Network effects don’t stop with the Internet.

Both water and power grids are highly exclusive and are very suitable for “monopoly” collective management, which can benefit or harm the entire society. However, the network of relationships between people is naturally distributed and decentralized, and it is difficult for even a super socialist to know everyone.

Is Crypto a network of funds, or a field of interaction between people?

Satoshi Nakamoto obviously believed it was the latter, a peer-to-peer transaction model. Starting from this point, the history of the currency circle is that with the appreciation and expansion of funds, the link of funds is completely embraced, while the direct interaction between people is reduced.

The only reasonable question is, how long will it take for this intensive financial network to collapse?

1. Why the market recovered

Many people are still immersed in the liquidation of the 10·11 and 11·03 crashes, wondering how long it will take for synthetic stablecoins, Vault and Yield products to recover. However, Hyperliquid’s BLP and HIP-3 growth models are coming one after another, and the stablecoins YC prepared by Framework are all launched on Sky.

There is also Aave’s sudden arrival of V4 and mobile financial product App.

From an absolute data point of view, it is indeed a market recovery period, but from a physical perspective, the project team seems to be grasping the historical trend to innovate.

In other words, the market cycle and retail investor activity have become detached, which is not uncommon. The fundamentals of the U.S. economy have nothing to do with the real industry. The only thing Chuanbao cares about is interest rate cuts + stock prices. Americans and real industries are just a part of Play.

In this cycle, if you still think that there is a four-year Bitcoin cycle, you are just stuck in a time machine in 2017. Like the CloudFlare flash crash, the encryption infrastructure is always changing.

The DEX represented by Hyperliquid has indeed seized the CEX market, especially in conjunction with Meme, which has changed the token valuation, pricing and distribution system. In the era of CEX, which is visible to the naked eye, Kraken has a valuation of only US$20 billion, and many CEXs have turned to support their own DEXs.

When high FDV impacts the Binance pricing system in 2024, VCs will be dead, and then it will be the world of market makers: Hyperliquid and other Perp DEXs are behind market makers, and many YBS projects are also behind market makers.

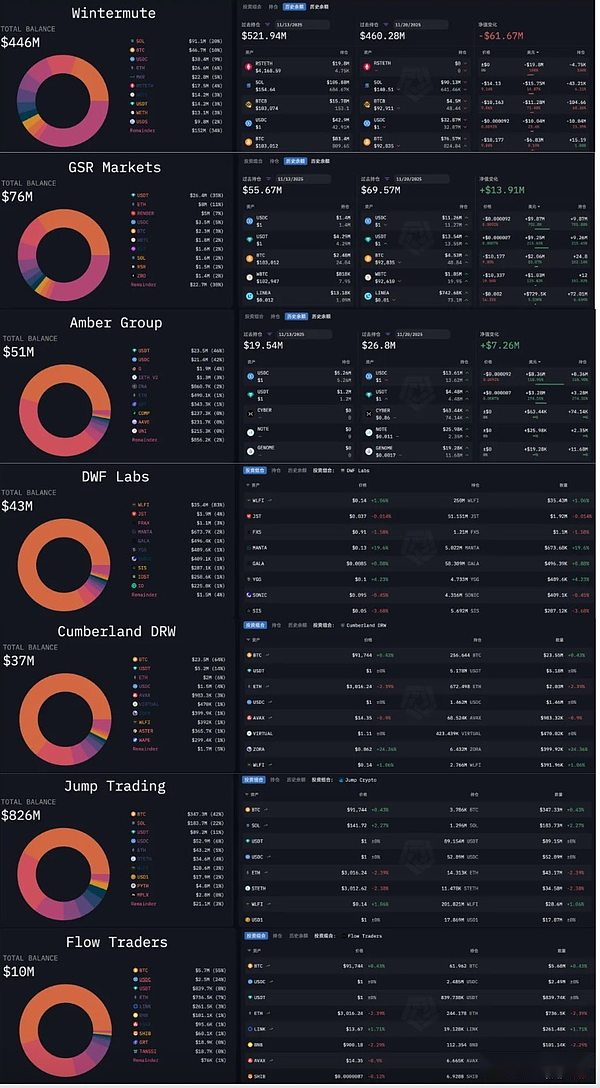

SBF was born in Jane Street, Jeff was born in Hudson River Trading, and the founder of Variational was born in the DCG market making department.

Even when ADL was liquidated on 10·11, it was the market makers who bore the brunt of the liquidation. This was a blessing and a curse. The market structure dominated by market makers became stiffer and stiffer than that dominated by CEX.

Web3Port wildly sells and manipulates currency prices, and DWF repeatedly manipulates currency prices. Even Hyperliquid’s HLP faces such accusations. Whether it is a centralized market maker or a decentralized treasury, as long as it participates in the market making system, it cannot escape the suspicion of market manipulation.

If the current market structure is called a “recovery”, then market makers have been hit hard, leaving them unable to continue to manipulate the market and instead allowing the market to stabilize.

This is not uncommon. Before the collapse of FTX in 2022, there were market rumors that Alameda once occupied 20% of the BTC market making share. In the SBF&FTX biography “Toward Infinity”, SBF admitted that they were the first professional company to make large-scale market making.

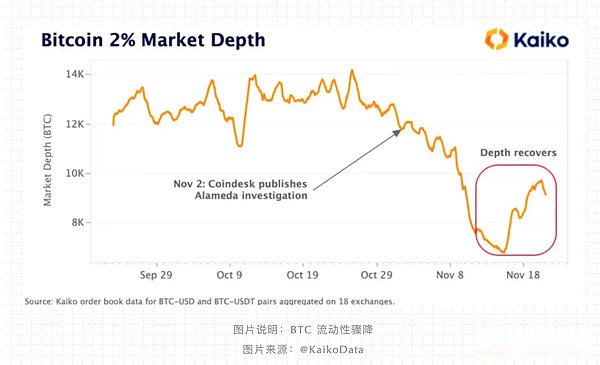

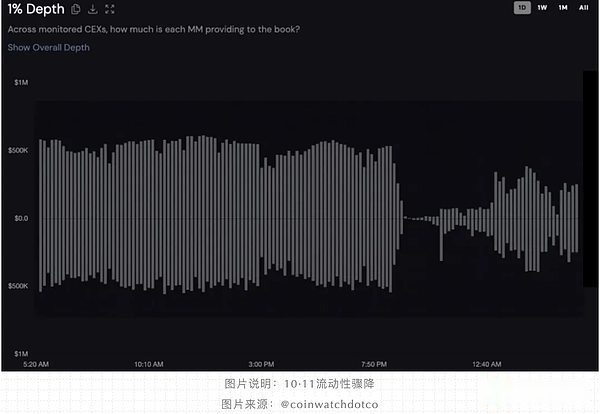

Going back to the flash crash of 10·11, from the perspective of market makers, it was a purely technical crisis, or in other words, the trading liquidity before that was a technical boom: retail investors were not trading, but market makers were buying and selling.

The existence of market makers is not a problem in itself, but for altcoins or TGE new coins, it means huge selling. Airdrop hunters and hair-raising parties, and even VCs and project parties themselves, will resolutely sell to market makers to lock in profits.

Market makers will be in a dilemma. If they don’t manipulate the market, they will inevitably eat up all the garbage coins, or they will become the Lich King, increasing market volatility as much as possible, making a little profit themselves, and occasionally letting market participants make a little bit.

There is a huge flaw in the reasoning here. We can only see the position composition and changes of market makers, and it is difficult to analyze specifically how they manipulate currency prices in CEX. The data of DEXs such as Hyperliquid are relatively transparent and are left for future analysis.

To sum up, the market is not rebounding, but the market makers have suffered heavy losses. In addition, the YBS project’s successive thunderstorms have caused the market makers to be unable to control the market. Now the real price mechanism is operating.

There is no recovery, only confession.

2. The 70% law of natural monopoly

The segmentation of various encryption circuits has revealed products with “natural monopoly” characteristics, such as EVM. In contrast, the Bitcoin network has failed as an infrastructure. Everyone is eager for BTC, but does not want to conduct P2P transactions.

Except for fans such as Jack Dorsey who insist on using the Bitcoin network as a stablecoin chain, BTCFi’s dream is real and tragic enough, and it would be good for the entire industry to stop imagining it.

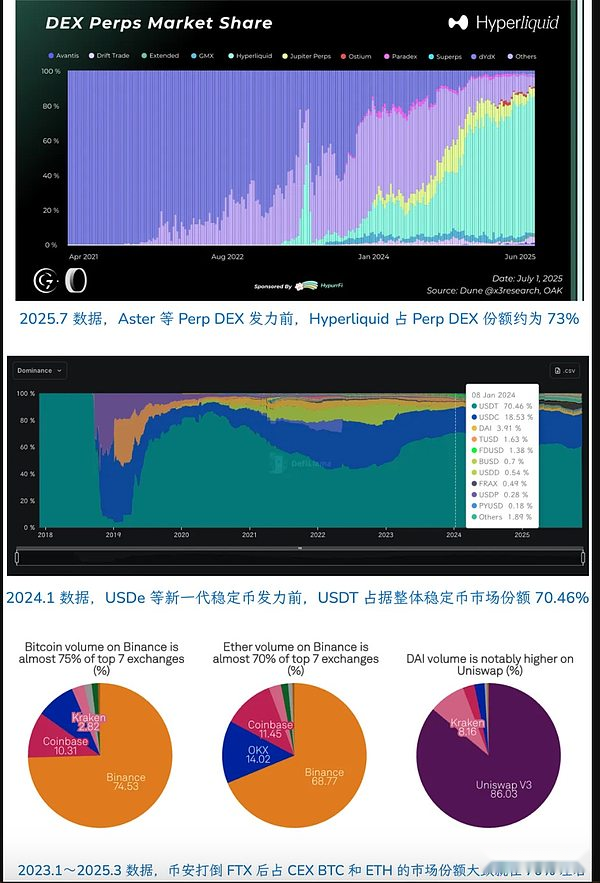

Outside of EVM, only Binance and USDT are close to the concept of “monopoly” as super single products. Please note that this does not conflict with CEX encountering the impact of DEX, or the innovation impact of USDC/USDe/YBS/Curator.

Super single product ≠ track

In other words, Binance and USDT are working hard to resist the increase in entropy. Ethereum has experienced repeated self-destruction (infinite garden, L2 scaling -> L1 scaling), and even now switches to privacy and AI, which highlight the freedom to do whatever you want. EVM is still the mainstream choice.

But the market share of Binance and USDT, and even Hyperliquid’s share of Perp DEX, roughly peaked at around 70%, and then more market action was needed to stabilize the current position.

An empirical summary shows that under a stable market structure, the top projects can occupy 70% of the market share of the track. However, the market environment changes over time, and the current shares of Hyperliquid, USDT and Binance have all dropped below 50%.

Of course, EVM is absolutely stable on the overall VM track, and only a few opponents, such as SVM or Move VM, can be regarded as entering an ultra-stable structure.

Looking at the market makers from this perspective, we know that there are at most 20 mainstream market makers in the market, and it is speculated that they occupied the mainstream position in the market before 10·11, but they have not reached the status of a natural monopoly. Even if they are forcibly maintained, they are now at the end of their strength.

So how will the market structure change in the next stage?

3. The replacement of the old with the new is in progress

-

If you follow the path of traditional finance, you will be limited in valuation using traditional financial valuation models.

-

Taking the path of an Internet financial technology company will be limited by the scale of the Internet valuation.

-

Only by finding a path that fits the valuation model of the currency circle and not being defined by any existing industry can we create the top 5 trillion players like AI.

The market has been really strange recently. Solana is a pioneer in RWA and institutional adoption. Lily Liu, the chairman of the foundation, suddenly said that she will regain the cryptopunk dream. Combined with Ethereum’s return to the L1 Scaling route, and the privacy concept mentioned above, Zcash has become popular from boundless.

Crypto seems to be rediscovering the technical logic and valuation system of the currency circle, and these have less and less to do with market makers. Even if it is adopted by institutions, it is more “Currency projects need to use institutional funds to do DeFi“, instead of “Sell DeFi in the currency circle to institutions“.

In one sentence, get rid of MM internally and get rid of institutions externally.

Even OGs have to keep up with the new era. The DAT co-branded by Li Lin and Xiao Feng also died. After breaking through the Chinese VC, the Big Name effect of OG will also go into history.

Crypto regains its dream at the cost of getting rid of the parasitic system on top of it.

Referring to the most mature US capital market, A16Z is a part of the US capital market, but Chinese VC is not. Only the government, state-owned enterprises (state-owned capital groups) and Internet companies (previously) have money.

Reflecting the situation of Chinese VCs in Web3, Chinese VCs do not have the ability to participate in the market’s pricing and distribution system. Market makers and CEX used to be, but after 10·11, the industry’s on-chain trend became increasingly clear.

On-chain ≠ decentralization.

Typical ones like Hyperliquid are transparent on the chain, but are not decentralized in terms of physical nodes and token economics.

Even the actual capitalization reform of state-owned enterprises does not simply involve selling old ones for new ones, but investing in new industries in exchange for a ticket to the new world.

From this perspective, the biggest problem of market makers is similar to Meme. Liquidity has no value. In the ultimate nihilistic PVP, you can make a lot of money, but market makers cannot be the leading force in the industry.

Dreams and long-term technicalism, Vitlaik does too much, MM does too little, so we should be more moderate.

4. Conclusion

Essentially, this article is written for myself. In theory, the market should have stagnated after 10·11 and 11·03, but the decline in TVL did not hinder the innovation and self-healing of DeFi, which puzzles me.

Vault, YBS (interest-bearing stablecoin) and Curator are still evolving, and the market is tougher than we thought. If you still look at the market with the same concepts as a month ago, or even a week ago, you will not understand.

In the post-MM industry-dominated era, the balance between currency circle values and product profitability will redefine valuation logic.