Why are the US President and the Fed Chairman always incompatible with the issue of interest rate cuts?

In the power field of American politics and economy, there is a pair of “roommates” who will never be able to live in harmony –White House President and Federal Reserve Chairman.

One stares at the votes, the other stares at inflation;

One pursues short-term prosperity, the other adheres to long-term stability;

One is keen on “release water”, the other is tightening the currency valve tightly.

This tension is pushed to the extreme in the confrontation between Trump and Powell:

First: Trump has been shouting since the day he took office: “Rate cut! Rate cut! Rate cut! Rate cut! It is best to cut from 4.25% to 1%!”

Second: Powell was almost determined to withstand the pressure and was unwilling to be the “second Burns”.

Why are the president and the Fed chairman always incompatible with the issue of “rate cuts”?To understand this issue, we need to develop from three levels: history, reality and institutional logic.

1. The President’s Political Logic: Short-term Prosperity and Election Cycle

The US President onlyFour-year term.This means:

First: If the economy is in a downturn, the unemployment rate rises, and the stock market is sluggish, voter dissatisfaction will ferment quickly.

Secondly: In order to strive for re-election or help the party maintain a majority in Congress, the president must demonstrate “economic management capabilities”, even if it is just a “illusion of prosperity.”

1. The political dividend of interest rate cuts

Rate cuts can bring a series of immediate results:

Corporate financing costs decline→ Investment and expansion accelerate;

Cheaper family loans→ Consumption and real estate demand rebounded;

Stock market benefits→ The capital market is rising, the 401(k) account becomes beautiful, and voters are in a better mood.

Under this logic, the president naturally tends to push for interest rate cuts because it is the simplest, fastest and most intuitive “economic stimulant”.

2. Data support

Looking back on history, the U.S. president’s approval rating is often highly correlated with economic data:

Reagan:When he was re-elected in 1984, the U.S. GDP grew by as high as 7.2%, the unemployment rate fell rapidly, and voters used overwhelming votes to keep him in power.

Bush Jr.:The Republicans lost the White House after the financial crisis broke out in 2008.

Biden:Before the 2022 midterm elections, it encountered great public pressure due to high inflation (CPI once exceeded 9%).

therefore,The president’s demand for interest rate cuts is essentially an investment in the probability of re-election.

2. The institutional logic of the Federal Reserve:Central Bank Independence and Historical Lessons

Unlike the president’s logic of “shortcoming quick success” and what the Federal Reserve Chairman must consider isEconomic stability over long cycles.

1. The Fed’s Responsibilities

Under the Federal Reserve Act, the Federal Reserve has a “dual mission”:

Maintain price stability (prevent inflation from getting out of control); achieve full employment.

This means that the Fed needs to make a calm judgment in the “inflation-employment” balance, rather than serving an election for a administration.

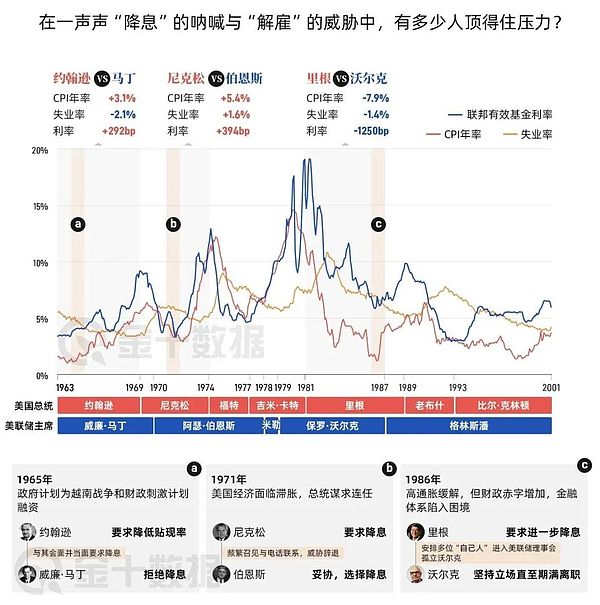

2. Nixon and Burns: A painful lesson in central bank independence

The most famous example happens in1970s.At that time, the United States fell into “stagflation”: the unemployment rate was 6.1%, and the inflation rate was 5.8%.In order to be re-election, Nixon frequently put pressure on Federal Reserve Chairman Arthur Burns.The data says it all:

In 1971, the Federal Reserve dropped interest rates from 5% to 3.5%;

M1 money supply growth rate soars to8.4%, the highest since World War II;

Nixon was successfully re-elected, creating short-term prosperity;

However, in 1973, the oil crisis and the excessive currency issuance, the inflation rate soared to more than 11%, the US dollar collapsed, and the gold price soared.

Burns was nailed to the pillar of historical shame, and his name became synonymous with the loss of independence of the central bank.

3. Powell’s persistence

Because of this, Powell has always maintained restraint in the face of Trump’s “storm”.

He is very clear: if a rashly cut interest rates will not only trigger an asset bubble, but will also put the United States in the second “stagflation trap.”History tells him:The presidency is four years and the inflation legacy may be ten years.

3. Realistic Confrontation: Trump vs. Powell

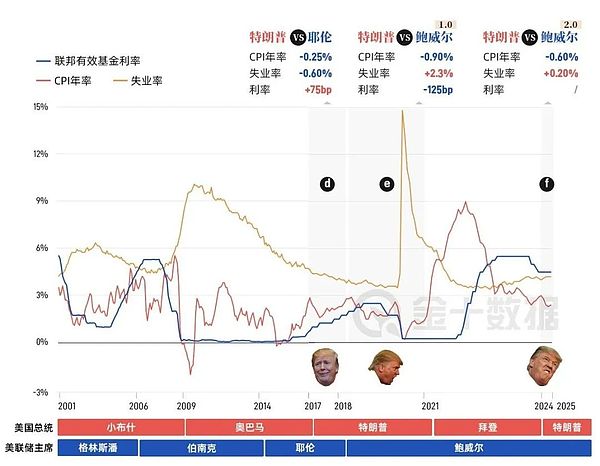

During Trump’s first term (2017-2021), this confrontation was particularly fierce.

In the next second term [2025-2029], this confrontation will be more open and upright!

1. Trump’s appeal

The trade war broke out in 2018, and the US economy faced uncertainty; in 2020, the US unemployment rate soared to14.7%, hit a new high since the Great Depression; Trump urgently needs monetary easing to stabilize the stock market, support the economy, and then support his re-election.

Therefore, he frequently criticized Powell on Twitter by name and even hinted at him to fire him.

2. Powell’s response

Faced with the interest rate of 4.25%, Trump demanded a drop to 1%; Powell withstood the pressure and insisted on gradual interest rate cuts rather than “one-size-fits-all”;

This made Trump angry, and he believed:Powell directly affected the US economic recession, allowing the US to continue to maintain the era of high interest rates!

3. Data verification conflict

Data 1: After the Fed cut three slight interest rates, the S&P 500 rose for the whole year28.9%The GDP growth rate of the United States remains at2.3%;

Data 2: However, the impact of the epidemic in 2020 caused the economy to shrink by -3.4% throughout the year, setting the worst record since World War II;

Data Three:High unemployment rate with high interest rates and unsatisfactory non-farm data.

visible,The president’s political pressure forms a direct conflict with the Federal Reserve’s “prudential rhythm”.

4. The institutional roots of contradictions: central bank independence and fiscal expansion

Why is this kind of conflict always inevitable?The reason lies in the institutional design itself.

1. “Monetary and Fiscal Misalignment”

The president is in charge of fiscal policy and likes to stimulate the economy through tax cuts and expanding government spending; the Federal Reserve is in charge of monetary policy and must suppress inflation through interest rate hikes or balance sheet reduction.

This leads toFinance is stepping on the accelerator, currency is stepping on the brakes.

2. “Short-term political cycle vs. long-term economic cycle”

The president’s timetable is a four-year election cycle; the Federal Reserve’s consideration is a decade or even twenty years of macro stability.

These two schedules are naturally misaligned, which determines that the interests of both parties are difficult to agree.

3. “Debt Burden and Inflation Control”

Currently, the US federal debt has exceeded$36.2 trillion, fiscal deficit accounts for close to GDP6%.

If interest rates remain high, the cost of debt interest will rise sharply (the interest expenses for U.S. Treasury bonds have reached 2024$1.1 trillion).

Therefore, the president and the Treasury Department would rather cut interest rates to ease debt pressure.But from the Fed’s perspective, this may amplify inflation risks.

5. Understand the King’s “rogue tactics” andPowell’s bottom line

Now there are less than 10 left before Powell’s term endsMonth [May 23, 2022 – May 15, 2026], Trump began to turn his finger from policy to individuals.

This means:

First: If Powell insists on not cutting interest rates, Trump may put further pressure on him or even use political resources to force him to compromise;

Second: If Powell compromises, the United States may once again go to the “Burns trap”, that is, short-term prosperity is exchanged for long-term inflation;

Third: If the two sides are in a stalemate until the general election, Powell’s historical positioning may depend on this last year.

Powell understood in his heart:After abdication, Trump can do whatever he wants; During his tenure, he must uphold the independence of the central bank, otherwise he will be infamous for thousands of years.

6. The inevitable conflict of power games

From Nixon and Burns, to Trump and Powell, and even any future president and Fed chairman,The dispute over interest rate cuts cannot disappear.

Because this is not a simple policy difference, but an inevitable conflict between institutional design and interest demands:

What the president wants is short-term political dividends;What the Fed wants is long-term economic stability.

History has repeatedly proved that when the central bank succumbs to political pressure, inflation is often out of control and the cost is ultimately borne by all people.

Therefore, today Powell would rather be called “Iron Head” than be the “second Burns”.

And this tug-of-war on “rate cuts” is destined to run through all cycles of American politics and economy.

A summary of one sentence:What the president wants is votes, and what the Federal Reserve holds on credit.The incompatibility between the two is a true portrayal of the normal operation of the American system.