Source: Galaxy; Compilation: Bitchain Vision

Quick look at the key points:

-

Galaxy has partnered with Superstate to allow tokenization of its Class A common stock on the Solana blockchain.

-

Superstate is a Galaxy tokenized stock digital transfer agent.

-

GLXY’s on-chain stock is a SEC-registered Galaxy Digital Class A common stock, whichEnjoyHave the same legal and economic rights as stocks in traditional formats.

-

Those who join Superstate can hold (self-custody), send and receive on-chain shares of GLXY.

-

Although GLXY can be transferred between listed entities on both directionsOn-chain stock trading based on AMM has not been enabled.

-

Galaxy Stock’s contract address on Solana: 2HehXG149TXuVptQhbiWAWDjbbuCsXSAtLTB5wc2aajK, any token from other smart contract addresses, as long as it claims to be an on-chain stake in GLXY stock, or a token actually issued by Galaxy Digital, is fraudulent.

-

Galaxy Research has created this Dune dashboard to track the availability of GLXY on the chain: https://dune.com/glxyresearch_team/glxy-class-a-common-stock-token

introduction

On September 3, 2025, Galaxy announced tokenizing its Class A common stock GLXY – thisThis is the first time in history that it has to tokenized publicly listed U.S. stock securities on major public chains.

Galaxy has allowed existing shareholders of its SEC-registered Class A common stock to transfer their shares from the traditional format to the on-chain version on the Solana blockchain.By creating a “bridge” between traditional and on-chain markets, Galaxy enables its shareholders to represent their GLXY shares in tokenized form.When a user owns these tokenized shares of Galaxy, the user’s token is the real shares of the company.They are not “packaged stocks”; they are real on-chain stocks.They give us the same financial and legal rights as we have existing public offering shares because they are existing public offering shares.This is the first time in history that a publicly listed U.S. stock was issued on major public chains.

We achieved this with the help of Superstate.Superstate is a transfer agency registered with the US SEC and a leading provider of tokenized services and on-chain operations.(Note: Galaxy Ventures is one of the investors in Superstate).

Users who have completed Superstate registration can hold their shares (in their own custody) and transfer them to the address on the allowed list.Therefore, although the AMM transaction has not been enabled,A two-way transfer of GLXY can be performed between entities on the allowed list.

This is just the first step in the capital market revolution we expect.The U.S. SEC Chairman said regulators will “develop reasonable and feasible rules” for decentralized systems in the securities market, including automated market makers AMMs.Both Superstate and Galaxy are actively working with SEC to help define a compliant public stock AMM trading model, and we believe clear rules will be introduced soon.

Galaxy has always been at the forefront of financial innovation.We will continue to work with key industry regulators and stakeholders to advance Galaxy’s long-term core mission: to build faster, more efficient, more inclusive and safer ways to transfer, store and create value for the global economy – and tokenized stocks is the next step we take.

How to get to this point?Tokenization history

Humans like direct, bilateral, point-to-point interaction.Direct relationships are our preferred natural state.But as organizations, systems and markets grow in size, these direct links tend to break and are often replaced by centralized governments, institutions, intermediaries and organizations.Throughout history, most forms of human organization have experienced the same development, from local to national politics, production and supply chains, money and markets.Centralization improves efficiency at the expense of autonomy.The history of the US capital market is no exception.

In the late 1960s, the U.S. capital market flourished, but the market infrastructure failed to keep up, eventually giving birth to the centralized stock clearing and settlement system we see today.US SEC Chairman Paul Atkins announced its launch on July 31, 2025The groundbreaking speech of “Project Crypto”Among them, one of the most famous examples of this collapse and its resulting centralization is described.

The securities are lost or stolen.The transaction failure rate surged.Many brokerage dealers with weak capital are in trouble due to transaction failures.In desperation, trading hours were shortened and the exchange was eventually closed on Wednesday so that the company could handle the mountain of credentials.

The then-chairman of the US SEC described the collapse caused by the outdated system as “the longest and most serious crisis in the securities industry in 40 years… companies went bankrupt one after another, and investor confidence plummeted.” It is commendable that the US SEC actively responded to the so-called “paper work crisis.”The agency helped market participants establish depositary trusts and clearing companies (DTCs), thus revolutionizing the way securities are held and traded.Stock ownership no longer requires the transfer of paper certificates between clients and brokers, between brokers and brokers, and between brokers and clients through computerized book records.The certificate itself is fixed and stored securely in the vault, and ownership is transferred electronically, laying the foundation for modern clearing and settlement systems that have continued to this day.

——SEC Chairman Paul Atkins, July 31, 2025

During the booming economy of the 1960s, the direct settlement process that Wall Street relied on collapsed amid a surge in transaction volumes.In order to cope with this “paper work crisis”, the US capital market abandoned the peer-to-peer settlement process and chose to create a centralized intermediary (ultimately known as a custodial trust and clearing company, “DTCC”).This centralized settlement process has played a good role, allowing the U.S. capital market to grow significantly over decades.If there is a way to avoid the complexity of the “paper work crisis” and maintain a peer-to-peer process, this might be the preferred solution.In the 1960s, Wall Street’s growing settlement and record keeping needs were not met without centralized intermediaries.But now this is no longer the case.

For more than a decade, technologists and financial professionals have recognized the transparency and efficiency that blockchain brings to asset ownership and transfers.As early as 2016, the US Custody Trust and Clearing Corporation (DTCC) foreseeed the market advantages and disruptive potential of decentralized public chains., and released an important white paper titled “Embraining the Subversion: Exploring the Potential of Distributed Ledgers and Improving the Post-Transaction Pattern”.

Over the years, dozens of companies have been committed to tokenizing real-world assets, including real estate, merchandise, physical collections and artworks, but most of them have limited applications.In some cases, the resistance to such tokenization attempts comes from regulation, but in most cases, the market failed to bridge the gap between the physical properties of assets and the intangible properties of blockchains, with tokenized gold being a significant exception.This is actually a technical barrier.

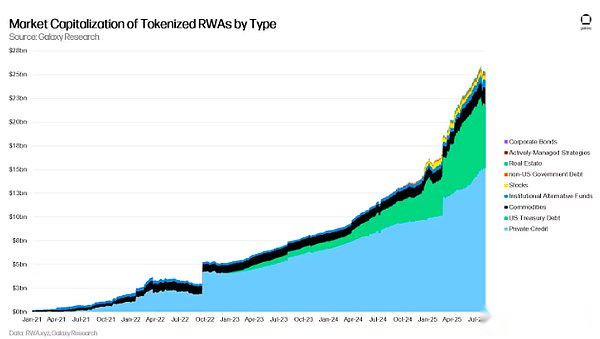

In contrast, tokenization, which takes intangible assets or even digital assets first, is more widely used.Stablecoins have become a hot-selling product with their extensive product market compatibility, and it is itself a form of tokenization.Today, stablecoins have shown three clear uses and continue to maintain strong growth: cross-border payments, overseas US dollar circulation in emerging economies, and as trading pairs for Bitcoin, ETH and other digital assets.Some tokenized categories other than stablecoins have also experienced strong initial growth, especially private credit and money market funds.The market currently tends to refer to this on-chain tokenization field as real-world assets (RWA); the supply of these assets is currently only about $25 billion, less than one-tenth of the stablecoin supply.

Securities tokenization

The limiting factors for the widespread use of tokenized securities have never been technical, but regulatory.certificateTokenization of vouchers is not a technological leap, but a change in the way of record preservation.Unlike gold, artwork or real estate – tokens in these fields must be linked to physical assets through custody and source information – most securities have been dematerialized and digitally preserved in bookkeeping.In the United States, positions are located within the DTCC indirect holding system (with DTC as the central custodian), and actual ownership is tracked through brokerage dealers and transfer agents.The system is a “centralized ledger”.”Tokenization” here is just to migrate entries from centralized ledgers to decentralized distributed ledgers; basic rights and obligations remain unchanged.

Regulatory resistance to equity tokenization

Historically, market regulators around the world, especially the US SEC, have hardly actively created a regulatory environment that allows tokenization of equity securities.As a result, startups have difficulty providing practical public chain services to traditional capital markets; traditional capital market companies, at least those willing to try, are struggling in the world of licensed blockchains; neither company has really crossed the gap.

The complex rules regarding issuance, recordkeeping, custody, settlement, reporting, brokerage and trading have mostly not been updated to allow the trading of equity securities in tokenized form.The US SEC, led by former chairman Gary Gensler, believes that existing securities rules are sufficient for issuers, intermediaries and exchanges, but do not explain why “tokenization enters the market and registers” are untenable.In short, the old rules worked well in the traditional financial system, but they did not fully apply to the functions inherent in blockchain technology.This impasse has led to two major consequences:

-

Inadequate regulatory approaches in the United States have led to stagnation of tokenization.Although the use of stablecoins as a medium of transactions and settlement assets continues to surge, the tokenization wave that has really begun in 2017 and 2018 has failed to make progress in the following years.Neither cryptocurrency native nor traditional companies are willing to prioritize technological and operational innovation.Regulators’ policy decisions have led to some complex regulatory issues that should not be partisan – for example, whether or how brokerage dealers interact with securities and non-securities tokens.

-

The market continues to adopt an inefficient tokenization structure to circumvent regulatory overheads in the United States.Although regulatory transparency in cryptocurrencies has stagnated or regressed, market demand for a new tokenized structure has not weakened.Earnings stablecoins, SPV-like structures for tokenized stock exposure, and teams that build trading applications and other mechanisms have all moved overseas.The launch of tokenized money market funds does not allow token transfer.To the extent tokenization of U.S. stock securities, these tokens exist in packaging form, with token owners having no specific equity requirements for the underlying company’s stock, or they are downgraded to private platforms that lack the transparency and openness of permissionless blockchains.The industry pursued these structures, like water on the road, and found some feasible structures, but no better ones were found.

Technology and regulation work together

Despite many obstacles over the years, progress has been made in blockchain technology and operational innovation, allowing securities tokens to be implemented on public, license-free blockchains while still following the principles behind Securities Law and Anti-Money Laundering Law.The previously hostile and indifferent regulatory environment has now shown a good momentum of support and participation.In 2025, the US SEC and the President’s Digital Asset Market Working Group have made it clear that promoting the application of public chains in the United States is a national priority.SEC Chairman Atkins and Commissioner Pierce have repeatedly elaborated on the benefits of blockchain innovation to traditional capital markets and promised that the SEC will review and modify existing rules or issue exemptions to allow innovation in the field of stock tokenization.

Crucially, the SEC has begun soliciting feedback from stakeholders on how to modernize its rules to cover blockchain tokens, with particular focus on brokerage dealers, issuers, secondary markets, custody and lending.This is a difficult task, especially given the failure of the SEC former leadership to do meaningful work in these areas.While setting new rules for the industry is of great significance to regulators, Galaxy will continue to be a trustworthy resource for regulators and stakeholders, with a common goal: to encourage innovations on which U.S. financial markets rely on to become famous and ensure clear guidelines are developed to safeguard trust and security as the cornerstone of our economy.

Sometimes changes are gradual and sometimes sudden.We believe that regulatory ambiguity over the past decade has been gradual (a bit like “nothing happened”), but now we are in the “sudden” stage.Regulators now have the opportunity to set rules for the future financial system in the coming weeks and months.Tokenizing GLXY through Superstate today demonstrates our determination to continue to innovate with regulators and move towards the economic future we have been looking forward to since its inception.

Galaxy Stock GLXY Tokenization

This leads to the tokenization of GLXY, which is currently trading on the Nasdaq.Although there are still major questions about how stock tokenization of US listed companies can be traded on-chain,We have developed a set of processes and structures that can truly achieve the tokenization of our existing GLXY stocks—not on a private licensed blockchain, nor through an SPV wrapper, but in the form of actual stocks.

We strictly abide by the current U.S. securities laws and construct equity tokenization work, which impose certain restrictions.We won’t cut corners, which means we have to innovate with caution and responsibility.We have built a bridge between the traditional capital market and the permissionless blockchain, allowing any shareholder who can join Superstate to convert their shares into tokenized forms on the Solana blockchain.

As regulatory provisions are unclear, we have not yet enabled automated market makers (AMMs) or other decentralized trading mechanisms on Solana to directly trade these tokens.With clearer guidance from U.S. securities regulators, our goal is to gradually expand trading venues and ultimately enable these tokenized stocks to trade directly on AMMs and other forms of decentralized exchanges.Importantly, GLXY’s on-chain stocks cannot be guaranteed to have any on-chain liquidity until these more durable, transparent, and stable secondary markets emerge, although two-way trading of GLXY can be conducted between addresses that have been added to Superstate.We will consider technology, transparency, decentralization and regulatory frameworks when evaluating increased support for other blockchains or trading venues.

The U.S. SEC also hasn’t fully adopted or clarified its rules, allowing brokers and traders to trade with any type of token, whether securities or otherwise.Therefore, it is unclear which U.S. brokers are able to assist GLXY’s on-chain holders in key operational or investment decisions.It is a pity that the SEC has not been involved in the formulation of this rule in the past four years, but the current SEC is seeking comments on how to enable brokers and traders to operate on-chain.Note that when you hold or trade GLXY on the chain, no broker will track your cost benchmark.

In the long run, we believe that the on-chain equity capital market will become as distinctive as traditional markets, and we are working closely with key stakeholders including the U.S. SEC to achieve this.

Process details: Convert traditional GLXY to tokenized GLXY

Galaxy Class A common stock shareholders can convert existing shares into tokenized shares.While we admit that the current process of converting traditional shares to tokenized shares is somewhat cumbersome, we believe: 1) The bridge between traditional finance and decentralized finance will be simplified over time; 2) Most people who want to use on-chain GLXY equity do not need to actually participate in the process of converting from traditional shares to tokenized shares.

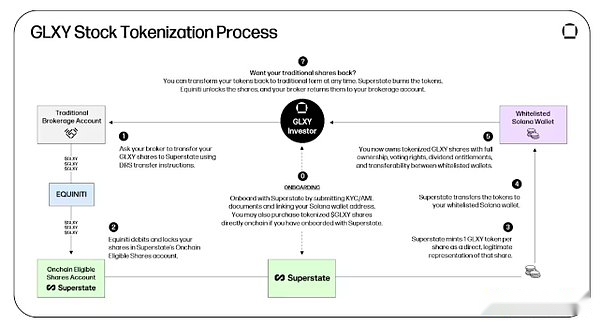

As shown in the above image, creating a tokenized GLXY from a traditional GLXY requires the following steps:

0. Visit Superstate.com/Register to register for Superstate.Yes, to hold or trade Galaxy tokenized Class A common stock, you must perform “KYC” authentication through our digital transfer agent.You can complete this step at any time even if you don’t own Galaxy stock.(It takes about time: Register for about 10 minutes and verification for about 2 hours).

In order to reformat existing GLXY stocks into tokenized stocks, you must already own GLXY stocks.

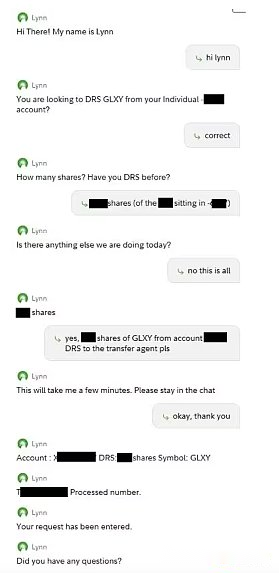

1. Instruct your brokerage company to transfer the shares to Galaxy’s transfer agent.Galaxy uses Equiniti (“EQ”) as its primary transfer agent.Transfer agents are entities registered with the U.S. SEC and are responsible for preserving and maintaining official shareholder records of each of our stocks, performing daily tasks including tracking and facilitating equity changes, calculating and paying cash dividends, handling stock splits, mailing and delivering agent materials, and performing other administrative tasks.Asking your brokerage firm to transfer the shares to the transfer agent for that stock (i.e. transferring to a direct registration system, referred to as “DRS”) may sound tricky, but the two authors of this article completed the task in minutes by having a live web chat with Fidelity and Charles Schwab.See the figure below.(It takes about 10 minutes).

Once processed, your stock will be transferred from your brokerage firm’s account with the Deposit Trust (DTC) to your Galaxy name and registered by our transfer agency EQ.You still own these stocks, but now your ownership is recorded by Galaxy and its transfer agencies.(It takes about 3 working days).

2. Instruct Equiniti to transfer your stock to Superstate’s Onchain Qualified Stock Account.Please email Investor.Relations@Galaxy.com to indicate that you have used DRS to transfer Galaxy stock to EQ and wish to tokenize it.Galaxy’s investor relations team will provide you with an EQ account and a simple form, please fill in and submit.(About processing time: about 4 hours).

3. Superstate will then mint your shares in the form of 1 GLXY token per share as its direct, legal version.This requires you to have successfully joined Superstate and add the Solana address to your Superstate account profile.After that, you can click the “Tokenization” button on the Superstate website, which will be minted in the form of 1 GLXY token per share.(It takes about 10 minutes).

4. Superstate will deliver the on-chain GLXY shares (tokens) to your Solana wallet, you are now free to store them in your self-custodial wallet, or send them, receive or transfer them to other registered addresses.

5. To reformat the GLXY tokens back to traditional format, perform these steps in reverse.Contact Superstate and ask them to transfer your shares back to EQ and then ask EQ to transfer the shares back to your brokerage account.Crucially, any GLXY equity token holder who joins Superstate can do this, whether they are the investors who originally created the stake.

Note that this process specifically describes the tokenization and de-tokenization process that connects Nasdaq-listed traditional Galaxy stocks with tokenized on-chain GLXY stocks.If you just want to buy existing on-chain GLXY stock, just register Superstate on Superstate.com/Register and purchase on-chain GLXY stock from existing holders.As more and more GLXY stocks are tokenized, we expect on-chain liquidity to increase, and most on-chain shareholders no longer need to undergo this increase and redemption process.In the long run, while this overweight and redemption process will always apply to all shareholders, regardless of their size or complexity, we expect this process to be primarily used by established trading companies.

Galaxy’s approach Vs “packaging” equity structure

We firmly believe thatTokenized stocks must be tokens that can give actual ownership of their underlying stocks.As mentioned above, this has not made any substantial progress in the United States due to technical and regulatory reasons.The emergence and application of public chains should not offset the decades of progress in the US capital market, but should supplement and enhance them.

We believe that tokenized equity packaging will split the relationship between the issuer and shareholders, which will be detrimental to both parties.If you buy stocks in a company, you should reserve all economic and legal rights associated with holding stocks in that company, regardless of the form of these stocks.Given that people need to use the licensing, composable, efficient and transparent nature of public chains to deal with issues such as equity securities, it is understandable that many companies have created structures that circumvent the U.S. securities laws.However, weDon’t consider packaging equity tokens to be a long-term viable or preferable solution, so our entire research on the field revolves around how to bring real stocks into blockchain.

Why choose Solana

Galaxy chose Solana as its first public blockchain for tokenized stocks for several reasons.

-

Solana is a decentralized Layer-1 blockchain.We believe that tokenized equity must be traded on the highly decentralized public Layer-1 blockchain, rather than on the Layer-2 blockchain, because in the Layer-2 blockchain, individual companies or foundations can unilaterally control important functions such as transaction sorting, transaction fees or settlement finality.For example, while today’s Ethereum Rollup may have a unilateral exit function (assuming the relevant assets exist on both Layer-2 and Layer-1), some Rollup functions can be controlled by a single sequencer fully operated by a single company or foundation.While these operators may be altruistic and even attempt to protect on-chain shareholders from problems such as high fees or delayed settlement, Rollup operators still have the theoretical unilateral, centralized ability to take (or fail to take) actions that may harm the interests of on-chain shareholders due to negligence or maliciousness.Furthermore, the ability to unilaterally exit Layer-2 depends on whether the relevant assets are available on the connected Layer-1.Therefore, in terms of on-chain securities available on Layer-2 Rollup, we believe that they should be issued primarily on the Layer-1 blockchain to retain the ability of Layer-2 users to unilaterally exit Rollup.We plan to support tokenized GLXY shares on Ethereum Layer-1 in the future and will continue to evaluate the applicability of other blockchains, including Ethereum Layer-2.

-

Solana aims to become “Nasdaq in the blockchain world”.Its high-speed settlement, local fee market, efficient network stack and flexible developer base make it an excellent carrier to lead the integration of traditional and decentralized capital markets.While these updates focus mainly on improving Solana’s bandwidth and reducing latency, Solana developers will launch more updates in the future to improve the microstructure of the market on Solana.Under its “Internet Capital Market” framework, Solana developers plan to add asynchronous program execution and multiple concurrent verification leaders, which will significantly improve parallelization capabilities and application control execution capabilities, thereby providing more flexible design space for applications, especially market applications.We also expect Solana to be the first to adopt DoubleZero, a new global fiber network tailored for high-speed blockchain settlements, which will further strengthen Solana’s position as a true competitor to the traditional financial system.Finally, the update release of Solana’s existing validator client Anza and the launch of a new validator client Firedancer will further improve network performance and resilience.

-

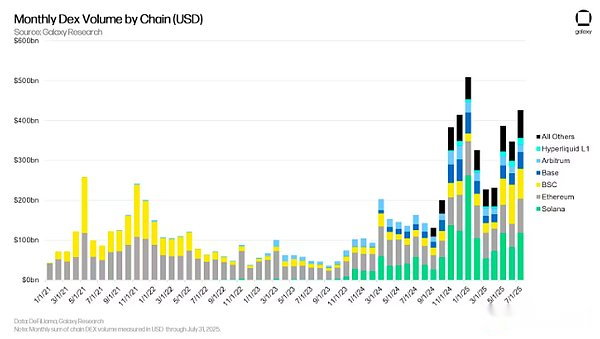

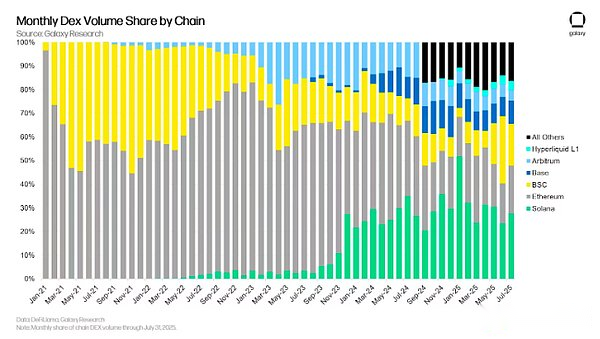

Solana has the most DEX activity.As for on-chain spot trading activities, Solana has topped the list of monthly transaction volumes since October 2024.While Solana has not yet led the way in on-chain credit (probably because its higher staking annual interest rates provide a competitive alternative) or on-chain perpetual contracts, Solana has become the preferred Layer-1 blockchain for spot transactions with high transaction volumes, fast settlements and low fees.With its huge retail user base, Solana has also become one of the most accessible networks in the cryptocurrency space, thus driving the development of a wide range of frictionless introductory solutions.

Securities, AMM and regulatory issues

When will the on-chain GLXY token be traded on DEX?

The US SEC is working to address the question of whether or how to regulate decentralized exchanges on public chains.The main purpose of U.S. securities laws is to protect investors from opacity, conflict of interest and arbitrary powers of centralized intermediaries such as brokers, traders and exchanges.Because some of these institutions may unilaterally control user funds, make mistakes in transactions, conflict with customer interests, and even malicious behavior, they face strict supervision, supervision and regulatory requirements.We believe that the decentralization, automation and transparency of public chains and decentralized financial applications largely eliminates the necessity of these requirements.Other laws and regulations may need to be adjusted to adapt to the new reality that intermediaries, issuers and investors have different roles than they are now.usIt is not clear when the on-chain GLXY token will be available in automated market makers (AMMs) or other forms of decentralized exchanges, but we are working closely with stakeholders including the SEC to achieve this.

DEX is not an “exchange” and should not be regulated

Decentralized exchanges (“DEX”) are fundamentally different from traditional exchanges regulated by the Securities Exchange Act of 1934 and we believe that they should not be classified as “exchanges” within the statutory framework of the Act.

First, Article 3(a)(1) of the Securities Exchange Act defines an “exchange” as “an organization, association or group that provides a trading market or convenience that brings together buyers and sellers of securities.”Here, “organization, association or group” is to be understood as applicable only to an individual and does not include or consider computer programs.DEX is not a “personal organization” (it is not an organization at all); nor is it a “personal association” (it is not an association at all); of course it is not a group.

This statutory definition clearly presupposes a centralized, identifiable entity that has independent control over market operations.In sharp contrast, many DEXs operate independently through automatic execution of smart contracts on decentralized blockchain networks, but lack any centralized institutions that impose governance controls.Therefore, from the perspective of statutory interpretation alone, we believe that DEX does not comply with the definition of “exchange” in the Stock Exchange Law.

Secondly, traditional exchanges have and exercise their own regulatory powers, actively manage market operations, formulate membership standards, implement regulatory compliance, and intervene when necessary to adjust or correct transactions.Autonomous DEX essentially lacks the ability to intervene subjectively or operate autonomously, because transactions are carried out deterministically through transparent, pre-programmed rules embedded in an unchangeable smart contract that cannot be changed once these rules are executed.There is a significant difference between autonomous DEX and traditional exchanges regulated by the Securities Exchange Act, mainly due to their complete lack of autonomy.

Third, the regulatory framework of the Securities Exchange Act empowers exchanges with specific regulatory responsibilities, such as member review, compliance supervision and disciplinary action, provided that the exchange is a centralized entity capable of performing these functions.Autonomous DEX structurally excludes these functions due to the lack of centralized governance or identifiable regulatory entities.Trading and market functions are automated, transparent and non-discretionary, making the centralized regulatory responsibilities envisaged by the Securities Exchange Act neither necessary nor possible for DEX.

Fourth, the legislative intention of the Securities Exchange Law is to reduce the risks of manipulation, fraud, conflicts of interest, information asymmetry and other abuse caused by centralized intermediaries.Autonomous DEX essentially eliminates these risks through decentralized transparency, automated execution and immutable auditability.Due to the lack of discretionary human intervention, the Securities Exchange Act effectively resolves regulatory issues, making it unnecessary to apply to DEX, and is contrary to the original intention of legislation.

Finally, the classification of autonomous DEX as an exchange under the Stock Exchange Act will undermine policy objectives that promote innovation and market efficiency.The traditional regulatory framework designed for centralized entities imposes unnecessary regulatory burdens, and autonomous DEXs cannot meet these burdens, thus stifling the technological advances inherent in decentralized finance and failing to provide corresponding regulatory advantages.

Therefore, DEX is not in line with the statutory definition or basic policy principles of the “exchange” by the Stock Exchange Act and should be excluded from its regulatory framework due to its autonomy, decentralization, transparency and certainty operational characteristics.

The principle of autonomy in AMM

We strongly believe thatDecentralized, transparent automated market makers (AMMs) do not require registration as an exchange or alternative trading system (ATS), and many AMMs may not be able to register due to the lack of identifiable operating entities..The reason is simple: autonomous, automatic and publicly available programs do not require supervision, and the current form of supervision is tailored to regulate and control personnel in centralized exchanges.

From a regulatory perspective, if autonomy excludes DEX from the scope of the rules of the Securities Exchange Act, it is crucial to establish a principled and manageable framework to determine what qualifies as an autonomous system compared to non-autonomous places such as Nasdaq.

Consistent with other regulatory analyses, we believe that the following factors indicate DEX is autonomous:

1. Lack of discretion.The platform must operate in accordance with pre-programmed, deterministic rules embedded in smart contracts that can be executed automatically.No entity, individual or group (including platform developers) may unilaterally modify, stop or affect the settlement, execution, matching or operation of deployed transactions, unless a governance process that is prior disclosure, transparently documented and requires extensive decentralized consensus is followed.

2. Transparency and verifiability.All operational logic, including transaction execution, matching algorithms, liquidity supply, settlement finality, and the governance process itself, must always be fully open source, transparent, auditable and publicly verified.Transparency includes full public access and open source availability of the code base, ensuring that there is no undisclosed discretionary control in external verification.

3. Self-execution and deterministic settlement.The platform must execute all transactions independently without manual intervention or judgment.Once initiated, transactions conducted through the agreement will not be blocked, reviewed or revoked by any identifiable central intermediary, administrator or other party.

4. Neutral and non-discriminatory access.The platform must provide open, neutral and extensive access to all eligible participants.No central or identifiable administrative agency shall give any preferential treatment.

5. Decentralized operation control.Operational functions must be distributed in a network of independent participants, each lacking the ability to direct, veto, or otherwise control the platform results.Governance and changes in protocol operations, if any, must be clearly in the hands of a widely distributed community, rather than in the hands of a centralized management structure or identifiable controller.

The term “decentralized exchange” is inappropriate, and at least there is a risk of confusing functions with regulatory status.Despite the name, in a legal sense, DEX is not an “exchange” as defined by the Stock Exchange Act.Instead, it should be understood as an autonomous custody mechanism designed to promote bilateral, peer-to-peer transactions between voluntary counterparties.

This difference is crucial becauseThe U.S. Securities Act does not prohibit voluntary, non-fraudulent direct securities transactions between individuals.Intermediary agencies are regulated, but not mandatory.Both parties who meet directly and agree to trade their own securities are free to conduct such transactions as long as they do not “operate” the exchange or act as a legally defined broker or dealer, without triggering the registration and operational requirements of the Securities Exchange Act.

The historical problem with this kind of interpersonal transaction is trust and pricing.At settlement, neither party is willing to deliver cash or vouchers first because they are worried that the other party may not be able to perform the contract.Traditionally, this problem has been solved by hiring a trusted custodian agent or liquidation agency.For the escrow agent, the seller will guarantee the delivery to the escrow agent, the buyer delivers the cash, and the escrow agent will deliver each amount to the other party at the same time.For clearing institutions, the intermediary institutions provide guarantees to both parties to the transaction and bear the performance risks themselves.Although these patterns are effective, there are two key limitations:

-

Central intermediary dependency – Each process relies on a trusted, centralized third party.

-

Static pricing risk – Once a transaction occurs, the price is fixed, even if the market may fluctuate.Therefore, the profits received by the seller at the time of settlement of the transaction may be lower than the market value at that time (or the price paid by the buyer is higher than the market price at that time), and these risks themselves will be further complicated by the margin system.

The AMM architecture solves these two problems.”Hosting” or clearing agency is not a manual intermediary, but an immutable on-chain program that stores assets in smart contracts, executes agreed pricing functions, and performs settlements atomically, eliminating counterparty risk.In addition, unlike traditional custody, AMM can continuously update prices according to the algorithmic pricing function to ensure that transaction prices better reflect the current market conditions.Since transactions are settled in almost real time, no clearing agency is required.

When liquidity providers contribute assets to the DEX pool, they actually deposit the assets into an autonomous escrow account and instruct the program to provide the assets to any counterparty willing to trade at a contract dynamic price.Liquidity providers do not need to negotiate directly with counterparties; instead, they interact with pre-set pricing and settlement logic in the agreement.Essentially, this is an automated over-the-counter trading (OTC) custody arrangement—no need to rely on centralized operators, nor does it possess the “exchange” characteristics stipulated in the Stock Exchange Act.

The Great Future of On-chain Securities

Every few decades, a new technology emerges that not only improves an industry or practice, but also revolutionizes it.Tokenization will have the same impact on stocks and the broader financial system.We believeThe impact of tokenization on value will be the same as the impact of the Internet on information.While the tokenization of GLXY today may be just a small step in this long evolution, we believe that the structure proposed in this paper (and implemented on-chain) has the potential to become HTTPS for stocks: a security standard for building trust in a new digital medium that has led to widespread adoption.

Although traditional payment systems and capital market infrastructure seem efficient to most people, they are still mostly a series of complex pipelines, like huge mazes operated by numerous intermediaries, intertwined with each other through different custom connections, and are often written in outdated code.Modern markets and payment infrastructure are built on decades-old old versions that require advanced degrees to understand.If these systems were designed from scratch using modern technology, they would almost certainly not be what they are today.

There is no doubt that compared with traditional capital markets, public, decentralized blockchains are more efficient, transparent, longer lasting and more resilient recording and settlement systems.If we are going to rebuild these systems from scratch, the public chain will undoubtedly play a key role.But since we are not rebuilding from scratch, we need a model to connect both systems, and we believe our model is the most efficient, compliant, transparent and innovative.

Evaluate opportunities for on-chain securities

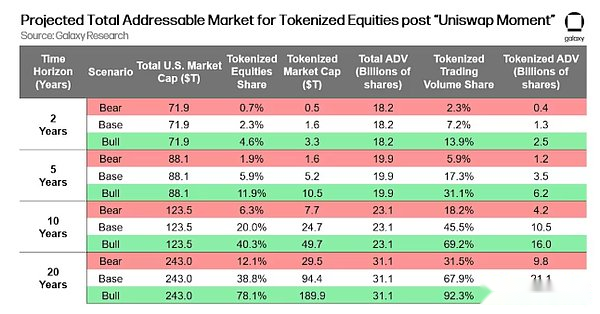

We believe that once equity securities are issued and on-chain transactions in practical forms such as the structures we create, large-scale adoption will begin.The decentralized transaction structure will be considered fairer, faster, cheaper and safer than traditional methods.By then,On-chain securities will usher in the “Uniswap moment”, the world of centralized trading will begin to pour into on-chain transactions in large quantities.We simulated the growth of the on-chain market after this moment.

To estimate the potential size of the on-chain stock market, we use historical benchmarks to predict U.S. stock market caps and total stock trading activity: driven by decades of electronicization and automation, the nominal growth rate is about 7% and the total stock trading volume is about 3%.

We then model the S-curve as tokenized stocks in bear, benchmark and bull scenarios and calibrate them based on three precedents: decades of ETFs’ rise since the 1990s, faster hockey stick-like growth in spot crypto ETFs recently, and growth in tokenized money market funds, which validate the demand for on-chain packaging.

To convert value migration into traffic migration, we assume that tokenized tracks have higher turnover rates than traditional tracks because they are all-weather, instant settlement, and well-funded, so as the adoption rate increases, the volume share will grow faster than the market cap share.

We also use the crypto market’s transition from CEX to DEX (total transaction volumes from 0% to nearly 20% in five years) as evidence that order flows can quickly migrate once liquidity and user experience on the new track are parity.

Total market value and Total Daily Average Trading Volume (ADV) remain consistent for each time period scenario, we derive tokenized market value, tokenized transaction share, and tokenized daily average trading volume based on these adoption rates and volume assumptions.Like any model, this model has limitations, especially sensitivity to volume gaps, S-curve calibration, regulatory timing, and price combination differences between tokenization and traditional groups.

Risk and Disclosure

Galaxy and Superstate have been working to eliminate or reduce risks to investors and the market.However, given the novelty of this equity investment model, it is crucial for investors to understand various risks.

Holders of tokenized GLXY may lose access to their wallets.Similar to missing security certificates, Superstate can reissue tokens into a new wallet controlled by shareholders if the key is lost.Since Superstate tracks all on-chain flows of tokenized GLXY between shareholders and all shareholder information is published, Superstate can reissue tokenized shares into new wallets controlled by shareholders while canceling unrecoverable shares.Note: If the wallet key is lost, GLXY shares can be recovered, but other assets (such as SOLs that do not require permission) will not be recovered after the wallet key is lost.

The price of traditional GLXY may differ from that of tokenized GLXY.Galaxy will fully support its on-chain stocks to trade in future DeFi applications, provided that regulation is clear enough.Creating a market structure that encourages DeFi and traditional exchange market prices to remain comparable is the company’s top priority.However, the on-chain securities market is still in its infancy. Even if automatic market maker (AMM) trading is enabled, it cannot guarantee that the liquidity and orderly market of tokenized GLXY can develop or continue.In addition, if tokenized GLXY starts trading on decentralized exchanges, it is worth noting that the liquidity, trading volume, transparency or regulatory strength of decentralized exchanges may be significantly insufficient compared to national stock exchanges such as Nasdaq.This could disperse cross-platform liquidity, hurt price discovery, expand bid-ask spreads, and lead to persistence in price differences between tokenized GLXY and traditional GLXY – especially if arbitrage is subject to operational or regulatory restrictions.

In addition, professional traders may face unclear or changing obligations when interacting with on-chain securities such as tokenized GLXY, andThe applicability of the U.S. federal securities laws and other regulations to tokenized securities transactions remains uncertain.This may prevent or crack down on trading of these companies holding, trading or contributing tokenized GLXY, further limiting liquidity.The decline in liquidity of tokenized GLXY, whether due to unfamiliarity among ordinary investors, uncertain demand, operational friction, poor connection between the tokenized GLXY market and the traditional GLXY market, may cause the trading price of tokenized GLXY to fall, and such negative price signals sent by the tokenized GLXY market may have an adverse impact on the trading price of traditional GLXY.

A core approach to encouraging cross-platform pricing consistency is to build and simplify the bridge between traditional finance and decentralized finance.In the first phase, Galaxy built this “bridge” that enables shareholders who join Superstate to deliver traditional stocks to Superstate to “create” tokenized stocks, or deliver tokenized stocks to Superstate and “redeem” them to traditional stocks.If there is a price difference between platforms, we expect shareholders, especially experienced shareholders, to use this bridge to narrow any spreads that occur.However, the use of bridges may take some time to normalize, so the ability of market participants to arbitrage spreads may be hampered.

The US SEC may rule that we may not to tokenize common stocks in this way.While we believe that this tokenization process is not only revolutionary in scope, but also well-designed and in line with current securities laws and regulations, it is also possible that the SEC will make different rulings.If the regulator determines that the platform, mechanism or participant involved in the tokenized GLXY secondary market transactions fails to comply with applicable laws, we or market participants may face enforcement actions or fines, or be required to revoke or reorganize certain parts of the project.If Galaxy is ordered to revoke its on-chain stock plan, Superstate can suspend token contracts, recall all tokenized stocks, and then work with on-chain shareholders to reformat the tokenized stocks into traditional formats for re-delivery to the traditional market ecosystem.However, this process can take time and while it is in progress, it may be difficult for shareholders to buy and sell their tokenized Galaxy stocks.These risks may lead to a decrease in investor confidence, reduced participation in tokenized GLXY transactions, and have corresponding negative impacts on the trading price, volatility and/or liquidity of traditional GLXYs.

FAQ

Can anyone buy, sell or hold GLXY on the chain?

Galaxy and Superstate require that all on-chain GLXY holders must register on Superstate, including authentication (“KYC”) and address “whitelist”.Anyone who can register for Superstate can hold on-chain GLXY, which covers almost everyone in the world, except for some government rejection lists such as the Special Designated Nationals (“SDN”) list of the U.S. Office of Foreign Assets Control (“OFAC”), also known as the “sanctions list.”

Only addresses that have been added to the Superstate and added to the token contract “Allow List” can hold the tokenized share of GLXY.Attempting to transfer the on-chain GLXY share to an address that is not on the allowable list will fail at the smart contract level.

Our digital transfer agents must be aware of all addresses and identities for two main reasons: 1) to ensure that Galaxy’s books and records accurately reflect equity conditions for regulatory and operational purposes, including maintaining contact with shareholders when proxy voting, dividends or other company actions; 2) to comply with important anti-money laundering and anti-terrorism financing laws and regulations.If the on-chain equity tokenization structure does not include identity verification (especially the issuer’s own identity verification), it is possible that bad actors can hold the company’s equity and make it difficult for token holders to truly acquire or exercise the company’s real equity ownership.

What if I lose my wallet key?

As Galaxy’s digital transfer agent, Superstate maintains books and records that contain all ownership information of GLXY on-chain, including holders, transfer records and any transaction records.If the holder of GLXY on-chain cannot access its wallet, the investor can request a digital transfer agent to cancel and reissue the tokenized shares to a new wallet.Note: Superstate can recover GLXY shares on the chain if you have no access to your wallet and keys; however, if the wallet key is lost, other assets (such as SOLs that do not require permission) cannot be restored by Superstate or Galaxy.

How is the tokenized GLXY different from other on-chain stocks?

To our knowledge, GLXY is the first U.S. stock to exist and trade on the public chain.The on-chain GLXY token represents Galaxy Class A common stock, with all rights as other forms of stocks, such as stocks in traditional brokerage accounts.

Other structures, such as those that rely on a packaging or synthetic model of a special purpose carrier (SPV), mostly do not represent direct claims against the issuer of the underlying stock, but rather derivatives or shares of a particular special purpose carrier (SPV), which may itself hold shares in the underlying stock.These “packaged equity tokens” are usually issued by offshore SPVs and are not subject to the framework of U.S. securities laws and regulations.

If the packed equity token holder has rights over the issuer, such as the right to vote on the corporate governance, the right to collect dividends, or the right to participate in other corporate actions, these rights may be limited to the special purpose carrier itself, rather than the underlying issuer.Whether the packaging equity token holder reserves any continuing rights to the subject issuer depends on any contract or obligation signed or agreed upon between the token issuer and the token holder.

When can tokenized GLXY be traded in a DeFi application?

We believe this is the first time that a US listed company has allowed its shares to exist on the public chain in the form of tokens.This achievement is thanks to the great technical and regulatory efforts of Galaxy and Superstate, but it is only the first step.

Although currently Superstate users can trade GLXY on-chain via a peer-to-peer approach, we have not yet implemented trading GLXY on DeFi applications such as automatic market makers AMMs.Just as Galaxy can track and limit the transfer of on-chain GLXY to Superstate users, Galaxy can also block or control which AMMs these tokens can interact with.

We expect that once the regulatory mechanism is clear enough, we will allow our tokens to be deposited and withdrawn into the AMM pool.Since these are real shares of Galaxy Class A common stock, there are practical regulatory considerations.

Are on-chain shareholders of tokenized GLXY subject to maximum extractable value (MEV) restrictions?

Since Galaxy’s token contract requires that all addresses must be in the “Allow List” to hold our on-chain share, unknown third parties, including MEV robots, cannot interact with the token.Therefore, our on-chain share will not be affected by preemptive transactions, resells, sandwich attacks or other MEV attacks conducted by unknown third parties unless they work with Superstate and pass Superstate’s KYC audit.

Can my broker help me interact with tokenized GLXY stocks?

Galaxy does not restrict any party from joining Superstate to buy, sell, hold or transferring its tokenized shares unless the party cannot successfully pass Superstate’s identity verification process (as described above).Like any entity, market intermediaries (including brokerage dealers) can also join Superstate.However, given the limited regulatory guidance, it is not clear to us which registered broker dealers or financial advisers have extensive activities involving tokens (whether securities or non-securities), so there may not be any institution that can provide services related to on-chain securities at this time.

In the absence of brokerage dealers, the on-chain stock market will be mainly custodialized by investors and ultimately enable direct interaction with the decentralized trading agreement without the need for intermediaries.We are working with the US SEC to promote the improvement of the current securities laws so that existing intermediaries can interact with public chains, but it is not clear when it will be possible.

What if there is a problem with my token?Who should I contact?

Holders of tokenized GLXY can contact Superstate at any time.Since all holders must create an account in Superstate during the registration process, on-chain shareholders simply need to log in to their Superstate account and contact our digital transfer agent.If for some reason no contact is possible, on-chain shareholders can contact investor.relations@galaxy.com at any time, just like other Galaxy stock holders.