The key to the future is not only to expand capacity and clear regulatory barriers, but also how the industry can unlock new value and practicality and surpass the changes that have been launched by stablecoins.