On August 14, after several hits a record high of 4870, Ethereum turned downward on August 14, starting its first round of adjustments after breaking through $4,000.As of August 20, its price had fallen from its high of $4,790 to $4,060, a cumulative decline of 15.2%, and triggered a long liquidation of up to $1.6 billion.This unexpected “scam” made many optimistic bulls who bet on historic breakthroughs suffer heavy losses.Many investors lamented that Ethereum was trapped at 4,800 four years ago, and it happened again four years later.

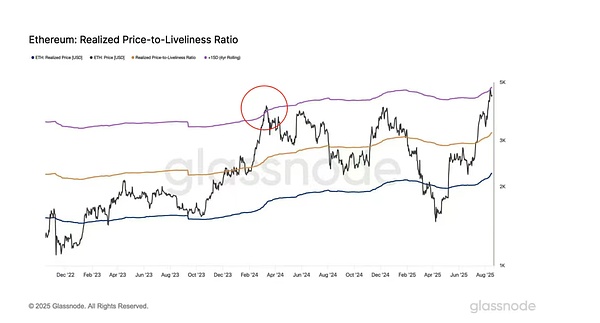

However, as of now, Ethereum’s adjustments are still mainly driven by profit-taking.Glassnode data shows that ETH price has hit a key threshold for +1SD active realization of prices after breaking through $4,700, indicating that the continuous rise has caused the price to significantly deviate from the average market cost (realization price).It is worth noting that the last time the indicator hit this level was in March 2024, followed by a significant sell-off on Ethereum.The pressure on market profit-taking is particularly prominent in the staking data: during the rebound from August 3 ($3,350) to August 14 ($4,790), the number of Ethereum unstaking queues surged from 410,000 to 916,000, while the average cost (staking cost) of this batch of tokens was only $2,800, indicating that a large number of early low-level holders are cashing out at highs.

Note: Implementation Price: The price weighted average of Ethereum’s last transfer.+1SD Active Achievement Price: 4-year rolling average of the ratio of realized price to activity plus 1 times the standard deviation.

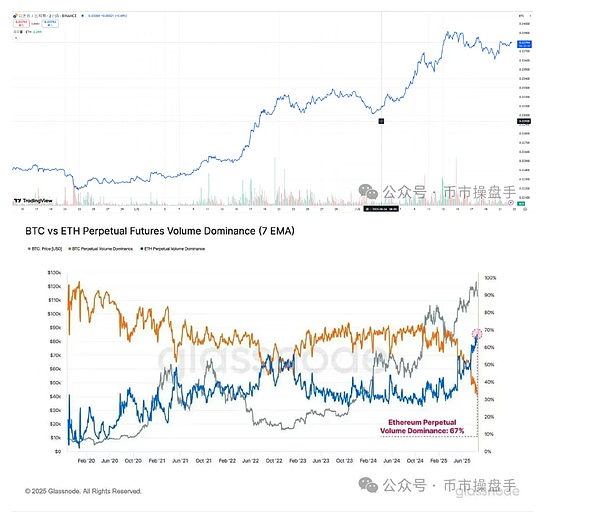

Although Ethereum faces significant profit-taking pressure in the short term, its upward trend has shown no signs of reversal.First of all, historical experience shows that the end of the strong market of any asset is often accompanied by capital diversion and hot spots. However, Ethereum’s exchange rate against mainstream currencies remains strong – for example, ETH/BTC has always remained firmly above the 5-day moving average, and its dominance in the market is also further strengthening.As of August 22, the proportion of Ethereum contract trading has climbed to 67%, which shows that Ethereum is still the main battlefield for capital games.

Secondly, in the global capital market, the valuation of core assets generally shows a bubble trend, and the valuation premium of high-growth assets is still rising.Taking the S&P 500 as an example, its current price-to-earnings ratio has risen to 29.51, at a high equilibrium level of 89% in the past decade; its price-to-book ratio is as high as 5.3, even exceeding the peak of the 2000 Internet bubble period.At the same time, the average P/E ratio of the “Seven AI giants” (AI7) that are regarded as high growth certainty has reached 37, significantly higher than the overall valuation level of the S&P 500, reflecting the market’s strong pursuit of scarce growth.What is more prominent is that the Science and Technology Innovation 50 Index, which is in the Mavericks market, has soared to 164 times, reflecting the highly optimistic expectations of some markets for the future growth of emerging technology companies.

In the blockchain field, Ethereum’s systemic importance position is comparable to that of the “big seven” in the AI field, and the certainty of its growth path is even clearer.Driven by the dual power of the compliance dividend brought by the GENIUS Act and the innovation plan of “Project Crypto”, Ethereum has entered a high growth phase driven by strong expectations.In the future, its valuation evolution is expected to follow the logic of premium expansion of growth assets, and achieve further value revaluation under the dual catalysis of policy and ecology.

In short, after a brief adjustment, Ethereum still has the potential to continue to hit record highs.

As demand for convertible bonds and preferred stocks gradually sluggish, MicroStrategy (MSTR) had to give up its previous commitment to “no additional issuance of common stocks for Bitcoin net assets (NAV) below 2.5 times the market value is lower than 2.5 times. This move has led to a sharp decline in its stock price and has also triggered widespread concerns about the sustainability of the Digital Asset Treasury (DAT) business model.

There is no doubt that this round of decline in MSTR is closely related to the deterioration of its capital structure, but the rise in leverage ratio is not the fundamental reason.Almost all Bitcoin treasury companies face a common challenge: their cash flow is mostly based on external financing rather than operating income.More importantly, the core asset it reserves – Bitcoin itself does not generate cash flow and is a non-productive asset.Once the financing environment tightens and financing activities are blocked, companies will be forced to sell Bitcoin to maintain operations and pay interest in debt, thus falling into a negative cycle of “selling assets-decreasing net value-decreasing confidence”.That is to say, once new external financing is not available, the net value of Bitcoin treasury companies per share will gradually decline and the stock price will gradually fall.

In contrast, the business model of Ethereum Treasury companies is more prominent in terms of sustainability.Currently, Ethereum PoS staking can provide an annualized return of about 4%, with some lending protocols (such as AAVE) yielding rates up to 5%-7%, while some mainstream stablecoin protocols yielding rates (such as Ethena) even exceeding 10%.Therefore, even if the most conservative asset allocation strategy is adopted – such as directly pledging Ethereum, the treasury can obtain benchmark returns from nearly 30-year U.S. Treasury bonds, thus providing endogenous cash flow support for operations without relying on continuous financing.Judging from historical data, the annualized return on corporate profits of the S&P 500 in the past 100 years (1923-2023) is about 5.5%, while Ethereum has approached this level through risk-free staking alone, which shows that Ethereum Treasury companies’ profit expectations are still quite considerable.

In the past, the Ethereum community has repeatedly suggested that the Ethereum Foundation adopt this model to obtain cash flow to avoid directly selling Ethereum assets.However, these proposals were opposed by God V, and the reasons were mainly based on the fact that the Foundation should avoid the possible conflict of interest caused by direct participation in the network verification process.The entry of Ethereum Treasury companies now happens to provide feasibility verification for this development model.

When investing in Bitmine, Mutou mentioned that investing in Ethereum Treasury companies has more advantages than encrypted ETFs: According to the provisions of the US Tax Law Act No. 40, funds obtain relevant exposures through investment in ETFs (encryption), which will inevitably face tax risks brought by complex tax processing, multi-layered management expenses, and potential “bad income”.It is particularly worth noting that if the gross profit of a certain investment of the fund exceeds 10% of its annual total profit, it may cause the entire fund to lose its tax preferential qualification, be forced to close, and even face high fines.In other words, U.S. stock fund companies face less compliance resistance and tax pressure than investing in crypto ETFs.

To sum up, based on its high-yield cost-effectiveness and natural compliance advantages, the market rate of Ethereum Treasury companies still has significant room for growth.As market awareness deepens, those Ethereum treasury companies whose net asset premium rate is close to zero will gradually show unique investment value.