Source: On-Chain Mind, compiled by: Shaw bitchain vision

There are some concepts in the financial field that most of us will accept and have never really questioned.For example, the price-to-earnings ratio, the “fair value” indicator, and it is even believed that the value of the currency itself will remain stable.But when you take a step back, some of these ideas start to look less like unchangeable laws of nature, but more like collective beliefs supported by tradition.

This article explores in-depth concepts of Strategy (MSTR), market capitalization to net asset value ratio (mNAV), and how these concepts fit into the ever-evolving world of companies with Bitcoin at their core.It is a more fundamental and philosophical perspective of this new type of company that connects the familiar ideas in traditional finance (TradFi) while questioning assumptions that many investors are accustomed to.

Finally, you will understand that companies like MSTR are not just “buying bitcoins” – they are reshaping the possible face of stock value over the next decade.

Let’s get started.

Overview of key points

-

Challenge traditional indicators: Free cash flow per share (FCF/Share) is the “Polaris” of traditional stock investments. It has close similarities with Bitcoin per share among companies with Bitcoin reserves.

-

Growing the power of narrative: Investors bet on long-term growth, even with many unknown factors, which complement Bitcoin’s excellent compound interest rates.

-

mNAV is the “new price-to-earnings ratio”: It is not only a valuation tool, but also shows operating strength, financing capabilities and investors’ confidence in Bitcoin holdings.

-

MSTR’s technical signals: Indicators such as the 200 daily chart and Z-score probability wave suggest that the company’s current price of about $350 is an attractive entry point.

FCF/Share: Polaris of Traditional Investment

If the nature of stock investment is simplified, there is one indicator that often stands out: free cash flow per share (FCF/Share).

Why?Because free cash flow represents the actual cash a company generates after paying for operating expenses and capital investments.

Free cash flow per share is often seen as the ultimate measure of a stock’s effectiveness in returning capital to shareholders, whether through dividends, buybacks or reinvestment.Free cash flow per share continues to grow by 15% per year, often referred to as “excellent” because at such a rate compounded, the stock’s value doubles approximately every 5 years – a feat that few companies in the world can continue to do.

This is why the market gives these companies a premium valuation, which typically has a price-to-earnings ratio of between 25 and 30 times.In some cases, investors can even accept a price-to-earnings ratio of more than 100 times.At first glance, this seems ridiculous – many companies don’t live when they see the expected return period.But the reason is simple: growth.If the story is attractive enough, investors will be willing to pay high prices.

Crazy high price-to-earnings ratio

Being willing to pay a very high P/E ratio for profit is one of the widely accepted quirks in the investment field.Few people stop to think about the reasons.But if you take a step back, people are actually betting on an unknown future.

-

Will this company still exist in 25 years?

-

Will it still dominate its industry?

-

Will compound revenue growth continue to continue?

Despite these uncertainties, the growth narrative itself becomes a currency.The market regards it as a guideline.

The reason is that if many people believe in the growth of a company, this statement can drive its stock price to rise for years to come.This concept is widely accepted in the investment community, but when you briefly analyze it, think about the real situation, you will find that it is actually quite crazy.

The rise of mNAV

Now, apply this logic to Bitcoin treasury reserve companies.Currently, the same concept is being staged in the field of Bitcoin reserve companies.mNAV (ratio of market capitalization to net asset value) is a “premium” paid by investors for a company to enable them to acquire more Bitcoin in efficient ways that they themselves cannot achieve.

I like to compare it to the price-to-earnings ratio (price to earnings ratio) in the “new era”.In fact, it is more conceptually similar to price-to-book ratio (price to book value), although the term is less familiar to the average investor.Interestingly, the current price-to-book ratio of the S&P 500 is about 5.4 times, with a historical volatility range between 1.5 and 5.5, which is surprisingly similar to the historical average mNAV of MSTR.

Price-to-book ratio measures the relationship between a company’s market value and its book value (assets minus liabilities).It shows how much investors pay for each dollar of net worth.

It’s really refreshing to see many investors question why we have to pay a premium for the underlying Bitcoin assets rather than blindly accepting the concept as many aspects of traditional finance.We should question why things are priced at such prices.I think this is a huge advantage for the average Bitcoin investor: being able to question the widely accepted viewpoints simply because they “have been doing this all the time.”

Why does Bitcoin premium exist?

-

Trust Growth Program——Companies will find ways to make their asset portfolio grow faster than individuals.

-

Get cheap funds——This is something that ordinary investors can never reach.

-

Operational leverage——Use structures such as convertible bonds or equity financing to achieve faster expansion.

Can you get a loan at about 0% interest rate to accumulate more bitcoin?Nearly impossible.This is where the best Bitcoin reserve companies – especially those with larger and firm commitments like Strategy (MSTR).

Specifically, companies like MSTR utilize convertible bonds, where lenders accept lower interest in exchange for equity conversion rights.This actually subsidizes the accumulation of Bitcoin.In traditional finance, this is similar to the practice of tech growth companies using leverage to scale up without diluting their equity immediately.

But if the annual growth rate of free cash flow per share of traditional financial stocks reaches 15% is considered “exceptionally excellent”, why do we give a 1.5x premium (or a 4-5x premium) to companies like MSTR? Know that Bitcoin has grown at a compound annual growth rate of 60% to 80% over the past 5 to 10 years.

I think this is a major concept that the majority of investment communities have not yet understood. They still generally do not understand that Bitcoin is the top five assets in the world and is gradually swallowing up the value of global capital.This is also a major reason why I look forward to companies like MSTR in the long run.

mNAV discount: Trap vs. True signal

So, can the company trade with mNAV below 1?sure.According to Bitcoin Treasuries, 21 of the 167 listed companies (about 13%) traded at discounted mNAV.

This is again very similar to the reasons why some stocks trade at extremely low P/E ratios, such as 5x P/E ratios.Many traditional financial investors fall into this “value trap” and think they have bought bargains at extremely low prices because the stock prices are very low.But in fact, the reason why stock prices are low most of the time is that the company fails to fulfill the performance promises investors expect.

I think this concept of value traps also applies to Bitcoin reserve companies.For companies that trade at discounted mNAV, this shows market skepticism, which may be related to the following factors:

-

Weak governance;

-

fragile financing model;

-

Current business operational risks.

In fact, this may also indicate that investors are confident in the ability of these companies to hold Bitcoin.Because, from a mathematical point of view, when mNAV is below 1, it is actually a good practice for the company’s shareholders to sell Bitcoin to buy back the shares.

But companies like MSTR reject the temptation.Even though their mNAV fell below 1 during the 2022 bear market, they retained all their Bitcoin holdings by restructuring their debts.That’s why I’m fairly sure MSTR won’t fall into this category.I have no doubt that they will continue to hold all Bitcoin even in less favorable circumstances.This long-term holding philosophy stems from Michael Saylor’s vision of Bitcoin as pure collateral.

I don’t have enough confidence in the other 166 listed companies.The only company I would fall into the category of “HODL Long-term Holding” is the Metaplanet Company in Japan.

Therefore, mNAV is not a simple buy or sell signal—it is a perspective.A premium may indicate confidence or just speculation, while a discount may reflect dilemma and may contain value.The key lies in the specific situation:

-

How big is the company’s growth per share of Bitcoin?

-

Does it have other sources of income to support the valuation?

-

How is its capital model risk resistance in the market cycle?

MSTR’s Financial Magic

The real difference between MSTR and many other Bitcoin reserve companies is its diversified fiat currency financing capabilities and its ability to effectively purchase the Bitcoin assets they hold.Its low-cost financing tools such as convertible bonds, and an ever-expanding list of preferred stock issuances can expand Bitcoin holdings faster without diluting the equity of ordinary MSTR shareholders.

For example, convertible bonds allow borrowing at nearly zero effective interest rates when converted to equity during a bull market.This forms a flywheel: more bitcoins increase collateral value, allowing more money to be borrowed.In my opinion, this kind of financial magic deserves a considerable premium.Just like in traditional finance, Nvidia has achieved a reasonable P/E ratio because its free cash flow per share grows far faster than almost every other company.

For most people, this is a completely new concept.Bitcoin reserve companies want to increase the amount of Bitcoin per share as fast as possible, while traditional financial companies want to increase free cash flow per share as fast as possible.This is the same philosophy.However, one party wants to grow a pure capital that increases by at least 30% to 50% per year for the foreseeable time in the future, while the other party tries to accumulate their favorite fiat currency, which depreciates at a rate of 8% to 10% per year.

I know that in another ten years, if the development follows their respective strategies, which one is more likely to create more value for shareholders.

Market Signal

Finally, let’s take a quick look at some charts to discover some potential value opportunities.

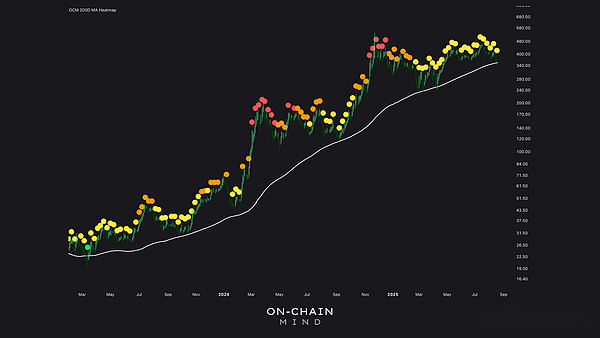

200-day chart signal shows strong:MSTR is expected to show a green signal point on the 200 daily chart for the second time in this cycle, and its trading price is at the 200 daily moving average of $353.This level is a key support level for bulls and marks the beginning of this round of upward trend.If this price can stabilize, it may indicate strong upward potential.

Z fraction probability wave: MSTR’s stock price has fallen to the negative 2 standard deviation level, which also happens to be $353.Historically, in this bull market, the stock price falling below minus 1 standard deviation often indicates that the price will fluctuate significantly. If the macro situation remains optimistic, the stock price is likely to return to the mean.

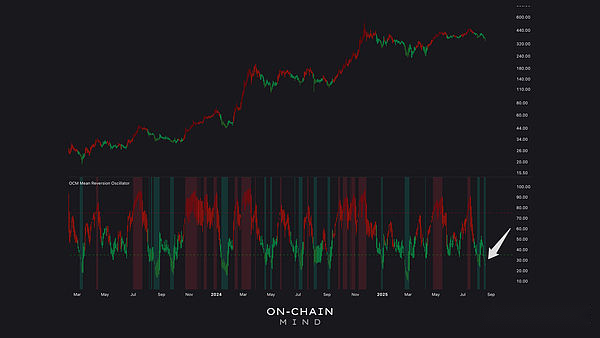

Oversold condition: My mean regression oscillator (its logic is similar to the RSI relative strength index) shows that MSTR is in the deep oversold area.In the past, situations at this level often led to short-term rebounds and sometimes significant upward trends.

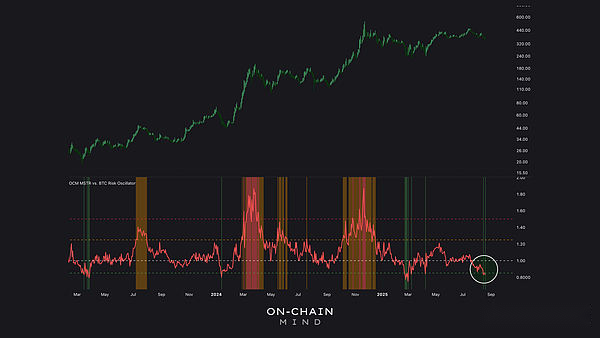

MSTR investment opportunities priced in Bitcoin: When priced in Bitcoin, the risk oscillation indicator of MSTR is at one of the lowest values, which is a strong signal for investors in a low-tax environment to shift investment from Bitcoin to MSTR.Historically, this lag in MSTR’s stock price relative to Bitcoin is often quickly compensated.

Why MSTR’s stock price lags does not worry me

To sum up, am I worried that MSTR’s share price will lag behind Bitcoin’s current gains?not at all.mNAV may have been compressed to around 1.5 now, but the true measure of its Bitcoin strategy remains intact: its number of bitcoin per share is still increasing weekly.To a large extent, that’s all I care about.

Just like traditional stocks, their free cash flow per share may increase year by year, but the stock price may fluctuate.This is the wonder of the irrational investor psychology.But if fundamentals continue to improve (such as the number of bitcoin per share continues to increase), I can’t wait to seize the opportunity to buy the company at a discounted price.Because as we know, when investor sentiment changes and the price-to-earnings ratio eventually expands again, this stock has the ability to make a big profit.