Key takeaways

-

Cut the interest rate by 25bp, Miran supports the cut by 50bp, and Schmid still opposes the cut.Goolsbee joins opposition,Disagreement further intensifies.

-

Expressed concern about the rising unemployment rate and found reasons for this interest rate cut.

-

reproduced in statement“Degree and timing” set the tone for subsequent action or inaction.

-

announceRestart asset purchases (table expansion) for reserve management targets, the scale isUS$40 billion in first month, in addition to short-term U.S. Treasury Bills, it also includes Coupons within 3 years.This is not QE, this is RMP.In addition,Restrictions on the standing repurchase facility have also been lifted.

-

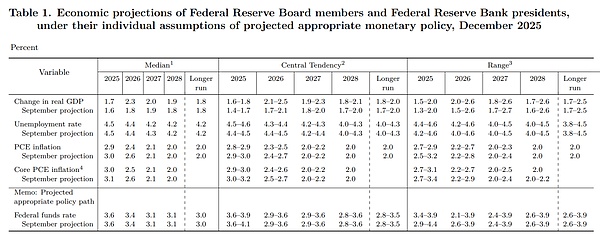

Economic forecasts reveal the Fed’s optimism about the outlook for the economy and inflation.

-

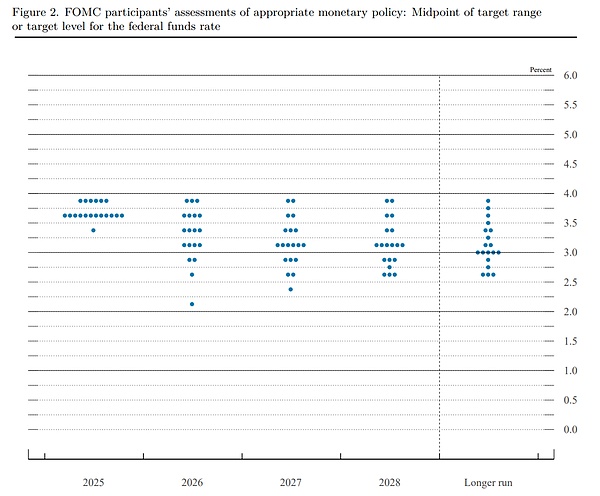

The dot plot shows a more dovish prediction point (nearly 2%).

-

Don’t even think about raising interest rates.

Statement (key changes in bold)

Available indicators suggest economic activity has been expanding at a moderate pace.Employment growth has slowed this year, and the unemployment rate rose slightly as of September.Recent indicators are consistent with these developments.Inflation has picked up since earlier this year and remains somewhat elevated.

The Committee strives to achieve full employment and an inflation rate of 2 percent in the long run.Uncertainty about the economic outlook remains high.The Committee is concerned about risks on both sides of its dual mandate and concludes that downside risks to employment have increased in recent months.

In support of its objectives and in light of the shift in the balance of risks, the Committee decided to adjust the federal funds rate toHeadThe target range is lowered by 1/4 percentage point to 3-1/2% to 3-3/4%..While considering additional adjustments to the target range for the federal funds rateextent and timingAt this time, the Committee will carefully evaluate subsequent data, the evolving outlook, and the balance of risks.The Committee remains firmly committed to supporting maximum employment and restoring inflation to its 2 percent objective.

The Committee will continue to monitor the impact of subsequent information on the economic outlook as it assesses the appropriate stance of monetary policy.The Committee will be prepared to adjust the stance of monetary policy as appropriate if risks arise that could impede achievement of the Committee’s objectives.The Committee’s assessment will consider a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, as well as financial and international developments.

The committee has judged that the reserve balance has dropped to ample levels and will initiate the purchase of short-term government bonds as needed to continue to maintain an adequate supply of reserves.

Voting in favor of this monetary policy action were: Chairman Jerome H. Powell; Vice Chairman John C. Williams; Michael S. Barr; Michelle W. Bowman; Susan M. Collins; Lisa D. Cook; Philip N. Jefferson; Alberto G. Mussallem; and Christopher J. Waller.Voting against the action were: Stephen I. Milan, who favored lowering the target range for the federal funds rate by 1/2 percentage point at this meeting;andAusten D. Goolsbyand Jeffrey R. Schmid, who prefer to keep the target range for the federal funds rate unchanged at this meeting.

economic forecast

More optimistic economic forecasts, lower inflation forecasts and unemployment forecasts.(soft landing)

Bitmap

Although the median has not changed, theThe divergence is large, with a more extreme single point appearing (an interest rate forecast close to 2%).

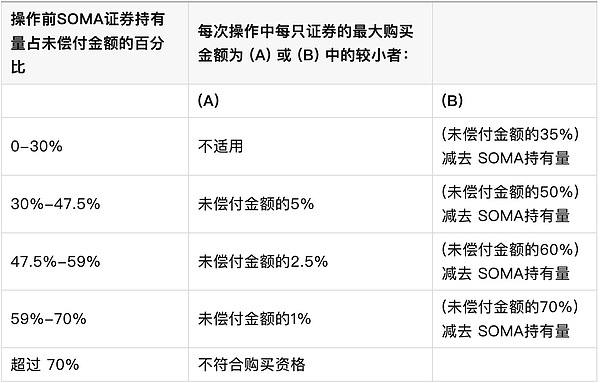

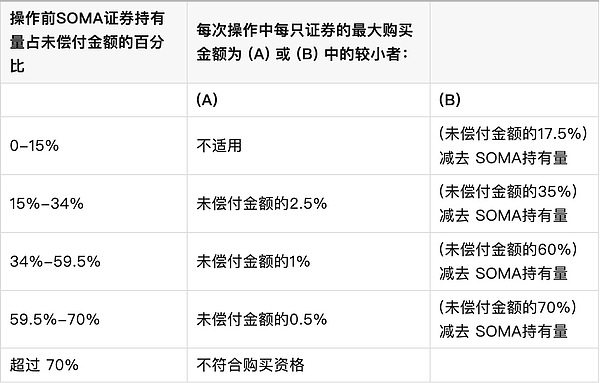

RMP details (provided by the New York Fed)

Please note that for the convenience of understanding and the confusion of the term “Treasury Bill”, the Bills in the following are “short-term U.S. bonds”, and the Coupons with a maturity exceeding the Bill are U.S. bonds with a shorter maturity. This purchase includes Coupons with a maturity of less than 3 years.

On December 10, 2025, the Federal Open Market Committee (FOMC) directed the Open Market Operations Desk of the Federal Reserve Bank of New York (the “Operations Desk”) to increase the holdings of securities in the System Open Market Account (SOMA),Maintain adequate reserve levels by purchasing short-term Treasury bonds (or, if necessary, Treasury bonds with remaining maturities of three years or less) in the secondary market.The size of these reserve management purchases (RMPs) will be designed to accommodate projected trend increases in Fed liability requirements as well as seasonal fluctuations, such as those driven by tax dates.

Monthly reserve management purchase (RMP) amounts will be announced on or about the ninth business day of each month, along with a preliminary purchase operation schedule for approximately thirty days thereafter.The operating platform plans to release its first timetable on December 11, 2025.Total RMP is approximately $40 billion; purchases to begin December 12, 2025.The operating table is expected toThe pace of RMP will remain elevated in the coming months to offset the large increase in non-reserve liabilities expected in April.Thereafter, the overall pace of purchases is likely to be significantly lower, in line with expected seasonal patterns in the Fed’s liabilities.The purchase amount will be adjusted appropriately based on the reserve supply outlook and market conditions.

The desk was also directed in October to reinvest all principal payments on agency securities held by the Fed into short-term Treasury securities through secondary market purchases.The monthly planned purchase schedule will include RMPs as well as these reinvested purchases.

The desk plans to allocate monthly secondary market purchases to two short-term U.S. Treasury bond sectors.The purchase amount for each sector will be determined by the sector weight.These sector weights will be based on the 12-month average of the outstanding face value of short-term U.S. debt in each sector relative to the total outstanding amount of the two sectors as of the end of September 2025.

The following frequently asked questions (FAQs) provide additional information about the Federal Reserve’s trading of Treasury securities in the secondary market.

What are the current policy directives regarding direct Treasury bond operations from the Desk?

On December 10, 2025, the Federal Open Market Committee (FOMC) directed the Open Market Operating Desk (the Desk) of the Federal Reserve Bank of New York (Federal Reserve Bank of New York) to increase securities holdings in the System Open Market Account (SOMA),by purchasingshort-term U.S. debt(Purchase other Treasury bonds with remaining maturities of three years or less as necessary) to maintain adequate reserve levels.Additionally, the FOMC directed the operating desk to continue to reinvest all principal payments received on agency securities held by the Federal Reserve inshort-term U.S. debt.

How will the console determine the monthly secondary market Treasury bond purchase amount?

As directed by the FOMC, monthly purchases of Treasury securities in the secondary market will include: reserve management purchases (RMPs) used to increase SOMA’s portfolio to maintain an adequate reserve position, and the reinvestment of proceeds from principal payments on agency securities.

The size of the RMP will be designed to accommodate seasonal fluctuations in Fed liability requirements (such as those driven by tax dates) as well as trend increases over longer periods of time.To ensure reserves remain ample, purchases may be increased ahead of an expected trough in reserves and then reduced during periods when demand for the Fed’s liabilities is lower.Monthly reinvestments in agency securities will consist of monthly principal payments on agency debt, agency mortgage-backed securities (MBS) and agency commercial mortgage-backed securities (CMBS) holdings.Reinvestment of agency debt and MBS holdings will be based on expected principal payments during the current month, while reinvestment of agency CMBS holdings will be based on actual principal payments during the previous month.

The operating desk will announce the amount of secondary market Treasury bond purchases for that month around the ninth working day of each month, and will also publish a tentative monthly operating schedule, which is expected to take place between the middle of that month and the middle of the next month. The schedule will convey the operation date, time, security type, maturity and maximum transaction amount.

What Treasury securities will the desk operate?

In accordance with the FOMC’s directive, the console will allocate the reinvestment of proceeds from agency securities toshort-term U.S. debt.RMP will also typically point toshort-term U.S. debt; However, depending on market conditions, the Operator may allocate some or all of such purchases to other Treasury securities with remaining maturities of three years or less.

Buyingshort-term U.S. debtAt that time, the operating table will calculate the outstanding balance of each segment based on the 12-month average as of September 2025.short-term U.S. debtproportional to the denomination, allocating purchases to two sectors.The table below shows the specific sectors and approximate sector weights that the console will use.Sector weightings are subject to change and will be re-evaluated periodically.

Short-term U.S. Treasuries (BILLS)

If market conditions require that some or all of the RMPs be directed to Treasury coupon securities with remaining maturities of three years or less, the console will allocate those purchases to the two Treasury coupon segments in proportion to the face value of outstanding coupon securities in each segment based on the 12-month average through September 2025.The table below includes the specific sectors and approximate sector weights that the console will use.Sector weightings are subject to change and will be re-evaluated periodically.

COUPONS

The operating platform’s monthly purchase schedule for secondary market purchases will communicate the specific sectors and term range for each operation in advance.The Desk expects to trade across the entire tenor range of each sector in most operations; however, in some cases, the Desk may not always trade across the entire tenor range of a sector for reasons of market functioning and operational efficiency.The Desk will avoid purchasing securities that have extremely high scarcity values in the repo market for specific collateral, securities that are four weeks or less from maturity, securities that trade in the when-issued market, securities that are the cheapest to deliver on active Treasury futures contracts, and cash management notes.Specific exclusions from the issuance of securities will be announced at the commencement of each operation.

What is the limit on the amount of any single Treasury bond issue held by SOMA?

The operator will cap SOMA’s holdings of any single Treasury security at 70% of the total outstanding amount of that security.

What is the limit on SOMA’s purchase of any single Treasury bond issue?

The console only allows SOMA’s share of a single Treasury security to exceed a certain level in modest increments.

For nominal coupon securities, Treasury Inflation-Protected Securities (TIPS), and Floating Rate Notes (FRNs), the console allows SOMA’s share of a single Treasury security to exceed 35% in the increments shown below.

Purchase limits for nominal coupon securities, TIPS and FRNs

forshort-term U.S. debt, the console allows SOMA’s share of a single Treasury security to be held in excess of 17.5% in increments as shown below.

Purchase limits for short-term U.S. Treasury bonds

Will the Fed lend out the Treasury securities it owns?

Yes, Treasury securities held by SOMA can be borrowed through the SOMA Securities Lending Program.For more information about securities lending, see here.

How are SOMA’s holdings of Treasury securities reported?

SOMA Treasury holdings are reported weekly in the H.4.1 statistical release.Changes in H.4.1 line item “U.S. Treasury securities” during any period reflect the net impact of rollovers, purchases and sales of Treasury securities, as well as changes in inflation compensation.

Who is eligible to conduct direct operating transactions on Treasury securities with the Federal Reserve?

Primary dealers at the New York Fed are eligible to conduct direct operating transactions on Treasury securities directly with the Federal Reserve.Dealers are expected to submit buy and sell quotes on behalf of themselves and their clients.

How does direct manipulation work?

The console conducts direct operations on government bonds through FedTrade (the console’s proprietary trading system).FedTrade operations are typically conducted using multiple-price, competitive auctions and approved counterparties.A “multi-price” auction is an auction in which securities are awarded at prices corresponding to participants’ bid or ask quotes in the operation, resulting in securities being awarded at multiple prices.The minimum auction amount, buy/sell size and buy/sell increment are all US$1 million.Participants may submit up to nine buy or sell quotes for each security, with each quote reflecting price and denomination.forshort-term U.S. debt, the bid and ask quotes will be entered in the form of interest rates, while for FRN, the bid and ask quotes will be entered in the form of discount margin.

Proposals in FedTrade operations will be evaluated based on their proximity to prevailing market prices at the end of the auction and relative value indicators.The relative value indicator is calculated using the New York Fed’s proprietary model.

How will the operation console communicate the results of the operation?

The results of the operation will be posted on the New York Fed website after each operation.Information posted will include the total number of proposals received, the total number of proposals accepted, and the amount purchased or sold for each issue.In addition, participating traders will receive the results of the operation, including their accepted proposals, via FedTrade immediately after the auction ends.

Will the operation desk publish operation pricing results?

Following the period in which the console conducts direct operations, the console will publish transaction price information for individual operations mid-month for the previous month’s trading period.For each security purchased or sold in each operation, the Operator will publish the weighted average acceptance price/rate, the least favorable acceptance price/rate, and the acceptance ratio for each proposal submitted at the least favorable acceptance price/rate.

In addition to the monthly release of pricing information, Section 1103 of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 requires the release of detailed operating results, including counterparty names, two years after each quarterly trading period.

Who should traders call if they encounter difficulties during operations?

Primary dealers with submission and verification questions may call the New York Fed’s Open Market Operations Desk.For system-related issues, traders can call the New York Fed’s primary dealer support department.

When and how does settlement of Treasury securities occur?

Settlement of Treasury securities is usually conducted on a T+1 basis, which is the business day following the operation day, through the Fedwire Securities system.

Will the Fed assess TMPG Treasury bond failure charges?

Yes.If a Federal Reserve counterparty fails to deliver a Treasury security on the contract settlement date for a transaction on this desk, the Federal Reserve will assess the applicable Treasury failure fee recommended by the Treasury Department’s Market Practices Group (TMPG).

Opening remarks and Q&A at the press conference

Good afternoon.My colleagues and I remain focused on achieving our dual mission goals of achieving full employment and price stability for the benefit of the American people.

While some key federal data from the past few months has yet to be released, available public and private sector data suggest that the outlook for employment and inflation has not changed much since our October meeting.Labor market conditions appear to be gradually cooling, while inflation remains somewhat elevated.

To support our objectives and to account for the balance of employment and inflation risks, today the Federal Open Market Committee (FOMC) decided to lower the policy rate by 25 basis points (0.25 percentage points).As a separate matter,We have also decided to initiate a program of purchases of short-term Treasury securities for the sole purpose of maintaining an adequate supply of reserves over the long term to support effective control of our policy rates.

After a brief review of economic developments, I will elaborate on monetary policy and its implementation.

While some key government data has yet to be released, available indicators suggest economic activity has been expanding at a moderate pace.Consumer spending appears to remain solid and business fixed investment continues to expand.In contrast, activity in the real estate sector remained subdued.The temporary federal government shutdown may have weighed on economic activity this quarter, but these effects should be offset by higher growth next quarter, reflecting the impact of the government’s reopening.

In our Summary of Economic Projections (SEP), the median forecast among participants was for real GDP to grow by 1.7% this year and 2.3% next year.This is slightly stronger than the September forecast.

On the labor market front, although the release of official employment data for October and November has been delayed, available evidence shows that both layoffs and hiring have remained low, with households’ perceptions of job opportunities and businesses’ perceptions of recruitment difficulties continuing to decline.

The most recent official labor market report for September showed that the unemployment rate continued to rise slightly to 4.4%, with employment growth slowing significantly from earlier in the year.Much of this slowdown may reflect lower labor force growth due to lower immigration, although labor demand has also clearly softened.

In a less dynamic and softer market, downside risks to employment appear to have increased in recent months.The unemployment rate is expected to be 4.5% at the end of this year and will decline slightly thereafter.

Inflation has eased significantly from its highs in mid-2022, but remains somewhat elevated relative to our long-term goal of 2%.There has been very little inflation data released since our October meeting.Overall PCE (personal consumption expenditures) prices rose 2.8% in the 12 months to September; excluding the volatile food and energy categories, core PCE prices also rose 2.8%.

The readings were higher than earlier this year as goods inflation picked up, reflecting the impact of tariffs.In contrast, the services sector appears to be continuing its de-inflation process.Near-term indicators of inflation expectations have fallen from their peaks earlier this year, and most longer-term expectations indicators remain consistent with our 2% inflation target, as reflected by market and survey-based indicators.

The SEP’s median forecast for headline PCE inflation is 2.9% this year and 2.4% next year, slightly lower than the median forecast in September.After that the median will drop to 2%.

Our monetary policy actions are guided by our dual mission of promoting maximum employment and price stability for the American people.At today’s meeting, the Committee decided to lower the target range for the federal funds rate by 25 basis points to 3.5% – 3.75%.Inflation risks are tilted to the upside in the near term, while employment risks are tilted to the downside, which is a challenging situation.

As we deal with this tension between employment and inflation targets, there is no risk-free path for policy.A reasonable baseline scenario is that the impact of tariffs on inflation will be relatively short-lived, effectively a one-time change in the price level.Our obligation is to ensure that a one-off increase in price levels does not turn into an ongoing inflation problem, but as downside risks to employment have risen in recent months, the balance of risks has shifted.

Our framework calls for a balanced approach in promoting both aspects of our dual mission.We believe it is appropriate to cut the policy rate by 25 basis points at this meeting.

With today’s decision, we have lowered the policy rate by 75 basis points (0.75 percentage points) over the past three meetings.Once the impact of tariffs subsides, further action will help inflation fall back toward 2%.

Adjustments to our policy stance since September put it within reasonable estimates of the neutral rate and put us in a good position to respond based on incoming data, the evolving outlook and the balance of risks.to determine the extent and timing of additional adjustments to policy rates.

FOMC participants wrote down their personal assessments of the appropriate path for the federal funds rate, based on what each participant considered to be the most likely economic scenario.The median forecast among participants was that the appropriate level for the federal funds rate would be 3.4% at the end of 2026 and 3.1% at the end of 2027, unchanged from September.

As always, these personal forecasts are subject to uncertainty and they are not plans or decisions of the Committee.There is no preset course for monetary policy and we will make decisions on a meeting-by-meeting basis.

Let me now turn to issues related to the implementation of monetary policy and remind everyone that these issues are independent and have no impact on the stance of monetary policy.

Given the continued tightening of money market rates relative to our managed rates, as well as other indicators of reserve market conditions,The Committee judges that reserve balances have fallen to the edge of “adequate” levels.Therefore, at today’s meeting, the Committee decided to initiate purchases of short-term Treasury securities (primarily Treasury bills) with the sole purpose of maintaining an adequate supply of reserves over the long term.

This increase in securities holdings ensures that the federal funds rate remains within its target range, which is necessary because economic growth leads to higher demand for the Fed’s liabilities, including currency and reserves.

As detailed in a statement released by the New York Fed, managed purchases will reach $40 billion in the first month and will likely remain elevated for several months to ease anticipated near-term pressures in money markets, after which we expect purchases to decline, so the actual pace will depend on market conditions.

In our execution framework, an adequate supply of reserves means that the federal funds rate and short-term interest rates are controlled primarily by our managed rate settings rather than through day-to-day intervention in money markets.

Under this system, standing repurchase agreement (Repo) operations are critical to ensuring that the federal funds rate remains within its target range even on days of elevated money market stress.According to this review,The Committee has realigned the limits on repurchase operations to support the conduct of monetary policy and smooth market operations and should be used when economically justified.

Finally, the Fed was given two monetary policy goals: maximum employment and price stability.We remain committed to supporting maximum employment, bringing inflation sustainably down to our 2% target, and keeping longer-term inflation expectations well-anchored.

Our success in achieving these goals is important to all Americans, and we understand it impacts communities, families and businesses across the country.Everything we do is in service of our public mission.At the Federal Reserve, we will do whatever it takes to achieve our maximum employment and price stability goals.

Thank you and I look forward to answering your questions.

Q&A session

>> Question:Thank you.First of all, regarding the statement, to make it clear that we understand the same.Insert the phrase “consider the extent and timing of additional adjustments”,Is this a sign that the Fed will now stand pat until there is a clear signal of some kind of departure from the baseline outlook on employment or economic evolution?

>> Chairman Powell:yes, adjustments since September put our policy within a broad range of estimates of the neutral rate.As we noted in today’s statement, we are considering adjustments based on incoming data, the outlook and the balance of risks.The new wording states that we will carefully evaluate incoming data.Additionally, I would note that we have lowered the policy rate by 75 basis points since September and 175 basis points since September last year,The federal funds rate is now within a wide range of estimates of its neutral value, we are well-positioned to wait and see how the economy evolves.

>> Question (Follow-up):If I can follow up on the outlook, it seems like with increasing GDP growth, coupled with inflation and stable unemployment, that seems to be a pretty consistent outlook for next year.What causes this?Is this an early battle about AI?Is it an increase in productivity?What’s driving it?

>> Chairman Powell:There are many factors driving changes in forecasts.If you look broadly at outside forecasters, you’ll find that many of them have also raised their growth expectations.This is partly because consumer spending remains strong and resilient; on the other hand, AI-related data center investment has been supporting business investment.So, overall, the baseline expectations for next year – at least at the Fed and I think outside forecasters as well – are a recovery from today’s relatively low level of 1.7%.I mentioned the SEP meeting (forecast) is 1.7% this year and 2.3% next year, and part of that is due to the government shutdown, so you can move 0.2% to next year.So maybe 1.9% and 2.1%.Fiscal policy will provide support and AI spending will continue.Consumers continue to spend, so the benchmark looks set for solid growth next year.

>> Question:Thank you Chairman for taking the question.You previously described rate cuts in terms of a risk management framework.Following up on the question Howard just asked, is the risk management phase here over?Given the jobs data we’re likely to get next week, have you taken enough insurance against potentially weak data?

>> Chairman Powell:We’re going to get a lot of data between now and the January meeting, and I’m sure we’ll be talking more about this.The data we get will be taken into account.But yes, if you look back, we kept the policy rate at 5.4% for over a year because inflation was high, very high, at a time when unemployment and the labor market were very solid.What then happened was that last summer, the summer of 2024, inflation fell and the labor market started to show real signs of weakness.

So, as our framework tells us, we decided that as the risks to both objectives become more equal, you should move from a position that tends to deal primarily with one of them, which is inflation, to a more balanced, more neutral setup.So, we did this.We made some cuts, paused for a while to sort out what was happening mid-year, and then resumed cuts in October for a total of 175 basis points.As I mentioned, we feel that our positioning now puts us in a good position to wait and see how the economy evolves from here.

>> Question:If I can follow up on the SEP, you’ve raised the growth numbers significantly, but employment hasn’t fallen that much.That is, you have more growth, but not much decline in employment.Thank you sir.

>> Chairman Powell:The implication here is always greater productivity.Part of that may be AI.Also, I think productivity has been almost structurally higher for a few years now.So if you start thinking about it at 2% a year, you can sustain higher growth without increasing job creation, and income increases over time, so that’s basically a good thing.This is certainly the implication.

>> Question:Today’s decision was decidedly divided.Not just two formal objections, but soft objections from four others.I wonder if this reluctance to support a rate cut suggests the bar for a rate cut is much higher in the near term?If it’s already well positioned now, what exactly does the committee need to see to support a rate cut in January?

>> Chairman Powell:Of course.As I mentioned before,The situation is that our two goals are kind of in tension (opposite), right?Interestingly, everyone around the FOMC table agrees that inflation is too high and we want it to come down.There is also agreement that the labor market has softened and that there are further risks.Everyone agrees on this.

The disagreement is about how you weigh those risks, what your forecasts look like, and ultimately, where you think the bigger risks are.It’s very unusual to have this kind of tension between two parts of a mission, and it’s what you expect to see when you encounter it, and we did.At the same time, our discussion was as good as any I’ve had at the Fed in the past 14 years.They are very thoughtful and respectful.We have people with strong views, but we get to a place where decisions are made.We made a decision today, and 9 out of 12 people supported it, so the support is quite broad.But it’s not like the usual situation where everyone agrees on the direction and approach.Opinions are more dispersed.I think that’s just inherent to the situation.

As far as what it takes, we all have an outlook on what’s going to happen, but I think ultimately a 75 basis point cut has been made and, you know, the impact of that 75 basis point is just starting to show.As I have said many times before, we are well-positioned to wait and see how the economy evolves.We’ll have to wait and see.We’ll get quite a bit of data.Now that we are talking about data, I should mention that we need to be careful in our assessment, especially household survey data.Because of very technical reasons in the way data is collected on some indicators, including inflation and the labor market, the data can be distorted, not just more volatile, but distorted.This is actually because no data was collected in the half months of October and November.So, we’ll get the data, but we’re going to have to look at it carefully and with a little bit of skepticism before the January meeting.Still, by January we will have a lot of December data.So, I mean what we get, like CPI or household survey data, we’ll look at it very carefully,and understand that it can be distorted by very technical factors.

>> Question (New York Times):One more question about the negative vote.You talk about these divisions in a very positive way, given the complexity of the economic situation we’re in.But at what point do these dissenting votes become counterproductive, both in terms of communications from the Fed and messaging about future policy paths?

>> Chairman Powell:I don’t feel – I don’t feel like we’re at that stage at all.I don’t think so.I want to say it again,These are good, thoughtful, respectful discussions, you’ll hear people say — you’ll hear a lot of outside analysts say the same thing.I can defend either side.It’s hard to decide.We have to make a decision.You know, we always want the data to give us a clear interpretation, but in this case, if you look at the SEP, you see a large portion of participants agreeing that unemployment risks are tilted to the upside, inflation risks are tilted to the upside.So, what do you do?You only have one tool.You can’t do two things at the same time.At what speed do you move?What side movements do you make and so on.What’s the timing?This is a very challenging situation.I think we’re in a good position, as I mentioned, to wait and see how the economy evolves.

>> Question:Chairman Powell, there was a discussion about the 1990s.During the 1990s, the Committee engaged in two discrete sequences of rate cuts of three quarter-point cuts each, one in 1995-96 and one in 1998.After those two times, the next move for interest rates was to go up, not down.With policy now approaching neutral, is the next move for rates necessarily going to be lower?Or should we think that policy risks truly go both ways from now on?

>> Chairman Powell:I don’t think raising rates is anyone’s baseline scenario right now.I didn’t hear that.What you’re seeing is some people feel like we should stop here, we’re in the right position and just wait.Some people feel that we should cut interest rates once or more this year and next year, but when people write down their estimates of policy and where it’s going, it’s either going to stay here, or it’s going to go a little bit lower, or it’s going to go a little bit more than a little bit.So I don’t see the base case involving a rate hike.Of course, two or now three data points is not a large data set, but you are right about those two and three interest rate cuts in the 1990s.

>> Question (Follow-up):Unemployment has been rising very slowly for much of the past two years, and in fact, today’s statement no longer describes the unemployment rate as remaining low.What gives you confidence that it won’t continue to rise in 2026, especially when housing and other rate-sensitive sectors still appear to be feeling the effects of restrictive policies — despite a 150 basis point rate cut, prior to today.

>> Chairman Powell:The idea is that with another 75 basis points of rate cuts now and policy – you know, call it within a broad range of reasonable estimates of the neutral rate – that will allow the labor market to stabilize or just move up a ten point or two, but we’re not going to see any sort of sharp decline, we’re not seeing any evidence of that at all.At the same time, policy remains unaccommodative and we feel progress has been made this year on non-tariff-related inflation.As the tariffs are implemented, as they are transmitted, that will show up over the next year.But like I said, we’re in a good position to wait and see how it plays out.That’s our expectation, but we’re going to start seeing data that will tell us whether we’re right.

>> Question:A lot of people interpreted your comments at the October meeting to mean, you know, when things are unclear, we’re going to slow down, which means that instead of cutting rates now, we’re going to cut rates in January.Why did the committee decide to act today rather than in January?Thanks.

>> Chairman Powell:Yes.In October I said there was no certainty of action, and that was certainly true.I said it was possible.You can think of it that way, but I’m careful to say that others may see it differently.

So why are we acting today?I’ll point out a few points.First, the gradual cooling of the labor market continues.From June to September, the unemployment rate increased by 0.30 points.Since April, employment has increased by an average of 40,000 per month.We think those numbers are overstated by 60,000, so that would be negative 20,000 per month.One other thing to point out, both household and business surveys show declining supply and demand for workers, so I think you could say the labor market continues to cool gradually, maybe a little more gradually than we thought.

In terms of inflation, it’s a little bit lower.I think the evidence is growing, and what’s happening here is that services inflation is falling, but that’s being offset by growth in goods, and goods inflation is entirely concentrated in the sectors that have tariffs.So, that really builds on that story.It’s just been a story so far, which is commodity inflation – and that’s really where the excess is coming from right now, more than half of the source of excess inflation is commodities, it’s tariffs – and then you have to say, well what can we expect with tariffs?

I would say it comes down to some extent to looking for “heat” in the broader economy.You know, are we seeing an overheating economy?Do we see limitations?What happened to wages?You saw the ECI (Employment Cost Index) report today.It doesn’t feel like an overheated economy trying to generate Phillips Curve-style inflation.So, we looked at all those things and we said this is a decision that needs to be made.It was obviously not unanimous, but overall that was the judgment we made and the action we took.

>> Question:On the question of reserves, how worried are people around the table about some of the tensions we’re seeing in currency markets?

>> Chairman Powell:I wouldn’t say “worried.”What really happened is this.Balance sheet reduction, sometimes called QT, has been ongoing.We have a framework for monitoring it.Nothing happened.Usage of the overnight reverse repo facility dropped to almost zero.And then starting in September, the federal funds rate started to rise in the range, right?It rises almost all the way up to the level of interest on reserve balances.There is nothing wrong with this.What that tells you is that we are in a well-reserved regime.

So, we knew this was coming.When it finally came, it was a little sooner than expected, but we were definitely there to take the action we said we were going to take, and that’s what we did today.Therefore, we are announcing the resumption of reserve management purchases.This is completely separate from monetary policy, we just need to maintain an adequate supply of reserves.

Why is it so big?The answer is,If you look ahead, you see April 15th (tax day) coming up, our framework is such that even when reserves are temporarily low, we want to have adequate reserves.This is what happens on tax day.People pay a lot of money to the government.Reserves fell sharply and temporarily.So, this seasonal accumulation that we see in the coming months is going to happen anyway.This is because April 15th is April 15th.

Additionally, there is a long-term, sustained growth trajectory for the balance sheet.We have to keep reserves, relative to the banking system, relative to the economy as a whole, call it constant.That alone would require us to add about $20 billion to $25 billion per month.This is just a small part.That’s ongoing, and it’s also happening in the context of temporary months of front-loading purchases to get reserves high enough to get through the tax period in mid-April, and that’s what happened there.

>> Question:Thank you, Mr. Chairman.This is the last FOMC press conference before important Supreme Court hearings next month.Can you talk about how you would like the Supreme Court to rule?I’m curious why the Fed has been so silent on such a critical issue.

>> Chairman Powell:That’s not what I want to discuss here, Andrew.We are not legal commentators.That’s before the courts, and we don’t think — we don’t think trying to engage in a public discussion is going to help resolve the issue.I’ll give you a Mulligan.

>> Question:Which means I have three questions?

>> Chairman Powell:No.Just one more question.

>> Question:I want to go back to the problems of the 1990s.Do you think that’s a useful model for thinking about the current state of the economy?

>> Chairman Powell:I don’t think it rises to that level.So, I do think in 2019, we had three rate cuts, but it’s really a unique situation.It’s not like the 1970s, let’s put it that way.But there is a real tension between our two goals.This is unique in my tenure at the Fed, and I think going back a long way, we haven’t been in this situation.

In our framework, as you know, when that’s the case, we try to take a balanced approach to those two things.We look at how far off they are and how long it takes to get each one back on target.This is actually a very subjective analysis, but what it tells you is that you have to — I think ultimately what it says is that you should maintain some kind of neutrality when they are broadly, equally threatened, or equally risky.Because if you’re either loose or tight, you’re biased towards one of the goals.So, we’ve been moving towards neutral.Now we’re in the neutral range.I would say we’re at the high end of the neutral range, and that’s what we’re doing right now.It just so happened that we cut interest rates three times.We haven’t made any decisions on January yet, but as I said, we think we’re in a good position to wait and see how the economy performs.

>> Question:Thank you, Mr. Chairman.I want to ask you, the inflation expectations in the SEP report have come down.Do you think tariff price increases will be transmitted over the next three months?Is this a six-month process?Are jobs at risk because of this?

>> Chairman Powell:Regarding tariff expectations, with the announcement of tariffs, which take months – the goods have to come from elsewhere – you know, it can take a long time for individual tariffs to fully take effect.But once it has that impact, the question is, is that a one-time price increase?We looked at all the announcements, and what you get from it is that for every announcement, there’s a time period that’s fully accounted for.

So, if there is no new tariff announcement – and we don’t know if there will be, but let’s assume there is no new tariff announcement –Commodity inflation should peak around the first quarter, probably.We can’t predict exactly – no one can – but calling it around the first quarter of next year should be the peak.It shouldn’t be very big from that point on.Maybe a few ten points or even less.We don’t really have precision on this.After that, if no new tariffs are announced, it’s going to take nine months to fully factor in, and that nine months is also an estimate, and then you should see it come down in the second half of next year.

>> Question:The media has been openly discussing the new Fed chair.Has this hindered your current work or changed your current thinking?

>> Chairman Powell:No.

>> Question:No Mulligan (opportunity to ask again)!The 10-year rate is up 50 basis points since you started cutting rates in September 2024, and the yield curve is basically steepening.Why do you think continuing to cut rates now, especially in the absence of data, will lower yields on the thing that has the biggest impact on the economy: long-term rates?

>> Chairman Powell:What we focus on is the real economy.When long-term bonds move, you have to look at why they move.If you look at inflation compensation, it’s very — you know, that’s part of it, is the inflation compensation, the breakeven inflation rates, they’re at very comfortable levels, and once you look beyond the very short term right now, the breakeven rates are very low, consistent with 2% inflation in the longer term.

So, rising interest rates there doesn’t indicate concerns about long-term inflation or anything like that.I watch this stuff all the time.The same goes for surveys.Surveys all show that the public understands our commitment to get back to 2% and expects us to get back there.

So why are interest rates rising?It must be something else.This must be an expectation of higher growth or something like that.That’s mostly what’s going on.You saw a big change at the end of last year, and that had nothing to do with us.That ties into other developments.

>> Question:Well, you just mentioned that the public expects you to get back to 2%.Americans overwhelmingly list high prices and inflation as their top concerns.Can you explain to them why you prioritize the labor market – which seems relatively stable to most – over their number one concern, inflation?

>> Chairman Powell:As you know, we have a network of connections in the U.S. economy that is really unparalleled if you span 12 reserve banks.So, we hear clearly how people experience costs.Really high cost.Many of these are not current inflation rates.A lot of it is just higher costs embedded due to higher inflation in 2022 and 2023.This is what is happening.

So the best thing we can do is get inflation back to the 2% target, and our policies are designed to do that.But also having a strong economy, real wages are rising, people are getting jobs, making money, we’re going to need a few years where real wages are higher – you know, it’s positive, significantly positive, so wages – nominal wages are above inflation, before people start to feel good about affordability.So, we’re working on that.We try to keep inflation under control but also support the labor market and strong wages so that people make enough money and feel the economy is healthy again.

>> Question:Hi!Just a follow up.I mean, this is the third time you’ve cut interest rates this year, and the inflation rate is around 3%.So, the message you want to convey is, are you satisfied with the current level of inflation?As long as people understand that at some point you still want to get back to 2% because inflation is relatively stable where it is right now?

>> Chairman Powell:Everyone should understand, and surveys show they do understand, that we are committed to 2% inflation and we will achieve 2% inflation.But this is a complex and often difficult situation, labor markets are also under pressure, and job creation may actually be negative.Now, the supply of workers has also dropped significantly, so the unemployment rate hasn’t moved much.This is a labor market that appears to have significant downside risks.People are very concerned about this.That’s their job and their capabilities if they are laid off or enter the workforce looking for work.This is really important to people.

Regarding the inflation story, we know very well that it’s a story right now, which is that if you take out tariffs, inflation is in the low 2% range, right?So it’s really the tariffs that are causing — most of the inflation overshoot.We do think that under the current circumstances this may be a one-off –You know, one-time price increases.Our job is to make sure it’s a (one-off) and we’ll get the job done.

But now you have this difficult balance where there are risks on both sides and there is no risk-free path.If it’s just inflation and the labor market is really strong, rates will be higher, as they have been for over a year.We don’t have to worry about inflation (slip of the tongue, we don’t have to worry about the labor market), we don’t have to worry about the labor market, because the labor market, the unemployment rate is very low, if you remember, when inflation was very high.There was a labor shortage so we could focus entirely on inflation.It’s different now.We actually have risks on both sides.

I think we’re doing what’s best for people.They also care about their jobs, they do care about affordability, and the best thing we can do is support economic activity, but also, you know, make sure that when tariff inflation comes down and goes away, that inflation falls around 2%.

>> Question:Thank you very much.Just to follow up, you’ve been talking about negative job growth.Why do you think job growth is much worse than some official data suggests?

>> Chairman Powell:Oh, well, we know, I guess – I don’t think it’s particularly controversial.Estimating job growth in real time is difficult.They counted everyone day and night to conduct the investigation.There has always been some kind of systematic overestimation.So, we expect, they revise twice a year.So, the last time they revised, we thought the revision was going to be 800,000 or 900,000 — I don’t remember the exact number, but that’s what happened, so we thought that continued.

So, we believe that there is an overestimation in the payroll employment numbers that continues and will be corrected.I don’t have the exact month in mind right now.Again, I think forecasters generally understand this.We think it’s about 60,000 per month, so 40,000 jobs is probably minus 20,000, but that could be off by 10 or 20 in either direction.But in any case, the thing is, this is job creation to some extent.That’s demand.

Labor supply also fell sharply.So, you know, if you have a world where workers are not growing, you don’t really need a lot of jobs to get to full employment, and some people think that’s what we’re seeing.But I think a world where job creation is negative, I think we need to watch that very carefully and be in a position where our policies don’t drive down job creation.

>> Question:When we talk about supply, we see large U.S. employers like Amazon citing AI and layoffs.To what extent do you factor this into the current softness of the job market?

>> Chairman Powell:So, that’s part of the story.It’s not yet part of the story, or if it ever will be.But you couldn’t miss the announcement of massive layoffs, and companies saying they wouldn’t be hiring anyone for a long time, citing AI.This is obviously all happening.

At the same time, people are not filing for unemployment insurance, and since jobs are being created—the rate of finding work is extremely low.If there were a lot of layoffs, you’d expect continuing claims to go up, you’d expect new claims to go up, but they really didn’t go up that much.So, it’s a little weird.

But in the long term, the question is what we’ll see here.We don’t know.It may be that – in the past, technology – really big technological innovation times, you would see some jobs destroyed and other jobs created.Ultimately, what happens over hundreds of years is that as you get through this, you have higher productivity and new jobs and people have enough jobs.

>> Question:Thank you, Chairman.Given the breadth of the policy committee’s views, why is there such a divergence of views?

>> Chairman Powell:What’s the disagreement?

>> Question:Why is there such a difference of opinion between (regional Fed) presidents and (Federal Reserve) governors on the committee?

>> Chairman Powell:It’s not that obvious.There is greater diversity of perspectives within each group.There are some cases of that, but I would also say there are trustees, there are people from both groups in both groups.I don’t take that seriously.

>> Question:Given your escalation on growth, if the Supreme Court overturns the tariffs that we’re hearing about so far, what will the economic impact be in terms of growth and inflation?Thanks.

>> Chairman Powell:I really don’t know.It’s going to depend on a whole bunch of things we don’t know, so I can’t really help you.

>> Question:Thank you, Chairman Powell.I wanted to ask you how high-income households are driving assets (appreciation) on the back of equity equity and lower wealth, but are struggling with five years of accumulation of price increases. It’s the price level, not just the inflation rate, that’s holding these households back.How sustainable is the so-called K-shaped economy?What are the Fed’s thoughts on whether this is a risk going forward?

>> Chairman Powell:So, we talk about this a lot through contacts and net worth (data).If you listen to earnings reports from consumer-facing companies that tend to deal with lower- and middle-income people, they all say they’re seeing people tightening their belts, changing the products they buy, buying less, and so on.

So, that’s obviously a thing.It’s also one thing for property values, home values and securities to be high, and they tend to be owned by people with higher income and wealth.

So, how sustainable is this?I have no idea.It is true that most consumption is done by people with more means.I think the top third of the population accounts for well over a third of consumption, for example.

So, that’s a good question, how sustainable is this.The best thing we can do is have price stability and a strong labor market.What we saw, for example, at the end of a very, very long expansion that ended with the outbreak of the pandemic, we saw that was 10 years and eight months or something like that, the longest on record.In the last two years, the largest share of wage growth went to people in the bottom quartile, the bottom segment of the lower- and middle-income brackets.So, from a social perspective, it’s really, really good to have a strong labor market over the long term.It helps people at lower income levels, which is what we all want to get back to.But we have to have price stability, we have to have, you know, full employment, maximum employment.

>> Question:Just a quick question, you mentioned that the housing market is still a little soft.With the interest rate cuts that we’re seeing, are there any opportunities for us to see more affordability in the housing market so that more people can enjoy that part of wealth creation.The median age of first-time buyers is 40, the highest level on record.

>> Chairman Powell:Yes.So, there are some very significant challenges to the housing record, and I don’t think a 25 basis point cut in the federal funds rate is going to have much of an impact on people.Housing supply is low.A lot of people had mortgages that had very, very low rates during the pandemic, and they’ve been refinancing and locking in really low rates.So moving can be expensive for them.

We still have some way to go to change this situation.Additionally, we haven’t built enough housing in this country for a long time, so many estimates suggest we just need more housing of a different kind.So, housing is going to be a problem, and, you know, the tools to solve it are – we can raise and lower interest rates, but we really don’t have the tools to solve the chronic housing shortage, the structural housing shortage.

>> Question (Associated Press):Thank you.You mentioned inflation, services inflation is low and goods inflation looks likely to peak.We saw the wage report today that you mentioned, which showed modest wage growth.Where are the risks of inflation?It appears to you that inflation is cooling and at the same time you may have negative hiring.Why not — why aren’t we hearing more noise about potentially more rate cuts in this environment?

>> Chairman Powell:Well, I think the risk to inflation is clear, which is, you know, we’re seeing that we have higher inflation, as I mentioned.Most of the above-target inflation comes from commodities.We think, we estimate, and most of us expect, that inflation will be a one-time price increase followed by a decline.

We just experienced a period of inflation that was much more persistent than anyone expected.Will this happen now?So, that’s the risk.The risk is either that the tariff inflation outcome becomes more and more persistent, and maybe because companies that are holding off on passing on tariffs now will continue to do so, so you’ll see that.

I think the other, less likely possibility is that the labor market gets tight, or the economy gets tight, and you see, you know, just traditional inflation.I don’t think it’s particularly likely, but, you know, again, across the committee, people look at the picture very similarly but look at the risks very differently.Some people do see inflation risks, and I’m not going to dismiss that scenario.I don’t refute that scenario, but you have to make an assessment, and that’s the assessment we made.

>> Question:Hi, Chairman Powell.This question has come up a few times today, but do you believe we are experiencing a positive productivity shock, whether from AI or policy factors, and how much of that is driving the higher GDP forecast in the SEP?

>> Chairman Powell:So, yeah, I never thought I would see us have five or six years of productivity growth.This is higher, absolutely higher.That’s before it can be attributed to AI.

I also think that if you look at what AI can do, if you use it in your personal life, which I think a lot of us have, you can see the promise of productivity.I think it makes people who use it more efficient.However, it may leave others looking for other jobs.So, it might have productivity implications, but it might also have social labor market implications that we don’t have the tools to deal with.

But yes, we’re definitely seeing higher productivity.I think it’s a little too quick to say it’s generative AI, but I don’t know.The pandemic may have prompted more automation, with computers doing more things instead of people, which has increased productivity, or output per hour.

>> Question:Does this mean a higher neutral rate and therefore perhaps a bit higher policy than (previously thought)?

>> Chairman Powell:All things being equal, yes, but all things are not equal.There are a lot of things pushing in a different direction than the neutral rate, but yes, that argument does come up.

>> Question:Thank you, Chairman Powell.After today, you only have three more meetings left at the helm of the Fed.Since becoming Fed chairman, you’ve been through multiple trade wars, pandemics, periods of high inflation.I know your term as president doesn’t end until May, but I’m wondering if you’ve thought about what you want your legacy to be?

>> Chairman Powell:My legacy?My thinking is, I really want to hand this job over to whoever takes over from me, and the economy is in a really good place.That’s what I want to do.I hope inflation is under control.back down to 2%.I hope the labor market is strong.This is what I want.

All my efforts are to get to that place.It’s always been that way, but ultimately, that’s what I want.I don’t have time to think about bigger things.I wish I had many years to come to worry about that, but there’s enough to do right now.

>> Question:Relatedly, have you given more thought to that and can you tell us more about your plans to remain on the Board of Governors after your term as chairman expires.

>> Chairman Powell:Again, I’m focused on the remainder of my time as president.I have nothing new to tell you.

>> Question:Even as many price levels remain high, lower federal funds rates mean savings rates, or more accurately yields, have peaked, while key borrowing rates remain high while many Americans face liquidity energy savings challenges.Is this just collateral damage or an unintended consequence because your tools are limited in terms of working around family constraints and having enough money in the bank?

>> Chairman Powell:I don’t know.I don’t agree that that’s collateral damage in our run.I mean, we do what we do over time to create price stability and maximum employment.These things are extremely valuable to all the people we serve.

When we raise interest rates to lower inflation, you know, that does work by slowing the economy, but we’ve moved our policy back to where it is now, which is certainly not strongly restrictive.I think it’s in the neutral range.

So, that’s what we try to do.I hope people understand this.I think what people are feeling is the impact of higher prices.There’s a global wave where almost every large economy in the world – every large open economy, market-based economy – has experienced a wave of inflation that looks a lot like ours.We got through this better than any other country, much better, with higher growth.We have an extraordinary economy with innovative people.They work hard and so, all of us who work in the economy are very lucky to have the American economy, so thank you very much.