Authors: Sha Jun, Yu Zhixia

With Trump officially signing theThe GENIUS Act also marks the first time the United States has officially established a regulatory framework for digital stablecoins, and it also means that many stablecoin issuers and companies are facing a new round of challenges.I believe many people will be unfamiliar with the GENIUS Act and may have more or less the following questions:

-

USA”What regulatory measures for stablecoins are mentioned in the GENIUS Act…

-

The bill is rightWhat are the impacts of USDT and Tether…

-

Can Tether take corresponding measures…

-

What is the difference between this bill and Hong Kong’s Stable Coin Act…

Crypto Salad TeamThe above questions will be answered one by one.

(Picture source: CCTV Program Official Website)

“What exactly is it about in the GENIUS Act?

First, let’s take you to learn about thisGENIUS Act.“The GENIUS Act is the “Guiding and Establishing the Innovation Act of the United States Stablecoin Country”, also known as the “Stablecoin Act” of the United States.The bill aims to establish a comprehensive legal and regulatory framework for payment of stablecoins in the United States to promote financial innovation, protect consumers, strengthen monetary sovereignty and maintain financial stability.The following is theA brief introduction to the regulatory framework of the GENIUS Act:

1.The core definition and scope of the bill: The bill mainly regulates payment stablecoins, which are defined as digital currencies used for payment or settlement and are pegged to the value of fixed currency.This bill requires onlyOnly “approved payment stablecoin issuers” can issue stablecoins in the United States.The approved issuer must be a subsidiary of an insured deposit institution, a federally qualified non-bank payment stablecoin issuer, or a state-qualified payment stablecoin issuer.(Basic basis:GENIUS Act, Section 2(22))

2.Regulatory structure of the bill:The bill establishes a unique dual-track regulatory system.For the volume of issuance exceedsThe $10 billion stablecoin will apply to the Federal Reserve’s regulatory framework for deposit institutions and the Agency’s framework for non-bank issuers.For issuers with circulation less than $10 billion, they can choose the state regulatory path.Reserve requirements of the bill: One of the most important consumer protection measures of the bill is the 100% reserve requirement.The issuer must hold at least one dollar of license reserve for each dollar of stablecoin.Licensed reserves include: coins and currencies, bank deposits, short-term treasury bonds, repurchase agreements, money market funds, and central bank reserve deposits.(Basic basis:GENIUS Act, Section 4(a)(1))

3.Transparency and disclosure requirements for the bill:The bill requires issuers to establish and disclose stablecoin redemption procedures and periodically report outstanding stablecoin and reserve compositions.(Basic basis:GENIUS Act, Section 6(a)(2))

4.National Security and Anti-Money Laundering Articles of the Act:The bill classifies payment stablecoin issuers as financial institutions under the Bank Secrecy Act, which means they must: maintain effective anti-money laundering and sanctions compliance programs; retain appropriate records of stablecoin transactions; monitor and report suspicious activity; implement policies to prevent, freeze and reject transactions that violate federal or state laws; establish customer identification programs.(Bill basis:GENIUS Act, Section 8(a))

The billWhat are the impacts of USDT and Tether?

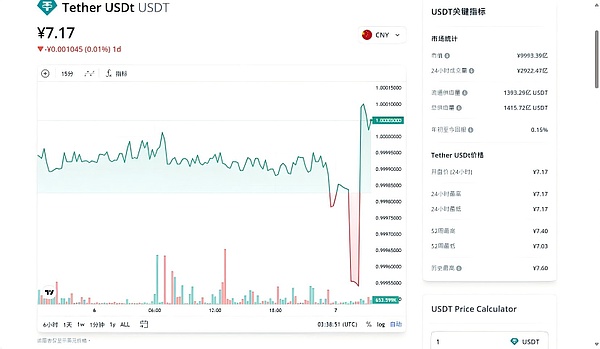

Let’s explain what isUSDT.USDT is one of the most representative stablecoins in the current cryptocurrency market, and its full name is Tether.It isTether, issued by Tether, aims to maintain currency stability by pegging to fiat currencies (mainly the US dollar), is an important liquidity tool and value storage medium in the cryptocurrency market.The core design of USDT is to promise that for every USDT issued, a USD will be deposited as a reserve in the bank account, and in theory maintains an anchor relationship of 1:1.Users can convert USDT into USD at any time to ensure stable currency value.Compared with traditional cross-border remittance methods, USDT transaction speed is faster, the handling fee is relatively low, and it is not restricted by regional and bank business hours, so it can achieve more efficient cross-border fund transfer.

(Picture source: CoinMarketCap)

According to the content of the bill, it is certain that the bill seriously restricts theDevelopment of USDT.“The GENIUS Act is a US bill, and USDT is also a product of the US. After this bill is implemented, according to the content of the GENIUS Act mentioned above, Tether is almost certainly unable to fully meet the compliance conditions.So in the future of the stablecoin market, Tether’s market share will only be continuously encroached until there is a replacement for it.Even if Tether still has a share of USDT in the future stablecoin market, it is highly likely that USDT will only be used in some specific links.

As for whyTether cannot meet its requirements, so the Crypto Salad Team will take you to sort out the core content of the bill:

-

First, the bill clearly statesStable coins are not subject to securities and commodity supervision systems, but are mainly regulated by the banking system;

-

Secondly, the reserves required by the bill must be made of high-quality current assets.For example, US dollar cash, Federal Reserve deposits, bank demand deposits,Treasury bonds that expire within 93 days or overnight reverse repurchase agreements, etc.,The issuer of the stablecoin is required to maintain an equal value to the stablecoin it issues (1:1) reserve assets to support the payment stablecoins in circulation issued by them.(Basic basis:GENIUS Act, Section 4(a)(1))

-

In addition,The total issuance of payment stablecoins combined exceedsA stablecoin issuer approved for payment that is not subject to the requirements of the Securities Exchange Act 1934 report must prepare annual financial statements in accordance with the United States General Accounting Standards (GAAP) to disclose any related party transactions;(Basic basis:GENIUS Act, Section 3(10)(A))

(Picture source: CCTV Program Official Website)

-

fourth,Regarding Anti-Money Laundering and KYC (known Your Customer, “Know Your Customer”) are one of the core regulatory requirements in the financial industry and compliance field.The requirements for verifying customer identity through a series of processes, evaluating risks, and preventing illegal activities such as money laundering, terrorist financing, fraud, etc. are also very strict. Issuers are not allowed to misappropriate reserve funds and must issue monthly reserve certificates audited by the certified public accounting firm.and comply with the Bank Secrecy Act;(Basic basis:GENIUS Act, Section 3(5)(A))

-

fifth,For stablecoin holders, the bill gives a super priority.In other words, if the issuer bankrupts the stablecoin holder’s claim takes precedence over all other creditors, thus realizing the “priority right to repay”, the “priority right to repay” also encourages more people to purchase stablecoins issued by the issuer, while further ensuring the legitimate rights and interests of stablecoin subscribers.(Basic basis:GENIUS Act, Section 10 (3))

And forFor USDT’s issuing company Tether, it cannot meet the many requirements of the GENIUS Act.

first,exist”The requirements for reserves in the GENIUS Act are “requiring full reserve support”, while USDT’s current reserves are not up to standard, only about 85%, so they do not meet the standards of the GENIUS Act, which may lead to fluctuations in the price of stablecoin and collapse of user trust.

second,Tether’s auditing agency is BDOItalia, which itself does not meet the standards of the US listed company Accounting Oversight Committee..

third,Tether also needs to sell its non-compliant asset reserves.For example, Bitcoin, precious metals, corporate notes and guaranteed loans, etc., must be replaced by compliant assets.

in addition,Tether has a high market value, and its market value has reached the standard that requires direct federal regulation.Therefore, the Crypto Salad Team believes thatTether has difficulty supporting regular monthly disclosures and strict anti-money laundering requirements (the total amount of stablecoins issued exceeds $50 billion and non-SEC reports must be conducted for annual financial statement audits).

Apart fromTether, Circle (USDC publisher), Paxos (PAX, USDP publisher), and Gemini (GUSD publisher) are subject to varying degrees of restrictions on the GENIUS Act.For example: liquidity, disclosure audit and other requirements of reserve assets,therefore,”The GENIUS Act affects not only an issuer, it has a huge impact on the entire stablecoin market.

(Picture source: CCTV Program Official Website)

according to”GENIUS Act, if stablecoin issuers led by Tether are unable to meet the requirements of the bill, they will face serious penalties.

First, if Tether fails to complete US entity registration or reserve rectification within the transition period, its USDT will be deemed to be an “illegal payment instrument”, and the issuance itself constitutes an illegal act and may face criminal charges.(Basic basis:GENIUS Act, Section 4(a)(12)).

In addition, three years after the bill came into effect, any foreign stablecoin issuer that has not been licensed by the United States (includingTether will be prohibited from issuing, selling or providing transaction services within the United States.Digital asset service providers (such as exchanges) will face a daily fine of up to $100,000 if they violate this provision, and Tether, as an issuer, may be included in the “non-compliance list” released by the Treasury Department, resulting in its stablecoin being forced to be removed from the shelves by US platforms.(Basic basis:GENIUS Act, Section 18 (a)(4)).

Of course, the Ministry of Finance may apply for non-compliance in reserve assets (such as holding non-licensed assets), failure to disclose reserve reports on time, or violation of anti-money laundering obligations, etc.Tether imposes a fine of up to $1 million per day(Basic basis:GENIUS Act, Section 18 (a)(4)).

Faced with such many unfavorable consequences, it can be said thatThe implementation of the GENIUS bill has issued an “ultimatum” to stablecoin issuers like Tether.

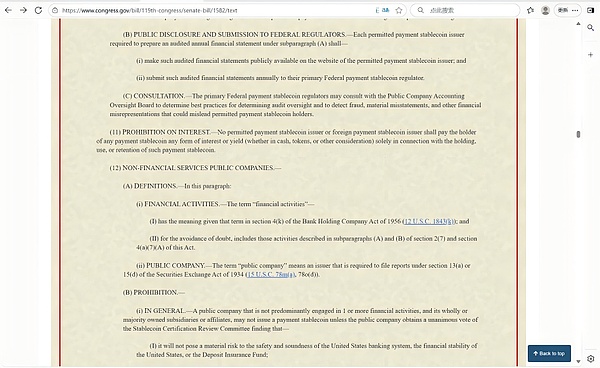

(Picture source: Congress.Gov)

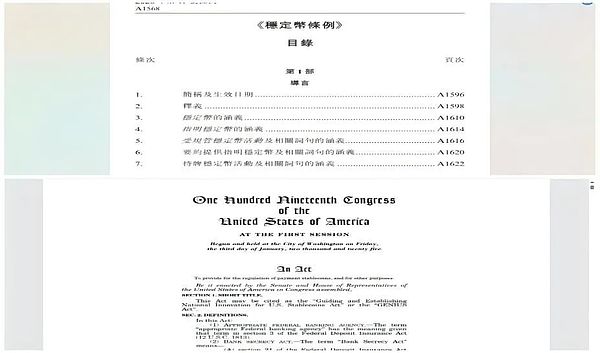

“What is the difference between the GENIUS Act and the Hong Kong Stablecoin Ordinance?

now,Trump has officially signed theGENIUS Act means that the GENIUS Act is officially implemented, andCoincidentally, Hong Kong’s Stablecoin Ordinance alsoComing soonAtIt will be implemented from August 1, 2025, and both regulations are regulatory policies for the cryptocurrency “stable currency”.Then many people may ask,These two are from two different regionsWhat is the difference between the “stablecoin regulations”?In other words, if you want to issue stablecoins in these two regions, then what is the difference between being controlled by the United States and Hong Kong?The following will answer you.

First of all, the access requirements of issuing entities in the two places are different.If you register in the United States, you must be a registered entity in the United States, or throughA foreign entity registered by OCC (need to prove that the home country’s supervision is equivalent) must be completed within three years, otherwise it is prohibited to enter the US market.The entity registered in Hong Kong must be a Hong Kong registered company or an overseas bank approved by the HKMA (such as HSBC and Standard Chartered). Non-bank institutions must pay the actual share capital of HK$25 million (banks are exempted).

Secondly, the reserve assets requirements of the two are different.Cash only andUS Treasury bonds that expire within 93 days are reserve assets, while non-compliant assets such as corporate notes and crypto assets are prohibited as reserve assets.Hong Kong requires reserve assets to be strictly consistent with the anchor currency (such as Hong Kong dollar stablecoins need to hold Hong Kong dollar cash or short-term bonds), and interest payments to holders are prohibited, which directly restricts “bornInterest Stable Coin” Business model.

Third, the United States and Hong Kong have different requirements for transparency and audit standards.The United States requires the public monthly reserve asset composition, market value and audit report, byGoing on the marketCompany Accounting Supervision Committee (PCAOB)The certification body conducts annual audits,CEO/CFO must sign a compliance statement(Basic basis:GENIUS Act, Section 4(10)(a)(iii)).

Hong Kong also requiresregularDisclose the composition, market value and audit results of reserve assets, but not mandatoryPCAOB qualifications require only “independent audit”.

Fourth, the penalties for illegal acts are also different.In the United States, the maximum possibility of violations is dailyA $1 million fine and could trigger civil compensation and criminal charges (such as up to 10 years in prison for securities fraud).In Hong Kong, a maximum fine of HK$5 million and 7 years in prison for unlicensed issuances, and a maximum fine of HK$10 million and 10 years in prison for fraud.

Comparing the above four dimensions, we can see that Hong Kong is more balanced, stable and innovative, so its policy inclusiveness is stronger, but the competition for applying for licenses is more intense; while the United States focuses more on maintaining the hegemony of the US dollar and imposes strict restrictions on the issuers of US dollar stablecoins.Therefore, there are pros and cons of choosing which country to issue stablecoins.

Interpretation of encrypted salad

Based on this, the Crypto Salad Team believes thatThe introduction of the GENIUS Act sets a critical 300-day window for Tether.Although the bill sets an 18-month (about 540 days) transition period, if Tether fails to come up with a compliance solution that meets the bill’s requirements within 300 days,The market prospects of USDT will be basically set.If USDT cannot pass the US compliance certification, its global market share expansion will be fundamentally restricted – even if Tether continues to issue additional USDT and push up the total token, the decline in its market share will still become an inevitable trend.

Regarding its future direction, the following possibilities can be predicted:

-

First,Tether may choose the “offshore niche” strategy, actively avoid countries and regions with strict stablecoin supervision, and instead indirectly participate in local markets through the transit mechanism;

-

Second, if the company cannot break through the compliance bottleneck, it may cause systemic risks due to the loss of market trust, and will eventually be squeezed out of the mainstream market by other compliant stablecoin issuers;

-

Third, maintain a “trenchy” state of existence – given that there is still some regulatory gray area in the current issuance of stablecoins, USDT still has room for survival in specific scenarios that it penetrated in the early stage, and it will not suddenly withdraw from the market, nor will it be difficult to reappear the dominance of the global market.

In addition, the Crypto Salad Team noticed thatThe GENIUS Act has common characteristics with the Hong Kong Stablecoin Ordinance implemented on August 1:Both of them are“Stablecoin Issuance Rules” are the core legislative orientation,And through the corresponding redemption system and mandatory disclosure requirements for stablecoin issuers companies, they will maximize the protection of investors’ legitimate rights and interests.So despite the regulatory requirements for stablecoin issuance in both regionsDetailsDifferent, butInvestors’ rights and interests can be strictlyofAssure.