Author: Hyphin Source: On Chain Times Translation: Shan Ouba, Bitchain Vision

The seeds under the uncertainty finally began to make fruit.Retail investors have brought a hole card to everyone, while private capital is like a bottle.What are they holding in their hands?What is the result of their betting?They have been doing cautiously since Bitcoin was traded at such a price transaction.Does this strategy change?

introduce

Regardless of the market environment, financing will never stop completely,Because the industry’s innovation engine is efficient enough to reward those who provide motivation for it.However, enthusiasm depends to a large extent on prediction.Historically, favorable conditions are often attractive to early capital, because potential returns far exceed relevant risks.For many viewers, the increase of these profitable entities indicates that the party has begun or is about to begin.Obviously, we have been in the bull market for a long time, and the fort is close at hand.Considering this, people can expect cumulative funds to exceed or close to the standards set at least in the previous cycle.

>

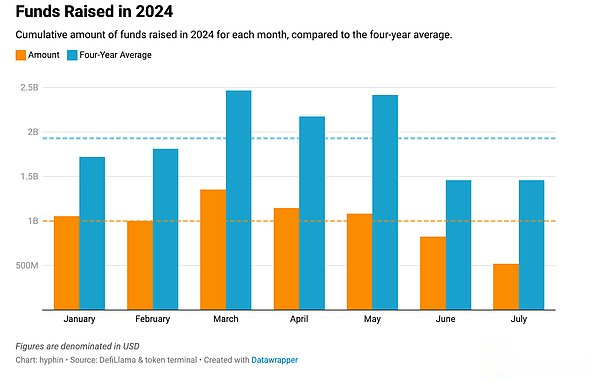

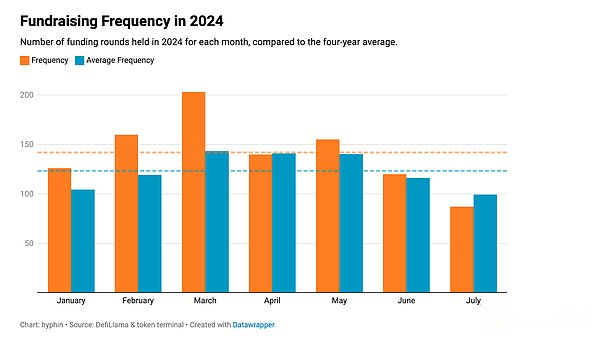

It is certain that these optimistic expectations have been supported by reality, because this year’s monthly indicators are dwarfed compared with the four -year average.Compared with 2018, 2021, and 2022, these numbers are just a drop in the seas made of zero interest rate and cheap currency era.Although the financial data of the report is not worth seeing, they do show that as we transition to the new normal, the opportunity to get a large number of initial initial funds has been significantly reduced.This does not mean that people in the office have relaxed their vigilance because the event seems to have decreased.Instead, the number of investment rings has actually higher than the average level.

>

Before Bitcoin reached a record high, the release of financing announcements drafted has accelerated significantly, showing the strong participation of behind -the -scenes guidance operations.This surge is mainly due to off -site participantsA large number of entering the marketAnd participate in more rotation than usual.However, the activity is gradually decreasing, because from a historical point of view, summer is relatively calm.

>

It is true that the average salary obtained by the founders is definitely not as much as before, which forces entrepreneurs to be resourceful and wisely managed their burning rate in order to successfully push their works to the end.

Emotion/positioning

After understanding the current financing situation, we can confidently infer that risk investment is expected to have some room for rise in unpredictable future.Although the scale of betting does not bring too much confidence, risk preferences may be possible.The company can raise funds at all stages of development, and each stage has its own considerations and the scope of industry standard amount.

To understand more information about general knowledge and terms, we recommend that you check our previous article about the theme before continuing.

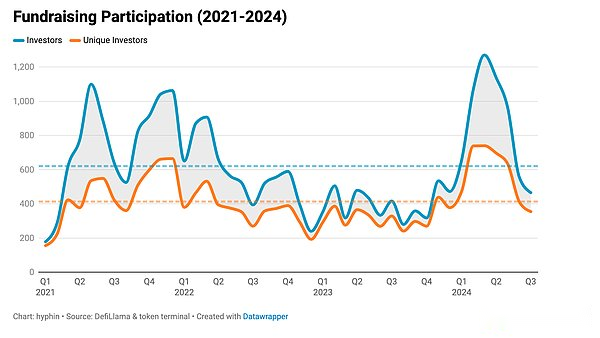

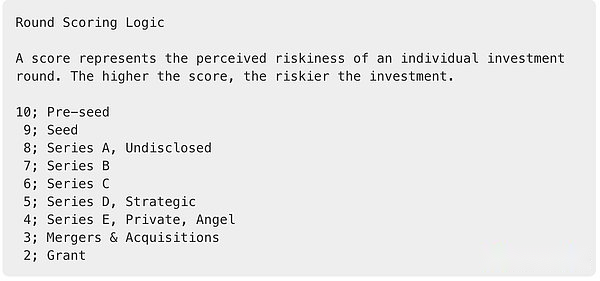

By classifying according to the characteristics of the investment type, we can allocate a risk score for them.This enables us to roughly measure the overall risk tolerance of all vested interests, so as to quantify the collective tendency of their participation in speculative activities to determine confidence in continuing or changing trends.

>

The emotions in our map will use oneComprehensive indicators to represent,This indicator is weighted by using the value we established beforeFrequencyandQuantity -based scoreAdd to calculate.

>

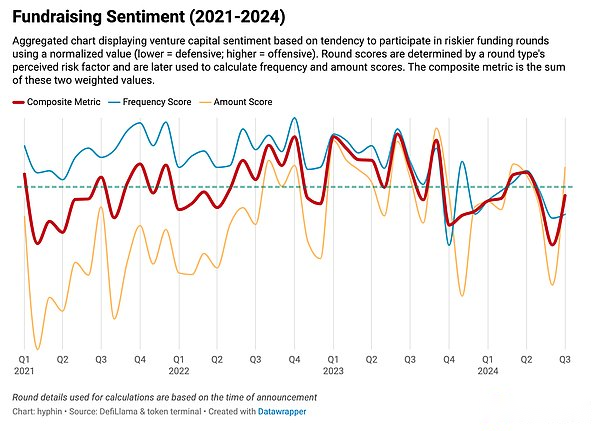

The lower the comprehensive indicators, the more conservative positions indicate, and the higher the comprehensive indicator, the more aggressive the position.The transformation between these positions can be determined by whether this value intersects with the average value (marked as a green dotted line on the chart).

>

Although this picture is a bit overwhelmed, it provides an interesting perspective, showing how the positioning and investment methods have evolved over time.In the previous cycle, the low and high frequency scores caused the comprehensive indicators to be relatively mild, because a large amount of funds were mainly invested in the high valuation series wheels.Many capital companies have made major bets on the industry through infrastructure and institutional products.This emotion began to change at the end of the rebound, and early financing with higher risks became more prominent, because people attach more importance to incubating emerging projects while maintaining conservative commitments.The rhythm changes can be seen around the last quarter of 2022. At that time, a large -scale personal round of personal rounds were performed during the FTX collapse and the future of cryptocurrencies.After the disaster surrender and the bottom of the market, the private capital adventure has greatly increased financial support for the development of companies in the development of companies until the fourth quarter of 2023.Subsequently, larger private equity and series of strategic rotation became the focus.This trend continues to exist most of this year. Although the activity has set a record, the frequency score has declined.This shows that investors are more cautious and selective during configuration, and tend to be more secure investment.

Capital analysis

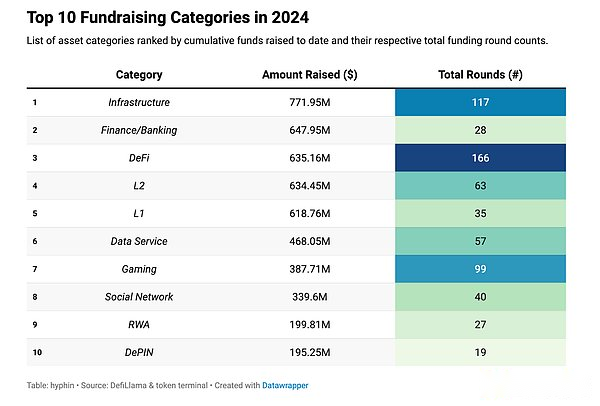

This year is a difficult year for most cottage coins. Only a few categories of cottage are better than major assets.Even those who obtain tokens at a discount price cannot be spared because it turns out that the downward potential of speculative investment is almost bottomless.Choosing the correct niche market is more important than ever.In order to fully understand the flow of funds and evaluate the most sought -after narrative, we can map the raised amount to their respective categories.In order to maintain consistency, all publicly traded Bitcoin mining companies are excluded from data sets.It is worth noting that not all the interest rate hikes have reported numbers, so the actual composition may be slightly different.

>

Compared with last year, investors’ interests have undoubtedly weakened. Some traditional industries that were previously ignored have attracted more attention together because investors have used a wider ecosystem and infrastructure methods.This further confirms such a view that risks are being carefully evaluated, with limited contact with newly formed or re -appearing.

>

Focusing on the popular part, infrastructure has naturally become the basic pillar of the industry. Projects like Eigenlayer paved the way for new primitives and generated a lot of economic value and activities.Unexpectedly, aimed at expanding existing businesses and launching various trading venues and financial services for new products for institutions and ordinary users, and also received generous funding.The last close attention to the corner of this market was in 2021, when the employment and simplified income work reached the highest level of history.As for the other entries on the list, compared with last year, the amount of funds is either declined or kept relatively stable, leaving only some noticeable observation results.

The revival of L1 and L2

After some high -profile financing, the blockchain as an investment has once again become the focus of attention.Although the market 1 has been saturated, Monad (US $ 225 million) and BERAChain ($ 100 million) have received a lot of liquidity injection, similar to 2022 injection.Compared with last year, the total value of the industry has increased almost tripled.Roll-up also shared this success, and its cumulative funds slightly exceeded the funds assigned to the basic chain, thanks to the new development of the field.Although the second -level solution on Ethereum or the use of its underlying technology solutions has always been the focus of attention, replacing virtual machines and chain deployment shows more and more attention.Bitcoin and Solana are typical examples in this area.

The rise of social networks

Although decentralized social platforms have existed for some time, they have always been difficult to attract a large number of user bases or obtain a lot of funds.The biggest challenge facing these platforms is to transform Twitter users, and Twitter is still the actual stage for encrypted discussions.However, Farcaster, launched at the end of 2023, has achieved significant success. Before Paradigm’s $ 1 billion in Series A financing led by Paradigm, it raised a daily active user of nearly 40,000 daily active users.

Ecosystem contribution

Ethereum and the recent expansion solutions are still the main centers of specific investment in ecosystems. Although their dominant positions are declining year by year, the emerging ecosystems provide a large number of opportunities in mature and established environments.

>

Most of the traffic is concentrated in Ethereum, Bitcoin and Solana, while other blockchains are competing hard.The status of Solana has improved in the past year, and has witnessed the influx of unique and active addresses, huge trading volume, and the popularization of their virtual machines.The situation of Bitcoin is not the case, because it failed to maintain momentum and surpassed by Solana, partly because it focused on the mining business.Nevertheless, the Bitcoin ecosystem is developing rapidly and is still in its infancy.

in conclusion

Although the price trend of Bitcoin is good and institutional investors have also participated in high degree, the cumulative raising funds are unexpectedly low, which is slightly improved than last year.The activity once increased, but after that, it fell below the average, reflecting the seasonal model.So far, the market’s emotions are relatively passive, and risk investment has remained cautious.There are four months before the Year of the Snake. Bitcoin has enough time to establish a range and show a clear direction.The upward breakthrough, coupled with the cottage coins can finally make more safely, it should turn on the green light for participating in higher risks.