Author: Haotian; Source; X, @tmel0211

Let’s talk about the $USDH stablecoin bidding event of @HyperliquidX.

On the surface, it is a battle for interests between several issuers such as Frax, Sky, and Native Market. In fact, it is a “public auction” of stablecoin currency minting rights, which will change the game rules of the subsequent stablecoin market.

I will share a few views based on @0xMert_’s thoughts:

1) The competition for USDH coin rights exposes the fundamental contradiction between the demand for native stablecoins by decentralized applications and the demand for unified liquidity of stablecoins.

Simply put,Every mainstream agreement tries to have its own “money printing rights”, but this will inevitably lead to fragmentation and fragmentation of liquidity..

To address this problem, Mert proposed two solutions:

1.“Align” the stablecoins in the ecosystem, everyone agrees to use a stablecoin and share the income in proportion..The question is, suppose that USDC or USDT is the most consistent stablecoin with the strongest consensus. Are they willing to share a large portion of the profits and give them to DApps?

2. Build a stablecoin liquidity (M0 model) and use Crypto Native’s thinking to build a unified liquidity layer. For example, Ethereum is used as an interoperable layer to allow various native stablecoins to be seamlessly interchangeable.However, who will bear the operating costs of the liquidity layer, who will ensure the architectural anchoring of different stablecoins, and how to resolve the systemic risks caused by the deanstation of individual stablecoins?

These two solutions seem reasonable, but they can only solve the problem of liquidity fragmentation, because once the interests of each issuance are taken into account, the logic will be unconsistent..

Circle relies on 5.5% Treasury bond yields to make billions of dollars a year. Why should we share it with an agreement like Hyperliquid?In other words, when Hyperliquid is qualified to divest traditional issuers’ stablecoins to establish their own portal, the “left-win” model of issuers such as Circle will also be challenged.

The USDH auction event can be regarded as a demonstration of issuing “hegemony” to traditional stablecoins?In my opinion, success or failure of the rebellion is not important, what matters is the moment when the rise is raised.

2) Why do you say that, because the profit rights of stablecoins will eventually return to the hands of value creators.

In the traditional stablecoin issuance model, Circle and Tether are essentially doing middlemen business. Users deposit funds, and they use them to purchase treasury bonds or deposit Coinbase to take fixed loan interest, but most of the benefits are taken for themselves.

Obviously, the USDH incident is to tell them that there is a bug in this logic: what really creates value is the agreement that handles transactions, not the issuer who simply holds reserve assets.From the perspective of Hyperliquid, if you process more than $5 billion in transactions every day, why should you give up the annualized treasury bond yields of more than 200 million to Circle?

In the past, the first requirement was the “safety and unrestrained” circulation of stablecoins, so issuers such as Circle that have paid a lot of “compliance costs” should enjoy this part of the profit..

However, as the stablecoin market matures, the increasingly clear regulatory environment will tend to transfer this part of the profit rights to the hands of value creators.

So, in my opinion, the significance of USDH bidding is to define a brand new stablecoin income distribution rule:Whoever has the real transaction needs and user traffic will be given priority to the right to distribute income.;

3) So what will be the Endgame in the end: the payment chain dominates the voice, and the issuer becomes a “backend service provider”?

Mert mentioned that the third solution is very interesting, allowing the payment chain to generate revenue, while the profits of traditional issuers tend to be zero?How to understand?

Just imagine Hyperliquid can generate hundreds of millions of dollars in revenue in a year. In contrast, although the potential treasury bond yields to manage reserves are stable, they are “dispensable”.

This explains why Hyperliquid chose to transfer the issuance right without taking over the issuance itself, because there is no need. In addition to increasing the “credit liability”, the profits obtained by himself are far less tempting than the handling fee for larger transaction volume.

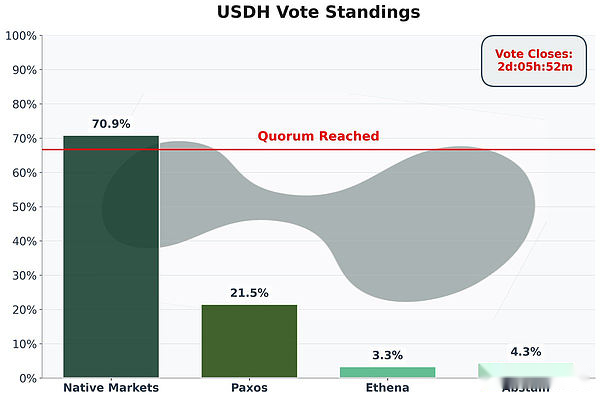

In fact, you see, when Hyperliquid transferred the issuance rights, the bidder’s reaction is enough to prove it all: Frax promised to return 100% of the profits to Hyperliquid for HYPE repurchase; Sky offered a 4.85% yield plus $250 million annual repurchase chip; Native Markets proposed a 50/50 share share, etc.;

In essence, the original battle for interests between DApps apps and stablecoin issuers has evolved into an “involved” game between issuers, especially the new issuers forcing old issuers to change the rules..

above.

Mert’s fourth solution sounds a bit abstract. It is still unknown at that point that the brand value of stablecoin issuers may be completely zeroed, or the right to issue coins is completely unified into the hands of regulators, or some kind of decentralized agreement is still unknown.That should still belong to the distant future.

In my opinion,This USDH auction battle can announce the end of the era of old and stable issuers winning, and truly guide the profit rights of stablecoin back to the “application” of creating value, which is of great significance.!

As for whether it is a “bribery” and whether the auction is transparent, I think that is a window opportunity before the GENIUS Act regulatory plan is truly implemented, and it is enough to see the excitement.