Author: Zhao Ying, Wall Street News

Last week, it was predicted that “RMP” would hit the market. The Federal Reserve announced the launch of the Reserve Management Purchase (RMP) program as scheduled this week. Wall Street may be ushering in a feast of liquidity injection.

The Federal Reserve announced overnight that it would begin purchasing short-term Treasury bonds as needed to maintain an adequate supply of reserves.The New York Fed simultaneously announced that it plans to purchase US$40 billion in short-term Treasury bonds in the next 30 days. This is the latest move since it officially stopped shrinking its balance sheet last week..The move comes amid recent disturbing interest rate fluctuations in the $12 trillion U.S. repo market, and continued turmoil in the currency market forcing the Federal Reserve to speed up its actions.

This initiative aims to maintain adequate reserves,Although officials have repeatedly emphasized that “it is not quantitative easing,” the market has voted with actual actions: U.S. bonds, U.S. stocks, Bitcoin, gold and crude oil have all risen, and the U.S. dollar has weakened. This is a typical “quantitative easing transaction”, and investors are trying to reproduce the benefits of the liquidity feast in 2019.

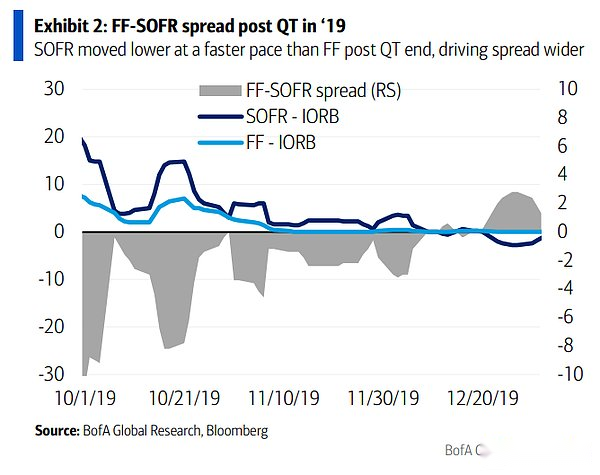

The impact of this decision on short-term financing markets is likely to be immediate.Based on experience in 2019, liquidity injection will quickly push down the Secured Overnight Financing Rate (SOFR), while the reaction of the federal funds rate (FF) is relatively lagging. This “time difference” will create significant arbitrage space for investors.

$40 billion in monthly purchases kicks off

The New York Fed’s announcement on Wednesday detailed the RMP’s operating framework.According to the FOMC’s instructions, the New York Fed will maintain adequate reserve levels by purchasing short-term Treasury bonds in the secondary market and, if necessary, purchasing Treasury bonds with a remaining duration of up to three years.The size of these purchases will be adjusted based on expected trends in demand for Fed liabilities as well as seasonal fluctuations.

Monthly RMP amounts will be announced around the ninth working day of each month, along with tentative purchase plans for the next approximately 30 days.The New York Fed’s trading desk plans to announce the first plan on December 11, when the RMP’s short-term Treasury bonds will total approximately $40 billion and purchases will begin on December 12.

The New York Fed expects RMP purchases to remain elevated in the coming months to offset an expected sharp increase in non-reserve liabilities in April next year.Thereafter, the pace of aggregate purchases could slow significantly based on expected seasonal changes in Fed liabilities.The purchase amount will be adjusted appropriately based on the reserve supply outlook and market conditions.

The FOMC said in a statement: “The Committee believes that reserve balances have fallen to an adequate level and will begin purchasing short-term Treasury securities as needed to continue to maintain an adequate supply of reserves.” This statement marks an important turn in the Fed’s balance sheet management strategy.

Federal Reserve Chairman Powell said that the Fed itself is not “worried” about tensions in the money market. “We knew this day would come sooner or later, it just came sooner than expected.”But the Fed immediately launched a Treasury bond purchase program and expects purchases to “remain elevated” for some time, suggesting officials are indeed concerned about the liquidity crunch.

RMP is not QE, but the market doesn’t care

The main goal of “quantitative easing” QE is to lower long-term interest rates by purchasing long-term Treasury bonds and MBS to stimulate economic growth.The purpose of RMP is more technical, focusing on the purchase of short-term government bonds (T-bills) to ensure that there is sufficient liquidity in the “pipelines” of the financial system to prevent accidents.

Although the Federal Reserve and purists have repeatedly emphasized that RMP is only an adjustment and not QE, the market has responded with “quantitative easing transactions”.The latest report from Bank of America’s interest rate strategy team is similar to market consensus, with the bank convinced that a large-scale liquidity injection is coming.

Bank of America previously expected that the RMP funds will be composed of two parts: one part is natural balance sheet growth (Natural Growth), which is to adapt to the natural expansion of the size of the economy and the demand for circulating currency; the other part is “backfill” (Backfill), which is expected to last for 6 months and is used to repair the gap that may be caused by the previous liquidity withdrawal.

Bank of America said that compared to QE, which is simply to lower long-term interest rates or stimulate the economy, RMP is more like a maintenance of the “pipeline” of the banking system.However, for short-term financing markets, the substantial impact is direct liquidity injection.Bank of America believes that the cash injected through RMP will quickly push down SOFR, but the response of the federal funds rate will be relatively lagging. This “time difference” creates significant arbitrage space.

Market pricing currently severely underestimates the risk of this liquidity injection.Bank of America believes that the SOFR/FF spread will quickly return to -5bp or even narrower from the current -10bp.What this means for investors is that there are clear trading opportunities in the front-end interest rates market.

Can the 2019 script be repeated?

To understand what is about to happen, Bank of America interest rate strategist Mark Cabana’s team emphasized that history has only provided one truly reference-worthy RMP case, and that was the fall of 2019.

In mid-September 2019, SOFR suddenly surged, showing an extreme shortage of liquidity in the system, known as the repo crisis.The Federal Reserve quickly launched repurchase operations and announced on October 11 that it would begin implementing RMP on October 16.The monthly RMP scale at that time was about 0.2-0.3% of GDP, and the total of repurchase operations was about 1% of GDP.

The market reaction was immediate.The injection of liquidity pushed the SOFR/FF spread to narrow rapidly from -21bp in September to -3bp in October, and further stabilized at -2bp in November.Experience in 2019 shows that cash injections can drive SOFR changes extremely quickly, while the federal funds rate shows a lag.

Bank of America pointed out that although the historical rhyme is similar, 2025 will not be a simple repeat of 2019.The current excessive withdrawal situation by the Federal Reserve is not as severe as in 2019, so the Federal Reserve’s response this time will not be as dramatic as in 2019.BofA expects monthly RMP to be about 0.15% of GDP, below 2019 levels.

Although the intensity is smaller, the logical transmission mechanism is consistent: increased cash drives SOFR to react quickly, while FF lags.This mechanism was also verified in the second half of 2021, when the Fed’s QE pushed SOFR towards zero faster than FF.Regardless of the official definition, the market is clearly ready for a new round of liquidity.