In the first two years, when we talked about “blockchain” or “RWA (real world asset tokenization)”, the response from most traditional finance practitioners was:“Isn’t this just putting asset tokens on compliant exchanges (such as HashKey, OSL) for sale? There is no liquidity at all and it is meaningless.”

The perspective holds true for a long time.If RWA can move off-chain assets to an isolated island on the chain that lacks liquidity, it is indeed a false proposition.

However, as we wait and see amid doubts, the underlying logic of the bond market is quietly undergoing fission.From Siemens’ instant settlement of 300 million euros on the public chain, to BlackRock’s introduction of U.S. bonds onto the chain, to MicroStrategy’s use of a convertible bond structure to leverage a market value of hundreds of billions, a new “RWA+bond” model is taking shape.

It’s no longer about “hyping the coin”;Reshape the entire life cycle of bond issuance (Issuance), registration (Registration), settlement (Settlement) and circulation (Circulation).

In the previous in-depth case, let’s address the pain points of the traditional bond market with our financing.Although we have strong infrastructure such as Euroclear and DTCC, bond issuance is still a “manpower-heavy, high-hardness, long-term” process:

-

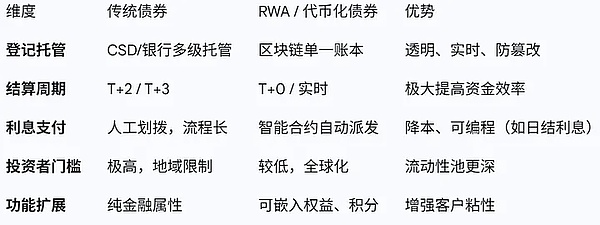

Settlement delay (T+2/T+3): High-level domestic (custodian banks, Hawaii exchanges, CSD) lead to time differences in the delivery of funds and bonds, which brings counterparty risks and capital occupation costs.

-

high internal costs: Each layer needs a share of the pie, resulting in extremely high debt issuance costs for small and medium-sized enterprises, which are insurmountable.

-

Information island: Top-level supervision of bonds is difficult, and the custody systems of different countries are incompatible with each other. Cross-border bond issuance is similar to “climbing mountains and ridges”.

The core of RWA’s bond issuance is to use the blockchain as a “unified ledger” to achieve atomic settlement and immediacy.

We will launch the next phase of RWA through the following four aspects – financial infrastructure transformation and asset structure innovation

The public chain is CSD (Central Securities Depository) – the “dimensionality reduction attack” of infrastructure

【Case】

-

Siemens, Germany: Issued 300 million euros of digital bonds on Polygon (public chain), sold directly to retailers, skipping the traditional Central Securities Depository (CSD), and completed central bank currency settlement within billions of dollars through the SWIAT permission chain.

-

BlackRock: Purchased $6.5 million in Quincy municipal bonds through JPMorgan Chase’s Onyx platform, achieving the first full on-chain registration and delivery.

This most “orthodox” reform is also the path most acceptable to traditional financial institutions.Here, blockchain replaces the traditional Central Securities Depository (CSD).Under the traditional model, coupon transfer and money transfer are reserved parallel tracks and require a third party.

On the chain, intelligence guarantees “payment with one hand and delivery with the other hand”, and can even achieve T+0 real-time payment.The case of Siemens proves that companies can directly face qualified investors without the large-scale intervention of traditional banks as underwriters.This means huge underwriting expenses for high-rated bond issuers.

In the future, technical service providers that can provide “on-chain bookkeeping” services will replace some of the traditional back-end operations functions and become new basic departments.

The “DTC model” of corporate bonds—turning bonds into customer relationship management tools

【Case】

-

Toyota Financial (Toyota): Issuing 1 billion yen corporate bonds on the Progmat platform.But this is not just about borrowing money. Toyota links the bonds with digital wallets to return points and redeem benefits to investors based on the subscription amount.

-

Muff Trading: Swiss precious metals traders issue bonds directly through obligation agreements on Polygon without bank participation.

This is the DTC (Direct-to-Consumer) revolution in bond issuance.Traditional bonds are cold financial contracts. Investors buy bonds and have no connection with the company except to collect interest.But Toyota’s case shows the viscosity of RWA bonds.

For the corporate finance department, debt issuance is no longer a financial act, but has become a part of brand marketing and user loyalty management.This kind of “functional bond” is extremely difficult to realize under the traditional securities account system, but it is easy to achieve on the real-time blockchain.

The “equity bond issuance platform” designed specifically for consumer companies (aviation, hotels, automobiles) will be a huge untapped market.

On-chain ABS—a liquidity engine that revitalizes “long-tail assets”

【Case】

-

Centrifuge / MakerDAO / Maple: These protocols convert real-life invoices, trade financing, and real estate loans into NFTs (non-fungible tokens), mortgage them to stablecoin protocols on the chain (such as Maker), and exchange them for DAI or USDC to lend to enterprises.

This is the globalization and atomization of asset securitization (ABS).The liabilities of traditional ABS are extremely high, and legal fees, rating fees, and SPV establishment fees can easily reach millions. As a result, only large asset packages can be securitized.It is difficult for small and medium-sized enterprises to access capital markets for their credit assets (such as a supply chain invoice of US$500,000).

What the RWA protocol can do:

Build layered automation: Automatically divide priority (high-level) and inferior (junior) levels through smart contracts, without manual calculation and allocation.

Global Liquidity Access: The asset side is in Southeast Asia or Latin America, but the capital side is DeFi players around the world (investors holding USDT/USDC).

This effectively opens up a global unlicensed bond market.For practitioners who focus on private placement bonds of small and medium-sized enterprises, this actually provides access to a 24/7 trading capital pool, and is no longer set at the bank lending quota in a single region.

Those asset sponsors and risk control experts who can evaluate the quality of off-chain assets and “bridge” them onto the chain will become hot spots for DeFi protocols to compete for.

Convertible Bonds 2.0 – Cryptoassets as the new “underlying beta”

【Case】

-

MicroStrategy (MSTR): This is an extremely special case.They issue convertible bonds (Convertible Notes) with extremely low coupons (even 0%) to raise funds to purchase BTC.

Essentially you are buying a “call option”.If BTC rises sharply, the stock price rises sharply, and the debt is converted into equity, investors will make huge profits; if BTC falls, the bonds will be redeemed to repay the principal and interest (the company’s investors will pay the bottom line).

This brings great imagination to traditional bond design.The conversion value of traditional convertible bonds is linked to the company’s operating performance.MicroStrategy created a convertible bond linked to a “digital asset reserve.”

This is actually a perfect closed loop of “issuing bonds in the currency circle, raising funds in legal currency, and returning assets”.For companies with a large amount of computing power, energy reserves or digital asset reserves (such as mining companies and technology companies), by issuing such rights-containing bonds, they can obtain huge liquidity at first glance, and investors get a high-quality label of “guaranteed bottom (debt nature) and no cap (equity/currency nature)”.

The design and underwriting of “encrypted asset allocation convertible bonds” for the company’s listing will be a new high-profit business line for investment banks.

Back to the original question: Are RWA bonds a concept hype?

If you understand that it is just “go to a compliant exchange to place an order”, then it is indeed true.But if we look beyond the surface, we will find that the essence of RWA bonds is a “dramatic change” caused by the aggregation of various “micro-innovations” in financial infrastructure:

For traditional bond practitioners, RWA is not about overthrowing their current jobs, but about upgrading the “Excel sheets” and “SWIFT messages” in their hands to “smart contracts.”In this blue ocean, it is no longer a one-man show for exchanges;Understand compliance, understand asset structure, and dare to use technology to improve efficiencyThe stage for professionals.

Instead of waiting at the door of an exchange with depleted liquidity, consider:How to use blockchain technology to issue a “next generation bond” for the assets in your hand that has faster settlement, lower cost, and more flexible structure?

The wind started at the end of Qingping, and the digital wave of the bond market has just begun.