Original title:>Why Ether Stands Out Among Digital Assets

Author: Lorenzo Valente, ARK Invest researcher; Compilation: 0xjs@作 作 作 作 作 作

Foreword

As Bitcoin consolidates its status as a reliable digital value storage and the only assets with rules -based monetary policy, Ethereum network and asset Etherbon (ETH) seem to be gaining development momentum at with similar potential.In fact, ETH is becoming an institutional -level asset with income potential.

As the only digital assets that really generate income, ETH seems to have unique and distinctive characteristics, making it a “reference indicator” in the field of digital assets.ETH has played a key role in the private and public financial markets, affects the monetary policy of other digital networks and applications, and measures the health of a wide range of digital asset ecosystems.The market value of Ethereum network is about $ 315 billion, and has millions of active users per month. As shown in the figure below, Ethereum Network is realizing meaningful economic value.

Source: ARK Investment Management LLC, 2024.This ARK analysis is based on a series of basic data sources and can be shared as required.Data as of August 15, 2024.For reference only, it should not be regarded as advice or holding any specific securities or cryptocurrencies.

ETH’s pledge yield has affected other smart contract ledger, making it different from digital assets other than Bitcoin.

Similarly, U.S. Treasury bonds play a key role in the traditional economy, with many role: set the benchmark interest rate, act as a high -quality value storage method in the uncertain period, and affect the market’s expectations for future economic conditions.Our research shows,As an asset, ETH has begun to develop similar attributes to US Treasury bonds in the field of digital assets.ETH’s potential for income -and its wide use in digital asset transactions -is becoming its two most unique and important quality.

Investors can protect Ethereum ledger by pledged ETH to obtain ETH income.In other words, technically, this income is not the native income of ETH assets.LiDo, Rocket Pool, or FRAX and other liquidity pledge derivatives provide the pledged ETH and its income tokenization methods.Liquid pledge allows users to pledge their ETH by receiving derivatives representing their pledged ETH, while maintaining liquidity.Another method called “solo pledge” can more directly control the pledge assets and get a higher return, but it will lock ETH.

The goal of this article is to identify and define the unique features of ETH.What is special about ETH?How can it stand out in a wider range of assets?We aim to answer the following questions:

1. How does ETH generate income?

2. How to predict the economic cycle of the yield of the miner’s extraction value (MEV)?

3. Does ETH have attributes similar to bonds?

4. Does pledge and re -pledge enhance ETH as a programmable mortgage?If so, how do you do it?

5. Will ETH’s Staking yield become a reference yield for the encrypted economy?What if it will, in what sense?

6. What are the mixed attributes of ETH in the standard classification of traditional assets?

1. How does ETH generate income?

“Certificate of Rights and Interests” (POS) is a quite new “consensus algorithm”, which is more energy -saving than the “workload certificate” (POW).Why?In the POS, the number of tokens held by the consensus algorithm based on the “verification” and the number of tokens willing to “pledge” as a mortgage to select “Verreder” -equivalent to the “miner” in POWBlocks and verify transactions.The more coins for pledges, the higher the probability of being selected to build and verify the next block.Therefore, the POS system does not need a large number of calculation of mining capabilities, but requires verifications to invest a large amount of investment on the Internet -if they verify fraud transactions or violate the core agreement rules, they may lose these pledge.Verivers pledge can prevent fraud, and the power cost paid by Bitcoin miners to participate in the network can also prevent fraud.Both ensure that each participant acts in economic rationality and integrity.

When the Ethereum network was upgraded to Ethereum 2.0, its agreement changed from a proof of workload to a equity certificate.Ethereum’s latest monetary policy upgrade EIP-1559 has introduced a novel cost market structure.Both changes have changed the way ETH generates and distributes income.

ETH yield is based on the following three factors:

issued(≈2.8PercentAPR.+ Tips(& lt; 0.5PercentAPR.+ MEV(& lt; 0.5PercentAPR.

Let us understand each component of the income more in detail.

issued

As of September 2024, the Ethereum Network increased by about 940,000 ETH each year. Based on today’s pledge ratio, it is equivalent to about 2.8%of the annualized yield (APY).The pledge ratio will change according to the number of ETHs of the pledged ETH.If the more authentication of the pledge, the higher the pledge ratio, which will lower the distribution yield, because according to the weighted pledge of the participants, the distribution yield will be allocated to them on average.It is important that the Ethereum network guarantees the minimum annual circulation rate of 1.5%, and it needs to pledge 100% ETH and there is no transaction on the blockchain. This is basically impossible.All authenticants who protect network security by reaching consensus and processing transactions will be issued.

tip

“Tips” is an optional fee introduced by London upgrade and EIP-1559. Users can include these fees in Ethereum transactions.Tips are “priority fees” because they inspire verifications to prioritize transactions in the block.

When the user wants to send a transaction, they must pay the basic costs, or they can choose to pay tip.Basic expenses will be dynamically adjusted according to network congestion. When the network is more busy, the cost will increase.If the user wants to speed up the transaction speed, the priority or tip is optional.In fact, the priority cost is a cost that changes with the usage of the network and the degree of congestion.

MEV

In addition to the issuance and user tip, the verifications will also receive an additional profit obtained by the “miner’s extraction value” (MEV), or the additional profits obtained through the blocks that contain, exclude or sort the transactions in the blocks they generate.

MEV is equivalent to the “order flow payment” (PFOF) in the traditional market -the additional income paid by the high -frequency market and traders to the verifications to prioritize their transaction flow.Like the priority costs, its yield is unstable because it depends on the supply and demand relationship of block space and uses less traders who have less knowledge of transactions on the Internet.The important thing is that the MEV reward is only applicable to the validator of running the MEV client (such as MEV BOOST).

Basic cost

It is important that basic expenses (re -emphasize that the standard cost of sending transactions) will not affect the income.Instead, it is “burned” and will not provide a direct cash flow for pledges.As part of the EIP 1559 upgrade, the basic cost mechanism makes the cost more predictable, and the Ethereum network is more user -friendly.

Only basic costs and circulation can change the total supply of ETH.The ETH tokens that pay the basic fee of the user will be removed permanently from the total supply.If the basic costs are high enough (more than 23 GWEI in the current market) and the “destroy” volume exceeds the number of network distribution (940,000 ETH per year), the total supply of ETH will decrease over time over time, which will reduce the currency of the agreement.Instead, if the amount of network circulation is higher than the basic cost of destruction, inflation will occur.

Two dynamic support for the tightening trend of currency supply by ETH.First of all, Ethereum’s Rights Certificate (POS) mechanism enables verificationrs to reduce operating expenses (OPEX) and capital expenditure (Capex) related to network server.In other words, the cost of energy and data centers related to POW and ASIC machines does not exist in POS.

Secondly, as the premier smart contract platform, Ethereum network operates at the bottom of 14 transactions per second.Thanks to the strict test code, Ethereum has attracted the most active developers, the most widely used applications and the highest settlement value in the development process of just nine years.

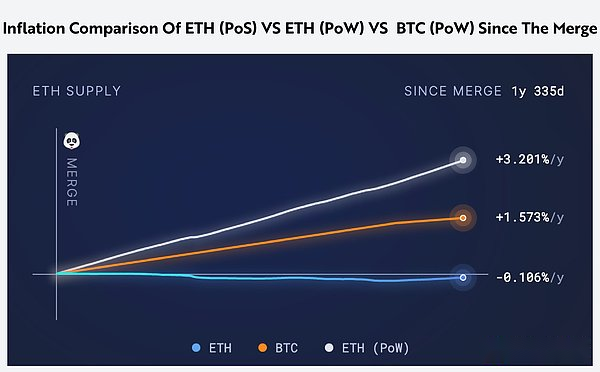

Since the transition to POS on September 15, 2022 and the implementation of EIP 1559, ETH has always served as a net -scale asset, with an average annual reduction of 0.106%.If Ethereum continues to run to POS with POW and there is no EIP 1559, the supply of the network will expand 3.2%per year, as shown below.

Source: Ultra Sound Money.Data visits are August 15, 2024.ETH (POS) and ETH (POW) and BTC (POW) have been compared since merging.For reference only, it should not be regarded as advice or holding any specific securities or cryptocurrencies.

2. How to predict the economic cycle of the yield of the miner’s extraction value (MEV)?

As mentioned above, miners can withdraw value (MEV) benefits are part of ETH pledge income.In this section, we will explore MEV in depth, pay special attention to how it produces, and how it predicts economic activities and market cycles.

MEV is equivalent to order flow payment (PFOF) in traditional finance. It is used as a city merchant and high -frequency trading company to pay additional fees to verifications to bypass the standard Ethereum “MEMPOOL” in the Ethereum.This happens.Similarly, companies like Citadel Securities like Citadel Securities pay fees to platforms such as Robinhood, TD American, Charles Schwab, and Fidelity to guide customer orders to them.In fact, MEV was born during the ETH ICO boom in 2017 as the basic form of “bribery”.In the ICO era, participants and investors who purchased tokens who purchased certain projects must deposit ETH in smart contracts in exchange for the original native currency of the project.As they become more and more popular, token issuance becomes excessive subscription, and operates in accordance with the principle of first -served.In order to become the first batch of people who deposited ETH into these smart contracts, the participants “bribed” verifications under the chain.

Like PFOF, MEV usually reflects retail trading activities because the marketing merchants are willing to pay higher prices for unknown orders than informed orders.Just as PFOF payment is the indicator of excessive expenditure and risk appetite in the field of retail stocks, MEV also plays a similar role in predicting the decline of the Ethereum ecosystem and the economic cycle, as shown below.

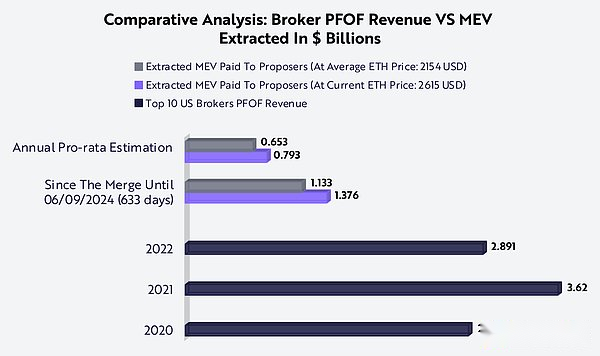

Source: ARK Investment Management LLC, 2024, data from Daytrandingz.com and MEV-EXPlore V1 based on June 9, 2024.For reference only, it should not be regarded as advice or holding any specific securities or cryptocurrencies.

Although MEV in Ethereum is equal to PFOF in the stock market, MEV accounts for a percentage of the total market value of ETH and ERC-20 token than the percentage of the US stock market.Since the merger, the $ 790 million income will be extracted per year accounting for 0.20%of ETH’s $ 315 billion.The total market value of ETH and ERC-20 tokens was about 500 billion US dollars, and the percentage of the withdrawal revenue was reduced to 0.15%, and it was still 27 times higher than the US $ 2.891 billion in US $ 2.891 billion in US $ 5.0056%.During the early development stage, Ethereum’s order route mechanism is more expensive than the order route mechanism in traditional finance, but it is worth noting that Ethereum supports a wider order type of orders through smart contracts -such as lightning loans, pledge, and swap — And other interactions with decentralized applications.

In addition, in traditional finance, other expenses and profit centers (brokerage fees, exchanges, and hedge funds profits) are the primary sources of PFOF income.These costs are not transparent, but it is essential for the overall cost structure of traditional financial transactions.

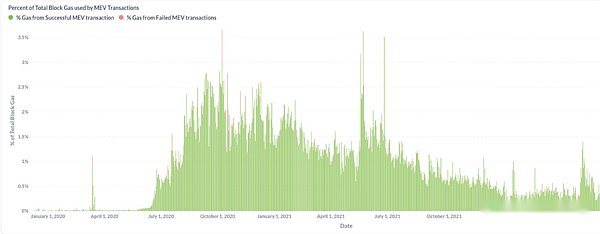

According to the PFOF model of history in traditional finance, the increase in PFOF income is related to increasing retail activities involving traders with less information, and the decrease in PFOF indicates the opposite.For example, between 2021 and 2022, as interest rates rose 16 times, Robinhood’s PFOF revenue decreased by 40% to $ 587 million from US $ 974 million, which indicates the beginning of the bear market.The same is true for MEV. From July 2021 to October 2021, the block space used by high -frequency trading companies and MEV robots fell five times before the severe cryptocurrency bear market in 2022, as shown below.

Source: ARK Investment Management LLC, 2024, data based on Explore.flashbots.net as of August 15, 2024.For reference only, it should not be regarded as advice or holding any specific securities or cryptocurrencies.

Our research shows that most of the MEVs may be extracted and re -assigned on Layer 2 in the next year.Layer 2 is a secondary agreement on Ethereum.They can improve scalability and efficiency by processing transactions outside the main chain, while using their security to shorten the transaction time and significantly reduce the transaction fee.In the next two years, we expect more than 90% of the total transaction to occur on Layer 2.In order to cater to retail investors who are more sensitive to prices, Layer 2 should dominate ETH trading activities and obtain incomparable benefits from MEV. When the sorter (or Layer 2 verification device) is further decentralized, the income will be greaterEssence

Today, the dominant Layer 2 network Arbitrum and Optimism are run by a single sorter, which means that the block space does not auction to the highest bidders.Instead, the transaction will be sorted in accordance with the principle of first -served, and the block searcher or the builder cannot be sorted again.

Therefore, some forms of MEV (maximum extraction value) are impossible, which shows that MEV is significantly lower than a more advanced state with multiple decentralized sorters and more mature MEV infrastructure.

MEV’s yield is a subset of ETH’s overall yield. It is becoming a reliable indicator on the Ethereum blockchain activities and the economic cycle.Compared with traditional finance, MEV is mainly based on retail transactions, and the proportion of funds with insufficient information. MEV is a measure of active and economic health.The ledger provides a framework.

3. Does ETH have attributes similar to sovereign bonds?

Fixed income assets (especially bonds) have already existed for hundreds of years, and are one of the most important financial promotion factors in the economy.Bond representative investors are loans provided by borrowers (usually companies or government).Our research shows,Although not the same as sovereign bonds, pledged ETH (STETH) has the characteristics similar to sovereign bondsThese similarities are worth exploring.

The most important and different points between the pledge ETH and the sovereign bonds are as follows:

Note: For the expiration period, the pledged ETH can be canceled at any time. In addition to the income obtained during this period, it can also recover the original pledge amount (called the “principal”).Source: ARK Investment Management LLC, 2024.For reference only, it should not be regarded as advice or holding any specific securities or cryptocurrencies.

When we discuss the comparison of pledge ETH and sovereign bonds below, we emphasize that their differences are as important as similarity.We believe that their risk status represents pledgeEthThe most significant difference between sovereign bonds.

Credit risk

Sovereign bonds: When a government issued a debt of local currency pricing, the government has the possibility of breach of contract, although this possibility is less likely for stable economies.

ETH: Ethereum network cannot be arrears of pledged ETH, because technically, this is not debt.The pledge income is obtained from the chain activity and network distribution through programming, which means that the income fluctuates according to network performance, activity level and pledge rate.

Inflation risk

Sovereign bonds: The inflation of local currencies can erode the value of bond returns, thereby reducing purchasing power.

Pickup ETH: If the circulation rate of the new ETH is significantly exceeded the destruction rate of basic costs, there is a risk of inflation, which leads to an increase in supply, thereby reducing the value of net income and diluted interest payment.

Interest rate risk

Sovereign bonds: Interest rate changes will affect bond prices, and rising interest rates usually lead to a decline in bond prices.

Eth: Although Ethereum itself does not issue a variety of bonds (a variety of pledge yields at different periods), the expected change of the yield of other 1 -level smart contract platforms may affect the perceived value and attractiveness of the pledge ETH.

Risk of currency depreciation

Sovereign bonds: The depreciation of local currencies relative to other currencies will lead to a significant decrease in interest payment and principal value when converted into other currencies.

ETH: ETH may fluctuate compared to other major cryptocurrencies and legal currencies, which affects the actual value of pledge yield and principal relative to other assets.

Political and legal risks

Sovereign bonds: Changes in the government or regulatory system may affect the repayment of bonds and may lead to changes in fiscal policy and/or debt reorganization.

Package ETH: This analogy is not very direct.Package ETH assumes additional risks related to network security and governance.If the verificationr is improperly or colludes, the pledged ETH may be punished as a punishment, which will cause potential losses of the principal.The change in regulatory changes in a wider range of cryptocurrency markets also affects the value and security of pledged ETH.

Volatility

Sovereign bonds: sovereign bonds are generally regarded as low -risk, low fluctuations.However, during the period of economic instability or political turmoil, the volatility of bonds may increase significantly.

Package ETH: pledged ETH’s volatility is large because it is still in the bud stage.Volatility will affect pledge income and principal value.

The pledged ETH modeling is a sovereign bond to understand the differences in their respective risk status.Although both will be affected by inflation, interest rate changes, and currency depreciation, the nature of these risks and its impact may be very different.In addition, ETH pledge introduces unique risks related to network security, verifier behavior, and intelligent contract errors. These risks have no direct similarities in traditional sovereign bonds.

Similar to the present value of calculating sovereign bonds, people can try to simulate the present value of the so -called “pledged ETH bonds”.The formula will add the present value of each re -investing interest ticket to the present value of the value of the ticket surface when the bond expires.Then, by modeling interest ticket interest with the pledge ETH yield and modeling the discount rate with the risk -free interest rate of US Treasury bonds, people can get the current price of pledged ETH bonds.

Nevertheless, one of the most important differences between sovereign bonds and “pledged ETH bonds” is that the yield of pledge ETH changes every day.Therefore, the “pledged ETH bond” needs to calculate the average yield during the expiration period.In addition, unlike traditional sovereign bonds, pledge ETH can cancel pledge or “redemption” at any time, and the principal can be redeemed at any time.

At present, ETH does not have a yield curve, which means that the pledge yield has nothing to do with the expiration time of pledge assets.However, according to our research, the ETH yield curve may change in the next few years, increasing similarity to sovereign bonds, and the period and period of ETH pledge are different.

4. Does pledge and re -pledge enhance ETH as a programmable mortgage?

Liquidate derivatives (LSD) are a protocol aimed at simplifying the pledge process, suitable for users who lack technical professional knowledge.LSD cooperates with the trusted node operators to manage pledge operations on behalf of users.Users who pledge ETH through the leading LSD provider will get STETH.STETH is the synthetic version of its pledged ETH, which is similar to the tokens -based deposit certificate.STETH tokens will automatically adjust to reflect the pledge reward (3.2% APY), and can be converted to ETH on centralized and decentralized exchanges.The tokens or deposits are then used to be used for borrowing, obtaining leverage, re -mortgage, and many other financial activities in the fields of digital assets, especially applications/protocols based on Ethereum.

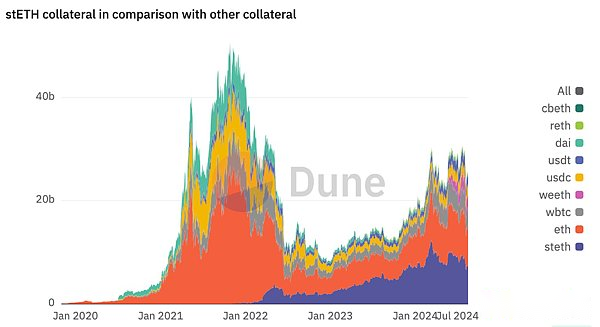

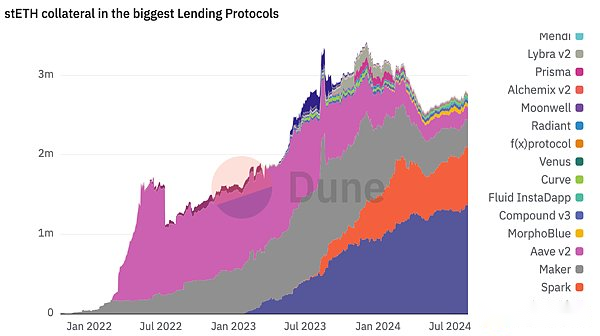

STETH is ETH’s revenue version.Because STETH has programmability and liquidity, it begins to replace ETH in many DEFI protocols and applications.In fact, STETH has been replacing ETH into high mortgages in Ethereum economy.Today, the total of about 2.7 million STETH as a DEFI mortgage, accounting for about 31%of the entire STETH supply, as shown belowEssence

Note: The y -axis on the left side of this third -party chart is based on US dollars (one billion US dollars).Each abbreviation displayed on the right side of the figure above represents a different asset, which can be used as a collateral. As shown below: CBETH (Coinbase Staked Eth), RETH (Rocket Pool ETH), DAI (MakerDao Stablecoin), USDT (TetherStablecoin, USCLE Stablecoin, Weeth (Ether.fi ETH), WBTC (Wrapped Bitcoin), ETH (ETH), STETH (Lido Staked Eth).Source: Dune (https://dune.com/lido/teteth- compare-to-sto-s) as of the end of August 15, 2024.For reference only, it should not be regarded as advice or holding any specific securities or cryptocurrencies.

There are more than 80,000 STETH in the liquidity pools of CURVE, Uniswap, BALANCER, Aerodrome, and other leading DEX.STETH is a kind of income asset. Because of its capital efficiency provided by users, liquidity providers, and municipal businessmen, it is becoming the preferred collateral.At present, the preferred mortgages on AAVE V3, Spark and Makerdao are 1.3 million STETH, 598,000 STETH and 420,000 STETH, respectively. They are locked in these protocols and are used as a stable currency for loan or cryptocurrency support.As shown below.Our research shows that other liquidity pledge derivatives of STETH and ETH are becoming the first choice of high mortgage in the Ethereum ecosystem in the Ethereum ecosystem.

Note: The y -axis on the left side of this third -party chart is measured by the number of STETH instead of STETH’s US dollar.Source: Dune (https://dune.com/lido/teth-Compare-to-sto-OTHers). For reference only, it should not be regarded as investment suggestions or purchases, sale or sale or sale or sale or selling or selling.Suggestions holding any specific securities or cryptocurrencies. Note: The label displayed on the right side of the chart is the name of the specific protocol.

However, if the user wants to obtain higher returns from ETH, which is pledged and provides more use as a mortgage, what will happen?

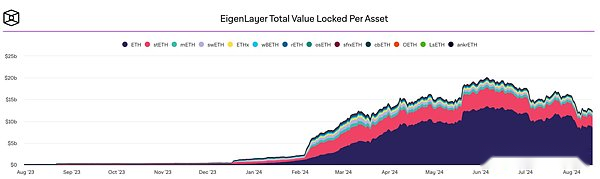

This is exactly the function that Eigenlayer (a re -pledge agreement) can be implemented.So far, EigenLayer has accumulated $ 13 billion in ETH tokenized deposit certificates, accounting for 50%of Lido TVL, accounting for about 4%of the total supply of ETH, as shown below.The LIquid pledge derivative of ETH pledged on the Ethereum network can pledge on the Eigenlayer platform, so that other protocols can enhance its network security within the specified period, this process is similar to rental security services.

The volatility of some protocols is too large to provide reliable network security. Therefore, it may face shortage of liquidity and/or it needs to enhance its security. Both situations can be pledged through dual centered currency or more stable with more stable.The mortgage (such as ETH) rents all its safety to solve it.For its security services, the reward rewarders like EigenLayer are rewarded by Parliament, just like Ethereum Network pays the verifications.

We believe that the emergence of re -pledge enables investors to better control their risks and returns, thereby improving the practicality and efficiency of ETH as mortgages in DEFI.

Note: Each abbreviation displayed at the top of the figure above refers to the protocols of different ETH liquidity pledged tokens, as shown below: STETH (LIDO), RETH (RocketPool), SFRXETH (FRAX), CBETH (CoinBase), ANKRETH (Ankr), LSETH (liquid collective), OETH (Origin Protocol), Meth (Mantle), SWETH (SWELL), WBETH (Binance).Source: The Block as of August 15, 2024.For reference only, it should not be regarded as advice or holding any specific securities or cryptocurrencies.

EIGENLAYER’s success shows that users and institutions have a strong interest in using ETH it they hold in more complex.By introducing new use cases, Eigenlayer allows participants to retain the ETH they hold and generate additional benefits.As they stand out from the launch of Eigenlayer -just like STETH stand out from native pledge -flowing campaign to the campaign is likely to act as a mortgage on various platforms.

Whether in the liquidity pool, lending platform, structured products, or stable coins supported by encrypted support, various forms of benefits ETH may become the first choice of programming mortgage in DEFI -regardless of the deployment in the deploymentEthereum 1 floor is still available on any 2 layer currently available.

5. Will the pledge yield of ETH become the endogenous benchmark of the encrypted economy?

So far, we have described ETH in some aspects of assets similar to sovereign bonds in this article, and described ETH and its liquidity pledged derivatives as high -quality liquidity collateral in DEFI, supporting many widely used applications that are widely used applicationsprogram.In this part of this article, we focus on another unique feature of ETH pledge yield: its impact on investment in the encryption economy. Our research shows that this effect can be related to the role of national bonds and federal funds in the traditional economy.Compared.

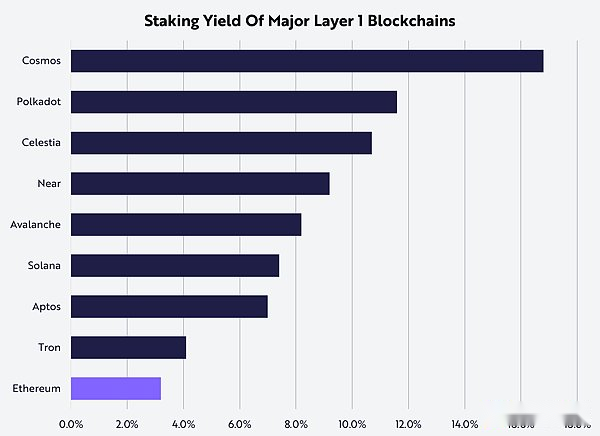

Today, pledge yields affect public and private investment in the field of digital assets, just like the role of high -quality liquid assets (HQLA) in traditional finance.First of all, ETH’s yield seems to put huge pressure on the native return of the competitive Layer 1 smart contract, forcing other blockchain to provide higher rewards for verificationrs to recognize their security and long -term commitments, as shown below.If the return on investment is unlikely to be higher, why should investors/verifications hold assets with higher risk of pledge and more volatility?It is important that, unlike ETH, the yields of other assets often dilute cash flow.In other words, if the investor holds and does not pledge any other Layer 1 generation, network inflation will dilute it.

Source: ARK Investment Management LLC, 2024, data based on The Staking Explorer as of August 15, 2024.(Https://www.stakingrewAnts.com) For reference only, it should not be regarded as a suggestion for investment suggestions or purchasing, selling or holding any specific securities or cryptocurrencies.

ETH’s pledge yield also increases the chance of holding and borrowing stable coins.As its native yield rises and becomes the benchmark, ETH’s activity, MEV costs and overall demand make multiple Defi protocols under pressure.MakerDao, AAVE and Compound are three of them.

MakerDao is an agreement to manage the issuance and management of DAI stablecoins.DAI is issued by the mortgage debt position (CDP), because users lock in mortgage products such as ETH or other white list assets to cast DAI.One of the core functions of the MakerDao protocol is the DAI savings rate (DSR), which allows DAI holders to earn interest by locking their DAI in a special smart contract.After DAI faces huge pressure on selling pressure and decreased circulation supply, MakerDao governance decided to increase the DSR interest rate from 5% to 15%.

In the currency market, such as AAVE or Compound, the return on supply/borrowing stablecoin is greatly increased.The APY range of fiat currency supports stablecoin is from 5% to 15%, depending on market conditions.This interest rate reflects investors willing to borrow stablecoins, while providing ETH or STETH as a collateral without being sold.

In addition, protocols like Ethena Labs (it provides a stable currency, with spot arbitrage transactions between spot STETH and sustainable futures short positions as mortgages) attracts many STETH holders.Why?The yield provided by Ethena’s stable currency is significantly higher than the DEFI alternative, let alone ETH’s general pledge yield.

ETH pledges also affect income farming opportunities.It is hoped that the launch of new products or new features and attracting ETH valuation capital to enter its capital pool must make their incentive measures consistent with the current market conditions.For many teams and agreements, higher pledge returns usually mean higher users’ acquisition costs, because potential investors and liquidity providers are more likely to pledge ETH to obtain more stable returns, not new or new or newIn less mature income farming opportunities related to higher risk returns.

The distribution of funds to investors with early digital assets are asking the same question: On the basis of risk and liquidity adjustment, will this project provide better return on investment than pledged ETH?We can use an example of a assumption to explore this issue.A typical investment period for investment is 7 years (the average harvest period of technology startups), to what extent can it be better than ETH after compound interest to achieve the balance of revenue and expenditure?If ETH yields are 4% after 7 years of compound interest, even if the price appreciation is not considered, the performance of closed funds must be more than 31% better than ETH.In other words, early investors in the field of digital assets often consider this: on the basis of risk and liquidity adjustment, whether the items they are evaluating can simply hold and pledge ETH to provide higherReturn?For example, considering a typical 7 -year fund, it is usually called the harvest period. During this period, the investment is expected to mature and provide liquidity.If the same funds are put into ETH and pledged, the average pledge yield is 4%, then the performance of the project needs to be at least 31%higher than ETH to make up for the composite yield effect.In a bull market with over -subscription, decreased valuation attraction, and unfavorable ownership conditions, competition from pledged ETH will become more intense.

6. What is the mixed attribute of ETH?

The reason why the spot Bitcoin ETF is successful is because compared to other value storage means (especially fiat currency), Bitcoin has the potential for appreciation and has high stability.The people of the currency authorities play an important role in the long -term devaluation of the fiat currency for decision -making (sometimes arbitrary and inconsistent).Instead, Bitcoin is “rules -based”, and its supply has been measured by mathematics, with a maximum of 21 million.Therefore, Bitcoin is becoming a powerful alternative to fiat currency and is a digital asset category similar to digital gold.

As a younger asset, ETH has experienced multiple currencies and technology upgrades for many years.In addition, its Turing’s completeness and yield cash flow make it difficult to describe, define, and framework within the boundary limit of the traditional asset category.

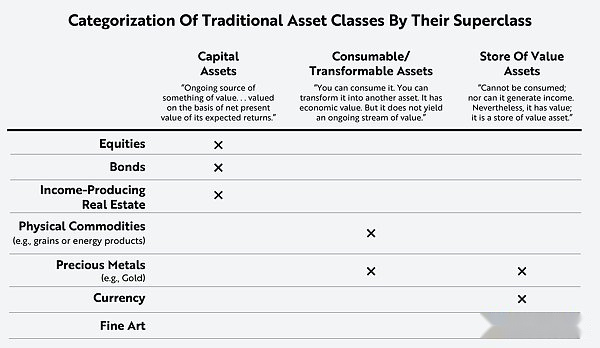

Robert Greer In the paper “What is an asset class (Anyway)” is divided into three categories: the assets are divided into three categories:

Capital assets:Assets that increase value in the form of cash flow, such as stocks, bonds or real estate.

Consumer assets:Can be consumed or converted into assets of other assets or products, such as goods.

Value storage:Assets that cannot be consumed or converted into other assets or products but can maintain value for a long time.

Source: Greer 1997.For reference only, it should not be regarded as advice or holding any specific securities or cryptocurrencies.

In this article, we explain the similarities between ETH yields and bond tools (especially sovereign bonds) yields.We have proven that ETH pledge yields are the standards for the measurement of smart contract activities and economic cycle in the digital assets, just like the federal fund interest rate in traditional finance.In addition, like any other 1 -level asset, ETH is an asset -consumable asset that is used in the Ethereum network to be included in the account transaction.This process involves exchanged assets to pay and calculate data for the payment verification.We also emphasize the ability to pledge ETH as a high -quality liquid asset in DEFI. It is just like primitive mortgagers, providing support for the most popular applications and stablecoins (such as DAI and USDE).

So, what are the best ways to classify and define ETH as assets?

Although the Bankless team believes that ETH is a “three -phase asset”, according to the classification of Robert Greer,ETH also reflects the characteristics of three different asset categories, But we believe that Bitcoin has been and will continue to become a very reliable value storage method.Saying, even so,We also believe that ETH is paving the way for a new hybrid assetEssenceAlthoughETH shows value storage attributes in the smart contract economy, but the difference between ETH and any other digital assets is that it is a programmable and cash flow asset.Essence

ETH and pledged ETH are extremely liquidity and are widely traded on many exchanges.Their liquidity ensures that they can easily liquidate and convert them to other assets and/or for various DEFI protocols.Although ETH has a greater volatility than government bonds or real estate, it is one of the most mature, valuable and widest cryptocurrencies in the world.With the launch of the spot ETH ETF, ETH’s acceptance may increase, and its volatility may be reduced.

At present, ETH and its liquidity derivatives have been used as mortgages in various DEFI protocols. They can be used not only to guarantee loans, but also to participate in liquidity pools, generate income and issue stable coins.Although ETH may not be suitable for a single asset category, its multi -faceted attributes highlight the charm of its unique assets, which is very attractive for those who want to participate in the global smart contract economy who want to participate in rapid growth.