Author: Thejaswini, Source: Token Dispatch, Compiled by: Shaw Bitchain Vision

In 1979, the Republican Bank offered several options for its clients.Save $1,475 for a period of 3.5 years, you can get a 17-inch color TV when it expires; or deposit the same amount for a period of 5.5 years, you can get a 25-inch TV.Want something more cost-effective?Save $950, with a term of 5.5 years, and you can get a sound system with built-in disco lighting when it expires.

During the Great Depression, bank regulatory regulations prohibited banks from paying competitive interest rates, and this is how banks compete for deposits.The Banking Act Q, promulgated in 1933, prohibited banks from paying interest on demand deposits and restricted interest rates on savings accounts.Although money market funds provide higher yields, banks can only give away toasters and TVs, but cannot provide real returns.

The banking industry calls money market fund investors “smart money” and calls their depositors “stupid money” thinking they don’t know how to get higher returns elsewhere.

Wall Street happily accepted this statement, using it to describe investors who seem to always buy at high levels, sell at low levels, chase trends, and make emotional decisions.

Fifty years later, these “stupid money” have ended in laughter.

The concept of “stupid money” is deeply rooted in Wall Street psychology.Professional investors, hedge fund managers and institutional traders build their entire identity on the role of “smart money” – they are those who can see the essence through market noise and make rational decisions, while retail investors blindly follow the trend in panic.

This statement works when retail investors do do this.During the Internet bubble, short-term traders mortgaged real estate and bought it at the peak of technology stocks.During the 2008 financial crisis, retail investors fled as the market bottomed out, missing the entire recovery cycle.

This model is: professional investors buy low and sell high, while retail investors are the opposite.Academic research confirms this bias.Professional fund managers point out that these models prove their superb skills and justify the fees they charge.

What has changed?It is a way of access, education and tools.

New reality of retail investors’ investment

The data today are completely different.US President Trump announced an increase in tariffs in April 2025, causing the stock market to plummet by $6 trillion in two trading days. Professional investors sold their stocks, while retail investors regarded it as a good opportunity to buy at the bottom.

Throughout the market turmoil, individual investors rushed to stocks at a record pace, and they netted $50 billion in U.S. stock, earning about 15%.During this period, retail clients of Bank of America bought stocks for 22 consecutive weeks, the bank’s longest consecutive buying record since 2008.

Meanwhile, stock exposure for hedge funds and systematic trading strategies was at the lowest 12% range, missing the entire rebound.

The same model has also been staged during market fluctuations in 2024.Data from JPMorgan shows that retail investors drove the rise in major markets in late April, with individual investors controlling 36% of the market share from April 28 to 29, setting an all-time high.

Steve Quirk of Robinhood summed up the shift: “Every time the stock is listed is oversubscribed. The demand is always greater than the supply. Issuers like this and hope that those who support their company will get a placement.”

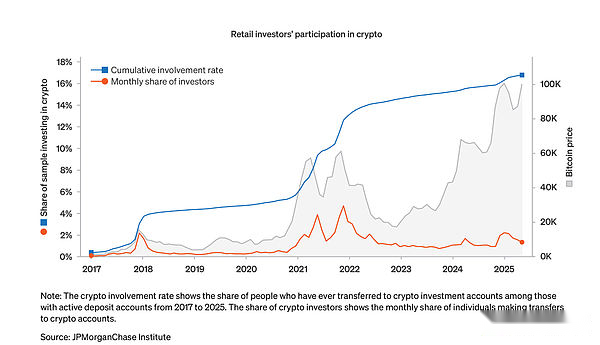

In the cryptocurrency field, retail investors’ behavior has evolved from the typical “buy high and sell low” model to a smart market timing.JPMorgan data shows that between 2017 and May 2025, 17% of active checking account holders transferred funds to cryptocurrency accounts, and participation surged at strategic moments rather than at peak mood.Data shows that retail investors are increasingly showing “buy on dips”, with the sharp rises in March and November 2024 synchronizing with Bitcoin’s record highs, but it is worth noting that when Bitcoin reaches a higher peak in May 2025, retail investors’ participation remains cautious rather than fanatical.This shows that retail investors are learning and restraining, rather than the “fear of missing out” (FOMO) behavior traditionally associated with retail cryptocurrency investors.The median cryptocurrency investment remains at a moderate level, indicating that they have adopted prudent risk management rather than over-speculation.

Industry sectors such as gambling, sports betting and Meme coins have proved that there is still a “continuous supply of stupid money”.But the data shows that this is not the case.

Gambling and sports betting platforms do generate billions of dollars in transactions, with the online betting market valued at $78.66 billion in 2024 and is expected to reach $153.57 billion by 2030.

In the cryptocurrency space, Meme coins often trigger speculative frenzys, leading to later entrants holding worthless tokens.

Yet even in these so-called “stupid money” areas, people’s behavior has become increasingly sophisticated.Pump.fun, despite earning $750 million in revenue by creating Meme coins, plunged from 88% to 12% when competitors provide better communication and transparency.Instead of blindly sticking to using existing platforms, retail users have turned to platforms that provide better value propositions.

The Meme currency phenomenon is not so much a stupidity of retail investors, but rather a retail investor rejects the issuance of tokens supported by venture capital and rejects fair access.As one cryptocurrency analyst puts it, “Meme coins give token holders a sense of belonging and promote connections based on shared values and culture” – they are both social and financial, not just speculative.

IPO revolution

This is most evident in the growing influence of retail investors in the initial public offering (IPO) market.Businesses are abandoning the traditional model of serving only institutional investors and high net worth individuals.

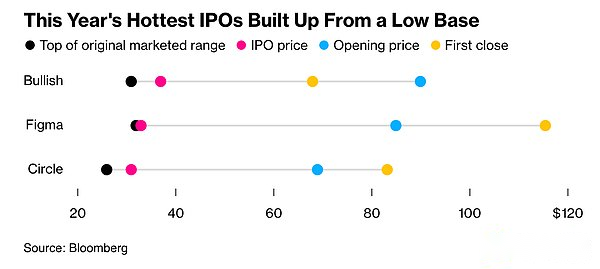

Bullish represents the watershed in the issuance method of corporate IPOs.Founded by Block.one and backed by major investors including Peter Thiel’s Founders Fund, Bullish is both a cryptocurrency exchange and an institutional trading platform.The cryptocurrency company raised $1.1 billion in its IPO, allowing retail investors to directly participate in its issuance through platforms such as Robinhood and SoFi.Retail demand is strong, with Bullish’s issue price set at $37 per share, nearly 20% higher than the initial issue price.The stock price soared 143% on the first day of listing.

Bullish sold one-fifth of its stock to individual investors, worth about $220 million, about four times the normal level seen by industry veterans.Moomoo’s customers alone placed orders of more than $225 million.

This is not an isolated incident.The Winklevoss brothers’ Gemini clearly stipulates that 10% of the funds are allocated to retail investors.Figure Technology and Via Transportation both use retail investors to conduct IPOs.

This shift reflects a fundamental change in the perception of retail investors.As Becky Steinthal of Jefferies Group explained:

“Issuers can choose to allow retail investors to occupy a larger share of the IPO process than before. This is all driven by technology.”

According to Robinhood, its platform’s IPO demand in 2024 is five times that in 2023.The platform currently has a policy prohibiting stock reselling within 30 days of the IPO, creating more stable buying and holding behaviors that benefit both the company and long-term shareholders.

This change is not only reflected in personal investment decisions, but also in changes in market structure.Retail investors currently account for about 19.5% of U.S. stock trading volume, up from 17% a year ago and far higher than about 10% before the epidemic.

More importantly, retail investors’ behavior has undergone a fundamental change.In 2024, only 5% of Pioneer 401k plan investors adjusted their investment portfolio.Currently, the target date fund has exceeded US$4 trillion.

This means that investors trust systematic and professionally managed investment plans more than frequent trading.This shift helps avoid high-cost transaction errors caused by emotions, thus achieving a more ideal retirement plan.

Data from eToro shows that by 2024, 74% of its users will be profitable, and the profit rate of senior members will be as high as 80%.This performance is contrary to the basic assumption that retail investors continue to lose money due to professional fund managers.

Demographic data support this shift.Young investors entered the market earlier – Generation Z started investing at an average of 19 years, while Generation X was 32 years old and Baby Boomer was 35 years old.They have educational resources that previous generations don’t have: podcasts, newsletters, social media celebrities, and zero commission trading platforms.

The popularity of cryptocurrencies best reflects the increasing maturity of retail investors.Although institutional investment news about Bitcoin ETFs and corporate treasurys have dominated the headlines, the actual use of cryptocurrencies is driven primarily by retail investors.

India leads the global cryptocurrency adoption rate, followed by the United States and Pakistan, according to Chainalysis.These rankings reflect the grassroots use of centralized and decentralized services, rather than institutional accumulation.

In 2024, the stablecoin market will be dominated by retail payments and remittances, with USDT alone processing more than $1 trillion in transaction volume per month.USDC’s monthly trading volume is between $1.24 trillion and $3.29 trillion.These are not institutional funding flows.They represent millions of independent transactions of individual payments, savings and cross-border transfers.

When we divide cryptocurrency adoption by World Bank income rating, the adoption rates of high-income, upper-middle-income and lower-middle-income groups peaked simultaneously.This suggests that the current wave of cryptocurrency adoption is widespread, rather than concentrated in the wealthy early adopter population.

Bitcoin remains the main fiat currency entrance, with the total amount of Bitcoin purchased through exchanges exceeding $4.6 trillion between July 2024 and June 2025.However, retail investors are becoming more and more mature in diversified investment allocation, and Layer1 protocol tokens, stablecoins and altcoins have all received a large amount of capital inflows.

By examining the recent behavior of institutional investors, you can most clearly understand the irony of the dispute between “smart money” and “stupid money”.Professional investors always misjudgment the main trends of the market, while retail investors show discipline and patience.

During the institutional adoption phase of cryptocurrencies, hedge funds and family offices made headlines for incorporating Bitcoin into their portfolios near the peak of the cycle.Meanwhile, retail investors increased their holdings of Bitcoin during bear markets and held them during market volatility.

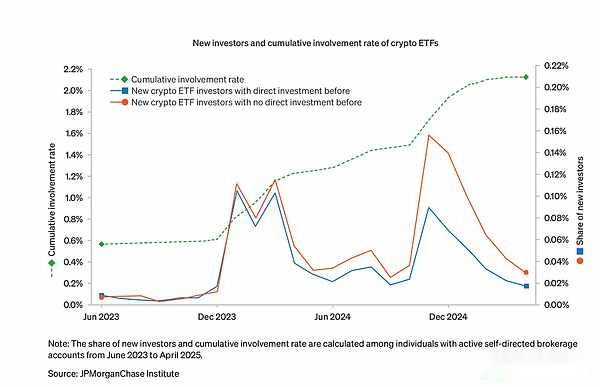

The rise of cryptocurrency ETFs perfectly illustrates this.More than half of cryptocurrency ETF investors have never held cryptocurrencies directly before, indicating that traditional channels are expanding rather than cannibalizing the investor community.Among ETF holders, the median allocation of the portfolio remains around 3%-5%, indicating that they have adopted a prudent risk management strategy rather than over-speculation.

The recent behavior of professional investors is exactly the same as the typical mistakes they have long criticized for the average investor.When the market is turbulent, institutional investors tend to flee the market to keep quarterly performance indicators, while retail investors buy on dips for long-term holdings.

Technology is a great equalizer

The change in retail investors’ behavior is not accidental.Technology democratizes access to information, tools and markets that were previously available to only professionals.

Robinhood’s innovations are much more than zero commission trading.They launched tokenized U.S. stocks and ETFs for European users, staking Ethereum and Solana in the United States, and are building a follow-up trading platform that allows retail users to follow verified top traders.

Coinbase expands consumer-facing cryptocurrency products by improving mobile wallets, forecasting markets and simplified staking processes.Stripe, Mastercard and Visa have all launched stablecoin payments to support cryptocurrency consumption at thousands of retailers.

Wall Street’s recognition of retail investors’ influence has formed a feedback loop, further empowering individual investors.When companies like Bullish succeed with retail-focused IPO strategies, other companies will follow suit.

Jefferies’ research pointed out that stocks with high retail trading volume and low interest from institutional investors are potential investment opportunities, including Reddit, SoFi Technologies, Tesla, Palantir, etc.The study shows that “when retail investors make up a larger proportion of trading, the quality in traditional indicators becomes less important” – but this may reflect that retail investors have different evaluation criteria rather than poor decision-making capabilities.

This dynamic is reflected in the evolution of the cryptocurrency industry towards mass accessibility.Today, the competition for major platforms is focused on user experience, not just institutional relationships.Convenient perpetual trading, tokenized stocks and integrated payments are all aimed at the participation of mass investors.

The “stupid money” has always existed in part because it is in the economic interests of professional investors.Fund managers justify charging high fees by claiming that they have excellent skills.Investment banks maintain their pricing power by limiting access to lucrative transactions.

Data show that these advantages are gradually disappearing.Retail investors are increasingly showing what professionals claim to be self-discipline, patience and keenness to grasp market opportunities.At the same time, institutional investors often show the emotional and trend-following behavior they have long believed to be unique to retail investors.

This does not mean that every retail investor will make the best decision.Speculation, abuse of leverage and trend pursuits are still common.The difference is that these behaviors are no longer unique to “retail investors” – they exist among all types of investors.

This transformation has structural implications.As retail investors continue to gain influence in IPOs, they may demand stronger terms, higher transparency and fairer access conditions.Companies that follow this change will benefit from lower customer acquisition costs and a more loyal shareholder base.

In the cryptocurrency space, retail dominance means that products and protocols must prioritize availability rather than institutional functions.Platforms that allow complex financial services to be used by ordinary users will succeed.

There is a fact behind the recent success of retail investors: Almost all assets have risen over the past five years.The S&P 500 rose 18.40% in 2020, 28.71% in 2021, 26.29% in 2023, 25.02% in 2024, and only showed a significant decline in 2022, with a decline of 18.11%.Even in 2025, it has risen 11.74% so far this year.

Bitcoin rose from about $5,000 in early 2020 to nearly $70,000 in 2021, and despite the continued volatility, it is on an overall upward trend.Even traditional assets such as Treasury bonds and real estate have seen a sharp rise during this period.In an environment where the “buy on dips” strategy has been tried and true, and almost any asset can generate positive returns after holding for more than one year, it is difficult to distinguish between skills and luck.

This begs an important question: Can retail investors’ seemingly sophisticated skills survive a real bear market.The longest significant drop most Gen Z and millennial investors have experienced is the COVID-19 shock that lasted only 33 days.Although the inflation panic in 2022 was painful, it quickly recovered afterwards.Warren Buffett’s famous saying “You only know who is swimming naked when the tide recedes” applies here.Retail investors may indeed be smarter, more self-disciplined, and more knowledgeable than previous generations.Or maybe, they are just beneficiaries of an unprecedented bull market in almost all asset classes.The real test will come when the easing monetary environment ends and investors face continuous losses in their portfolios.Only then can we know whether the “stupid money” transformation is permanent or simply due to a favorable market environment.