Author: Kieren James-Lubin, founder and CEO of BlockApps; compiled by: Baishui, Bitchain Vision

ETH was conceived at the end of 2013 and launched in July 2015.I started working on Ethereum in the summer of 2014, and this decade seems unimaginable.When these milestones pass, it is useful to check what we expect and what actually happens.

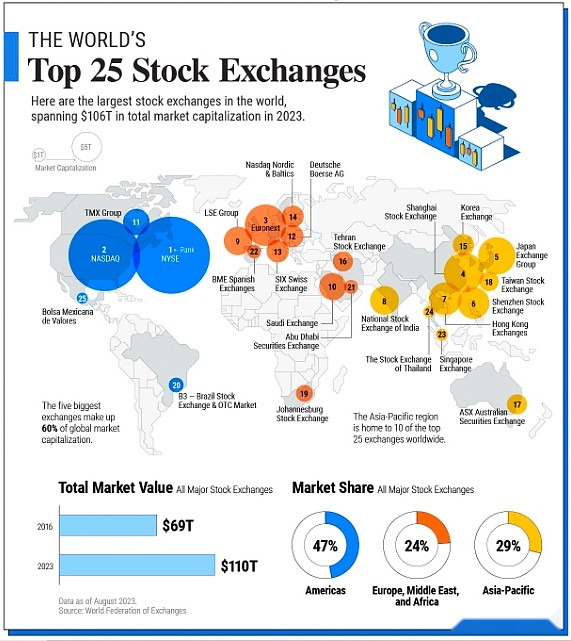

Public chains and tokens are not unified, but are increasing

Blockchain has a strong network effect, which is almost defined.Therefore, one may expect a few blockchains, or even a single blockchain, where most of the end-user activity occurs.Ethereum was created partly to “one chain dominates everything”, which is in stark contrast to the practice of making a new blockchain for each new feature at the time.

Social networks and stock markets show integration behaviors – we have a popular social network for about every purpose (X/Twitter — text, Instagram — pictures, YouTube — video, etc.).There are two popular stock markets in the United States.Most countries have only one or no, only the top 20 or so stock markets have truly global significance.By comparison,There are about 2.5 million cryptocurrencies – a five-fold increase from 2021.While many of these tokens and blockchains may not be widely used,As of September 2024, there were more than 50 tokens and blockchains with a market capitalization of billions of dollars.

Blockchain and blockchain-based tokens are relatively easy to build and finance, so it is reasonable to have a large number of such tokens.Ethereum has greatly facilitated this activity, simplifying the issuance of new tokens into a small piece of code or even a few clicks.Private investment usually chases hot areas, with a large amount of money flowing to a specific category—such as artificial intelligence and blockchain, or the ride-sharing companies of the past.

The top 25 stock exchanges in the world.Source: Visual Capitalist

We usually see that after market integration, one to three winners will occupy most of the market share, and other participants will be acquired or closed down.In contrast, blockchain and blockchain native tokens have strange flexibility, and some projects will always exist even if they are no longer actively developed.Some projects will make a comeback – Dogecoin, for example, has gone through a long period of silence, but since 2020, the event has become active again.

The argument that “the market determines everything” has not been confirmed

Around 2014, every long discussion about the inaccuracy of blockchain technology eventually turned to the assassination market—a market that allowed speculators to bet on the time of someone’s death.The assassination market did appear for the first time in 2018, but it does not seem to be ongoing.The areas where the forecast market was popular before blockchain emerged—elections and sports—have become popular, with huge transaction volumes lately.

What is less striking is that decentralized on-chain insurance has been conceptualized early on, but still seems to be on the edge.We can imagine countless micro insurance markets – will my train arrive on time?If not, can I get compensation?But this ability alone is not enough to allow these markets to exist.There is not enough interest in the operation of these markets—at least not enough for now.

Progress in institutional adoption is different from expectations

Institutions adopt more new assets than migration business processes, while legacy assets are put on the chain slower than expected.

In the early days of the tech industry, government (especially defense) is often your first customer.Well-funded institutions hire technicians who can use less mature products and get better results than the ones used at the time.This may be the path to adoption of blockchain technology, especially given the strong interest of traditional financial institutions.

Instead, the use cases that are digitally successful in large institutions tend toward consumers.This technology may be too transformative and difficult to adopt gradually to allow traditional players to use it for core business processes.New asset classes have been the main focus, with brands like Nike receiving an astonishing $185 million in non-fungible tokens (NFT) revenue, while the iShares Bitcoin Trust manages over $20 billion in revenue.

Startups are more successful than traditional institutions in bringing traditional assets onto chains.Tether has a market capitalization of $120 billion, making it the most obvious success story.Large financial institutions have much larger asset management scales, with BlackRock leading the way with $9 trillion in asset management.But relatively speaking, they have had very little on-chain action so far.

The development of this industry was completely beyond my expectations.It’s weird, disappointing in some ways, but amazing in others.In a letter to shareholders in 1997— Amazon’s revenue that year was $150 million—Jeff Bezos called the internet “global wait.”With a pragmatic and optimistic attitude, we all succeed.

Original link: https://cointelegraph.com/news/10-year-look-back-ethereum-now-and-then