Author: Arnav Pagidyala, Source: Bankless, Compiler: Shaw Bitcoin Vision

On-chain lending has become the backbone of decentralized finance (DeFi).However, despite rapid development, its underlying architecture has changed little since Compound v2.Over 99% of DeFi still runs on some form of the over-collateralized, floating-rate model pioneered a few years ago.

For the world to truly function on-chain, lending must mature well beyond its current form.

What started as a simple stablecoin lending mechanism is now developing into a complete financial system.This article aims to highlight the latest breakthroughs in protocol design, credit architecture, and regulation that are driving on-chain lending to become the foundational layer of a programmable global economy.

1. DeFi as a new financial operating system

Over the past cycle, DeFi has quietly evolved from a collection of siled applications to a suite ofComposable global financial operating system.In 2018, protocols such as Aave, Compound, and Uniswap operate as independent applications, each with its own liquidity, governance mechanism, and user base.By 2025, they have developed into “financial core”: a programmable environment where liquidity, risk and execution are abstracted into modular layers that other developers can combine, extend or build into new financial systems.

In traditional software, an operating system provides three functions: shared memory, standardized interfaces, and permissionless scalability.The same model is now appearing in the DeFi field.These new “operating system protocols” manage the shared state of funds rather than the shared state of files.Liquidity acts as the memory layer, interest rate curves and automated market makers (AMMs) act as system calls, while oracles, treasury and governance mechanisms form the layer for coordinated execution.

There are currently a variety of mainstream protocols that embody this design concept:

-

Aave v4Evolving into a hub-and-spoke liquidity operating system.At its core is a controlled core called the Liquidity Center, surrounded by modular marketplaces for RWAs, GHOs, and permissioned pools.Liquidity is provided once and deployed to all branches under controlled risk parameters, enabling unified capital efficiency rather than fragmented liquidity pools.This marks an important step forward for Aave v4 from the isolated market structure of Aave v3 to a fully shared liquidity layer.

-

Morpho v1 and Euler v2have taken the opposite route: they adopt a minimalist credit core and do not share liquidity, only logic.Each vault is an independent micro-market, but all inherit the same underlying architecture, a unified accounting and clearing engine.Morpho v2 expands on this foundation by replacing static vaults with an intent-based request-for-quote (RFQ) matching layer, allowing fixed-rate and floating-rate loans to coexist in a unified credit market.

-

FluidRepresenting the most vertically integrated version, it is a unified liquidity operating system where lending, trading and collateral all come from a shared pool of funds.It is the first system to treat every dollar of idle capital, collateral, and borrowed funds as an interconnected resource.

Together, these architectures mark the next stage of DeFi development.The era of siled money markets is giving way to more interoperable financial systems that function more like operating environments than applications.Liquidity, risk and governance are becoming shared infrastructure rather than product features.Whether through a modular hub, a minimalist core, or a vertically integrated engine, the end goal is the same: to build an open, programmable, and globally composable financial system.

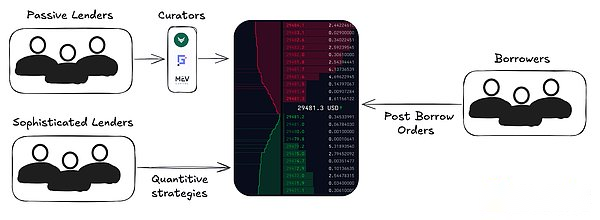

2. Lending and borrowing based on order book

Most DeFi lending still relies on a fund pool model, where all liquidity providers share risks and rewards.The advantages of this model are simplicity and liquidity sharing, but the price is lack of accuracy.In addition, interest rates are not determined through negotiation, but are generated by algorithms or decentralized autonomous systems (DAO), which is in sharp contrast to the refined interest rates provided by traditional finance (TradFi).

The next breakthrough in lending microstructure isOrder book-based lending model, in this model, lenders and borrowers publish specific quotes, similar to the central limit order book (CLOB) in traditional finance.This structure enables granular control over terms: fixed or floating rates, maturity dates, collateral requirements, and even custom risk parameters.Hybrid models are also emerging, combining liquidity pooling to increase depth with order book mechanisms for price discovery.

Just as AMMs evolve into liquidity-focused models, lending markets may also move toward this more expressive design.The key difference, however, is that the lending market is built for passive lenders, so the experience for regular lenders will be essentially the same, but borrowers will have more options.

The order book can be used for both floating-rate and fixed-rate loans, but the basic mechanism is similar: the lender publishes a quote, the borrower accepts the quote, and the matching result generates a credit position on the chain.Most funding in these systems comes from passive lenders, often deployed through custodians or treasury managers who aggregate liquidity and manage parameters on behalf of passive lenders.Avon is pioneering a hybrid architecture that combines a central limit order book with custom strategies (independent markets), allowing compatible orders to be liquidated atomically while still meeting the needs of passive lenders.

3. The era of convenience

As mentioned above, the underlying lending protocol will be completely abstracted by a series of consumer-facing products.Examples include revolving lending, automated risk management, revenue abstraction, consumer agency, and more.

-

cycle strategyis being abstracted into seamless one-click operation products.Platforms such as Contango and Loopscale have automated processes, while lending marketplaces such as Jupiter, Euler and Silo have begun integrating these mechanisms directly into their front-end interfaces.

-

revenue abstraction: For end users, borrowing and lending will be reduced to a single “net benefit” number.The strategy behind it will gradually fade from view, just as banks hide the workings of overnight repos behind current account interest.With exchanges like Coinbase integrating directly with protocols like Morpho, earnings will become a basic user experience feature rather than a complex financial operation.

-

consumer agent: Intelligent agents will dynamically manage collateral ratios, refinancing and liquidation protection on behalf of users.These systems will rebalance positions across protocols in real time, optimize borrowing costs and hedge volatility in real time, turning active portfolio management into a back-office process.

4. Ratings, Benchmarking and Compliance

DeFi can only grow to trillions if chief financial officers (CFOs) use DeFi without jeopardizing their positions.

Any financial market is inseparable from standards, and the lending market is no exception.A framework of credit ratings, transparent benchmarks and compliance mechanisms form the trust infrastructure that connects code-based markets to real-world capital.

Rating: Just as Moody’s or S&P assess corporate and sovereign credit, independent risk rating agencies will emerge to assess DeFi vaults, protocols and on-chain credit portfolios.These ratings will quantify smart contract risk, collateral quality, counterparty risk exposure and historical performance, allowing institutional risk frameworks to be clearly mapped to the underlying DeFi technology.While I think S&P and Moody’s will likely still dominate this space, there are also emerging players like Web3SOC, Credora, and others.

Benchmark: Standardized indices, such as “DeFi LIBOR” or “On-Chain SOFR”, will enable borrowers, lenders and vaults to price risk and compare yields under different protocols.This will lay the foundation for the native on-chain construction of derivatives, yield curve and structured credit markets.

Compliance: As institutions join, embedded KYC/AML will become a basic requirement.Protocols will increasingly divide liquidity into permissionless and compliant tiers, enabling regulated entities to access DeFi rails while maintaining open access to all other users.For example, Morpho v2 vaults support customizable access controls designed to meet institutional-level compliance requirements.

These elements together constitute the institutional interface for on-chain credit.

5. Beyond overcollateralization

Today’s market is dominated by crypto-asset over-collateralization and floating-rate lending, which, while practical, is still an inherently narrow market segment.The future development direction of on-chain credit will go far beyond this model and unlock a complete credit system that supports traditional finance.

fixed rate loan: Predictable payments, clear maturities and structured instruments are prerequisites for institutional adoption.Protocols such as Morpho v2 are pioneering intent-based fixed rate markets, while emerging designs such as Term and Tenor explore auction-driven and order book mechanisms to price term risk directly on-chain.In effect, Morpho v2 will likely serve both ends of the market: a highly liquid, order book-style market on one end; and highly customizable OTC-style quotes on the other, with custodians allocating liquidity vaults and lending arms managing more targeted credit exposures.

low mortgage loan:3Protocols such as Jane and Wildcat have pioneered a framework for trust-minimized, low-collateral credit, combining smart contract-enforced guarantees with real-world underwriting and delegation reputation.

alternative credit market: Lending is also expanding into long-tail and non-traditional collateral areas, such as tokenized RWA, alternative FX trading pairs, stablecoin arbitrage trades, and even credit-guaranteed credit lines.These markets introduce diversification, cross-border liquidity, and new dimensions of risk that reflect the complexity of global finance.The explosive growth of Midas is a case in point, highlighting the two-way demand dynamic: traditional finance seeks to enhance on-chain liquidity through circular mechanisms, while crypto-native investors seek high-yielding exposure to uncorrelated traditional financial instruments.

Together, these frontiers mark the evolution of DeFi from a collateral-limited niche to a full-scale, programmable credit system capable of guaranteeing a wide range of financial products from consumer loans to sovereign debt, with all transactions settled directly on-chain.

Finally, when discussing the future of DeFi lending, I have to mention the rise of custodians like Gauntlet, Re7, Steakhouse, and MEV Capital.These institutions actively manage liquidity, optimize returns, and adjust protocol parameters.They are evolving into on-chain versions of Millennium or Citadel, deploying quantitative strategies, risk models and dynamic liquidity management across multiple protocols.

In past years, custodians have earned modest performance fees and often subsidized users with incentives to attract deposits.But this didn’t happen overnight.They know that hosting itself will become one of the most scalable and profitable businesses in the next decade.Taking deposits is just a means of attracting traffic, and its purpose is to distribute data.As these companies continue to accumulate scale and reputation, it is not difficult to imagine that they will become on-chain asset management companies with over $10 billion in assets under management and have a pivotal position in all mainstream protocols.

Competition for deposits will only intensify.There are many hedge funds, but there is only one Millennium. Every project manager in the DeFi field is competing to become its successor on the chain.

Conclusion

DeFi lending is no longer a collateral-based leverage experiment, it is evolving into the architecture of a programmable financial system.From order book-based credit markets and one-click cycle products, to agency-grade ratings and low-collateral frameworks, every layer of architecture is being rebuilt for scale, precision, and accessibility.

Once credit becomes truly programmable, finance will no longer be limited to institutions but will exist within networks.