Author: Memento Research; Translation: Bitchain Vision xiaozou

This article positions the enduring Pokémon Trading Card Game (TCG) as a unique durable collectible IP, which is pouring into the crypto chain field with the form of “RWA × Gacha” (note; Gacha, draw card, from the Japanese noun gachapon) platform to achieve a real economy that combines mobile scale demand and crypto-native distribution.

This article covers many contents, including TCG IP mental share and asset performance, mobile demand funnel, on-chain platform growth, traffic quality and user groups, economic benefits of each scenario unit, as well as risks and catalytic factors.

Through data research, we concluded that:

Gacha accounts for more than 90% of the platform’s transaction volume;

5-20% of users contribute about 90% of their consumption;

The net commission rate after deducting repurchase is between 12% and 31%.

1, market overview and background introduction

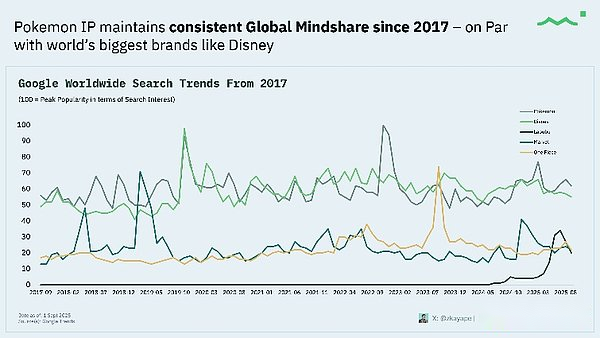

Pokémon continues to maintain a global mental share comparable to Disney (2017-2025), and outperforms other popular fans’ IPs (Marvel, One Piece and Labubu, the most popular recently).

The Lindy effect shows that the longer the thing lasts, the longer its expected remaining life.Lasting attention is crucial to long-term liquidity; this explains why secondary markets do not collapse due to short-term macro factors (such as watches, rare TCG cards, artworks and classic cars).

What we need to explain is: Search interest scale≠The amount of consumption, but this isTCGThe leading indicator of the activity will show how attention is converted into paid behavior in the future.

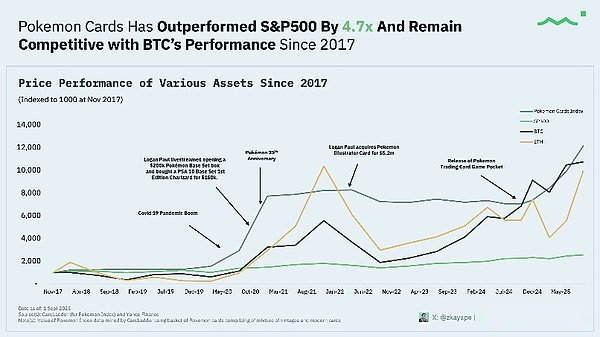

Since November 2017, the Pokémon Card Index has outperformed the S&P 500 by about 4.7 times, and is even on par with Bitcoin – a specific event (Logan Paul hype incident, COVID-19 crisis, 25th anniversary) has boosted the momentum.

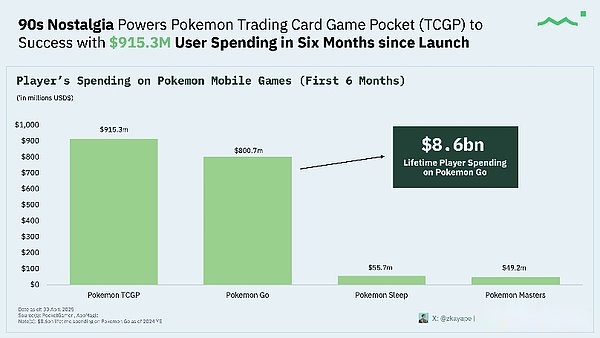

Pokémon TCG Pocket (TCGP) generated approximately $915.3 million in 6 months, significantly surpassing other Pokémon mobile products, and Pokémon GO’s lifetime consumption ($8.6 billion) confirms the IP’s paid basis.This shows the huge paid funnel for opening a card bag, and how the gacha mechanism becomes a money-making machine.

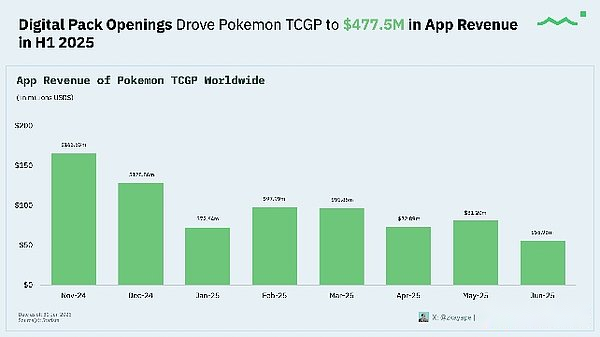

The US$477.5 million in the first half of 2025 (strong performance at the beginning of the cycle) showed the “new work explosion effect” boosted by the opening of digital cards.Similar to the Labubu phenomenon, this confirms the continued attractiveness of the blind box economic model – the gacha platform replicates the same behavioral pattern with physical cards.

Blind box and gacha culture originated from Japanese gauge capsule machines: randomly obtain toys/figures from the series, with the characteristics of low cost and high repurchase rate.TCG focuses on the opportunity to draw rare and high-value cards.The combination of the two works because:

Surprise is the product: Drawing rare cards can obviously stimulate dopamine secretion;

Community + onlooker effect: unboxing videos, unpacking live broadcasts, and showing off culture on social media;

Financialization: The card bag/box itself becomes tradable assets (sealed Pokémon box, Pop Mart cargo box).

2, PokémonCardOn-chainTokenization

FocusCourtyard(Polygon)Collector’s Crypt(Solana)Phygitals(Solana)andEmporium(Solana)platform.

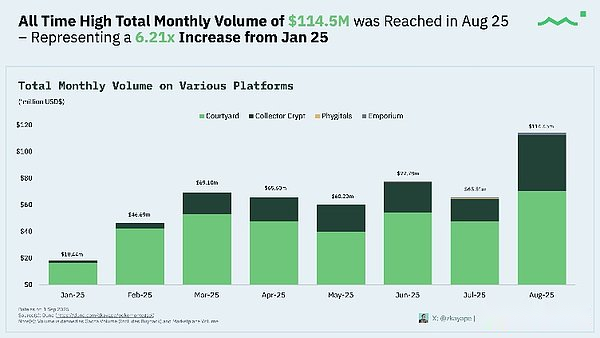

The monthly trading volume of the card tokenized trading sector reached a historical peak of about US$114.5 million in August 2025, an increase of about 6.2 times from January 2025 – this data covers four major leading platforms: Courtyard (Polygon), Collector Crypt, Phygitals and Emporium (the latter three are based on Solana).

This data shows how these platforms form continuous liquidity through compound network effects (inventory depth × user scale).

Note: Trading volume includesgachaMechanism and market transactions.

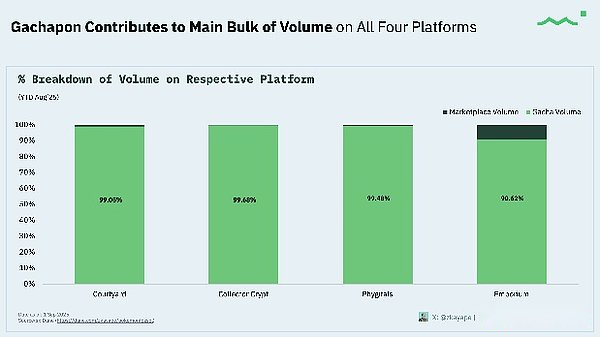

The data clearly shows that the Gacha mechanism is the dominant driving force (accounting for about 90-99% of the total transaction volume of the four major platforms), which accurately reveals the actual sources of most revenue (card package profits, handling fees and repurchase income), rather than peer-to-peer transactions in the secondary market.

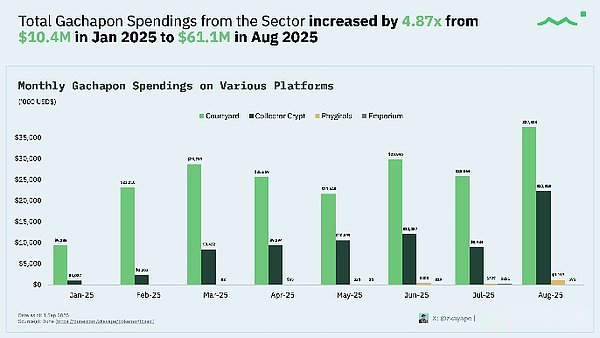

Gacha consumption expanded from about $10.4 million (January) to about $61.1 million (August), an increase of about 4.9 times.Consistent with the recent boom trend of traditional card game platforms, these on-chain platforms have found product market fit.What is more noteworthy is that the growth rate of user consumption has exceeded the growth rate of market transaction volume, which means that users have a good acceptance of the repurchase/application cycle model.

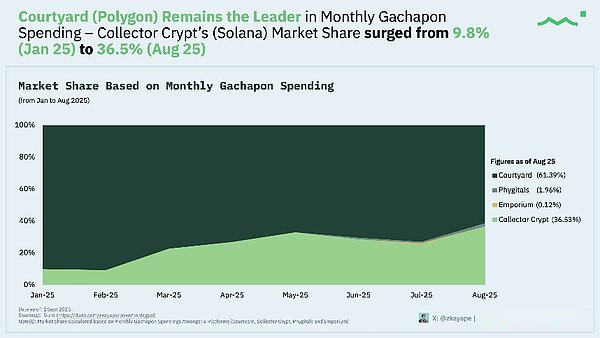

Courtyard maintains a leading position in terms of market share, but Collector Crypt’s share rose sharply from about 9.8% (January) to about 36.5% (August); Courtyard accounts for about 61.4%; Phygitals accounts for about 2%; and Emporium accounts for about 0.1%.

3,GachaUser consumption habits and financial status

Analysis on the contribution of users at all levels of income, consumption distribution and total income dismantling

(1)Courtyard

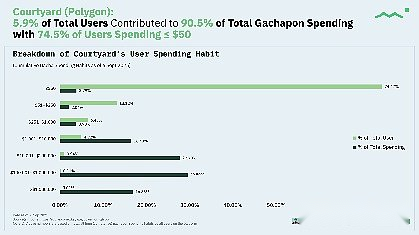

As for Courtyard, it can be seen from the consumption model that 74.5% of users consume ≤ US$50, while only about 5.9% of users contributed about 90.5% of the total gacha expenditure.This is a typical whale economic model.

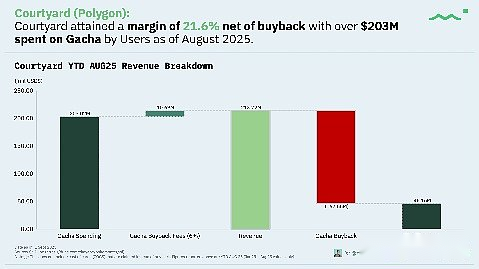

Courtyard has consumed approximately US$203 million in the year to date (January-August), and its net profit margin after repurchase is about 21.5%.This shows that under the scale effect, even if there is a large inventory cycle, the “gacha+ repurchase” flywheel can still achieve a net profit margin of more than 20%.

(2)Collector Crypt

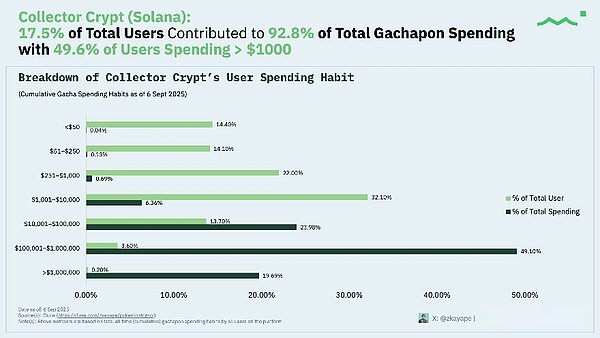

Collector Crypt data shows that 17.5% of users drive about 92.8% of consumption, of which about 49.6% of users spend more than $1,000.Its consumption distribution is more profound than Courtyard, and it tends to be a “strong collector” group.Pricing strategies, repurchase speed and series planning should reflect higher risk tolerance.

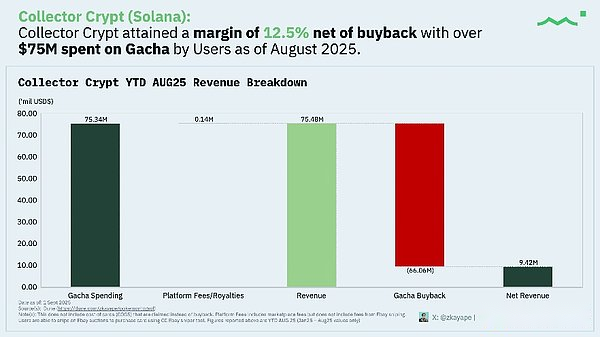

The platform’s Gacha consumption has been approximately US$75.3 million since the beginning of the year, and its net profit margin is approximately 12.5% after approximately US$66.1 million in repurchase and moderate platform/copyright fee expenditures.Compared to Courtyard’s lower net profit margin suggests that it may adopt a more aggressive repurchase strategy, different fee structures or higher inventory, most of the revenue has been embedded in the Gacha mechanism.

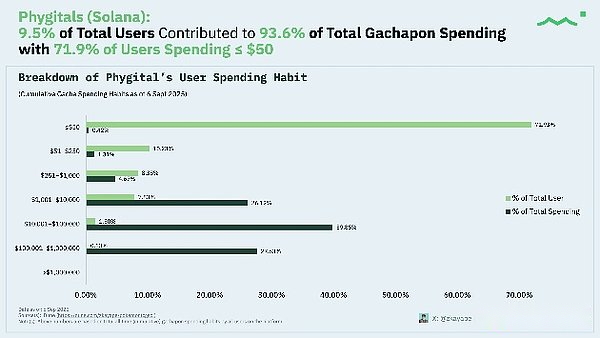

(3)Phygitals

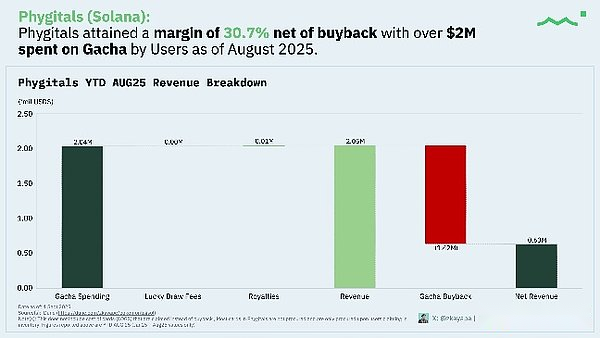

Phygitals platform data shows that 71.9% of users spend ≤ US$50, but about 9.5% of users contributed about 93.6% of the consumption.Gacha consumption has been approximately US$2 million since the beginning of the year, and its net profit margin after repurchase of approximately US$1.42 million is about 30.7%; Note: Most cards are only purchased when applying.

On-demand procurement models can generate higher net profits at smaller scales, as there is no need to bear sales costs in advance, which is especially beneficial for platforms lacking strong balance sheets.But the risk is transferred to the performance process – any delay or supplier error may quickly lose user trust.

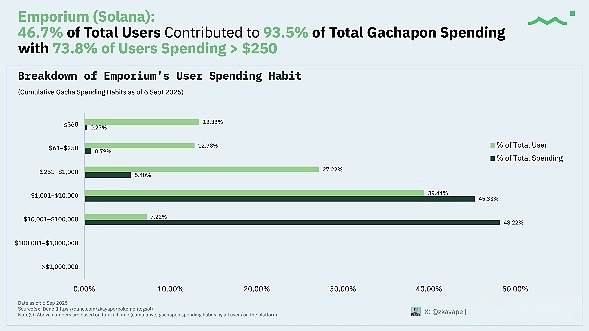

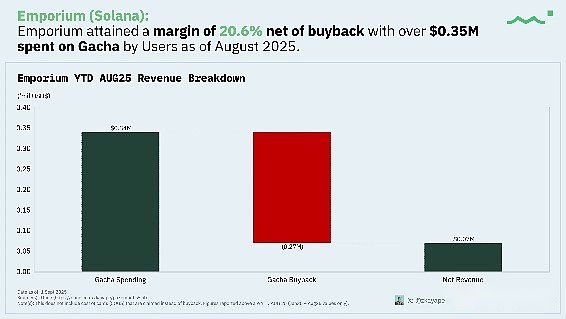

(4)Emporium

About 46.6% of the users of the Emporium platform contributed about 93.5% of the consumption, and about 73.8% of the users spent more than US$250.Data shows that the platform is positioned at a medium- and high-consumption group and gathers more loyal collectors.Gacha consumption has been approximately US$350,000 since the beginning of the year, and its net profit margin after a repurchase of approximately US$270,000 is about 20.5%.

4, conclusion

For all platforms, the Gacha mechanism is the core business – because it accounts for 90-99% of the capital flow; placing it on the chain to attract crypto community fanatics, achieving product market compatibility.

Different whale groups have different operating paths: Courtyard = broad user base + a small number of whales; Collector Crypt/Emporium = deep consumer group; Phygitals = dumbbell structure has the advantages of application and procurement.

Net profit margin is the result of policy orientation.The repurchase frequency, fee structure and inventory model jointly determine the platform’s net profit level of about 12%, 20% or 30%.