Author: TTx0x, encryption KOL; Translation: bitchain hozou

1. Preface

Galaxy Digital (NASDAQ: GLXY) is arguably the underestimated opportunity at the intersection of two of the most powerful long-term trends—encryption technology and artificial intelligence.The market is misevaluating Galaxy as a volatility crypto company, but ignoring the huge value of its “Crown Pearl” asset Helios data center.Helios is a world-class AI infrastructure platform that is expected to generate stable, high profit margins, and long-term cash flow.

The core of this investment view is that the market will eventually re-rated GLXY as it successfully transforms from a digital asset service company to a top AI infrastructure operator.The company’s recent 15-year main lease signed with AI supercomputing service provider CoreWeave – covering Helios’ current approved 800 megawatts of electricity – has verified its business model and predicts an annualized recurring revenue stream of approximately $720 million and an EBITDA margin of 90%.

Galaxy has a clear advantage over competitors who are trying to make a “Bitcoin miner’s transformation to AI”, mainly reflected in a bastioned balance sheet with more than $1.8 billion in net cash and investment, a management team with deep professional experience, and a clear path to expanding Helios to a potential 3.5 GW campus.

2. Investment view: Unlocking top AI infrastructure targets

(1) Core error pricing

Galaxy consists of two completely different business segments: traditional digital asset financial services business and emerging AI data center infrastructure business.However, the market currently evaluates GLXY only through a single perspective—i.e., crypto companies.GLXY’s price movement remains highly correlated with Bitcoin, indicating that investors have not yet priced the tailwind factors that their AI data center business offers.

(2) Unexpected acquisition opportunities

At the end of 2022, Galaxy acquired the Helios data center campus from Argo Blockchain for a mere $65 million.Argo was facing bankruptcy at that time and needed to liquidate assets.Galaxy has acquired this world-class infrastructure asset for a price that is much lower than the current replacement cost.The deal came before ChatGPT triggered an outbreak of demand for AI-driven power and data centers, which alone repositioned Galony’s growth trajectory for the next decade.

(3) Helios’ strategic assets

Helios is by no means an ordinary data center; it is a first-class infrastructure asset built specifically to meet the needs of the AI revolution.

Power Advantages:

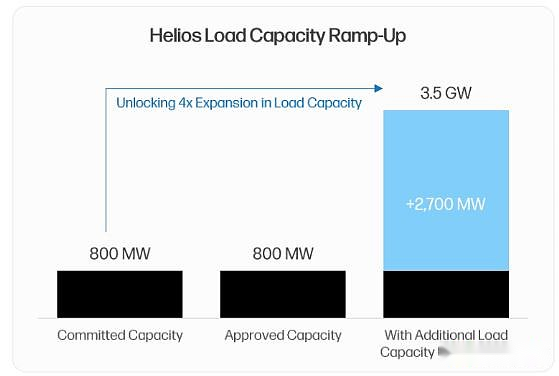

The biggest constraint faced by the AI data center industry is power supply.Power contracts are a “limiting element” in the ability of supercomputer service providers to deploy GPUs.Helios has an 800 MW approved power contract with Texas power operator ERCOT, which allows tenants to bypass the waiting period for new grid access that typically takes more than 36 months.In addition, the park has a clear and clear expansion path, and another 1.7 GW of capacity is in the load research stage, making the potential capacity of the initial site up to 2.5 GW.The latest announcement in the second quarter of 2025 disclosed that the company has acquired adjacent land and submitted a 1 GW grid access application, increasing the total potential power capacity of the park to an astonishing 3.5 GW, ranking among the world’s largest data center sites.

Scale and location advantages:

AI supercomputing service providers prefer centralized facilities to achieve economies of scale and performance advantages.Helios is perfectly suited to this mode as a single scalable campus.Its location in West Texas provides access to the cheapest and most reliable electricity resources in the United States.The key is that Galaxy is investing in long-distance fiber optic networks to ensure 10-15 millisecond transmission delays in the Dallas/Fort Worth metropolitan area.This distinguishes Helios from an increasing number of pure AI training facilities—its low-latency connectivity features unlock AI inference use cases, ensuring premium pricing capabilities.

Future-oriented design:

Any data center currently built is at risk of being outdated for several years.Galaxy avoids this risk through a phased development program, allowing for the integration of cutting-edge technologies in each new construction cycle.Advanced cooling solutions including direct chip liquid cooling are crucial for next-generation GPUs.The 10 million gallon freshwater reservoir on the campus supports these critical cooling needs.

(4) CoreWeave Partnership

The collaboration with CoreWeave is the most important verification of Galaxy AI data center strategy.In the second quarter of 2025, CoreWeave promised to lease all 800 megawatts of total power currently approved by Helios.

Transaction economy:

Its 15-year triple net lease agreement is extremely attractive.Only the first 600 MW of electricity is expected to generate approximately $720 million in revenue each year (including a 3% annual increase clause).Due to the triple net lease structure (tenants bear all operating expenses), the revenue is expected to be converted to EBITDA with a profit margin of up to 90%.

Risk resolution and value verification:

This landmark protocol achieves several key goals.First, it provides long-term predictable cash flow visibility, reducing Galaxy’s financial risks.Secondly, it strongly verifies Galaxy’s operating capabilities and establishes the company’s position as a reliable partner.This is crucial to attracting other hyperscale tenants who prefer partners with verified resumes.

3. Galaxy traditional business: the cornerstone of profitable and synergistic effects

A common bearish view on Galaxy believes that its traditional crypto business is a negative asset that increases volatility and risk.There is a misunderstanding of this view.In fact, Galaxy’s digital asset business is a profitable and market-leading entity that provides capital and reputation synergy to its other businesses.

Galaxy’s digital asset business is mainly composed of two major units: the global market (including institutional transactions, lending and investment banking services) and asset management and infrastructure solutions (including series of asset management products and pledge and other on-chain services).

Its second quarter 2025 financial data confirms the business’s strong profitability:

The adjusted gross profit of the digital asset sector reached US$71.4 million, a month-on-month increase of 10%;

Global market performance outperformed the market, with institutional loan accounts rising 27% to $1.1 billion, indicating a growing demand for its credit products;

The investment banking business demonstrates the strength of M&A consultant and is the exclusive financial advisor of Bitstamp’s acquisition by Robinhood;

Total assets of the asset management and infrastructure solution platform increased by 27% month-on-month to nearly US$9 billion;

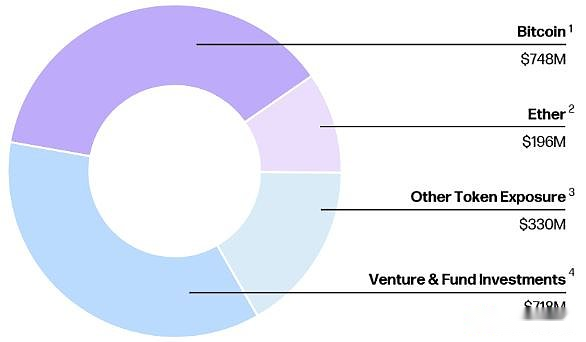

The second-quarter balance sheet showed holdings of $1.18 billion in cash and stablecoins, and $1.27 billion in digital assets (mainly BTC and ETH).

Galaxy’s profitable digital asset business not only generates cash flow, but also enhances its balance sheet strength, allowing the company to self-raise funds to complete the major equity investment part required for the construction of Helios.In addition, the business segment has proven its ability to execute large-scale complex transactions—such as the recent sale of more than 80,000 bitcoins (worth over $9 billion) for a single customer.All these traits ensure that potential supercomputer customers: Galaxy is a experienced, reliable and well-funded partner with the ability to deliver billions of dollars in infrastructure projects.This synergistic effect forms a strong self-reinforcement cycle between the two major business segments.

4. Competitive landscape: the leader in AI transformation field

Galaxy Digital is often confused with a community of Bitcoin miners trying to turn assets to AI computing hosting services.But the comparison below shows that Galaxy is unique and has become the most attractive target for investing in this theme.The competitive landscape can be divided into two levels: companies that have signed AI agreements (such as Core Scientific, TeraWulf) and companies that only claim strategic intentions (such as IREN, Hut 8, Riot).Compared with similar companies that have signed contracts, Galaxy shows obvious advantages in all key dimensions.

Galaxy’s leading position in key dimensions is specifically reflected in:

Protocol Attraction:Galaxy’s lease with CoreWeave is more economical.Its annual rental income per megawatt is higher ($1.8 million vs. $1.4-1.6 million), EBITDA margins are better (90% vs. 75-80%), and includes the 3% annual rental increase clause that competitors lack.

Balance sheet strength:Galaxy has $1.8 billion in net cash and investment.On the contrary, competitors such as CORZ and WULF are burdened with a significant net debt burden – CORZ has just recently gone out of bankruptcy and reorganization, while WULF has avoided similar fate through substantial equity dilution.These competitors’ mining businesses continue to consume cash flow, while Galaxy’s traditional businesses remain profitable.

Capacity expansion capacity:The Galaxy’s single Helios campus has a potential capacity of 3.5 GW, and its competitors’ fragmented and limited power capacity dwarfs, allowing Galaxy to capture a larger share of future demand.

Strategic focus:Galaxy has made a strategic decision: completely withdraw from the Bitcoin mining business and focus 100% on AI data center opportunities.Competitors are trying to adopt a hybrid model to distract and capital between two completely different businesses.

5. Helios valuation analysis

Helios data center business should be valuated in reference to other top listed data center REITs (real estate investment trusts) and recent private equity market transactions.The transaction multiples of publicly comparable companies such as Digital Realty and Equinix are about 25 times that of adjusted EBITDA.Private M&A transactions of data center assets are also achieved in similar multiples.

Benchmark scenario(Only currently approved 800 MW):

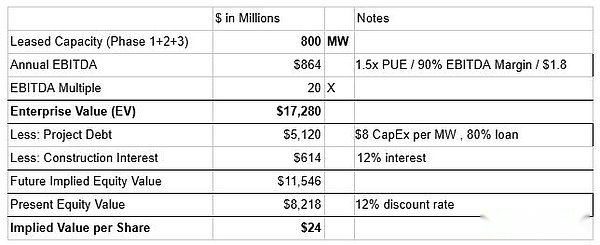

Assume that only the currently approved 800 MW is rented for an average of $1.8 million per MW.Applying 20x EBITDA multiple calculations will generate approximately US$17.28 billion in enterprise value.After deducting approximately US$5.73 billion of project-level debt and interest, the corresponding equity value of Helios is approximately US$11.54 billion.Since we expect that the annual EBITDA will be realized in 2028, we use a 12% discount rate to calculateThe current equity value is $8.2 billion, or $24 per share.

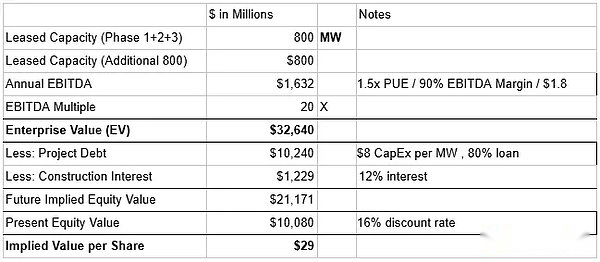

Bull market situation(Lease 1,600 MW as of fiscal year 2026):

Assume that the subsequent 800 MW of electricity, which is expected to be approved in the fourth quarter of 2025, is rented at an industry average of $1.6 million per MW.A total of 1,600 MW will generate approximately $1.63 billion in annualized EBITDA.Applying a 20-fold multiple can result in an enterprise value of about $34.5 billion.After accounting for approximately $11.46 billion of project-level debt and interest, the corresponding future equity value of Helios is approximately $21.1 billion.As we expect 1,600 MW capacity to not be fully operational until 2030, we adopt a higher discount rate of 16% to account for additional execution risks.This leads to the current equity value of $10.01 billion, or $29 per share.

GLXY is currently trading at about USD 24 (as of September 2, 2025).The benchmark scenario valuation per share for the Helios project alone has reached $24.Our valuation does not yet include Galaxy’s profitable traditional digital asset business.Bullish recently successfully completed its IPO at a valuation of $5.4 billion, and the company reported a net loss in the first quarter of 2025.If the valuation of Galaxy’s digital asset business is close to Bullish’s IPO valuation, this alone can increase the value of about $8-10 per share.

6. Key risks and mitigating factors

(1) CoreWeave tenant concentration and credit risk

The most prominent bearish arguments are the concentration risk of a single tenant CoreWeave and the question of credit reliability arising from its debt burden and lack of investment grade ratings.

Risk mitigation: CoreWeave’s business model has high income visibility, with 96% of its revenue coming from long-term commitment contracts.Its debt is mainly composed of delayed withdrawal of term loans, which are specifically used to finance growth capital expenditures based on signed client contracts.The credit has been fully underwritten by mature investors such as Blackstone, which once led major financing arrangements for CoreWeave.In addition, CoreWeave has built a lasting moat through a strategic alliance with NVIDIA, allowing it to prioritize the latest GPUs and is the only “Neocloud” operator that can meet the scale needs of top AI labs such as OpenAI.

(2) Project execution and timetable risks

The transformation and expansion of Helios is a complex multi-billion dollar infrastructure project with significant execution risks.

Risk mitigation: The Galaxy management team (particularly Chief Investment Officer Chris Ferraro) has a deep project financing and capital market expertise to mitigate this risk.The company’s strong balance sheet (recently enhanced through approximately $500 million in financing) provides an important financial buffer for unexpected costs or delays.Phase-based development strategies reduce risks by breaking down projects into manageable phases.

(3) Supervision and grid risks

Future expansion beyond the currently approved capacity could face scrutiny or delays from Texas grid operator ERCOT – the agency is closely monitoring new large load access requests.

Risk mitigation: Galaxy’s existing 800 MW of approved access capacity is a huge de-risk asset that protects it from the biggest bottlenecks faced by new projects.The approved electricity has been guaranteed.In addition, Texas regulators’ generally pro-business and anti-regulatory stance provides significant benefits for future growth compared to more restrictive jurisdictions.

7. Conclusion

In short, Galaxy Digital is an undervalued investment opportunity.The market still evaluates GLXY through a narrow perspective of volatility cryptocurrency proxy, failing to recognize its fundamental transformation to top AI infrastructure providers.

The core of the investment argument is Helios Data Center, a world-class asset that enables risk hedging through a landmark 15-year triple net lease signed with supercomputer giant CoreWeave.This cooperation not only ensures a predictable high-margin revenue stream, but also verifies Galaxy’s position as a trusted partner to realize its ambitious future expansion plan.

Our valuation analysis shows that Helios assets alone are already supporting the current share price.Its profitable traditional digital asset business continues to distinguish it from other “AI transformation” competitors, highlighting itself in a fortress balance sheet, multiple non-associated revenue streams, and a highly focused management team.Although there are risks associated with tenant concentration and project execution, Galaxy’s experienced management and robust financial status have created effective relief.As the company executes its clear roadmap and the market gradually digests the scale and stability of Helios cash flow, we expect its stock to experience a revaluation.