On November 3, the Hong Kong Securities and Futures Commission issued two important circulars: “Circular on Expanding Products and Services of Virtual Asset Trading Platforms” and “Circular on Shared Liquidity on Virtual Asset Trading Platforms.”

These two circulars respectively significantly relaxed the requirements for licensed (VATP licensed) crypto-asset trading platforms in terms of “products and services that can be provided” and “connecting the liquidity of overseas crypto markets.” Not only did they carry out a series of rule updates and clarifications, they also created a new “shared listing” system to achieve the purpose of connecting global virtual asset liquidity.

Of particular note is the “Circular on Expanding Products and Services of Virtual Asset Trading Platforms”For the first time, the connotation of “digital assets”, a rather complex legal concept under Hong Kong law, has been clearly explained:

“The term ‘digital assets’ includes ‘virtual assets’, ‘tokenized securities’ (a category of digital securities) and stablecoins. ‘Digital asset-related products’ refers to investment products related to digital assets.” This greatly facilitates market entities to correctly understand regulatory requirements.

Due to the limited space of the article, there are too many points to discuss about the new regulations.Today, Sister Sa’s team will first give you a detailed analysis of the new changes brought about by the “Circular on Expanding Products and Services of Virtual Asset Trading Platforms”.As for the content worthy of attention, the “Circular on Shared Liquidity on Virtual Asset Trading Platforms” will be discussed in two days.

1. Are licensed exchanges trapped in the “impossible triangle” of regulation?

The so-called “impossible triangle” of supervision, in layman’s terms, means that regulatory agencies cannot “both… and… and…”. The current licensed exchanges in Hong Kong have this meaning.

Previously, Sajie’s team had communicated with partners in an article about the current operating status of licensed virtual currency exchanges. The summary in one sentence was “not very profitable.”Part of the reason is that the China Securities Regulatory Commission’s compliance is too stringent – the objects that licensed exchanges can operate, the products that can be traded, and the services that can be provided are all subject to strict restrictions.It kind of means “if the water is clear, there will be no fish”.

In fact, this issue has been noticed by the Hong Kong Securities and Futures Commission, and it is working hard to find an “appropriate path” that can balance compliance requirements and stimulate market vitality. The “Circular on Expanding Products and Services of Virtual Asset Trading Platforms” is the product of its current efforts. The specific “relaxation” content and policies are as described below.

2. Relaxation of “coin listing” regulations on licensed exchanges

The Hong Kong Securities and Futures Commission has long required licensed exchanges to only list virtual currencies (including stablecoins) with a “12-month track record.”

The popular explanation is that the currency you list needs to be a currency that has lived for at least one year. The messy local dogs and rug pull projects will go as far as possible, highlighting the need for stability and all-round protection of investors.But this also brings about a problem. One year may indeed be too long for the virtual currency market where “one day on earth, one year in the currency world” makes it extremely difficult for licensed exchanges to acquire a market-capital currency, and the overall liquidity of the exchange is also dragged down.

The new regulations significantly modify this provision.

The first is the loosening policy on virtual currencies sold to “professional investors.”The new regulations completely cancel the “12-month track record” review requirement for the sale of virtual currencies to “professional investors”. Whether it is a stable currency or a market-cap currency, there is no requirement to live for more than one year.This means that in the future, cryptocurrency exchanges will be able to provide “professional investors” with broader crypto asset investment services.

The second is the loosening policy of virtual currencies sold to “retail investors”.Considering that the investment experience and risk resistance of “retail investors” are weaker than that of “professional investors”, the “12-month track record” review is still partially used for virtual currencies sold to “retail investors”.

On the one hand, for licensed stablecoins, licensed exchanges can sell them directly to “retail investors.” On the other hand, other virtual currencies (market capitalization coins) are still subject to the “12-month track record” limit.

However, it should be noted that this does not mean that the review requirements for “coin listing” have been significantly reduced.Licensed exchanges still have to follow the requirements of the “Virtual Asset Trading Platform Guidelines” for the coins to be listed.“Reasonable due diligence”, if the currency does not live for more than one year, it still needs to befull disclosure, otherwise it will still be illegal to list the currency.

3. Confirm the compliance of licensed exchanges distributing digital asset-related products and tokenized securities

Can a VATP license engage in the distribution business of digital assets (limited to virtual assets approved for trading on licensed exchanges) related products and tokenized securities?There has been no clear answer to this question before.

This is mainly because this matter is not clearly stated in Hong Kong’s “Standardized Licensing Requirements Normative Document Collection” formed by a series of laws, codes, regulations, manuals, guidelines, circulars, etc.

Based on the “Licensing Manual for Virtual Asset Trading Platform Operators” and “Guidelines for Virtual Asset Trading Platforms” and other normative documents, in addition to using virtual asset trading platforms to conduct virtual asset transactions, licensees can also provide virtual asset trading business and ancillary services to customers outside the platform (limited to virtual assets that have been approved for trading in licensed exchanges).

But, this regulation is too vague. Does the virtual asset trading business outside the platform include virtual asset financial derivatives trading?Does it include crypto asset custody business?Market players have varying understandings of these issues. Generally speaking, they tend to believe that it can be done, but they dare not take action easily.

This new regulation clarifies the regulatory rules involved in this issue.

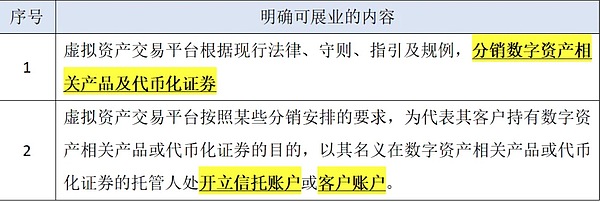

First,Licensed exchanges can clearly engage in the following two businesses:

Secondly, licensed exchanges specify the businesses that they are not allowed to engage in:Provide custody services for digital assets that are not bought and sold on virtual asset trading platforms by itself or by using its own affiliated entities.

However, this prohibitive regulation does not directly block the road. In principle, the Hong Kong Securities Regulatory Commission now allows exchanges to submit applications to modify relevant licensing conditions, or to conduct case-by-case reviews of projects to be managed by exchanges. If this project is really good enough that I cannot refuse, then I can exempt you.

write at the end

Change cannot always be achieved overnight. The current Hong Kong Securities Regulatory Commission is indeed only a small step in regulatory requirements, but it is also a milestone in the history of my country’s virtual asset supervision.

After all, this is a true rule update after the establishment of standardized licensing rules in Hong Kong, my country, and it truly takes into account the pain points and difficulties faced by market entities in the business process, and does its best to respond.

Sajie’s team applauds this regulatory progress and looks forward to further “relaxation” measures by the Hong Kong Securities Regulatory Commission.In the future, we will update the analysis of the “Circular on Shared Liquidity on Virtual Asset Trading Platforms” and fully explain the new regulations.