Author: Zhou Hang

I want to start with a structural issue: US debt is not just a government financing tool, it is the cornerstone of the global financial system.And now,It is heading to a critical point.

Before continuing to analyze, I would like to add a detail: the U.S. federal government currently has about 2.4 million civilian employees, with an average annual salary of $106,000.In this way, the total annual salary expenditure of the United States for the administrative system itself is roughly around $250 billion.

Put this figure in the big plate of total federal spending (about $6.8 trillion in 2024), accounting for less than 4%.In other words, the US government’s administrative expenditure itself is actually relatively restrained and does not constitute the main cause of fiscal pressure.

What truly constitutes a “rigid structural burden” are the following four major sectors:

– Social Security Expenditure: US$1.52 trillion, accounting for 22.4%;

– Medicare expenditure: US$1.05 trillion, accounting for 15.4%;

– Defense expenditure: US$826.2 billion, accounting for 12.2%;

– Interest expense: US$950 billion, accounting for 14%.

These four items are basically “unable to be easily reduced”. Social security and medical care involve the bottom-level sense of security of the whole people, national defense involves the status of a major country, and interest expenses are the obligation to repay debts, and if they do not repay, they will default.

Therefore, there will be no significant reduction in fiscal spending in the United States, and it will even continue to increase.与此同时,美国的财政收入(税收)在当前政治和经济环境下也极难显著上调。Spend rigid and income elasticity,U.S. debt will naturally become a structural long-term problem for the U.S. fiscal.

Sooner or later, the United States will face a realistic problem: the problem of excessive debt volume must be solved.The traditional paths are nothing more than three: tax increases, expenditure reduction, and inflation implicitly reduce debt.

But these methods are all restrictive and expensive.The new channel for digital assets may be a new weapon in the hands of the United States:

My point is that the ultimate appearance of US bonds may be tokenization – US bonds themselves have become super stable coins endorsed by national sovereignty..

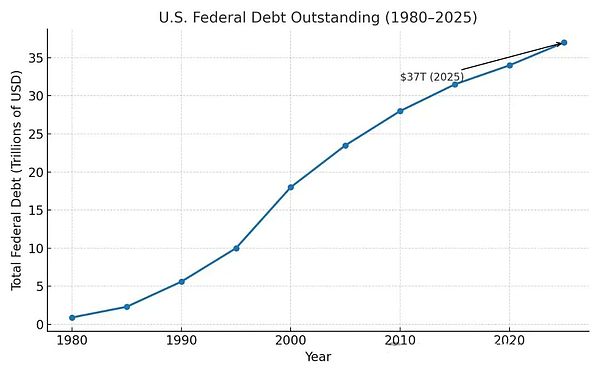

Current Situation of U.S. Treasury:A behemoth who is out of control but still believed

As of 2025, the total U.S. bonds reached US$37 trillion, far exceeding the pre-epidemic forecast.Currently, the United States adds about $1 trillion in debt every five months, more than twice the historical average.In 2019, debt accounts for 79% of GDP, and has risen to 97% by 2022, and it is only a matter of time before it breaks through 100% by 2025.

In fiscal year 2024, interest expenses for U.S. Treasury bonds have reached US$950 billion, accounting for 14% of total federal expenditure.Interest expenses almost caught up with the defense budget ($826.2 billion).Interest expenses are approaching becoming “the first rigid expenditure of the U.S. fiscal policy”, and this is the first time in history.

Before 2020, the United States will add about $1 trillion to $1.5 trillion in new Treasury bonds each year, which is a controllable and linear growth.butDuring the epidemic, in order to maintain social stability, the US government directly passed various stimulus bills and aid measures, adding US$5 to 6 trillion in government bonds in a short period of time.Most of this money is used to issue personal subsidies (Stimulus Checks), PPP small business loans, health system subsidies, and unemployment benefits.

The United States used national credit as collateral to borrow money from the global market, completing a countercyclical and stable operation that was almost “war mobilization level”.Although it is heavily in debt, it maintains social operation order and maintains the hegemony and stability of the US dollar.

Usage and mechanism of US debt:Why does it still stand?

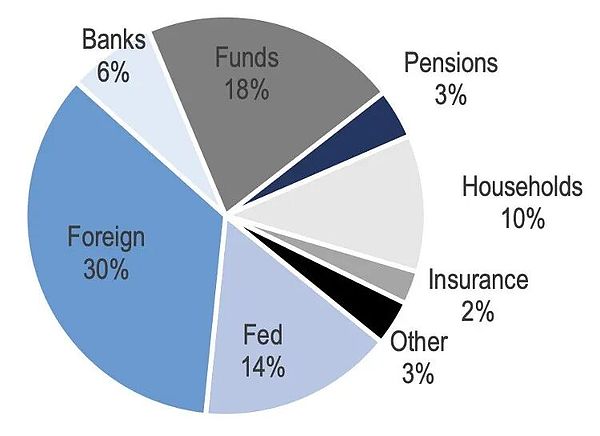

The main uses of U.S. bonds include social security, medical care, national defense and interest expenses, which constitute the vast majority of fiscal expenditure.The Ministry of Finance auctions bonds and is purchased by the market (including overseas governments).Holders include foreign governments (such as China, Japan), the Federal Reserve, pensions, banks, etc.The liquidity of US bonds is extremely high and is the settlement and mortgage base for global financial transactions.

If U.S. Treasury is the safest asset, why do people start buying Bitcoin?Digital assets are rising rapidly, and BTC/ETH has become “digital gold”; stablecoins (USDT, USDC) have begun to play the role of “on-chain USD” – USD assets are facing a revaluation of liquidity and trust.A inference at this time is:U.S. Treasury could become the next tokenized sovereign asset.

U.S. bond tokenization,The ultimate form of stablecoins

What will happen if US debt is tokenized?US Treasury bonds will become a real anchor of stability, replacing USDT, global funds will directly subscribe to US Treasury bonds on the chain, and the closed loop of US fiscal “digital seigniorage” has been initially formed.

When US bonds are tokenized, it is not only a debt instrument, but also a bottom-mounted anchor asset of the “on-chain dollar”.It can replace existing stablecoins and become a truly compliant, transparent and highly liquid “on-chain US debt version USDT”.

That is to say,The ultimate form of stablecoins may be US debt itself.This will redefine the foundation of global digital assets and may also become a conspiracy turn for the United States to solve fiscal problems.Instead of raising taxes, cutting social security, or tightening, it turns debt itself into a “stable value unit” needed by the whole world.

If this is true, if US bonds are directly posted on the chain and issued coins in the future, it will become the real ultimate stablecoin, then the problem of US bonds may be completely solved. This will be the most landmark innovative and bold move in financial history.It will also cause fundamental changes in the sovereign currencies of countries around the world.existSome small countries in Latin America and Africa may be completely dollarized or stable currency, and their local currencies will be completely replaced. Some major countries such as China, Japan, and the EU will also consider whether to issue their own stable currency. In short, there will be a fundamental change in finance.