Authors: Zhang Jiqiang, Wu Yuhang

Stable CoinEnterdevelopThe fast lane of the world’s financial order has also changed and impactedBecome the focus of market attention.As the core hub connecting the traditional finance and the crypto ecosystem, stablecoins provide a key transaction medium for payment and settlement, cross-border remittance, DeFi (decentralized finance) and other scenarios.However, its operating mechanism also triggered in-depth discussions on the market’s issues such as its value stability, financial system risk impact, monetary system impact, and regulatory adaptability.Against this background, this articleFocus on the operation logic, application scenarios and potential impact of stablecoins, and further analyze its potential impact and reshaping role on the evolution of the monetary system and the development of the financial ecosystem.

Core point

Report core points

Against the backdrop of the prominent risks of the traditional monetary system, profound changes in the global order, and accelerated iteration of new technologies, the international monetary system structure needs to be re-examined.As a bridge for fiat currency to extend to the cryptocurrency field, stablecoins have the dual characteristics of blockchain cryptocurrency and fiat currency, forming diversified application scenarios in cryptocurrency trading, value storage and DeFi.Its development is not only reflected in its driving role in the upstream, middle and downstream of the industrial ecology, but also has a profound impact on the international monetary system, global payment network and financial ecological pattern.At present, countries are competing fiercely in this field. The shift in US policy has had a significant impact on the global market. China has chosen to respond with the policy path of China-Hong Kong pilot and the digital RMB.

Stablecoin Overview

Stablecoins are the bridge derived from fiat currency to the cryptocurrency field, and have the dual characteristics of blockchain cryptocurrency and fiat currency.There are quite a variety of stable currencies, including fiat currency reserve type, crypto asset mortgage type, algorithm type and commodity type. Among them, fiat currency mortgage type has the largest scale, mainly USDT and USDC.The issuance of stablecoins is based on blockchain technology and has the “1:1” anchoring principle, custody, redemption and destruction, secondary arbitrage, incentive guidance and other issuance rules design, making it take into account the dual characteristics of cryptocurrency and fiat currency, and is significantly different from the traditional fiat currency and central bank digital currency and other forms of existence.However, it should be noted that issuance mechanisms and blockchain technology are also the sources of their potential risks.

Stablecoin full chain sorting

The development of stablecoins will play a significant role in promoting the development and change of the upstream, middle and downstream of its industrial chain.From the upstream perspective, stablecoin issuing institutions benefit the most directly, and issuers’ credibility, mechanism design and reserve assets are the core elements that determine the value of stablecoin.From the perspective of midstream, exchanges and blockchain infrastructure are key nodes supporting the circulation of stablecoins. The profit model of exchanges is relatively diversified, and the broker cooperation model of traditional securities and exchanges is developing rapidly.From the downstream perspective, the role of stablecoins has evolved from “help-averse chips within the exchange” to a multi-dimensional financial infrastructure, especially the establishment of a decentralized finance (DeFi) ecosystem is the most promising application direction in the downstream.

The momentum and prospects of stablecoin development

At the macro demand level, the rise of crypto trading, inefficient traditional cross-border payments, storage value, arbitrage and financial management have jointly created the market prospects of stablecoins.At the national strategic level, the shift in US policy has had a great driving effect on the world. Countries have formulated strategic and regulatory frameworks based on considerations such as monetary sovereignty and financial competitiveness, and have pulled stablecoins from the “gray zone” into the “legal express”.China’s choice is worth paying attention to.

On the one hand, it is difficult to implement the RMB stablecoin and go to the public chain, and the development of offshore RMB stablecoin is the key to breaking the deadlock.The current relevant regulations and sandbox testing in Hong Kong, China have been opened, and further testing of offshore RMB stablecoins can be carried out in the future.On the other hand, China’s mobile payments are well developed, and there are not many applicable scenarios for stablecoins. It is safer and feasible to continue to accelerate the development of the digital RMB.

Macro impact of stablecoin development

The impact of stablecoin development on the global monetary system, banking business and liquidity is gradually emerging.First, the development of stablecoins will affect the global monetary system, and the hegemony of the US dollar may achieve on-chain expansion with the help of stablecoins. The systemic transfer mechanism of the US debt crisis has been strengthened again, but technological openness also opens a window for multipolar development; second, the development of stablecoins will have a great impact on banking business and cross-border finance, thereby weakening the transmission efficiency of monetary policy and the ability of national capital control; third, the maturity of the stablecoin system will promote the accelerated development of decentralized finance (DeFi), thereby promoting the migration of traditional financial services to the crypto field; fourth, the impact of stablecoin development on liquidity varies significantly between the United States and non-US countries.

Risk warning: currency and financial sovereignty risks, regulatory restrictions imposed by countries on the stable currency industry chain, and cryptocurrencies exposed technical defects.

text

Since 2024, we have successively launched a series of reports on “The Bottom Logic of the New Era”, focusing on three major era issues: sustained US debt, reconstruction of global order, and AI revolution.The three major issues jointly outline the framework of a new era – the inflation of US debt weakens the global credit anchor, the reshaping of the international order has exacerbated external uncertainty, and the AI revolution has reconstructed the supply and demand structure and productivity form.

As an important part of the reconstruction of the global order, the financial system is also undergoing epoch-making changes.Among them, stablecoins have attracted much attention recently.The major economies in the world areShouldFrequent domain movements:

1)USA:At the policy level, the U.S. House Financial Services Committee passed the STABLE Act of 2025 in April; the GENIUS Act was passed by the Senate in June, pushing stablecoins into the era of federal unified regulation.

At the market level, Mastercard joined hands with MoonPay to launch a stablecoin payment card service in May, and Visa simultaneously launched a stablecoin settlement pilot in six Latin American countries; Circle, the issuer of USDC stablecoin was successfully listed on the US stock market in June, becoming the first mainstream stablecoin issuing institution to be listed.In addition, retail technology giants such as Walmart and Amazon are actively exploring solutions to issue their own stablecoins.

2) Hong Kong, China:The Legislative Council of Hong Kong, China, passed the “Stablecoin Bill” in May, establishing a licensed regulatory system for stablecoins anchored by fiat currencies (the new regulations are expected to take effect at the end of the year), becoming a model for stablecoin issuance and compliance supervision in the Asia-Pacific region.At the market level, Ant International and Ant Digital Technology both said they will apply for stablecoin issuance licenses in Hong Kong (and Singapore), China, to accelerate the application of blockchain and stablecoin technology to cross-border payments and fund management scenarios.

3)Chinese mainland:On June 18, Central Bank Governor Pan Gongsheng mentioned stablecoins for the first time at the 2025 Lujiazui Forum. “With the improvement of efficiency and technology preparation, digital RMB and stablecoins are proposed as feasible alternatives to cross-border settlement… But digital technology has exposed the weaknesses of traditional cross-border payment systems, which are inefficient and vulnerable to geopolitical risks.”

4)Europe&U.K:On May 28, the UK Financial Conduct Authority (FCA) issued regulatory proposals on stablecoin issuance and crypto asset custody.On June 21, the Luxembourg Financial Industry Regulatory Commission issued a Crypto Asset Market Regulation (MiCA) license to Coinbase, allowing compliant crypto services to be provided throughout the EU. Coinbase became the first US exchange to obtain a MiCA license.

Stable CoinEnterdevelopThe fast lane of the world’s financial order has also changed and impactedBecome the focus of market attention.As the core hub connecting the traditional finance and the crypto ecosystem, stablecoins provide a key transaction medium for payment and settlement, cross-border remittance, DeFi (decentralized finance) and other scenarios.However, its operating mechanism also triggered in-depth discussions on the market’s issues such as its value stability, financial system risk impact, monetary system impact, and regulatory adaptability.Against this background, this articleFocus on the operation logic, application scenarios and potential impact of stablecoins, and further analyze its potential impact and reshaping role on the evolution of the monetary system and the development of the financial ecosystem.

The evolution of the international monetary system and the birth of stablecoins

Before formally discussing stablecoins, we might as well look back.Looking at history, behind every major change in the monetary system is the result of the interweaving of pain points of the times and the impulse of innovation.HistoricalThe evolution of the currency form canIt simply boils down to:Physical currency→Metal currency→Paper currency(Peer-to-peer trading)→Creditcurrency(Double Accounting)→numbercurrency.The monetary attributes have gone through three levels of iterations of “nature” → “credit endorsement” → “technology”, and behind it is the change from the natural economy to the market economy to the digital age.The birth of stablecoins is also the result of the joint effects of economic development stage and technological progress.

For a long time in the past, the gold standard has been a common currency system in the world, and currency originates more from natural attributes.Early 19th century,Britain was the first to complete the industrial revolution and establish the gold standard. The Gold Standard Act linked the pound to gold, forming an international monetary system with gold as the value benchmark.However, after World War I, European countries’ military expenditures have soared, and the exchange of gold for arms has led to a significant reduction in gold reserves in various countries, and they are unable to maintain the currency exchange for gold under the gold standard.During the Great Depression from 1929 to 1933, countries completely decoupled their currencies from gold, which led to problems such as hyperinflation, government debt arrears, and trade chaos caused by self-depreciation of the exchange rate.This exposed the lack of flexibility and stability of the gold standard system, which brought great difficulties to the reconstruction of European countries after the war and it was difficult to adapt to the development needs of modern economics.To solve these problems, countries on the eve of the end of World War II proposed to establish a “stable” international monetary cooperation mechanism.

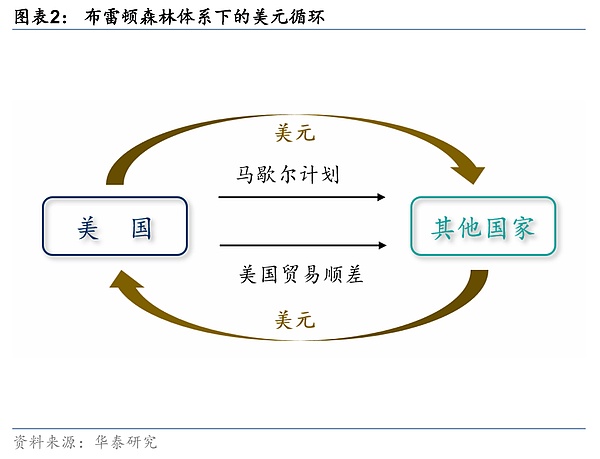

The Bretton Woods system that followed was based on US dollars and cooperated withIMFandBISWith a fixed exchange rate system structure, the currency has begun to be initially given legal attributes, but it still relies heavily on gold.twoAfter the war, the United States’ economic, political, military, international status and other aspects have significantly leaped. The Bretton Woods system pegs the US dollar to gold at a fixed price of $35 per ounce, and the currencies of various countries are pegged to the US dollar.This depends on the dollar cycle with “dollar capital output + US trade surplus” as the core: the United States invests and exports US dollars through the Marshall Plan and the Dodge Plan, and then exports goods to foreign countries based on its industrial base and returns to the US dollar through the trade surplus.The dollar cycle formed in this way ended the chaotic international foreign exchange and foreign trade situation before World War II, and greatly promoted the recovery and development of the post-war economy.

However, with the completion of post-war reconstruction work, the advancement of the European Community construction and the rise of Japan, American industries have gradually been diverted by other countries and transitioned from a trade surplus country to a trade deficit country.The cycle of the US dollar returning to the United States through a trade surplus has been blocked, and offshore currency circulation continues to flood, forcing global holders to return the US dollar to maintain the currency value through exchange for gold, which also causes the US gold reserves to continue to lose (i.e. the “Triffen Problem”).By 1965, the Federal Reserve’s gold reserves had dropped to 60% of the early stages of the Bretton Woods system.As the balance of payments deficit continues to expand, coupled with the arrival of “large stagflation” in the United States, the US economic strength is no longer enough to support the operation of the system. In 1971, US President Nixon announced a suspension of the exchange of US dollars and gold, and the Bretton Woods system collapsed.In 1973, nine European Common Market countries held a meeting in Paris and reached a “floating exchange rate” agreement. At this point, the fixed exchange rate system was also abandoned by major economies.

After the disintegration of the Bretton Woods system, the International Monetary Fund was1972In 2019, a special committee was established to study the reform of the international monetary system and conducted many discussions, and finally1976The conclusion of the “Jamaica Agreement” in 2019 marked the birth of the second generation of the Bretton Woods system.The Jamaican system has two main reforms: one is to confirm the legalization of the floating exchange rate, and member states can decide the exchange rate system on their own; the other is to abolish the official price of gold, and the currencies of various countries are basically decoupled from the gold price.The Jamaican system has established a US dollar system based on the credit of the United States itself. The monetary basis of the international monetary system has officially transitioned from the physical standard to the sovereign credit standard, and the currency has formal legal significance.The United States successfully promoted crude oil trading in US dollars, further strengthening the hegemony of the US dollar.

Although the Jamaican system has largely solved the institutional defects of the previous gold standard and fixed exchange rate, it has also exposed some disadvantages.For example, under the floating exchange rate system, exchange rate overshoot is prone to occur, and exchange rate fluctuations are likely to cause a balance of payments crisis.Moreover, the “Triffen problem” still exists under the credit monetary system: the United States exports the US dollar through trade deficit and purchasing goods from abroad, and then returns the US dollar by issuing treasury bonds to absorb overseas investment, while foreign liabilities continue to accumulate and shake the long-term credit of the US dollar.Especially under the impact of events such as the subprime mortgage crisis, the drawbacks of the US dollar standard system have been further amplified.

The IMF has also launched the Special Drawing Rights (SDR), creating a complementary international reserve asset to make up for the shortcomings of the US dollar system.However, in practice, there are still many disadvantages such as distribution mechanisms, and their actual effects are very limited.

The market is also spontaneously brewing more flexible, decentralized, technology-driven alternative mechanisms in order to get rid of excessive dependence on single country credit.In this context, Bitcoin (BTC) and Ethereum (ETHcrypto assets represented by ) emerge one after another, and currencies are beginning to be assigned technical attributes.Bitcoin, born in 2009, is the world’s first decentralized digital currency, marks the beginning of cryptocurrency to enter the historical stage.Crypto assets are based on the underlying mechanism of decentralization (no central issuer, and the issuance of new currency depends on network consensus algorithms), openness and transparency (transaction information is recorded on globally publicly distributed ledgers, no trusted intermediaries such as banks), and cannot be tampered with (the records cannot be unilaterally modified after transactions are put on the chain), which is in sharp contrast with the traditional monetary system led by the central bank and relies on intermediaries such as banks, and try a new path.

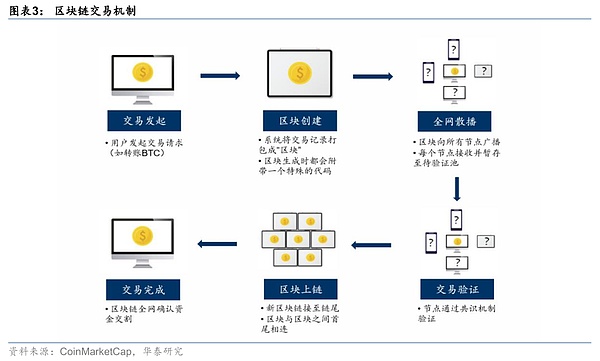

The core driving technologies behind this are blockchain and distributed ledgers.Blockchain can be understood as an online ledger shared by everyone,Every time a transaction occurs, the system will package the transaction record into “blocks”.Each block will be generated with a special code, similar to a human fingerprint. This “fingerprint” is calculated based on the transaction information in the block. It is very unique. As long as the content changes, the fingerprint will also change.The block is connected to the end (each block is attached with a fingerprint of a block for each block generated). Tampering with any historical record will invalidate the fingerprints of all subsequent blocks, so the content of the ledger is almost impossible to tamper with.

The so-called distributed ledger is that the above-mentioned shared ledger distribution is stored in each person’s computer, and each computer has a complete copy. Once a new transaction occurs, these computers will check whether the transaction is true or not. Only after confirming that there is no problem will the transaction be officially written into the ledger, which is the so-called “consensus algorithm”.Anyone can participate in accounting and can view all transactions on the chain at any time.In contrast, the previous accounting methods (single/multi-entry accounting methods) were all recorded their own accounts and belonged to private account books.Thanks to thisPublic, distributed andNoTampered“dataLibrary”, cryptocurrencytalentCan be issued without intermediaryand transactions,thisalsoyesencryptionThe fundamental difference between assets and traditional currencies.

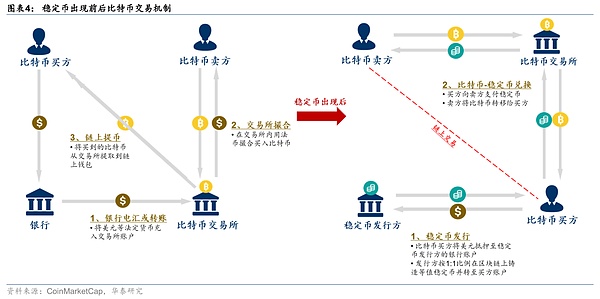

But a key issue is that transactions of cryptocurrencies such as Bitcoin involve two systems on-chain and off-chain systems, which are complex processes, inefficient and costly.In the early purchase of Bitcoin, you generally have to go through the three steps of “fiat currency → exchange → withdrawal of coins”:

1) Users need to recharge legal currency such as US dollars into the exchange account through bank wire transfer or transfer;

2) Use fiat currency to buy Bitcoin on the exchange (the exchange matches the orders, and usually only process fiat currency recharges within working days and working hours);

3) Extract the purchased Bitcoin from the exchange to the on-chain wallet.

During this process, it often takes several days to transfer fiat currency funds within the banking system, and cross-border remittances are slow and expensive.The crypto market is operating continuously for 7×24 hours a day. During the delay in these days, the price of Bitcoin may have fluctuated violently, and investors may have missed the opportunity to buy.In addition, fiat currency control and cross-border procedures in different countries also make it very inconvenient to directly use fiat currency to participate in Bitcoin transactions.

Therefore, the market urgently needs a trading medium that has both stable value and can be circulated quickly on the chain, with both “credit endorsement”+Stablecoins with two major attributes of “technology” came into being.Stablecoins were initially primarily crypto digital tokens anchored by fiat currencies (USD) to act as a measure of value and a median of payment/circulation in the crypto world.Its introduction greatly simplifies the path of crypto asset trading. Previously, fiat currency entered and exited and needed to bypass the bank. Now, only fiat currency exchanges for stablecoins are needed, and subsequent capital flows and transactions can be completed on the chain.When transferring funds between different trading platforms, it can also be completed in real time by transferring stablecoins on-chain without having to transfer via bank wires.In short, stablecoins have successfully connected the traditional finance and crypto worlds with their two major advantages of “stability” and “on-chain”.

Stablecoin operation mechanism

What is a stablecoin (Stablecoin)?In short, stablecoins are crypto assets that establish an anchor relationship with certain types of assets and thus maintain relatively stable currency value.Stable coins are usually issued by private institutions based on consideration assets, circulated on the blockchain network, and promise to anchor the currency value to a certain fiat currency or commodity unit.Therefore, it combines the “on-chain” advantages of cryptocurrencies and the stability/security characteristics of traditional assets such as fiat currencies.The emergence of stablecoins provides a stable value scale and trading medium for the digital asset market, and is vividly called the “bridge” connecting the fiat currency world and the crypto world.

Specifically, we understand stablecoins from the following aspects.

First of all, the reason why stablecoins can be “stable” is not only due to their “1:1The anchoring principle of “is also relies on its “affiliated” mechanisms such as reserve custody, redemption and destruction, secondary arbitrage, incentive guidance (the stablecoin types involved will be expanded later):

First,”1:1”Anchoring principle.Compared with “non-anchored” crypto assets such as Bitcoin, stablecoins are supported by specific assets when issuing, that is, for each stablecoin is issued, the issuer will add equivalent assets (such as US dollar, Hong Kong dollars, etc.) to the reserves.Given this binding relationship, the price fluctuation range of stablecoins is significantly smaller than that of other crypto assets such as Bitcoin, and a fixed exchange ratio of “1:1” to the anchor is maintained most of the time.

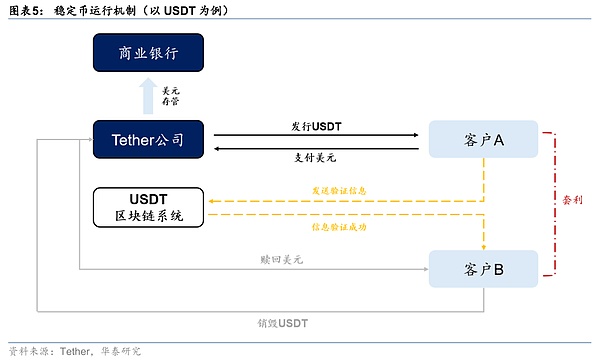

Second, reserve asset custody mechanism.For stablecoins anchored by fiat or commodities, the issuer usually promises to hold sufficient reserve assets for redemption and deposit them in an independent custodian or regulated bank account (for example, USDC’s US dollar reserves are escrowed by several US-qualified banks and asset management institutions) to ensure that the reserve assets are not misappropriated and thus guarantee the redemption commitment.Regular proof of reserves or audit reports are also a key link, that is, major stablecoin issuers publish monthly reserve compositions and are verified by independent audit/accounting agencies to enhance transparency.

Third, the redemption and destruction mechanism.Stablecoin issuers usually promise that holders can directly exchange the stablecoin back to the corresponding fiat currency, physical assets or other collateral according to the anchor price.When the user applies for redemption from the issuer, the corresponding amount of stablecoins will be destroyed, and the reserve assets of the same value will be paid to the user.This mechanism ensures that stablecoin supply and reserves change simultaneously and prevents over-issuance.

Fourth, the arbitrage mechanism.Based on the above issuance and redemption mechanism, when the trading price of the stablecoin in the market deviates from the anchor value, traders will drive the price to “return” through arbitrage activities between the primary and secondary markets.For example, when the price of a stablecoin in the market is higher than the anchor price, the arbitrageur will subscribe to the issuer for 1:1 price and sell it, thereby increasing supply and lowering the market price; when the market price of a stablecoin falls below the anchor price, the arbitrageur will buy cheap coins and redeem them 1:1 to reduce the supply and push up the price.

Fifth, incentive and guidance mechanism.Some stablecoin systems will also introduce incentive mechanisms to guide supply and demand balance.For example, MakerDAO can better stabilize the price of the coin by adjusting the stable fee rate (borrow rate) of DAI (a type of stablecoin).If DAI continues to be below $1, interest rates can be raised to increase the cost of borrowing DAI and prompt supply to shrink; otherwise, interest rates will be lowered to encourage supply.Similarly, in algorithmic stablecoins, designers often set incentives to encourage market entities to perform operations that are conducive to restoring anchors.These endogenous incentive mechanisms are an important supplementary means for stablecoins to maintain stability.

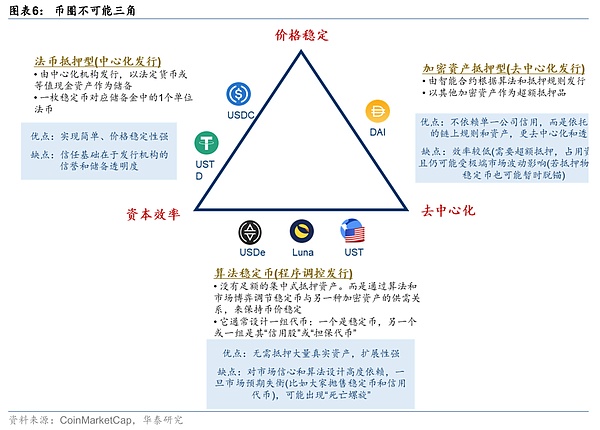

Secondly, stablecoins have multiple types according to anchor assets or collateral.

First, fiat currency reserve stablecoin.This type of stablecoins is issued by centralized institutions, with fiat currency cash or equivalent assets as reserves. A stablecoin corresponds to one unit of fiat currency in the reserve.This type of stablecoins currently has the largest market size (typical USDT, USDC, FDUSD and other US dollar stablecoins), with simple implementation and strong price stability.However, the basis of trust lies in the credibility and transparency of the issuer, and is subject to the supervision and restrictions of the monetary authorities of various countries.

The second is a crypto asset-collateralized stablecoin.That is, stablecoins issued with collateral with other cryptocurrencies, typical of which are DAI issued by the MakerDAO protocol.Compared with fiat currency reserve stablecoins, this model controls the fluctuations of underlying assets through over-collateralization and automatic liquidation mechanisms: 1) Users need to deposit ETH, USDC and other crypto assets at a certain excess ratio (such as 150%) to lend the corresponding amount of stablecoins; 2) When the value of the collateral falls to the cordon, the smart contract will force the position to close the position and auction the collateral.

The advantage of this type of stablecoins is that they are decentralized and do not rely on the credit of a single company. The issuance and management are executed through on-chain code, which has strong censorship resistance and meets the needs of the DeFi ecosystem.The main drawbacks are low efficiency (high mortgage rate occupies funds), and excessive reliance on single crypto assets may cause chain risks. For example, DAI, which had a single mortgage ETH in the early stage, was deaned due to the plunge of Ethereum.At present, DAI has adopted a diversified asset mortgage strategy, such as introducing USDC, WBTC, etc. to improve stability.

The third is algorithmic stablecoins.This type of stablecoins does not rely on external asset collateral and mainly uses on-chain algorithms to regulate token supply and demand to maintain anchoring.It usually designs a set of tokens: one is a stablecoin and the other/group is its “secured tokens”.Typically, a dual currency model of TerraUSD (UST) and its associated token LUNA, the algorithm dynamically adjusts the supply of UST and LUNA based on the UST price deviation against the USD.This type of mechanism has been highly expected (completely decentralized and does not rely on collateral), but it is also the most challenging in practice, mainly because of its high dependence on market confidence and algorithm design and high market vulnerability.Since the UST incident in 2022, regulators and the market have gradually taken a cautious attitude towards algorithmic stablecoins. The scale of mainstream algorithmic currency projects has dropped sharply, and only some experimental projects remain (such as Frax, a mixed algorithm + mortgage, etc.).

Fourth, commodity stablecoins.That is, stablecoins issued with physical commodities (usually precious metals or commodities) as reserve assets.Commodity-type stablecoins are smaller (only less than 1% of fiat-types in 2024), and the most common are stablecoins anchored by gold, such as PAX Gold (PAXG) and Tether Gold (XAUT).The risks of this type of stablecoin are mainly fluctuations in commodity prices, commodity storage and verification costs, insufficient liquidity, etc.And since commodity stablecoins involve physical delivery and traditional commodity market supervision, issuance and custody usually need to meet corresponding industry norms.

It is also worth mentioning that there are some common misunderstandings about stablecoins in the market, such as:

1.Is the bank’s voucher a stablecoin?Easy to understand, but not!Bank vouchers usually refer to electronic/paper discount vouchers issued by banks with a certain denomination, which can be used to deduct shopping and consumption payments. In form, it is also a value voucher.But it is not a stablecoin: 1) It is not circulated on the blockchain, there is no on-chain account book; 2) There is no anchor reserve assets, nor is there a fiat currency convertible, but it exists as a merchant’s voucher; 3) The scope of use is limited, and it can usually only be used in designated merchants or activities, and it does not have cross-border liquidity.Prepaid cards, membership points, etc. similar to this are also similar logic.

2.Is Hong Kong dollar a stablecoin?Neither!The Hong Kong dollar is pegged to the US dollar under the linked exchange rate system, and the currency value is relatively stable, which is similar to the anchoring principle of stablecoins.But it is not in the category of stablecoins: 1) The Hong Kong dollar is issued uniformly by banks authorized by the Hong Kong Monetary Authority of China. It is a sovereign legal currency, not a private institution issuance based on blockchain; 2) The Hong Kong dollar exists in the form of paper money or bank deposits, and even if it is in the form of electronic payment, it does not rely on blockchain technology; 3) It does not have a redeemable mechanism, and the Hong Kong dollar itself is a legal currency and does not need further exchange.

3.Tencent’sQQWhere is the currency?Also not!QQ Coin is an internal virtual currency issued by Tencent for its social and gaming products. Users can purchase QQ Coin in RMB and consume it in Tencent’s ecosystem. It seems to correspond to the RMB “1:1” and circulate in the “virtual world”.But it is essentially different from stablecoins: 1) QQ coins are uniformly issued by Tencent and recorded on private servers and are not circulated on public blockchains; 2) QQ coins can only be used in games and services specified by Tencent and cannot be exchanged back to RMB at the original price; 3) QQ coins can only be circulated within the Tencent platform and do not have the attributes of cross-platform or cross-border circulation.

In addition, although the central bank’s digital currency also has the characteristics of “digitalization”, it is not equal to a stablecoin. We will further compare and analyze it later.

Application scenarios and features of stablecoins

Stablecoins have dual characteristics:On the one hand,The issuance mechanism of stablecoins anchoring fiat currency ensures the stability of its value and is the basis for its value measurement and transaction swap function;On the other hand,, Stable Coins have the relevant advantages of blockchain decentralized accounting, including low transaction costs, transparency, traceability, global liquidity and privacy.

From the perspective of application scenarios,The function of stablecoins has gradually expanded from the initial cryptocurrency transaction settlement to cross-border payments, store of value and other fields.Especially decentralized finance (DeFi) Ecology is the most currentToolPotentialDevelopment direction.Specifically, stablecoins mainly have the following application scenarios:

1)Crypto Asset Trading.As the “trading medium” and “counter unit” of the cryptocurrency market, stablecoins undertake more than 80% of the transaction settlement functions of crypto assets, and are currently mainly based on exchanges (see the analysis below for details).

2) Cross-border payment and settlement.With the help of blockchain technology, stablecoins can realize point-to-point real-time transfer, which significantly improves both cost and efficiency.In terms of transaction costs, Binance research shows that the minimum completion of a small amount of $200 blockchain remittance is $0.00025, and the cost of point-to-point stablecoin transfer is lower. The average cost rate of traditional cross-border remittances is relatively high, and there is a limit on the minimum fee. Overall, blockchain transactions are only 1/10 to 1/100 of the traditional banking system; in terms of transaction efficiency, the settlement time of blockchain has been shortened from 3-5 days to seconds. According to research by the China Financial Association, cross-border remittances of existing banks usually take five days to settle, but 100% of transactions based on cross-border payments based on blockchain will be completed in less than an hour.

3) Store of value.In high inflation countries (such as Turkey, Argentina, and some African countries), stablecoins with US dollar or gold as reserve assets have become an important hedge tool for the public and enterprises, and their currency stability makes them have the property of a store of value similar to fiat currency.

4) Decentralized Finance (DeFi).DeFiIt is a financial ecosystem built on stablecoins as the core and based on blockchain, and diversified business scenarios are achieved through replicating traditional financial logic..Specifically including the following contents,

① Financing business.First, real asset tokenization (RWA) allows ownership of real assets such as real estate, intangible assets, accounts receivable and treasury bonds to be traded on the blockchain, and stablecoins provide a basis for value measurement and liquidity; in addition, companies package the future cash flow of their business or project and realize “currency circle IPO” financing by issuing their own tokens, which is also part of RWA.Second, all types of lending, derivatives and re-pled businesses are inseparable from stablecoins. They can pledge other assets to borrow stablecoins, or pledge stablecoins to borrow other cryptocurrencies. In the lending agreement business in 2025, stablecoins account for a large proportion of DeFi locked positions.

②Invest in business.First, users can directly invest in cryptocurrency, which is divided into two categories. One is virtual speculative projects based on algorithmic rules (similar to “luxury investment”), and their value depends on market recognition; the other is tokens anchoring physical assets and returns (similar to entities, stocks, and bond investments).Second, the liquidity mining and pledge mechanism allows users to provide assets (join the liquidity pool) to the exchange platform and obtain income sharing through pledge mining (similar to the “current interest” paid to users by the exchange); third, users can participate in “money circle financial management products”, such as income-based stablecoins will generate returns by participating in DeFi activities or RWA investments. If investors purchase such stablecoins, they are equivalent to participating in “money circle financial management”.

③Derivatives and risk management business.The blockchain ecosystem has derived tools such as leveraged trading (such as SushiSwap), decentralized insurance (such as Nexus Mutual), and such derivatives and insurance businesses provide the market with traditional financial risk hedging methods.

④ Blockchain specialty business.For example, multinational enterprises can use stablecoins to build a customized supply chain financial system to achieve real-time flow of upstream and downstream funds, and effectively improve the operational efficiency of the cross-border industrial chain.

As of now, in addition to the most common crypto asset trading, stablecoins have been implemented in other fields:

1) in terms of cross-border payment and settlement,It is currently the most widely used field except for crypto asset trading.Typical examples are stablecoin co-branded cards launched by JD.com and Visa, which have tested retail payment scenarios in the Middle East.When consumers shop overseas to swipe JD Stablecoin (JK-HKD), the settlement cost will be significantly reduced from 6% of SWIFT to 0.1%, and the timeliness is compressed from 3 days (at least) to several seconds.In addition, Gcash, the Philippines’ largest digital wallet, has integrated the USDC stablecoin owned by Circle, allowing millions of users to exchange pesos for USDC in the Gcash app, facilitating the transfer of money from Filipino overseas workers to their hometowns.

2) in terms of value storage,Inflation in Argentina has continued to reach three digits in the past two years (the CPI exceeded 100% year-on-year in 2023 and further exceeded 200% in 2024). DAI has become a tool for the people of the country to fight the depreciation of their local currency (the direct purchase of the US dollar is restricted by the banking system).According to local exchange data, DAI transaction volume increased by 300% in 2024, mainly used for cross-border procurement and salary storage.The same is true for countries such as Türkiye and Nigeria.According to Chainalysis statistics, the year-on-year growth rate of stablecoin transactions in Latin America and sub-Saharan Africa in 2023-2024, far higher than the global average.In addition, the transaction volume of underlying stablecoins in countries such as Russia and Iran that are affected by geopolitics has also increased exponentially.

3) Financing business/RWAaspect,Typical examples include GCL Energy Technology and Ant Digital Technology, which has cooperated to complete the first and largest (over 2 trillion) photovoltaic green asset RWA project in China last year, announced the establishment of a new company “Ant Xinneng” in June this year, planning to tokenize existing photovoltaic assets and denominate in stablecoins.For example, RealT is the first benchmark project for real estate tokenization in the United States, focusing on the acquisition and renovation of low-priced old houses in Detroit and other places. It will then be rented out and put on the chain to tokenize and split the property rights, allowing investors to purchase token shares at a minimum price of $50 and settle rental income through USDC.In terms of intangible assets, IPwe has also digitized and tokenized 25 million patents to facilitate valuation, transactions and financing.

4) In terms of investment business,Currently, USDC’s 30-day borrowing yield is between 4% and 9%, which is generally higher than the yield on the near term (such as 3 months).

5) Other aspects,For example, the centralized insurance platform Nexus Mutual supports users to purchase insurance policies with stablecoins, providing an on-chain compensation mechanism for smart contract attacks, vulnerabilities, etc.In addition, the JD Coin Chain Technology stablecoin project has recently entered the second phase of the “stable coin issuer sandbox” of the Hong Kong Monetary Authority of China. Suppliers can obtain real-time financing with blockchain warehouse receipts, and the interest rates are lower than those of traditional banks.

Looking forward, the convenient payment of stablecoins andRWARepresented byDefiFinance is the application scenario with the greatest potential for future development.

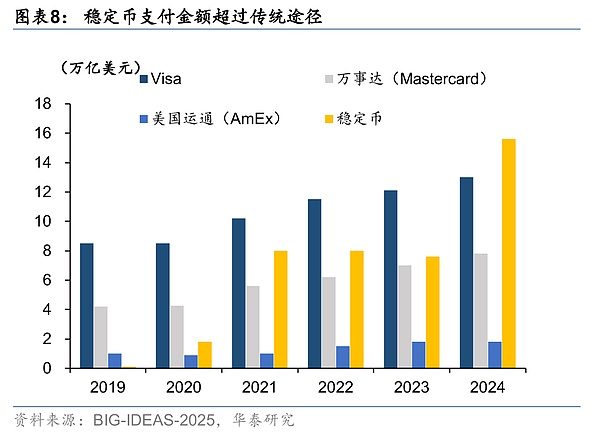

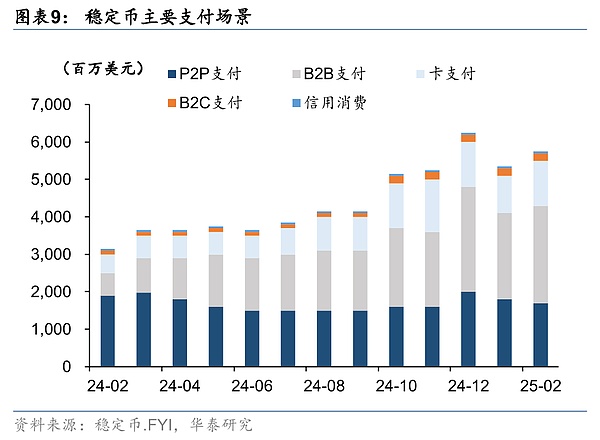

On the one hand,, stablecoins have significant advantages in convenient payments, and their current transaction volume has exceeded traditional payment systems such as VISA and Mastercard. The transaction volume in 2024 is US$15.6 trillion, significantly higher than Visa (US$13 trillion) and Mastercard (US$8 trillion).However, the number of transactions of stablecoins accounts for only 0.41% and 0.72% of the transaction volume of Visa and Mastercard, indicating that a single transaction is more valuable, and the scale of B2B payment is proof of the current widest use scenario.But it is worth noting that according to Visa data, more than 70% of stablecoin transactions are used for automated transactions of cryptocurrencies in most times, and real payment transactions still have a lot of room for improvement in the future.

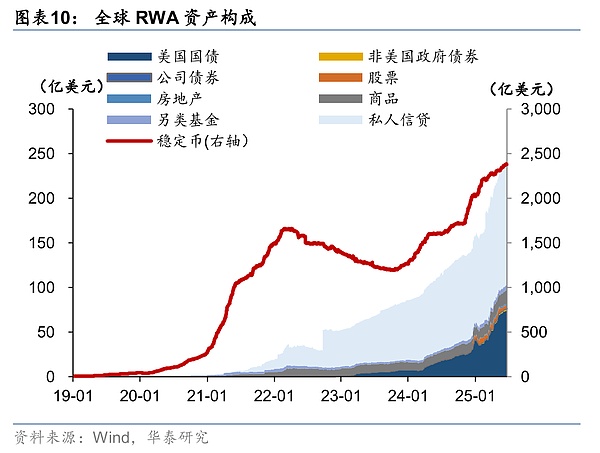

On the other hand,, RWA digital assets have entered a booming stage.RWA technology originated earlier, but with the development of the Defi concept, RWA began to be circulated on the blockchain.From a conceptual perspective, the US dollar is behind the asset endorsement, which is essentially in line with the definition of RWA assets, accounting for 90% of RWA assets.After excluding stablecoins, RWA is involved in personal credit, treasury bonds, stocks, real estate, alternative funds and other fields, and the first two categories occupy the vast majority of the scale.The combination of stablecoins and RWA promotes the transformation of finance from virtual hype to physical empowerment.According to Chainlink data, the global market size of real-world assets is US$867 trillion, and currently only 0.0013% of the value is on the chain, and RWA is large.Boston Consulting predicts that the RWA market size will soar to US$16 trillion in 2030, and 30%-50% of the stablecoin shares will flow into RWA assets.

At the same time, stablecoin trading also has obvious risk points, specifically from two aspects.

On the one hand,Risks related to its issuer include internal management risks of the issuer (governance defects, operational loopholes, etc.), reserve assets risks (insufficient reserves, fluctuations in asset value, etc.) and compliance supervision risks (policy differences, anti-money laundering, regulatory fraud, etc.);

On the other hand,Risks related to blockchain’s own technology include algorithm mechanism risks (issuance model failure, etc.), network security risks (51% attacks, smart contract vulnerabilities, etc.), performance bottleneck risks (blockchain throughput restrictions, cross-chain interaction delays, etc.).

In addition, the existence forms of stablecoins and various existing currencies in the market are essentially different. The specific comparison and analysis are as follows:

1) Comparison with traditional fiat currency: Fiat currency guarantees its payment function and value stability through sovereign credit endorsement and power. It has hard liquidity capabilities in China, but has low cross-border efficiency; while stablecoins are technology-driven “digital cash”, which are generally issued by third parties, rely on reserve assets and algorithms to maintain price stability, lacking the compulsory liquidity and sovereign credit endorsement of fiat currency, but they have advantages in cross-border circulation;

2) Comparison with central bank digital currency (CBDC): Both are digital currency forms, among which CBDC is a digital extension of the state’s sovereign currency and a digital form of “paper currency” (normally no interest is paid).CBDC is still attached to the account, with controllability and legal compensation. Compared with mature mobile payment methods, it has more advantages in scenarios such as network-free (offline payment). Cross-border recognition depends on the process of RMB internationalization.China and the EU have successively launched CBDCs. Among them, the central bank comprehensively promotes digital RMB application scenarios in six cities including Suzhou and Shenzhen as a supplement to paper currency and applies them in various scenarios such as shopping, wages, and subsidies.Due to the development of Internet payment in China, currency digitalization has become the mainstream, and the launch of digital currency will fill the gap.The EU regards CBDC as an important measure to enhance strategic autonomy and reduce dependence on the US payment system.

The biggest difference between stablecoins is that most digital currencies that may be established by third parties. The stability of value depends on the issuer’s credibility, reserve assets, etc., which has certain compliance risks, cross-border advantages, and the scale of use is still in the early stage of development.It is worth noting that digital RMB can also adopt blockchain technology. The difference is that its participation nodes are authorized and only specific members (such as central banks and state-owned banks) are allowed to participate in data recording and verification, that is, they adopt the form of a alliance chain.

3)Comparison with bank deposits:Bank deposits can benefit, and current deposits can have partial payment functions, but due to restrictions on bank business hours, fixed deposit returns are high, but liquidity is poor, and the credibility is related to the bank itself; stablecoins cannot generate returns in blockchain wallets, but in centralized exchanges and other institutions, the platform will operate funds through lending, market maker transactions, fund pool operations and liquidity mining, etc., and distribute the returns to users, forming a income model similar to “current deposits”.The yield of stablecoins in trading platforms is generally high and is liquid in the exchange. The scale and scenarios of use are currently far less than bank deposits.

4) Comparison with Internet payment.Internet payment tools (such as WeChat, Alipay, etc.) anchor the value of fiat currency and are closer to stablecoins in nature, but most institutions are third parties.The usage scenarios are relatively limited, but the convenience and penetration rate are high.Internet payments, as a payment medium for third-party companies, face strict supervision and need to operate under network conditions.

5) Comparison with traditional cross-border payments:Traditional cross-border payment media (such as Visa cards, SWIFT systems, etc.) have high recognition and their value can remain relatively stable with the help of banks and financial institutions around the world, but factors such as efficiency, cost and geographic influence on them is obvious.With the help of blockchain technology, stablecoins have low global circulation and cost, but their scale share is still in the early stages of development.

6) Comparison with the rest of cryptocurrencies: Stable coins have become the basis for measuring value in the crypto market because they anchor fiat currencies such as the US dollar, and have the characteristics of stable value and strong liquidity; other cryptocurrencies are either based on algorithmic consensus (such as BTC), or anchored to real assets and cash flow (such as platform coins), and their investment attributes and value storage attributes are more prominent, but high volatility limits the application of their payment and circulation functions.

The development history and market structure of stablecoins

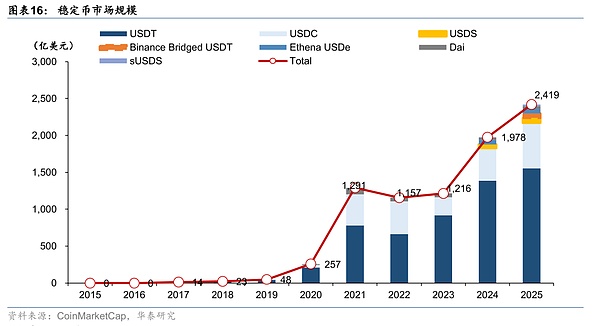

From the perspective of development history,2014The first dollar stablecoin in the yearUSDTThe launch unveils the curtain on a new cryptocurrency that maintains price stability by anchoring fiat assets.In the following decade, the stablecoin market has experienced several ups and downs, and has experienced an evolutionary trend from budding exploration to rapid development, and then to thunder and then adjustment.Enter2023In 2018, as the regulatory frameworks of various countries gradually became clear, stablecoins returned to the track of rapid development, and market recognition and compliance were significantly improved.

Germination period (2014-2017Year)

In 2014, the first batch of stablecoins represented by USDT launched by Tether were born.USDT was anchored to the 1:1 US dollar issuance, which mainly served Bitcoin transactions at the time.Because of its stable value, it has lower transaction costs, high efficiency and no exchange lag compared to traditional fiat currency, it has become a “value bridge” in the crypto market.During the same period, there were also attempts to mortgage crypto assets, such as BitUSD launched by BitShares and NuBits anchored by Bitcoin. However, due to the large fluctuations in the collateral assets themselves, these early products frequently lost their anchors and failed to maintain stability for a long time.

In the three years from 2014 to 2017, the stablecoin market size was relatively small, with USDT’s market value roughly only one million US dollars, and it was mainly tried in the digital asset circle. It mainly adopts a simple reserve support model in technology, and has been initially recognized in a few scenarios such as exchanges.It is worth mentioning that2017The bull market in the crypto market in the year and the ban on token issuance in China and other regions have objectively promoted theUSDTWhen the demand for stablecoins surges,2017End of the yearUSDTThe circulation scale is close14billion US dollars, laying the foundation for subsequent development.

Rapid development period (2018-2020Year)

2018Year to2020During the years, stablecoins ushered in rapid development, driven by several main forces:

First, new compliant stablecoins are launched one after another, the most typical one is2018Year10YueyouCircleandCoinbaseCooperation launchedUSD Coin(USDC), with transparent reserves and “full compliance” as the selling points, quickly becomingUSDTA comparable dollar stablecoin.In addition, fiat currency reserve stablecoins such as TrueUSD and Paxos Standard also poured into the market during this period, and the stablecoin ecosystem was further enriched.

Second,2019YearFacebookAnnouncedLibra(Later renamedDiem) The global stablecoin plan has aroused high attention and discussion among global regulators.G7 and G20 have conducted research and set regulatory principles on the potential impact of the “Global Stablecoin”. Although Libra was ultimately unable to go online, it also marks that the stablecoin has officially entered the mainstream vision.

Third, with decentralized finance (DeFi) has emerged, and stablecoins have become a critical infrastructure.The “Summer of DeFi” in 2020 witnessed the explosive growth of lending agreement Aave and decentralized exchange Uniswap, and the demand for stablecoins as pricing and trading media has increased significantly.Investors bought a large number of stablecoins to participate in “mining”, which drove the stock of stablecoins to soar.By the end of 2020, USDT’s market value exceeded US$20 billion, and USDC also exceeded US$4 billion.

Fourth, the regulatory authorities maintain a vigilant and wait-and-see attitude towards the rapid development of stablecoins.The U.S. Commodity Futures Trading Commission (CFTC) fined Tether in 2021, accusing its early reserve disclosure of falsehoods; the Financial Stability Council (FSB) issued regulatory recommendations for stablecoins in 2020, requiring “one currency, one anchor”, full disclosure and risk control.But overall, the regulatory rules have not been fully implemented at this stage, and the market mainly expands in wild growth.

Risk exposure and adjustment period (2021-2022Year)

2022Year5Month, the third largest stablecoinTerraUSD(UST) in a few days from1The dollar fell to almost zero, announcing the failure of the algorithmic anchoring model.USTThunderstorm triggered a chain reaction, that monthUSDTMarket value plummeted20%(From the appointment830$100 million fell to650More than $100 million),USDCMarket value also550$100 million fell to the end of the year450$100 million.

USTAfter the incident, the United States and the European Union accelerated the promotion of the Stable Coin Transparency and Reserve Guarantee Act respectively (StablecoinTRUST Act), “Regulations on the Supervision of Crypto Asset Market (MiCA)》 and other regulatory frameworks.The US Presidential Financial Markets Working Group also recommended legislation at the end of 2021 to require stablecoin issuers to have bank qualifications to prevent bank runs.Europe completed the MiCA draft legislation in 2022, clarifying that stablecoins are issued with equal reserves to meet liquidity and transparency requirements.Regulators in Hong Kong, Singapore and other places in China have also issued guidelines, planning to implement a licensing system for stablecoin issuance and reserve custody.

The industry has also begun to adjust its self-discipline, and major stablecoin issuers have optimized information disclosure and risk control measures.Typically, Tether began to reduce commercial paper holdings in the second half of 2022 and instead held U.S. Treasury bonds to improve liquidity.Circle continues to release USDC reserve reports audited by independent accountants every month to improve transparency.In the field of decentralized stablecoins, MakerDAO introduces more collateral (including USD₮/USDC, etc.) to its DAI stablecoins and increases the excess collateral rate.After this round of risk clearance, the growth rate of the stablecoin market has slowed down phased.

Regulatory promotion period (2023Year to present)

2023Since the beginning of the year, global regulatory frameworks such as Europe, the United States, the United Kingdom, and Asia (Hong Kong, Japan, Singapore) have been intensively implemented, and stablecoins have entered a new stage of accelerated development of compliance, and the stablecoin ecosystem has ushered in prosperity again.American online payment giant PayPal issued the US dollar stablecoin PYUSD in August 2023; the first batch of compliant stablecoins in Hong Kong, China, such as FDUSD issued by First Digital, was launched in 2023. With strict reserve custody and promotion of the Binance Exchange, its market value has jumped to US$3 billion within one year, ranking among the top four in the world.At the same time, the original stablecoin pattern in the currency circle has been adjusted. Paxos stopped issuing Binance USD (BUSD) in February 2023, and its market share is filled by USDT, FDUSD, etc.

2024In 2018, the total market value of global stablecoins has recovered to close2000$100 million, and it is showing a growth trend again.Up to2025Year6moon16On the day, the total market value of global stablecoins exceeded2400$100 million,2017Annual growth exceeds170Times, accounting for about the total market value of cryptocurrencies in the world7%.Among them, Tether’s USDT is “dominate” and accounts for about 64% of the stablecoin market share; Circle’s USDC is second, with a share of about 25%.The two together account for 90% of the stablecoin market, minting the dominance of the US dollar stablecoin in the global market.

Sorting the entire business chain of stablecoin

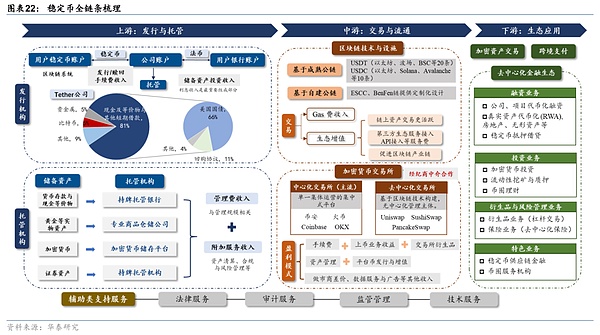

From the perspective of the entire stablecoin chain, the stablecoin business includes many core links such as issuance and custody, transaction circulation, technical facilities, application ecology and compliance assistance. We divide it into upstream, middle and downstream according to its industrial logic. The following is a detailed review of the entire chain:

1, in terms of upstream, it is mainly the issuance and custody institutions of stablecoins.Among them, the issuer’s credibility, issuance design and potential yield of reserve assets are the core of determining the value of stablecoins.

1) The issuer of stablecoins

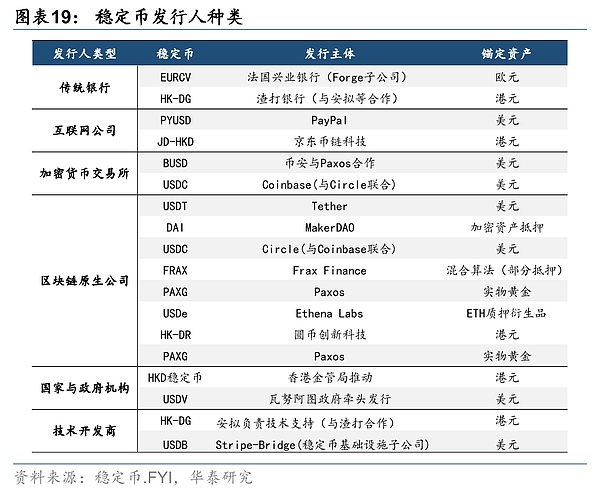

The issuer of stablecoins is responsible for the minting, redemption and institutional design of stablecoins, which is the first link to benefit the development of stablecoins.According to the above, the issuance model of market stablecoins is roughly divided into three categories, but only the USDT and USDC are centralized, with high recognition, accounting for more than 85% of the global market share, representing the main companies are Tether and Circle.

From the issuer type, the range of issuers of stablecoins is a wide range. Traditional banks (Standard Chartered Bank), Internet companies (Amazon, JD.com), exchanges (Binance, Coinbase), blockchain companies (Tether), national and government agencies (Hong Kong Monetary Authority), technology developers (Announcement), payment companies (Stripe), etc. have all made some arrangements in the stablecoin market.In 2024, the Hong Kong Monetary Authority of China announced three participating institutions for stablecoin issuers, including JD.com Coin Chain Technology, Yuanbi Technology, and Standard Chartered Bank Announcement Group Hong Kong Telecom.The access regulatory policies for stablecoin issuers in major countries and regions such as the EU, the United States, Japan, Singapore, the United Arab Emirates, and Hong Kong, China show that the implementation of licensed access licenses and supervision on stablecoin issuers is a global trend.

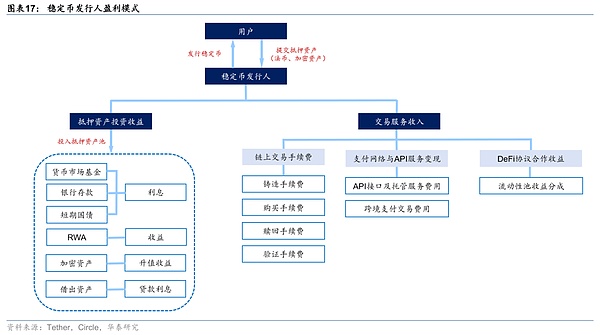

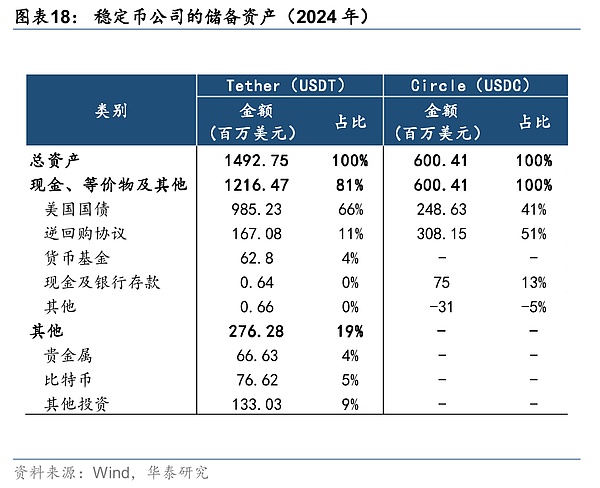

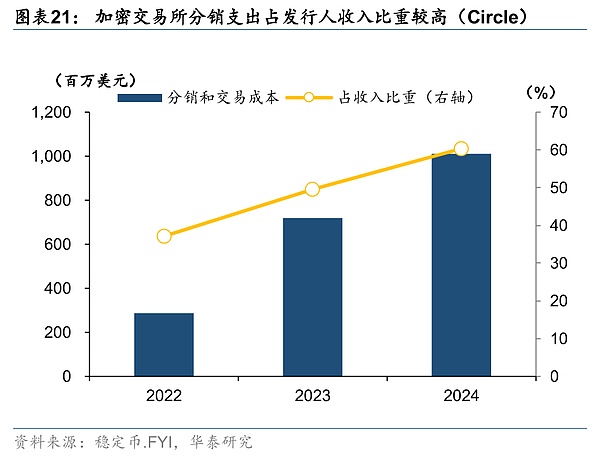

From the perspective of profit model, the profit model of stablecoin issuers is closely related to their issuance mechanism, reserve management and ecological layout.Among them, taking fiat currency collateralized stablecoins as an example, the most core profit point is reserve interest income, accounting for more than 90%. The issuer absorbs funds at zero cost on the liability side, and invests in high-liquid and low-risk assets on the asset side to earn interest spreads.Circle (USDC) will reserve almost all the assets obtained by issuance into cash and equivalents, while Tether (USDT) will also invest in some precious metals, Bitcoin and other assets.Secondly, issuers can also earn stablecoin minting/redemption fees, with Tether fees around 0.1%, while Circle may charge a fixed fee for large redemptions of institutional users.In addition, issuers can also charge the enterprise API (application program interface) service fee, that is, earn income by deploying standardized technology interfaces for the enterprise.It is worth noting that most regulatory authorities in various countries require stablecoin issuing institutions to not pay interest on stablecoins (avoid vicious competition) and cannot directly carry out lending services, so they cannot create multiple credits like banks.

In addition, the core of the issuer’s decision on the value of a stablecoin is that its credibility, issuance design and the potential return expectations of the assets behind it are all key factors that affect the recognition of stablecoin.

2) The custodian of reserve assets

The custodian of stablecoins is mainly responsible for ensuring the security of reserve assets and realizing the isolation and custody of off-chain assets.Taking fiat currency collateralized stablecoins as an example, the most core reserve asset is monetary deposits, which need to be custodialized by the bank. The reserve bank will become an important bridge for the link between currency and fiat currency.In addition, since reserve assets also involve physical assets such as gold, cryptocurrencies, securities assets, etc., it needs to be managed by corresponding commodity warehousing companies, cryptocurrency storage platforms and licensed custodian institutions.

For stablecoins, being able to ensure time-consuming redeem of fiat currency is key, so it is necessary to focus on the issuer’s reserves.The EU, the United States, Singapore and other countries have carried out policy designs on the stability of the value of reserve assets and preventing user runs. They have taken the third-party isolation and custody of reserve funds as the core, and have also put forward detailed requirements on the scope and proportion of investment assets, customer redemption mechanism and time limit, and the priority order of repayment when issuers go bankrupt.

From the perspective of profit modelThe custodian mainly charges management fees based on the total value of the custodian assets, and may earn income by providing corresponding asset liquidation, compliance and risk management services.

2) In the midstream, the main support links related to the circulation of stablecoins, including exchanges, blockchain infrastructure, etc. Traditional securities companies can participate in the circulation link through the broker model.

1) Blockchain technology and facility support

The circulation of stablecoins is highly dependent on the underlying architecture of blockchain, and current mainstream stablecoins (such asUSDT,USDC,DAI) are all based on Ethereum, Tron,SolanaWait for mature public chains to be issued.By utilizing the infrastructure of existing public chains, the recognition of stablecoins can be quickly improved, and the stablecoin is deeply bound to a variety of ecology, which also promotes the development of related mature chains. Currently, USDT covers 20 public chains such as Ethereum, Tron, and BSC; USDC covers 10 public chains such as Ethereum, Solana, and Avalanche.In addition, a few stablecoin projects will choose to build their own public chains in order to establish their own independent ecosystem. The ESCC and BenFen chains reduce transaction costs through customized designs, and help the project party build a complete ecosystem.

From the perspective of profit model, the benefits of the relevant links of the public chain are the most direct.,On the one hand,Any transactions conducted on the public chain (including stablecoin transfer, exchange, pledge, etc.) require gas (native tokens of the public chain). As a high-frequency trading asset, its high transaction volume will make the higher the Gas fee income obtained by public chain nodes (miners/verifiers), and will also increase the liquidity and value appreciation of the native tokens.On the other hand,When a stablecoin is connected to the public chain, it can improve the recognition and liquidity of the public chain, thereby driving the transaction activity of on-chain assets (such as DeFi tokens, NFTs), and attracting third-party ecological services such as exchanges and wallets to access, public chain companies can obtain service fees such as API access.Secondly, the entire blockchain-related industrial chain will be promoted, including basic industries (chips, mining machines, storage, etc.), technical industries (privacy computing, security technology) and characteristic industries (supply chain finance, meta-universe), etc.

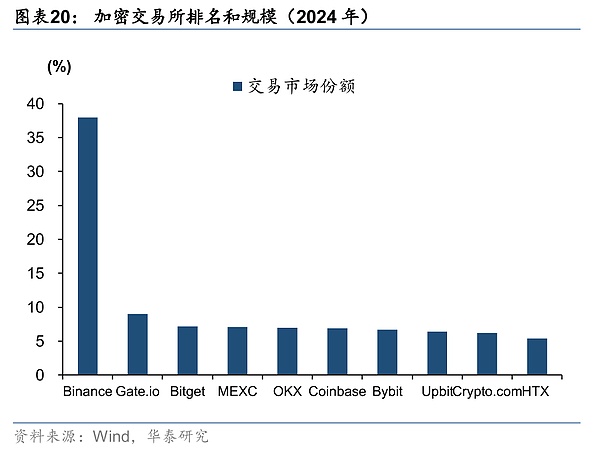

2) Cryptocurrency Exchange

Cryptocurrency Exchange is an online platform for digital currency trading services. Users can trade crypto assets such as Bitcoin, Ethereum and stablecoins through the platform, and realize exchange with traditional fiat currencies (such as US dollar and RMB), providing guarantees for the circulation of stablecoins.CoinMarketCap data shows that as of April 2025, there were about 600 cryptocurrency exchanges around the world, mainly divided into centralized exchanges (CEX) and decentralized exchanges (DEX).The former is a centralized platform operated by a single collective. Users register accounts and entrust assets to the exchange wallet, and transactions are matched and managed by the platform; while the latter is a non-centralized platform built by blockchain technology.

Exchanges such as Binance, Huobi, and Coinbase, which currently have high market recognition, are all centralized exchanges. Internal transactions on the exchange are off-chain transfers. Investors’ assets on the exchange account are only a digital sign. Only when the platform transfers/proposes the outside world, the transactions will be on-chain. Therefore, transactions on the exchange may be weaker than on-chain transactions in terms of security.The exchange switch solves problems such as high difficulty in traditional blockchain trading operations, insufficient liquidity, and low trading efficiency.

From the perspective of profit model, the exchange’s profit model is relatively diversified,One isThe exchange charges a proportional fee for each transaction, which is the core source of income of the platform, usually 0.1%-0.5%;Second,Income from listed currency business, including the launch of various cryptocurrencies on exchanges, technical docking and marketing promotion services;Third,Exchange derivatives business, including perpetual contracts, options, futures, etc.;FourthAsset management business, that is, users deposit currency assets into exchange financial products, and the exchange conducts pledge mining, lending and other businesses, and charges management fees (1%-3%) and performance sharing;FivePlatform coins are issued and added, and platform coins are issued for financing, and investment in high-yield projects or volatility arbitrage;SixthMarket makers’ price difference, data services and advertising and other sources of income;SevenSubscription revenue from various tools and services on the platform.

In addition, regional exchanges will review investor qualifications according to relevant regulatory requirements.In addition to providing basic information such as ID cards, address proofs, facial recognition, etc., centralized exchanges require customers to provide other supplementary information.Hong Kong (such as OSL), Japan (FSA), Singapore and the United States will evaluate users’ net assets, income and risk tolerance, and set corresponding investor thresholds for trading.Decentralized exchanges and accounts of specific currencies generally require only a wallet address to trade, without qualification certification, but lack regulatory protection.

3) Securities companies+Broker cooperation model

Securities companies cooperate with cryptocurrency exchanges through broker cooperation model.Provide virtual asset trading services for investors.Under the cooperation model, traditional securities companies can make full use of their existing qualifications, customer resources and brand advantages, without building their own exchange system, and can enter the market by just upgrading their licenses; while licensed exchanges are responsible for underlying liquidity, clearing and custody, and user traffic may increase under the coordination of the industrial chain.

For exampleThrough cooperation with OSL, Interactive Brokers launched crypto trading services in 2023, and institutional customers can directly access the cryptocurrency market through their platform; Futu Securities began to cooperate with HashKey in 2024, and users can trade crypto assets through the Futu entrance. The transaction began to be limited to BTC/ETH spot trading, and it will gradually be opened to the integration of USDT recharge and comprehensive account; recently, Guotai Junan International has been upgraded to become the first Chinese brokerage firm in Hong Kong, China to provide comprehensive virtual asset services. Its business covers transactions, tokenized securities distribution and over-the-counter derivatives, and the underlying relies on HashKey’s technology and liquidity support.

3, in terms of downstream, application scenarios and ecology such as crypto asset trading, cross-border payments, value storage and decentralized finance are accelerating their development.

The downstream of the stablecoin industry is the core link in value realization, Based on its functions and characteristics, the role of stablecoins has evolved from “help-averse chips within the exchange” to a multi-dimensional financial infrastructure, especially the establishment of a decentralized finance (DeFi) ecosystem is the most promising application direction downstream.For specific application scenarios, please refer to the content of the previous chapter of this article.

Except for the crypto asset trading function that is mainly undertaken by the exchange, the development of other application scenarios of stablecoins has had a significant impact on downstream traditional financial businesses.On the one hand, stablecoins have outstanding advantages in the cross-border payment field, and decentralized payment methods can achieve full-day transactions. At the same time, they avoid the exchange and transfer processes of banks between the two parties. High-recognition blockchain and exchanges can assume this part of the functions, and related cross-border payment companies will also accelerate the layout of blockchain technology; on the other hand, as the value and recognition of stablecoins stabilize, the Defi market will usher in rapid development, which is essentially the derivative of traditional financial services into the currency circle. In the context of the subcontext, relevant technology companies in the relevant blockchain field may give priority to seizing the market and establishing new currency circle financial institutions, such as virtual currency issuance service providers (currency investment banks), virtual currency Yu’ebao (currency circle financial management), etc.

4, In addition, pay attention to the significance of legal, audit, supervision and technical services to the development of the industry.

The stablecoin industry chain also requires many auxiliary support services, including legal services, that is, assisting issuers in meeting regulatory requirements in various places, such as the Hong Kong Stablecoin Ordinance and the US GENIUS Act; audit services, Deloitte, PricewaterhouseCoopers, etc., regularly review reserve assets to improve transparency; regulatory management, the Hong Kong Monetary Authority, the US SEC and other institutions are responsible for the issuance of licenses and standardize the operation of issuers; technical services, access and design of various related technologies, including regulatory technology, payment technology, wallet technology, network technology, etc.

It is worth noting that the characteristics of stablecoins such as decentralization, globalization, anonymity, convertibility (exchanged into fiat currency) and irrevocable transactions may lead to more illegal financial activities.The necessity of relevant anti-money laundering financing supervision has increased. The EU, the United States and other countries have transplanted the anti-money laundering and anti-terrorist financing requirements of payment institutions (money service providers) and banking institutions to the stablecoin/crypto assets field, and complying with the FATF anti-money laundering standards is the core trend in the cryptocurrency field.

The prospects and impacts of stablecoin development

The development momentum of stablecoins and the choice of various countries

Behind the rapid development of stablecoins, global macro demand, national strategies and regulatory systems are inseparable from the joint drive.

1, At the macro demand level, the rise of crypto trading, inefficient traditional cross-border payments, storage value, arbitrage and financial management have jointly created the market prospects of stablecoins.

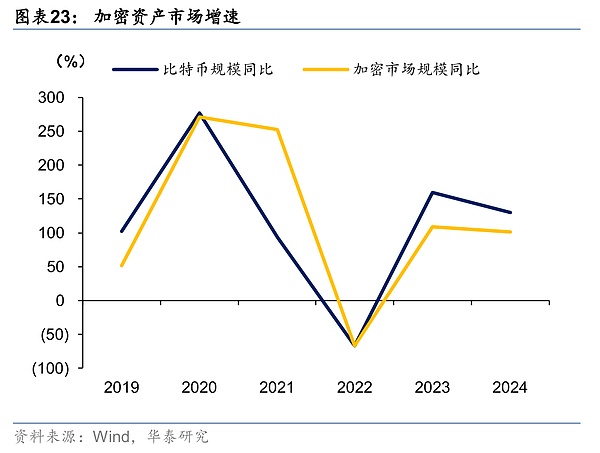

First, the demand for crypto trading ecological services has surged.The global cryptocurrency market size reached US$3.5 trillion in 2024, an expansion of more than 15 times compared with five years ago. Stablecoins are the core medium of crypto trading. A large number of borrowing, trading, and derivative contracts are settled in USDT or USDC, accounting for more than 80% of the total spot trading volume of cryptocurrencies.The accelerated expansion of the crypto market in recent years has driven the growth of stablecoin demand.

Second, the penetration rate of stablecoins in cross-border payments has increased rapidly.Stablecoins have obvious cost and efficiency advantages in cross-border payments. In 2024, the annual transaction volume of stablecoins (US$10.8 trillion) has accounted for about 24% of the total global cross-border payments, and the growth rate far exceeds traditional channels such as Visa and Mastercard.With the expansion of cross-border remittance scale and the increase in penetration of stablecoins, the demand for stablecoins has increased.According to BIS data, the total global cross-border trade and remittances in 2023 is approximately US$45 trillion, and is expected to increase to US$76 trillion in 2030.

Third, driven by hedging and stored value demand.When the traditional financial system faces inflation, currency depreciation or policy risks, stablecoins have become an important hedge tool for emerging market users, and emerging economies such as Turkey, Venezuela, and Nigeria have increased their demand for US dollar stablecoins.In addition, in the context of the reconstruction of global order, geopolitical events occur frequently, and the transaction volume of stablecoins in related countries such as Iran has also increased exponentially.

Fourth, under the global low interest rate environment, investors’ pursuit of high returns has also promoted the development of new interest-generating stablecoins.In addition to the basic cryptocurrency trading needs mentioned above, yield products for stablecoins have gradually appeared in CeFi and DeFi, and the yield rate is relatively high. Typically, Yield-bearing Stablecoins issuance has increased from US$1.5 billion in early 2024 to approximately US$11 billion in mid-2025, accounting for about 4.5% of the stablecoin market.In addition, the convenient cross-border capital flow channels and all-weather trading support of stablecoins also provide space for investors to cross-chain or cross-regional arbitrage transactions.

2, At the national strategic level, the shift in US policy has had a great driving effect on the world. Countries have formulated strategic and regulatory frameworks based on considerations such as monetary sovereignty and financial competitiveness, and have pulled stablecoins from the “gray zone” into the “legal express train”.

1) In the United States, TrumpgovernmentGreat effortspromoteCryptocurrency strategy.Government officials such as Becente have not kept aside the strategic considerations of stablecoins against the United States, which are reflected in the following aspects:One, Stablecoins are the “technical extension” of US dollar hegemony in the digital age, which is inherited from gold dollar, oil dollar to token dollar (digital dollar) (see analysis later);Second, stablecoin reserve assets can purchase U.S. Treasury bonds, providing new channels for fiscal financing;ThirdThe United States hopes to respond to the acceleration of countries with the help of the high penetration rate of stablecoins on the chain.CBDCCompetition brought by R&D;The fourthThe Trump family has made in-depth layout and full efforts in the crypto industry, which is also one of the most critical driving forces for the development of the stablecoin field.

In January this year, Trump signed an executive order to strengthen the U.S. leadership in the field of digital financial technology as soon as he came to power. In March, Trump announced on social media that he would promote the strategic reserve plan for cryptocurrency.The Genius Act, which promotes the innovative development of stablecoins, was voted in May, and was voted by the Senate in June and is expected to be officially passed in October.

The Genius Act focuses on the US dollar pegging “payment stablecoins” and makes clear provisions on its issuance qualifications, reserve requirements, and regulatory system, marking the first time that the crypto asset industry has been included in the US federal legal supervision and can be officially “corrected” from the gray area. The specific points and intentions are as follows:

1) in terms of issuer qualifications,The bill requires stablecoins to be issued by federally regulated institutions or approved non-bank financial institutions.The issuer must obtain a federal license to register with the competent authority (Treasury, the Federal Reserve and the FDIC).The issuance of stablecoins by listed companies not mainly engaged in financial business must be unanimously approved by the Minister of Finance, the Chairman of the Federal Reserve and the Chairman of the FDIC.

2) in terms of reserve requirements,The bill requires that all licensed payment stablecoins must be reserved 100%, and the reserve assets must be deposited in US dollar cash or high liquidity assets and be isolated from the issuer’s own funds.The bill clearly states that acceptable reserve assets include US dollar cash, US Treasury bonds that expire no more than 93 days, overnight repurchase agreements and designated money market funds.All stablecoin assets shall not be used for pledge, refinancing or reuse, and the issuer is also prohibited from paying any form of interest or income to the holder.

3) In terms of regulatory system,A dual-track regulatory system with “federal dominance and state-level supplement” has been established.A $1 billion issue size threshold has been set, and non-bank issuers exceeding this size must undergo federal supervision or can operate under state supervision.In addition, the bill requires stablecoin issuance to publicly disclose the composition of the reserve portfolio every month and conduct annual audits of issuers with market value of more than $50 billion.All licensed issuers are required to strictly comply with the United States’ anti-money laundering (AML) and sanctions requirements

2) China, domesticcurrentofPlanning focuses more on the construction of the digital RMB system, Hong Kong, China and Hong Kong actively deploy stable coins.Central Bank Governor Pan Gongsheng pointed out at the Lujiazui Forum, “With the improvement of efficiency and technology preparation, digital RMB and stablecoins are proposed as viable alternatives to cross-border settlement… But digital technology has exposed the weaknesses of traditional cross-border payment systems, which are inefficient and vulnerable to geopolitical risks.” The Hong Kong Monetary Authority of China also stated that “stablecoins can become a widely accepted means of payment, but must operate on the track of sovereign currencies.”