Author: Bradley Peak, Source: Cointelegraph, Compiler: Shaw Bitcoin Vision

Summary of key points

-

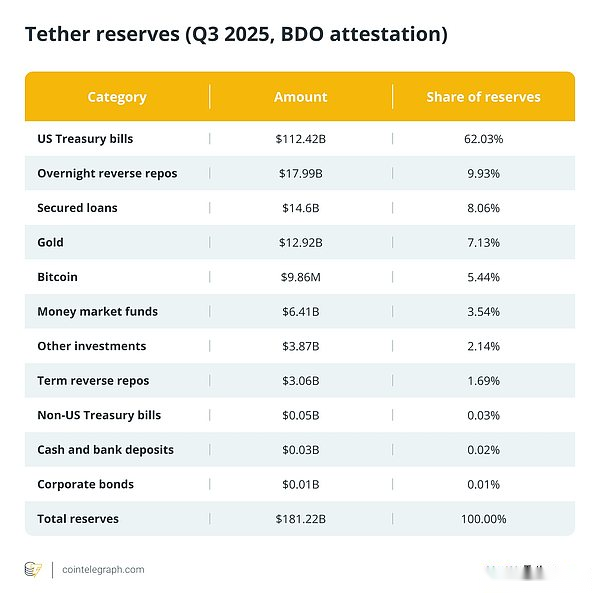

Tether’s balance sheet is dominated by treasury bonds and repurchase agreements, holding $181.2 billion in reserves, $174.5 billion in liabilities, and a surplus of $6.8 billion.

-

High interest rates have made these reserves profitable, generating more than $10 billion in interest income as of 2025, which is unusual for the average cryptocurrency issuer.

-

It used policy leverage by freezing sanctioned wallets, moving supporting blockchains, and allocating up to 15% of profits to Bitcoin.

-

There are limitations to the analogy between Tether and a central bank.Tether has no public authorization or guarantee, relies on certification rather than full auditing, and relies on private counterparties.

Tether no longer looks like a pure stablecoin company.Its balance sheet is littered with short-term U.S. Treasuries, reverse repurchase agreements, gold and even Bitcoin.It is able to mint and redeem U.S. dollars at scale, and can freeze related addresses at the request of law enforcement.

Its latest audit data shows that Tether reserves are US$181.2 billion, liabilities are US$174.5 billion, surplus is US$6.8 billion, and USDT in circulation exceeds US$174 billion.In a high interest rate environment, as of 2025, its asset portfolio dominated by government bonds has made profits of more than $10 billion, a figure that is more in line with the performance of a financial institution rather than a cryptocurrency start-up.

This is why critics and supporters alike argue that Tether acts like a private central bank pegged to the U.S. dollar in parts of the cryptocurrency economy, albeit without a sovereign mandate or safety net.

Playing the role of a central bank: what does it mean?

In fact, Tether does four central bank-like actions.

First, it issues and redeems currency on demand.Verified customers mint new USDT by sending in fiat currency and redeem it by exchanging USDT for USD.This primary market is responsible for expanding or contracting supply, while secondary market transactions occur on exchanges.The actual balance sheet changes occur during this minting and redemption process.

Second, it manages its reserves like a fixed-income arm, allocating the bulk of its assets to short-term U.S. Treasuries and repurchase agreements, supplemented by smaller amounts in gold and Bitcoin.A Treasury-heavy portfolio maintains liquidity and provides steady demand for short-dated Treasuries, something the bond sector will keep a close eye on today as it identifies key buyers of U.S. Treasuries.

Third, in a high interest rate environment, it can obtain seigniorage-like benefits.Users hold interest-free tokens, while Tether collects interest on government bonds. As of the third quarter of 2025, Tether has achieved profits of more than $10 billion and excess reserves of $6.8 billion.It is this income that makes comparisons with “private central banks” persuasive.

Finally, it leverages policy tools such as contract functionality that can freeze addresses upon request from law enforcement or sanctioning bodies.It is also able to add or remove blockchains such as Omni, BCH-SLP, Kusama, EOS and Algorand to manage operational risks.

While this is not sovereign monetary policy, it still represents proactive intervention in a dollar-like asset used by hundreds of millions of people.

Expand policy levers similar to central bank tools

Tether now intervenes in its own dollar system in a manner similar to a central bank’s policy tool.

On the compliance side, it can freeze addresses associated with sanctions or enforcement actions.It first introduced a policy of actively freezing wallets in December 2023 and has been used in specific cases, such as those associated with sanctioned Russian exchange Garantex.These are issuer-level interventions that immediately impact who can move USD liquidity on-chain.

In terms of market operations, Tether manages its reserves similar to a short-term fixed income investment portfolio, investing mainly in U.S. Treasury bonds and reverse repurchase agreements.This structure allows minting and redemption activity to match highly liquid, high-yielding assets while maintaining flexibility.

According to Tether’s latest report, this combination has helped it generate billions of dollars in profits and a sizable buffer of excess reserves.Although Tether is still a private issuer rather than a central bank, these mechanisms are similar to open market-style management.

Tether has also defined its scope of operations.It has concentrated its operations in areas with the strongest user volume and infrastructure by adding and decommissioning blockchains, discontinuing minting and subsequent support on legacy networks such as Omni, BCH-SLP, Kusama, EOS, and Algorand, while continuing redemptions during the transition period.

In addition, it is diversifying its reserves by allocating up to 15% of realized operating profits to Bitcoin, a policy that will be launched in 2023 and represents another decision at the issuer level with systemic consequences.

From stablecoin issuer to infrastructure provider

Over the past 18 months, Tether has transformed from a single-coin company into a broader financial infrastructure group.

In April 2024, Tether was reorganized into four operating divisions: Tether Finance, Tether Data, Tether Power and Tether Edu.These departments are responsible for managing Tether’s digital asset services, data and artificial intelligence projects (such as Holepunch and Northern Data), energy plans, and education projects, respectively.The reorganization formalizes a strategy that goes far beyond issuing USDT.

In terms of energy, Tether has invested capital and expertise in the Volcano Energy project in El Salvador.The project is a wind and solar power park with an installed capacity of 241 MW, designed to power one of the world’s largest Bitcoin mining projects.This project directly guarantees the normal operation of the payment and settlement system.Additionally, the company is discontinuing support for multiple legacy blockchains in order to focus liquidity on the networks with the strongest tools and demand.This operational decision has consequences for the entire ecosystem.

In order to directly enter the US market, Tether announced the launch of USAT, a US dollar token planned to be issued under US supervision and issued by Anchorage Digital Bank in accordance with US domestic regulations, in parallel with the existing offshore USDT.If launched as planned, USAT will provide Tether with a compliant onshore platform, while USDT will continue to serve global markets.

Why does this analogy not work?

Importantly, Tether is not a sovereign currency institution.

It does not set interest rates, does not act as a lender of last resort, and does not operate under a public mandate.Although the company claims to have consulted with one of the “Big Four” accounting firms to audit its reserves, its transparency still relies on quarterly confirmations rather than a full financial audit.

This gap between certification and auditing is one reason why critics reject the “central bank” label.

In addition, there are hidden dangers in the balance sheet.Tether has previously said it would reduce such exposures but has maintained a portfolio of secured loans at times.This type of asset attracts a lot of attention because terms and counterparties matter.More broadly, the company’s reliance on private banks, custodians and repo counterparties rather than sovereign guarantees means market confidence and infrastructure remain outside its direct control.

Finally, some of Tether’s most policy-like actions are primarily compliance measures, such as proactively freezing addresses listed by sanctioning bodies.

What role does Tether play in the bigger picture?

In essence, Tether looks less like a typical stablecoin issuer and more like a dollar-denominated private central bank in the cryptocurrency space.It expands and contracts supply through massive minting and redemptions, holds short-term Treasury bills and repurchase agreements, earns billions in interest income, and takes compliance actions when necessary.

However, this analogy only goes so far.It lacks public mandates or safeguards, transparency still relies on attestation reporting, and its policy actions focus primarily on compliance rather than macro-management.

Keep an eye on Tether’s reserve composition, profits, redemptions, audit progress, and how USAT’s plans with Anchorage unfold in the United States, as this will determine whether Tether’s narrative continues to resemble a central bank, or begins to diverge.