Author: Sumanth Neppalli Source: decentralised.co Translation: Shan Oppa, Bitchain Vision

This article continues the topic we have repeatedly discussed:Income and capital flows.A thorough analysis of the source of miner extractable value (MEV) and the current new methods to mitigate MEVs.

As you may have noticed, almost all of our recent articles revolve around one common point:The primitive of frequent and large-scale flow of funds.Our core view is still: blockchain is the new financial “track”, and products that can drive capital flows at high frequency will become winners in the next stage of crypto evolution.This logic also guides us on how to view the M&A market.

Now, it’s time to understandHow is the value drawn in each blockNow.

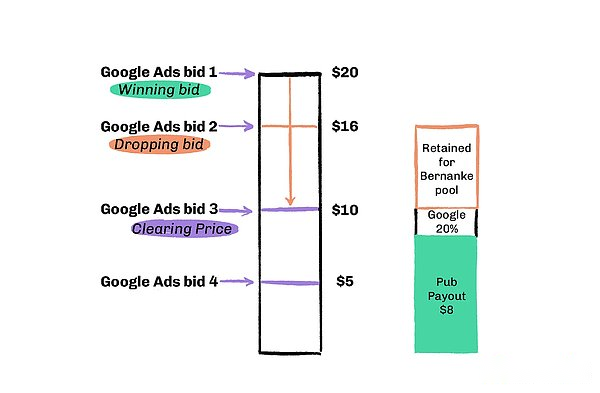

Welcome back to 2010.That year, Google launched theBid price advertising auction system”. The principle of running is simple: the highest bidder wins the ad slot, but only pays the second highest price.

This is perfect in the eyes of economists: advertisers don’t need to worry about “it’s expensive to buy at a high price.”However,Google secretly manipulates it behind the scenes, quietly pulling out millions of dollars in profits.

For example, the highest bid is $20, the second highest is $16, and the advertiser only needs to pay $16.But Google paid website publishers the third highest bid (such as $10), which means Google quietly swallowed $6 profits.They put this hidden profit in the name “Bernanke Pool”’s internal fund, used to achieve quarterly profit targets and please Wall Street. The truth was not revealed until an antitrust lawsuit in 2016.

Although Google turned to “in 2019”One-price auction system”, that is, advertisers pay as much as they pay (minus platform handling fees), but this historical description:Even the “fair” mechanism may be distorted when the auctioneer controls the underlying structure..

Interestingly –This history is reenacting in the blockchain world.The maximum extractable value (MEV) phenomenon is essentiallyAn extension of a secret auction, which allows miners/verifiers to reorder, insert or exclude transactions in blocks,Draw profits.

For ordinary users, this kind of operation is mostly invisible and intangible, but it affects every behavior participant on the chain – this is simplyAn invisible tax.

Then MEV will go like GoogleSecret and centralization?Can it be built into oneA system that is open, transparent and rewards to users?Can we design a system that makes this inevitable value extractionIt is beneficial to the entire ecosystem, not to make a few people rich?

Physics of Delay

Blockchain is a distributed network of thousands of computer nodes (miners or validators) that together receive and process transactions.

The validator has two roles:

-

Communication node (receive and broadcast transactions);

-

Compute nodes (execute and verify transactions).

Since these nodes are distributed around the world,There is inevitably delay in communication——Limited by the speed of light.

In order to ensure the consistent transaction order, each chain has set a “block time” to synchronize all nodes.Each round is rotated to select a validator to package the next set of transactions, and this mechanism is maintained by consensus protocols such as PoS.

-

Bitcoin: One block is released every 10 minutes

-

Ethereum: 12 seconds

-

Solana: Approximately 400 milliseconds

-

Second-layer chains (such as Arbitrum and MegaETH): 10ms to 250ms

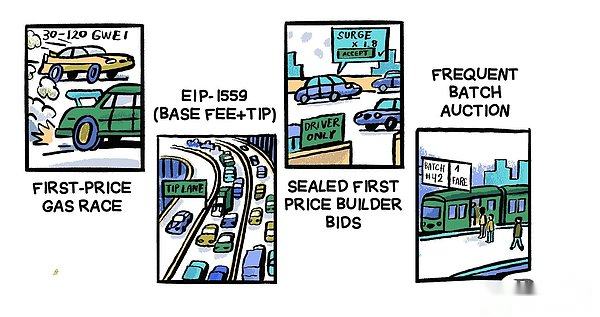

Each time window, regardless of length, creates opportunities for validators to reschedule transactions within the block to maximize their own profits rather than prioritizing user fairness.Ideally, it should be first come first served.But since nodes are distributed around the world, this is difficult to achieve.When a user initiates a transaction, due to network delay, it is guaranteed that not all nodes can receive the transaction at the same time.This means that sometimes unfair transaction order (the end user pays an extra fee, and the MEV maker profits) can be packaged into the block without violating any block building rules.

MEV is a big business

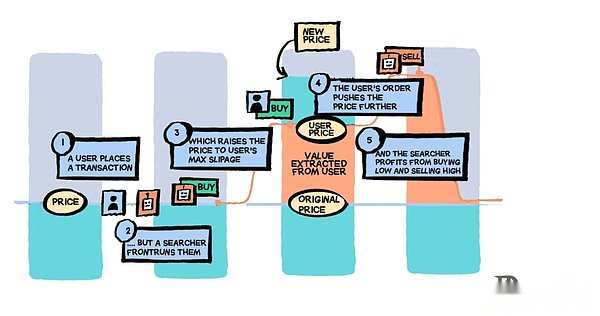

If Joel bought ETH at $1800 on a decentralized exchange (DEX) like Uniswap and set a 10% slippage tolerance, that is, he can accept that the price will rise to up to $1980 when it is closed.

Joel’s transaction enters the memory pool (the transaction memory pool, which is the “waiting room” on the chain), where it is waiting to be packaged into the block by a certain validator.At this time, a robot discovered the transaction.Copy the same payout orderand submit it using a higher gas fee, so its transaction willBeing given priority.

A higher gas fee is essentiallyBribery to the verifier, let them rank the bot’s transactions ahead of Joel.The robot’s payout will push up the price of ETH on DEX, for example to $1900.Joel’s transaction is executed at this time and is traded at this price after the rise.The robot then immediately sells its ETH for $1900, thus earning the spread (net profit after deducting gas fees).

Joel did get ETH but paid $100 more.And the robot made the $100 profit.This kind of thing happens thousands of times a day in the crypto market.

More extreme cases also exist.For example, a poor trader forgot to set a slippage, and was swallowed by the robot in one bite.Profit of $200,000.This time the “raider” is famousjaredfromsubway.eth, a robot address, which has long dominated the Ethereum gas consumption list with extremely high gas consumption, and specifically inserts the transactions it wants to attack.Jared is estimated to make over $10 million in profits through MEV attacks.

MEV mainly manifests in three forms:

-

arbitrage: Found that the prices between exchanges do not match, buy low and sell high in the same block.For example, ETH trades for $2,500 on Uniswap, but trades for $2,510 on Sushiswap.Robots can buy ETH on Uniswap within the same block and sell on Sushiswap, thereby locking in profits of $10 per ETH without taking market risks.It is worth noting that this is good for the market, as it will eventually make asset prices consistent across different platforms.

-

Sandwich Attack: Check out Alice’s large payout orders in the memory pool, grab her before she buys (push up the price), let her pay a higher price, and then sell it immediately.Robots earn the difference, while Alice bears the slippage.The example mentioned above is a sandwich attack.Joel paid an extra $100, which is actually profit from the MEV value chain.This is not advisable because the user ends up paying more than the necessary amount.

-

Clearing: In a lending agreement, when a position meets the liquidation conditions, the MEV withdrawer will compete for the first liquidation and receive a liquidation reward.Suppose Saurabh borrowed $15,000 worth of ETH and $10,000 worth of USDC on Aave.After the price fell, his ETH collateral fell to $11,000, breaking the liquidation threshold.A robot competes to liquidate 50% of his loan.It repaid $5,000 in USDC and in return it received $5,500 worth of ETH (benefited from a 10% liquidation bonus).That’s $500 profit, you can get it with the first action.This can be good or bad, depending on the situation.The incentives provided in the form of liquidation are beneficial to the overall health of DeFi.But most of this revenue ends up going to validators.

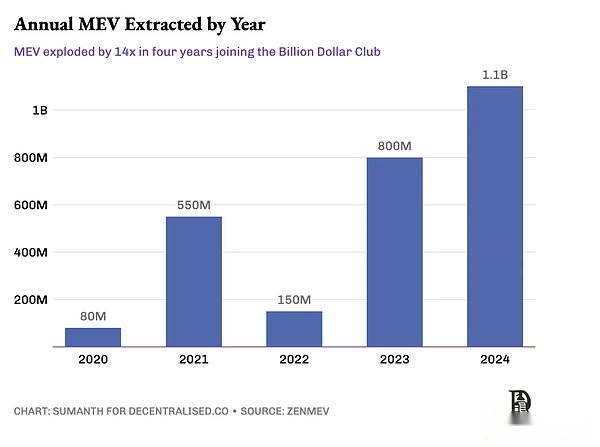

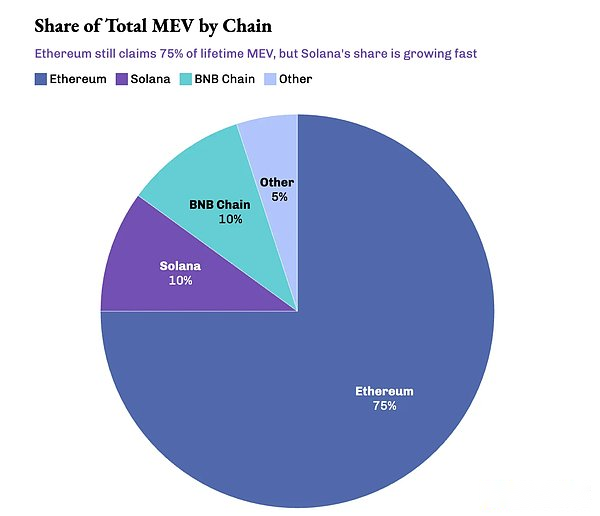

From $550 million in 2021 to double in 2024$1.1 billion, the extraction scale of MEV has shown explosive growth.Due to Ethereum’s open memory pool and deep DeFi liquidity, it is still the “episode” of MEV, with more than100 active robotsActive here.To date, about 75% of MEVs occur on Ethereum.

In the past 30 days, MEV transactions on Ethereum,66% is a sandwich attack,33% is arbitrage, and the proportion of clearing exchanges is less than 1%.

As on-chain transactions expand to other public chains, MEVs also spread.Solana, BNB Chain and various Ethereum Rollup (L2) have all become the “hunting grounds” for robots to pursue profits.Even Binance founder CZ was attacked by sandwich when exchanging coins.

Sandwich robots on Solana have earned over $4 million (approximately 24,000 SOL) in the past 30 days, this is almost the revenue from Ethereum robots during the same period50 times(approximately $80,000).

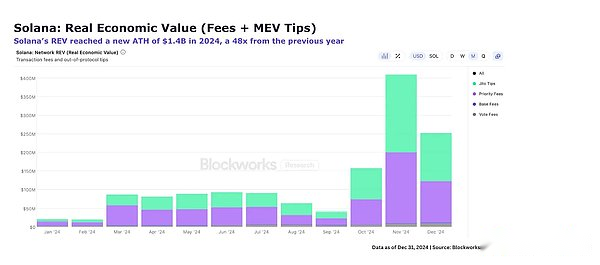

The cross-chain bridge also transforms the competition of MEV into a cross-link race, with robots shuttle back and forth between different ecology, trying to capture every opportunity.In December 2024 alone, MEV activity on Solana exceeded $100 million, mainly affected by market volatility caused by Trump’s re-election campaign.

In 2024, the total transaction volume on DEX reached$1.5 trillion, while the cost of MEV accounts for the transaction activityAbout 0.1%.Frontier Labs estimates that this number may rise to1%, it is expensive for large-scale transactions.

It’s easy for us to see MEV as “bad, evil.”But the fact is:In any financial market, loss of value is an inevitable phenomenon.The real issue is that weCan this loss be reduced or it will be distributed more equitably to all market participants.

MEV’s supply chain

Early blockchains gave validators two “super permissions”:

-

Decide which transactions are included in the next block;

-

Determines the sort of these transactions.

This raises a serious problem,Like the dark pool described in Flash Boys.Just as stock exchanges provide “privileged channels” for high-frequency traders, validators in blockchain can also privately reach cooperation agreements with robots to ensure that transactions of these robots are processed before ordinary users trade.

This “pay priority” mechanism allows insiders to always get the best price, while ordinary users can only eat “sweet soup”.

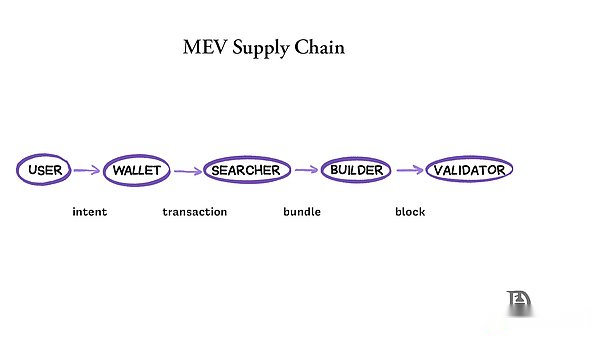

To solve this centralized risk, the Ethereum ecosystem is promoting a kind ofProposer-Builder Separation (PBS)architecture.It separates the process of block “building” and “oning”:

-

User submits a transaction or advanced intent (such as “swap token A for token B with the optimal price”);

-

The wallet processes these transactions and sends them through nodes to the searcher/builder/memory pool;

-

Searchers scan memory pools, look for arbitrage opportunities, and package related transactions;

-

The builder builds the complete blocks from these packaged transactions and auctions them out;

-

The validator (or proposer) selects the optimal block from it, checks its legitimacy, and adds it to the chain.

This mechanism limits the authority of validators – they can only choose from the sorted blocks submitted by the builder, thusAllocate MEV opportunities more widely to market participants, form a fairer block building competitive market.

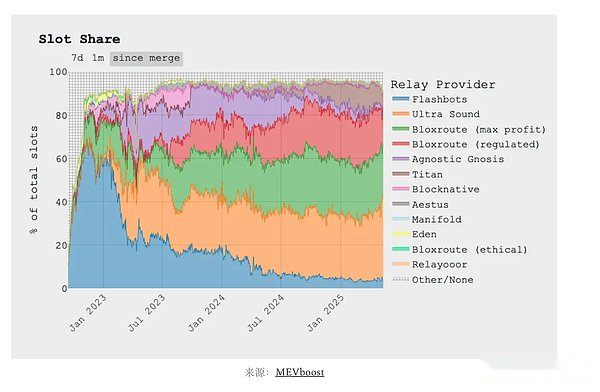

The most widely used PBS isMEV-Boost launched by Flashbots, as of the beginning of 2025,More than 90% of Ethereum validators have adopted it.

From “miner” to “maximum” value extractor

MEV, miners can extract value first dominated by miners, has evolved intoMaximum extractable value.The extractor is no longer just a miner, but aA huge ecosystem of multiple roles.

When you click “Swap” on Uniswap (DEX based on automatic market makers) or Raydium (DEX based on order book),Your opponent is almost impossible to be another ordinary person.

What you are facing is likeWintermuteSuch a professional market maker.They make profits by capturing the bid/ask spread (i.e. bid/ask spread).In the AMM model, they provide liquidity by depositing funds into liquidity pools, earning handling fees from user transactions.

It is unrealistic to “eliminate” MEV because itDeeply embedded in the block time economic structure.

-

On the positive side: Arbitrage helps price consistency between CEX and DEX markets, whileSubsidize cybersecurity through MEV commission;

-

Negative side: sandwich attacks and gas bidding wars make ordinary users pay higher costs.

MEV is an inevitable product of an efficient market – wherever there is profit, there will be someone to compete for it..

In the current ecosystem,Professional searchers, builders and market maker robots are the biggest beneficiaries.The ones that bear the costs are ordinary traders: they are snatched up, suffer additional slippage, or trade opaque because liquidity moves to an invisible “dark pool”.

Robots are frantically sending “bullet deals” to compete for MEV opportunities.Complete the run in a few milliseconds, causing memory pool blockage, bandwidth waste and transaction fees to rise.This is what we say“Invisible Tax”.

The rules of the game of MEV are not “elimination”, but rather clarification-Who should enjoy the benefits and under what rules to allocate them.

Strategies to reduce MEV

The ecosystem is currently trying four main ways to deal with MEV problems:hide,use,MinimizeandRedirect.Each approach has different tradeoffs between efficiency, fairness, and technical complexity.

MEV Hide

The easiest strategy is to before the transaction is packaged into the block.Undisclosed transaction content.Such tools include Flashbots Protect and Cowswap’s MEV Blocker.

These services are used very directly: the user’s transactions are not sent to the public memory pool, butSubmit privately to block builders.This way, the MEV robot cannot see the transaction before it is processed.

The disadvantages are:You have to wait until a validator using these services becomes a block producer.On Flashbots Protect, this wait may be over6 minutes.However, during this period you can cancel the transaction at any time because the transaction has not been sent to the memory pool yet.

Market makers and big money traders usually use this kind of service.Avoid premature exposure of trading intentions.So far, more than$43 billion dealSend via Flashbots Protect.

But I’m ok with thisCentralized privacy solutionsKeep it reserved because it reminds me of the “dark pool exchange” in traditional finance.These platforms were originally designed to protect users, butOften evolved into an internal privilege system like Robinhood.

Flashbots and Beaverbuild are exploringTrusted execution environmentTo encrypt it proves that its behavior is honest and reliable.This direction is exciting, but for nowNot yet validated on a large scale.

Some communities have also begun to take the initiative.For example, the BNB community voted to pass“Good Will Alliance”, requiring validators to accept only block proposals from compliant MEV builders.These builders filter out malicious MEV transactions,Verifiers will be punished if they do not use compliant infrastructure.

MEV Utilization

Some protocols are not to eliminate MEV, but to “fight poison with poison” and weaponize competition among robots through a private bidding mechanism.

For example: Suppose Joel wants to exchange 100 ETH for USDC.In traditional AMM mode, this transaction will appear publicly in the memory pool and is prone to sandwich attacks.However, if you use RFQ (Request-for-Quote) mode, Joel will send a coin exchange request to a group of market makers networks.

For example, Wintermute quotes $2,000/ETH, while DWF Labs quotes $2,010/ETH.Joel chose the latter and completed the transaction at a good price in 2010.No slippage, and avoids attacks.

Behind the scenes, every market maker is evaluating how much they can make from the deal.They will ensure profitability,Extract liquidity from different sources, to give Joel the best strike price while surpassing its competitors.

However, RFQ systems also come with their costs.It depends on aStable, 24/7 online, liquid market maker network, in order to respond in real time.If there are insufficient participants, the system will respond slowly – the user can only wait, and the price is still fluctuating.

RFQ mode more forMarkets with insufficient liquidity such as bonds, because order books in these markets are usually too shallow.If the institutions involved in market making are not credible or lack decentralization, RFQMay degenerate into another “insider club”.

To solve these problems,Python builds Express Relay on Solana, this is aOff-chain market maker market.Any DeFi protocol can be accessed through it to a competitive market maker pool, andThere is no need to develop a separate interface for each market maker, which not only simplifies the integration process, but also reduces MEV losses.

Jito took a different strategy and eventually becameThe leading validator client on Solana, currently controlledMore than 90% of pledges SOL.Jito once tried to introduce a Solana memory pool, but it was quickly exploited by attackers, and some people were willing to spend the money.$300,000Taking advantage of block priority, this attempt was eventually abandoned.

Now, Jito200 millisecondsRun an off-chain auction and chooseThe most profitable dealPackage into the next block.If the user wants to execute the transaction first,Add “tip” to the transaction, to prevent MEV attacks.The highest bidder is preferred for transaction execution, and these tips are converted into validator revenue – currently account for Solana validator revenueMore than half.

MEV Minimization

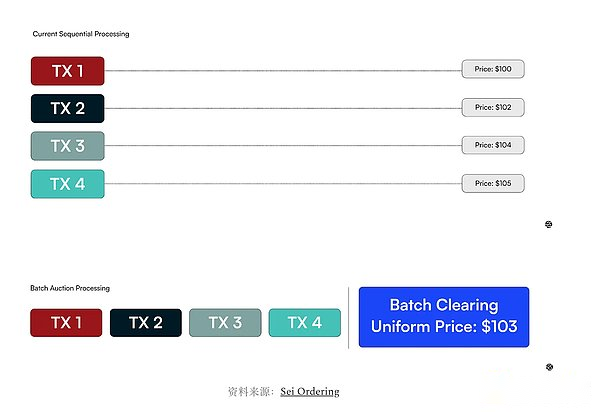

This method is built onOrder Flow Auction MechanismBased on the goal is toDesign smarter auction mechanismsmiddle,Reduce the total amount of MEV that can be extracted.

When transactions are processed one by one, the robots are created to view each transaction and quickly insert profitable arbitrage operations to make profits.And ifPackage multiple orders and execute them at the same price, it will smooth out the MEV brought by sorting and time difference.

CoWSwapIt is the pioneer of bulk trading. Its core concept is very simple: when a user wants to replace ETH with DAI, and the other wants to replace DAI with ETH, they can actuallyDirect swap, there is no need to pass traditional exchanges at all.CoWSwap will collect user’s trading intentions in a short time window and prioritizes matching these “natural rival plates”. It will only seek the liquidity pool on the chain if no match is found.

What’s even better is,Users do not need expertise in crypto market structure.When trading on CoWSwap, there is no need to manually set slippage tolerance, nor do you need to set up routing policies for different pools.The user only needs to submit the content they want to trade, and the system will complete the execution through a group of special market makers called “solvers”.

These solvers willCompete in fair bidding to win the best price for you.In each round of batch trading, the transaction prices of all assets are unified, which further prevents jumping.

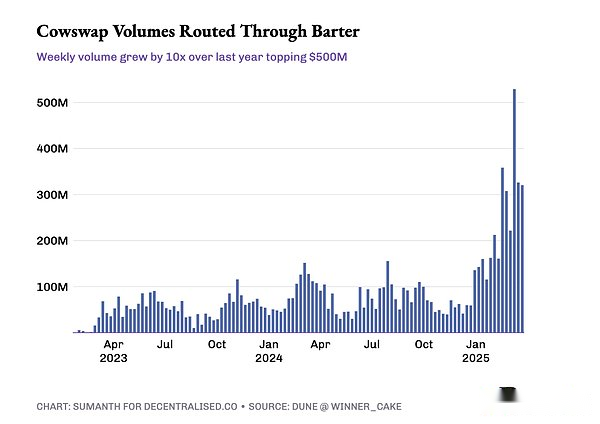

The actual results say it all: CoWSwap decentralized exchange has processed the$100 billiontrading volume.One of the leading solvers, Barter, occupied about15% market share, processed through this protocolMore than $11 billiontransaction.Barter’s continued growth further verifies how CoWSwap’s bulk auction mechanism isBy fair pricingRather than time advantage to reduce MEV.

This approach is also associated with Professor of Economics at the University of Chicago Booth School of BusinessEric BusinessThe research views are highly consistent.He believes:

“Processing orders every second in high-frequency auctions eliminates meaningless competition for speed.”

He pointed out that this batch processing mechanism can solve the “prisoner’s dilemma” problem in the continuous order book market (such as centralization or the limit order mode in some DEXs), and can also truly allocate the transaction costs saved to ordinary investors.

In the cryptocurrency market, the continuous limit order book rewards those who are “fastest” — which leads traders to invest in better hardware, faster robots, or direct-connected nodes, which are resourcesNot good for ordinary users, just the price of survival.And similar to CoWSwapBatch auction systemSubverting this logic:All transactions are processed at the same price within a fixed time window. The speed is no longer important, and the focus is on price discovery and user value.

MEV Recycling

Some innovators have taken moreA pragmatic approach: Since MEV cannot be eliminated, why not put itCapture and return to the community?

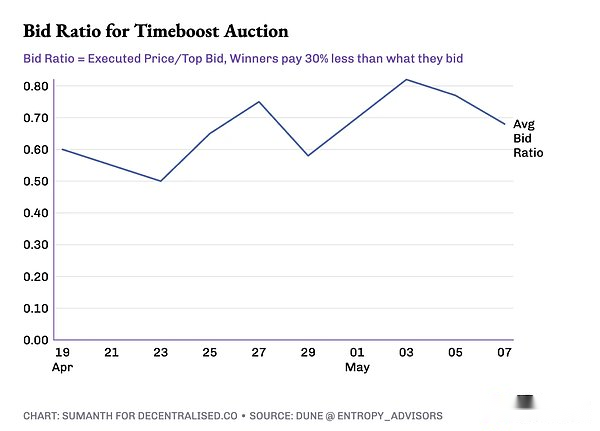

Arbitrum’s TimeBoostThis is an example of this idea.It passes every minuteClosed double-price auctionA 200 millisecond “fast track” for sale – like a Grocery Store’s VIP Quick Checkout Channel,The person with the highest bid can intervene in a queue to execute the transaction in this short time.

Searchers who want to prioritize their transactions can bid by predicting the potential of MEVs in the next 60 seconds rather than through the fierce Gas war.

This mechanismChanged the game rules for attackers: Any transaction executed through the fast lane will not be attacked by forward runs or sandwiches.Moreover, since the auction rotates once a minute and is open to all searchers,Nearly impossible to form an exclusive MEV monopoly alliance.

The end result is: MEV is no longer a mechanism for secretly increasing taxes, but has become a kind of “Public income tools“.at present,97% of TimeBoost’s revenue is returned to the ARB DAO treasury, in theory, it can create up to 100% annually for it$30 millionincome.

Even what we mentioned earlierJito, also adoptedHybrid strategy: Among the tips paid by users for priority transactions, there are3% are reassigned to Jito DAO and JitoSOL holders.

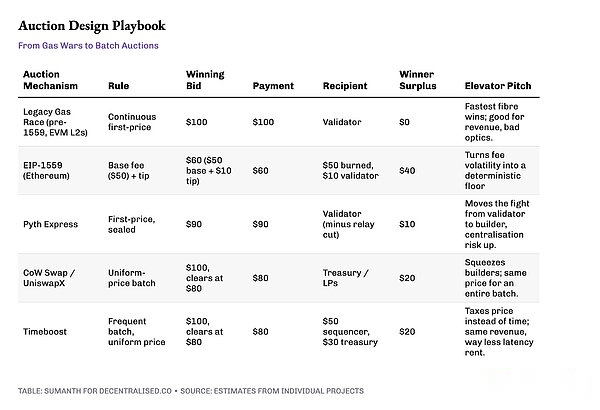

Choose the right auction mechanism

Among the five main auction mechanisms that currently dominate the MEV field, we can use a simple example to illustrate their differences: Suppose there are three bidders (searcher/solver/block builder) who bid $100, $80, and $60 for one block location.

Which auction mechanism is “best”,No standard answer, it depends on the specific objectives of your agreement:

-

If you pursueCurrent considerable income, continue to useClosed one-price auction

-

If you pursueCommunity recognition and long-term sticky users, similarThe mechanism of EIP-1559——For example, the intention order system with basic expenses plus a unified price.

-

If you wantBreak the delayed arbitrage alliance, you need to use itFrequent batch auctions, let “price” rather than “speed” determine who can enter the block.

-

If your scene is rightExtremely high transaction speed requirements(such as DEX), then private order flow is the best choice.

Where is the next step?

Does the strategy of hiding order flows and auctioning them to private market makers sound familiar?Wall Street’s “Dark Pool” story is being re-enacted on the chain.This trend is expected to accelerate as the crypto market becomes increasingly institutionalized and intersects with traditional auction mechanisms.

at present,There are only a few most professional teamsAble to compete in the role of searcher, builder or solver.TheirComplexity advantages will accumulate over time: This type of large-scale organization is equipped with top-level infrastructure and has an engineering team developing exclusive ML algorithms, which is likely to form an overwhelming advantage.We may even see traditional giants likeMorgan Stanley or Goldman SachsEntering the field as well.

Blockchains have also begun to form on the MEV issueIdeological stance: Solana is obsessed with ultra-low latency and naturally tends to follow the NASDAQ speed advantage in its privacy order flow mechanism.In contrast, Ethereum uses PBS and MEV-Boost to democratize access.Other blockchains explore new directions based on their own architectural priorities.

But the most important innovation,May appear in Layer 2.These new chains have the opportunity to design from scratchMEV-resistant architecture.For exampleArbitrum’s TimeBoostShows the ability of L2 in value distribution and auction mechanismsMore free trial.

DeFi’sComposability and permissionless features, make the field of encryption an excellent laboratory for experimental auction mechanisms.In traditional finance, “frequent batch auctions” have attracted attention since 2015, but it has been difficult to advance due to regulatory resistance.And on the chain, we can quickly iterate and implement it in a few months, just likeSeiWhat is done.

The other direction isBuild a decentralized market maker network.We may see in the futureBlock Builder Reputation MarketThe emergence of the participants prove honesty by pledging tokens.CombinedEigenLayerWith such a re-staking agreement, market participants can establish transparent reputation scores for upper-level protocol calls.

If you think these sound crazy, think about it:Twenty years ago no one could imagine that microwave signal towers would reshape the S&P order book.Incentive mechanisms will always find new ways out.