Author: Michael Roberts

The gap in the U.S. economy is growing: on one side is rising inflation and on the other side is employment.According to mainstream Keynesian theory, this should not happen.This is because weak labor market should lead to wage growth and consumer demand falling, and price inflation will fade.The experience of economies in the 1970s overturned the theory, which was supposedly supported by the so-called Phillips curve, i.e., the trade-off between rising prices and unemployment.Inflation broke out and unemployment soared.The 2010s after the Great Recession overturned this theory again, when inflation in major economies fell back to near zero and unemployment was at an all-time low.Inflation rose sharply during the post-COVID-19 pandemic period from 2021 to 2024, but the unemployment rate remained low.

Why is Keynesian theory wrong?Because Keynesian theory assumes that total demand drives spending and price.If demand exceeds supply, prices will rise.However, during these two periods, whether in the 1970s or 1910s, the driving force was the supply side, not the total demand.In the 1970s, crude oil prices soared as economic growth slowed down due to plummeting capital profitability and investment growth, followed by oil producers restricting energy supply.In the 1910s, economic growth was slow and inflation fell, but unemployment did not rise.In the 1920s, the post-epidemic recession led to collapse of global supply chains, rising energy prices and a decrease in skilled workers.This is a supply-side problem.

Monetary theory was also exposed during these periods.Central banks – especially the Federal Reserve under Ben Bernanke – Bernanke is a disciple of Milton Friedman, the founder of monetaryism, who claims that inflation is essentially a monetary phenomenon (i.e. money supply drives prices) – believe that the answer to the Great Recession of 2008-2009 is to lower interest rates and increase the money supply through so-called quantitative easing (QE), which means that the Fed “prints” money and buys government and corporate bonds from banks, which in turn is expected to increase loans to companies and households (money supply) to promote consumption.But this didn’t happen.The real economy is still in a depression, and all currency injections have only pushed up the prices of financial assets.Stocks and bond prices soared.Monetaryism once again ignores the real driving force of economic growth, expenditure and investment: the profitability of capital, that is, the supply side.

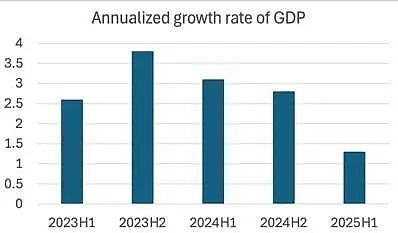

Last February,In an article, I pointed out that there are “signs of stagflation” in the US economy.”Staxia” means that national output and employment are stagnant or slow growth, while price inflation continues to rise or even accelerates.The U.S. economy has obviously been slowing down.Quarterly growth rates are unstable, mainly due to large fluctuations in imports.Early this year, imports surged as businesses tried to “snatch” Trump’s hike in import tariffs; then, as tariffs began to affect imported parts needed by industries, real GDP growth slowed.But in the first half of this year, during Trump’s administration, the economy slowed down significantly.

Indeed, economic growth is declining, close to what some analysts call “stall speed” – below this speed, the economy will fall into recession (a direct decline in GDP).The U.S. economy has not yet fallen into recession as profits in the U.S. corporate sector are still growing, and the AI investment boom is still driving the development of key economic sectors.But now, stagflation is no longer just a glimmer of light in the economic air as it was in early 2025.

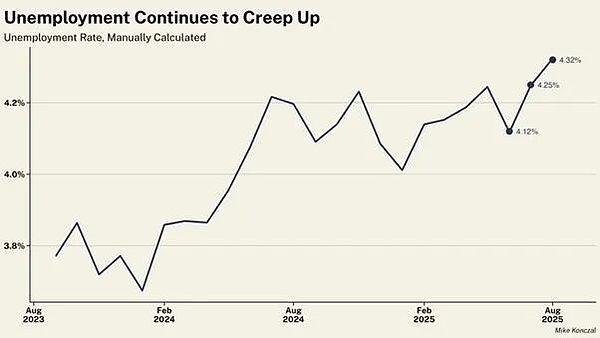

Taking employment as an example, employment growth is slowing down rapidly and the unemployment rate is also rising.

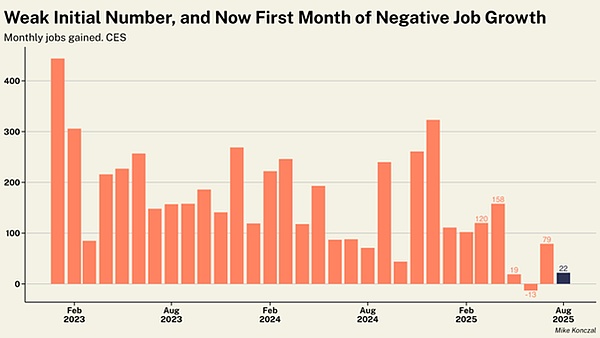

Net jobs rose only 22,000 in August, while net jobs were lowered to a decrease of 13,000 in June.

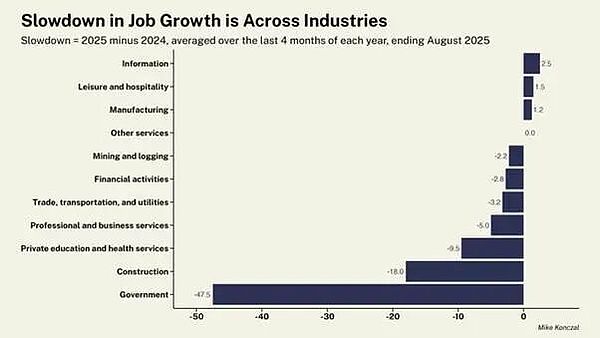

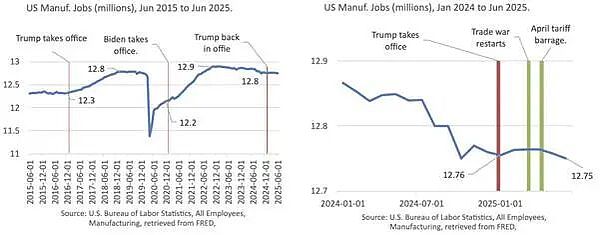

Trump’s economics believes that tariffs will increase manufacturing jobs, while federal layoffs will free up more labor.This is simply impossible.The rate of loss of jobs in manufacturing is almost as fast as the federal government’s labor force is lost (-12,000 vs -15,000).Employment growth in almost all industries is slowing.

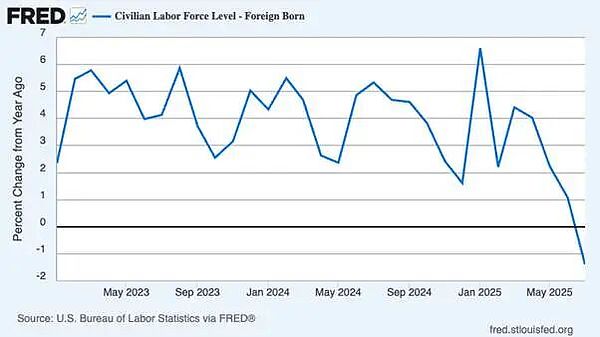

Men are particularly unemployed.In the past four months, the number of male unemployed people has reached 56,000.The main reason is that Trump’s suppression of immigration policies has led to a sharp decline in the number of labor.The U.S. Immigration and Customs Enforcement (ICE) is conducting mass arrests and deportations, but the number of foreign-born workers in the U.S. has begun to shrink after years of rapid growth.Locally born workers have not benefited from it – their unemployment rate has reached its highest level since the end of the pandemic.Both youth and black unemployment rates have risen (currently at 7.5%, the highest since October 2021), suggesting that the suppression of immigration has not created a more favorable job market for the more vulnerable groups in the U.S. workforce.

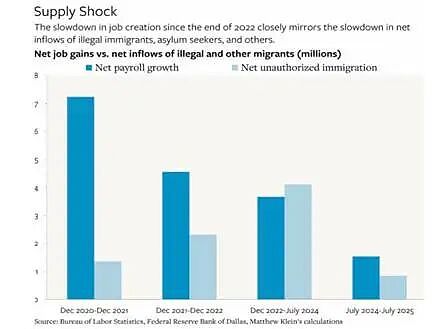

Trump fired the Director of the Bureau of Labor Statistics because the bureau released job growth data was very weak.But since then, annual revisions to employment data have led to job growth in the year ended March 2025Reduced911,000.Dismissal of the messenger does not change the nature of information transmission.U.S. job growth has slowed to levels outside of a recession that has not been seen in more than 60 years.Employment growth slowed not because of weak demand, but because supply growth is drying up as immigration declines, manufacturing continues to decline, and government agencies and labor force hit hard by Trump.

The fundamental problem is that insufficient demand is not a factor that restricts the development of US manufacturing, but a labor force.The number of workers who can and are willing to work in factory workshops is decreasing.According to the United StatesBureau of Labor StatisticsAccording to data, there are currently nearly 400,000 vacancies in manufacturing.

The decline in productive workers means slowing economic growth.The Fed is helpless in this, whether it is cutting interest rates or increasing currency injection (quantitative easing).Even if Trump succeeds, fires some Fed directors, then takes control of the Fed, and significantly lowers the Fed’s policy interest rate, it will only further fuel the stock market speculation boom and will do little to the productive sector of the economy.

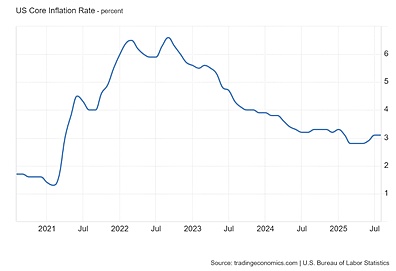

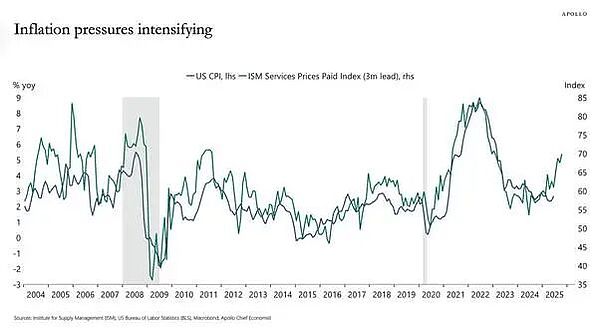

The current Fed’s board of directors is reluctant to cut interest rates because they fear inflation will accelerate.Inflation has risen.The latest consumer price index (CPI) accelerated to 2.9% year-on-year in August 2025, far higher than the Fed’s 2% inflation target.The Fed tends to track its so-called personal consumption expenditure (PCE) inflation rate.This inflation rate has always been far lower than the average price increase in household consumer goods in the United States.But even PCE inflation rate is still higher than the Fed’s 2.6% year-on-year target.The core inflation rate (excluding energy and food prices) is stubbornly staying at the 3.1% year-on-year level.

Again, the rise in inflation is not due to the demand for goods and services exceeding supply; it is due to slowing production and rising production costs, especially in service industries such as utilities and medical insurance.

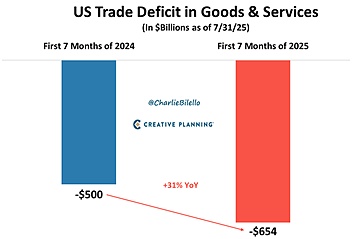

Trump administration officials argued that tariffs had no effect on inflation.But if this is true, it means that the “supply shock” of the price will happen no matter what.Admittedly, so far the tariffs have had limited impact.This is because Trump was angry at the beginning, and American importers rushed to increase their inventory and took action before the tariffs were raised.This is why U.S. imports soared in the first half of 2025 and the U.S. trade deficit sharply worsened.

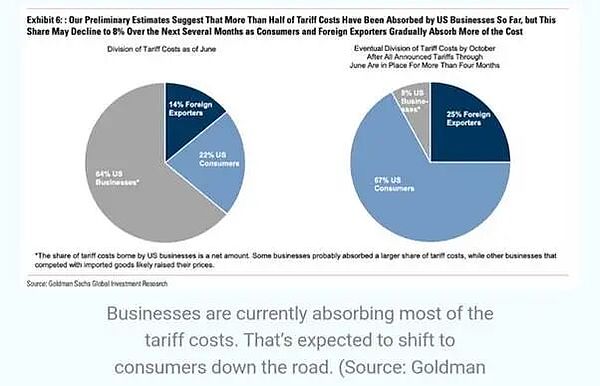

In addition, some exporters to the United States have lowered prices to absorb the impact of tariffs on import prices.But the tariff hike will eventually be reflected in consumer prices.An analysis by Goldman Sachs shows that about 22% of the tariff costs have been passed on to consumers.Goldman Sachs estimates that this ratio will eventually rise to 67%.

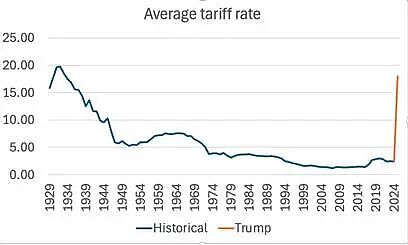

Given that the current effective tariffs on imports are about 18% (up from about 4% before Trump took office) and imports account for about 14% of U.S. GDP, this can only mean inflation in the next 12 monthsWill furtherThe rise was about 1.5 percentage points, bringing U.S. inflation to 4.5-5%.

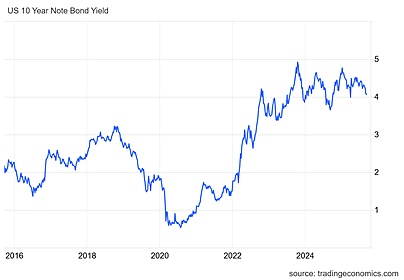

It is this potential inflation rise that has concerns government bond investors in financial markets.They want higher yields to compensate for the reduction in real returns caused by rising inflation.So, even if the Fed lowers its short-term interest rate, we expect U.S. long-term government bond yields to rise.

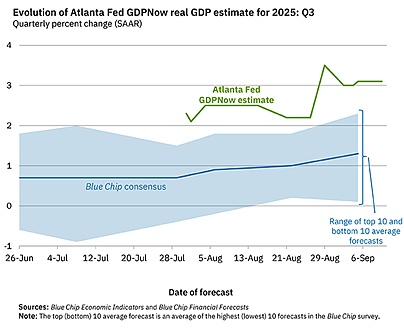

Therefore, the driving force of stagflation is increasing.However, this does not mean that the U.S. economy is about to fall into a complete recession.A recession refers to a decline in total output (mainstream economists like to call a “technical recession” for two consecutive quarters).The National Bureau of Economic Research (NBER) tracks recession, and use various indicators to “predict” recession.But NBER’s judgment is always retrospective (i.e. after the recession is over).NBER has not declared a recession so far.There are other predictive models trying to track the pace of U.S. economic expansion.The Atlanta Fed GDP Now model is very popular.The model currently predicts that the annualized growth rate of real GDP in the U.S. in the third quarter of this year is 3.1%—although it should be noted that the consensus among all major forecasting agencies is around 1.3%.

The New York Fed also has a predictive model.New York Fed staff’s forecast for the third quarter of 2025 is currently 2.1%.Again, this is an annualized growth rate, unlike quarterly or year-on-year growth rate.But so far, regardless of the measurement or model, the U.S. economy is expected to continue to expand from June to September this year, despite a slowdown in growth.

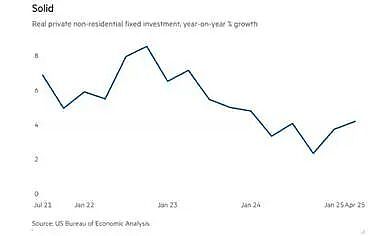

I and other scholars point out that the economy falls into recession only when corporate investment shrinks sharply, and corporate investment only recession when profits begin to decline.So far, corporate investment has maintained positive growth, with an annual growth rate of about 4%.

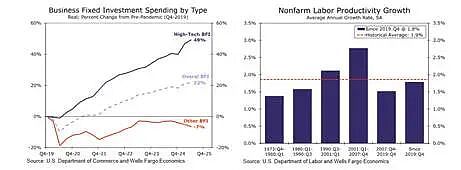

However, a large portion of the growth in corporate investment is concentrated in the high-tech AI fields, such as data centers and other infrastructure, in an effort to drive the so-called AI boom.Since 2019, corporate investment in the sector has grown nearly 50%, while investment in other sectors of U.S. enterprises has declined by 7%.The impact of high-tech AI investments slightly increased the growth rate of labor productivity, but remained below levels in the 1990s and early 2000s.If the AI investment boom fades, corporate investment will drop significantly.

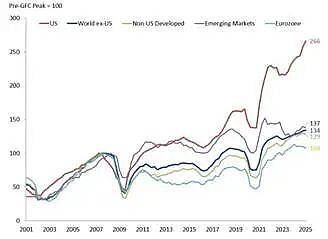

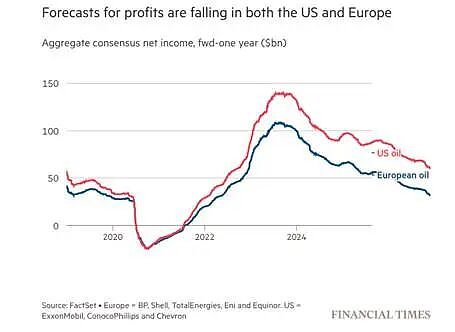

In terms of profits, U.S. businesses far outperform other regions.Since its pre-global financial crisis, U.S. corporate profits have soared 166%, far exceeding other regions.By contrast, euro zone corporate profits have barely changed, up just 8%.

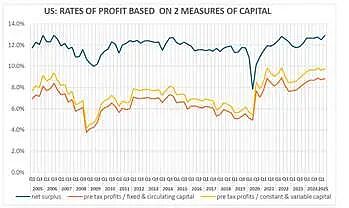

The profitability of US capital has improved since the end of the sluggish epidemic in 2020. According to Brian Green’s calculations, US corporate pre-tax capital profit margins are already at a level higher than those in 2006.

Source: https://theplanningmotive.com/2025/08/30/us-corporate-profits-2025-q2-plateauing-but-yet-to-collapse/

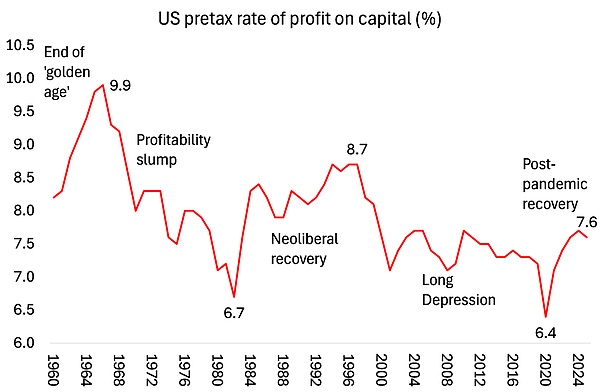

My own calculations of the U.S. profit margin since the end of the Great Recession and after the COVID-19 pandemic are similar.

Source: EWPT 7.0 series, Basu-Wagner et al., AMECO, author calculations

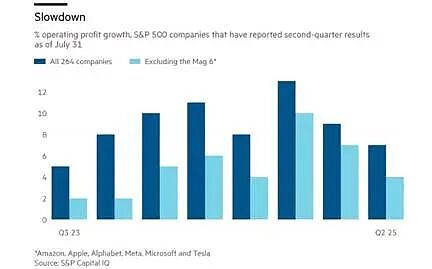

Corporate profits are still growing.Operating profits of S&P 500 companies (excluding financial stocks) rose 9% year-on-year in the latest quarter.But this figure contains huge profits from the so-called “seven high-tech companies”.If these companies are excluded, the profit growth of the remaining non-financial and non-energy companies is about 4-5%, and the growth rate is slowing down.The profit growth of these companies is being squeezed by rising production costs.This squeeze will be further intensified as import tariffs push up the prices of parts and raw materials.

In addition, crude oil prices continued to fall, resulting in a decline in profits in the US energy industry.Global capital expenditure on oil and gas production is expected to fall by 4.3%, the first annual investment decline since 2020.Energy companies are laying off employees, cutting costs and reducing investment at the fastest pace since the pandemic plummeted.The US shale oil industry has been hit particularly hard.

Trump and the “Make America Great Again” team claim that tariffs will bring huge taxes ($1.8 trillion) and new business investment (an additional $3-5 trillion) to boost economic prosperity (they claim the economy will grow 4% next year) and create hundreds of thousands of new jobs.But there is no evidence for these statements.

As of August 2025, the total actual tariff revenue was approximately US$134 billion.Meanwhile, the federal government’s budget deficit shows no sign of shrinking, but insteadHave weakened.The Big Beautiful Bill Act passed by Trump in July promised to cut the deficit, but current forecasts show that the deficit is still ongoing.The U.S. Congressional Budget Office (CBO) expects the federal budget deficit to reach $1.9 trillion in fiscal 2025.Tariff revenue this year is expected to account for only a small part of federal revenue, at just 2.4%.

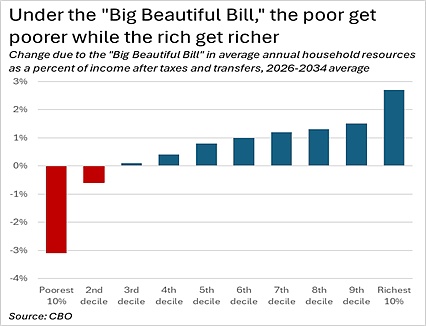

During the Trump administration’s years to come, corporate tax and income tax cuts targeting high-income earners will reduce potential incomes far exceeding the increase in tariffs.In fact, these tax cuts will constitute the largest income transfer historically by the government from the poor to the rich.

Tariff revenue will not lower the federal government’s annual deficit, which currently accounts for more than 5.5% of GDP (even if growth slows slightly).In fact, the annual deficit is expected to rise to 5.9% of GDP over the next decade, and the ratio of public debt to GDP will reach 125% of GDP.The rising public debt ratio is another concern for government bond investors, so no matter how the Fed lowers short-term interest rates, it will push up bond yields.

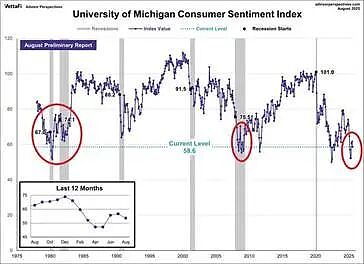

American families are feeling financial pressure.Consumer confidence indexes in the economy have fallen to one of the lowest levels of the century, comparable to those during the financial crisis and the recession in the 1980s.

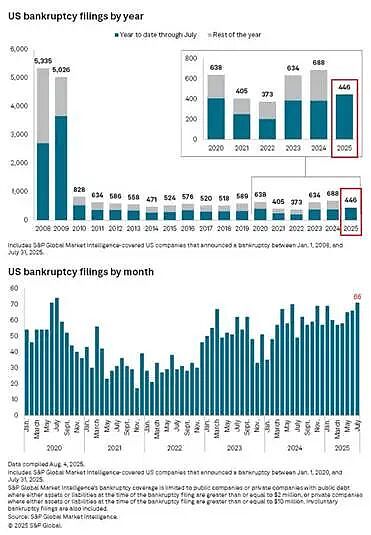

The weakest part of the business world is struggling.446 companies have gone bankrupt so far this year, setting a record high in 15 years.

At the beginning of this article, I pointed out that the US economy is entering a period of “stagflation”, that is, both inflation and unemployment rates have risen.Stagflation shows that both Keynesian and monetary inflation theory are wrong.This means that no matter what the Fed takes in interest rates or currency injection, it has little impact on inflation or employment—the central bank’s so-called targets.

Whether inflation and unemployment rates decline depends on whether the U.S. real GDP and productivity growth recover.This depends on whether corporate investment continues to grow.Ultimately, it depends on whether the company’s profitability and profits remain unchanged or declined.So far, there has been no decline, but signs of downward trend are showing.