Introduction

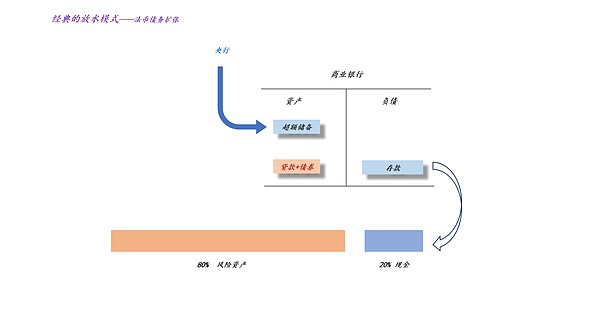

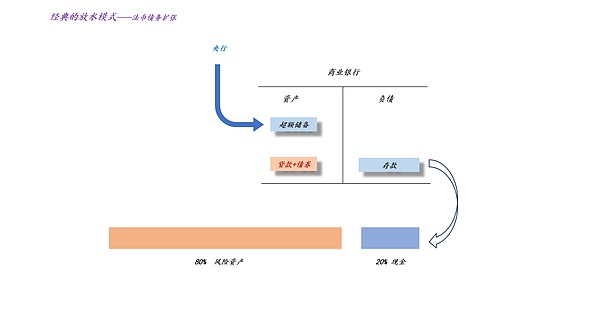

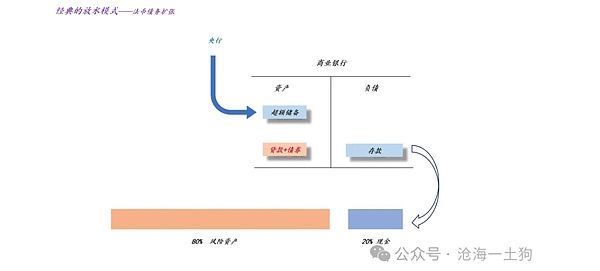

Generally speaking, the traditional monetary and banking theory is a set ofFiat debt expansionIn the monetary and banking theory, the expansion of fiat currency debt is at the core of everything.

As shown in the figure above, under this system, on the one hand, the central bank expands excess reserves; on the other hand, commercial banks expand credit, and the scale of legal currency debt such as loans and bonds expands.Eventually, we will observe an expansion of deposits and an inflation of risk asset prices (ps: Assuming that risk preference remains unchanged, that is, the cash/risk asset ratio of residents’ willingness).

This theory is so classic that most people use this framework to analyze problems.Therefore, there are two undoubted reasonings:

1. The Federal Reserve expands its balance sheet to stimulate risky asset prices;

2. The Federal Reserve cuts interest rates to stimulate risk asset prices.

However, this theory is too old and even a little out of date with the development of the times.For example, this theory relies strongly onFiat debt expansion.However, in the real world, there are two counterexamples,1. Cross-border capital flows; 2. The substitution of gold and other assets for legal currency.

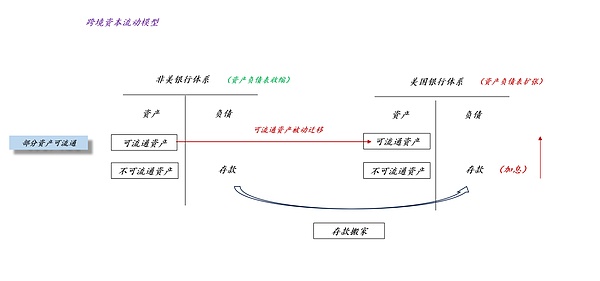

Cross-border capital flow effects

As shown in the figure above, we can regard the U.S. system and the non-U.S. system as two commercial banks. The flow of stock currency strongly depends on the interest difference between the U.S. system and the non-U.S. system.

Obviously,If interest rates in the U.S. system are higher than those in non-U.S. systems, deposits will tend to move to the U.S. system.

Therefore, we have found a pair of contradictions. If the money supply depends on incremental legal currency debt, then low interest rates are conducive to increasing the money supply; if the money supply depends on the cross-border flow of stock currency, then high interest rates are conducive to the money supply.

Therefore, we need to clarify a prerequisite:

Is it the impact of incremental debt that is greater, or the impact of cross-border capital flows?

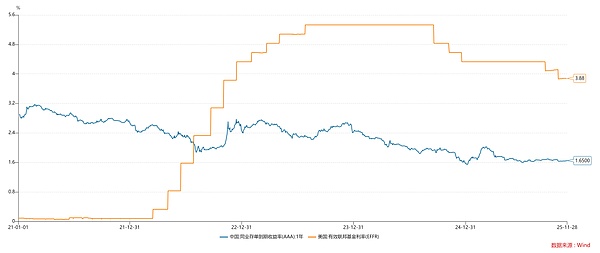

Obviously, the traditional model implicitly assumes that the impact of cross-border capital flows is weak.So why was this assumption reliable in the past?Because, most ofThe central bank will keep pace with the Fed, however, this assumption is now invalid.

As shown in the chart above, the Federal Reserve has raised interest rates rapidly since 2022, but China’s policy interest rates have always remained low.Therefore,The monetary policies of China and the United States are misaligned.

According to traditional monetary and banking theories, U.S. stocks should go into a bear market and A-shares should go into a bull market.However, the result is exactly the opposite.This shows thatCross-border capital flow effects are major, the stimulation of low interest rates to the expansion of fiat currency debt is secondary.

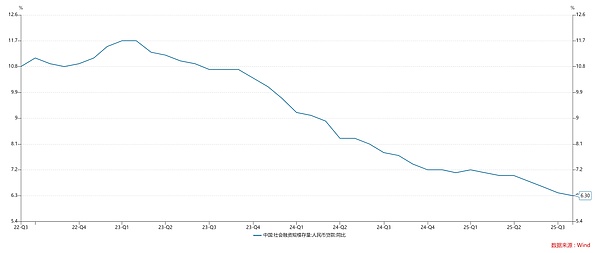

As shown in the chart above, China’s credit growth rate continues to decline during this period. Many people attribute this phenomenon to the real estate bear market.However, the real problem for most people is thatThey have reversed the relationship between policy interest rates and housing prices..

The substitution effect of safe-haven assets

Previously we discussed in the article,The development of modern financial instruments has caused changes in the form of money supply.

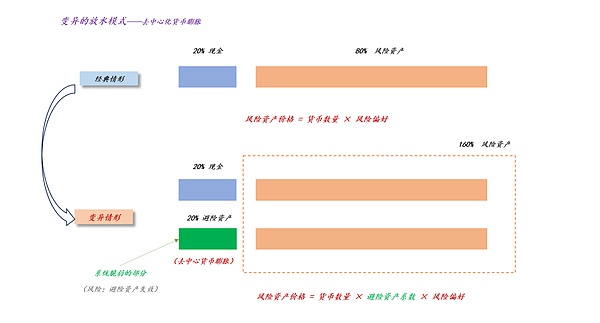

The popularity of all-weather strategies essentially based on “shorting cash” has made safe-haven assets such as gold, gold contracts, BTC, and BTC contracts increasingly substitute for cash.As a result, the pricing formula for risky assets has changed:

Traditional: Risk asset price = cash size × risk preference;

Modern: Risk asset price = cash size × safe-haven asset coefficient × risk preference.

It is not difficult to find that under the modern money supply system, “safe haven assets” occupy a core position. They can completely bypass the constraints of “cash scale” – the constraints of the Federal Reserve, and inflate the prices of risky assets by increasing the coefficient of safe haven assets.

Currently, the global M2 is on the order of 123 trillion U.S. dollars, and the market value of gold is on the order of 30 trillion U.S. dollars. Therefore, the expansion of gold prices will indeed significantly change the global currency supply mechanism.

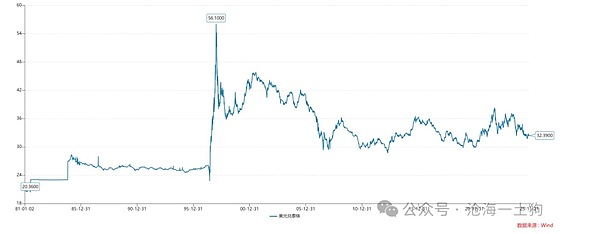

As shown in the chart above, the price of London gold at the beginning of 2024 was less than $2,000, and has now soared to $4,200.

In other words, the market value of gold has almost expanded by US$15 trillion in the past year.

What is this concept?The Federal Reserve spent more than two years engaging in QT and reduced its balance sheet by US$2.4 trillion. As a result, gold’s market value expanded by US$15 trillion in one year.Therefore, the modern money supply system has undergone earth-shaking changes.

Gold’s “thrifty” expansion mechanism

Under the traditional model, the increase in fiat currency depends on the increase in fiat currency debt:

In fact, it is a very expensive form of money supply, with lenders constantly paying high interest rates.

So, is there a cheaper way to supply money??Yes, that is decentralized currency.

Under the new model, the expansion of decentralized currency does not depend on the expansion of legal currency debt, but only on the expansion of decentralized currency prices.

This is a very clever way of expansion. There is no increase in legal currency debt, only a change in the concentration of gold holdings.

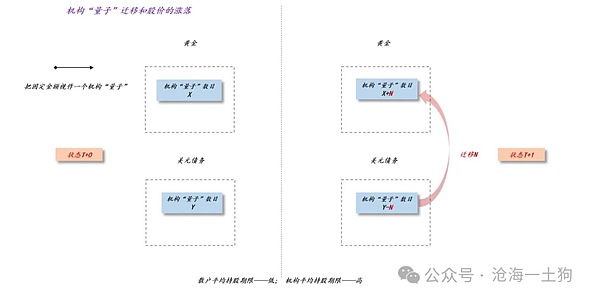

In previous articles, we discussed the underlying principle: the average holding period of institutions is longer than that of retail investors. Therefore, the grouping behavior of institutions will significantly push up the stock price.

Symmetrically, we can transfer this logic to gold. The average holding period of central banks is greater than that of financial institutions, and financial institutions are greater than individuals.Therefore, the central bank’s selling of U.S. dollar debt in exchange for gold will significantly push up the price of gold.

Theoretically, there is no limit to the rise in gold prices caused by this central bank grouping. As long as there is a reason for global central banks to continue to increase gold reserves, the price of gold will become higher and higher.(ps: We must get rid of the illusion here that the price of gold is not bought by retail investors, but by central banks and large financial institutions)

It is not difficult to find that as long as there is an attractor that causes central banks of various countries to unite with gold, then the “gold price increase” will become a new source of money supply, competing with the Federal Reserve and the US government for global coinage rights.

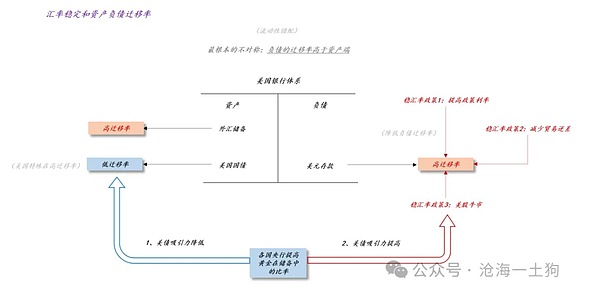

A new way to stabilize the dollar exchange rate

So, has the behavior of central banks around the world harmed the U.S. dollar??On the surface, it will indeed cause the dollar to depreciate. After all, central banks have switched their reserves from U.S. bonds to gold.However, according to the pricing formula of risky assets, the expansion of gold’s market value will lead to an increase in the “safe haven asset coefficient”, which will strongly support the rise of U.S. stocks. Ultimately, the U.S. dollar will strengthen due to this mechanism.

As shown in the figure above, for any economy, the essence of the exchange rate problem is that the migration rate on the liability side is higher than the asset side.Specifically, local currency deposits are easier to convert into foreign currency deposits, but local currency government bonds do not have such high cross-border liquidity, so the country has to rely on foreign exchange reserves to smooth out the difference.

However, the rapidly rising U.S. government debt has changed this situation. Central banks have increased their gold reserve ratios, and the cross-border migration rate of U.S. debt has declined. Ultimately, the special nature of the U.S. dollar has declined.

On the surface, this is a dead end. The United States can only perform a financial tightening to restore international investors’ trust in U.S. debt.However, Wall Street elites thought of a more ingenious way.Following the wave of central banks increasing their holdings of gold, the price of gold is further pushed up.So there is a situation of “lost in the east, gained in the elm”——Although the attractiveness of U.S. bonds has declined, the attractiveness of U.S. stocks has increased.In other words, although central banks of various countries have replaced U.S. debt with gold, causing the U.S. dollar to depreciate, the liquidity released by rising gold prices has boosted the rise of U.S. stocks, guided the inflow of foreign capital, and stimulated the appreciation of the U.S. dollar.

The U.S. government likes to see safe-haven asset prices rise and inject cheap money into the system.

Overall, throughout the process, the dollar’s support pillars have shifted, from U.S. bonds to U.S. stocks, and from central banks to international investors.The rise in prices of safe-haven assets such as gold has played a vital mediating role.

So, what is the practical significance of this conversion??When the U.S. stock market enters a bear market, international investors will once again regard U.S. debt as a piece of cake..In other words, this conversion is beneficial to the US government debt.

The art of resolving debt

To sum up, we will find that we should not be imprisoned by the specific form of currency, but we should directly examine the final results of monetary expansion——Inflation in risky asset prices.That is to say,As long as risk asset prices are rising, we consider money to be expansionary;As long as the price of risky assets is falling, we believe that the currency is contracting.Through this “ideological emancipation”, we will not be bound by the traditional blind methods of “raising interest rates” and “cutting interest rates”.

Through inspection ““With this formula, we will find that the actual supply mechanism of money is more complicated than we imagined:

1. Monetary expansion can come from the expansion of fiat currency debt or cross-border capital flows caused by interest rate increases;

2. The rapid expansion of safe-haven assets such as gold will also drive the price expansion of risky assets.

So, we have three tools to stimulate the rise of risk assets:1. Expansion of legal currency debt; 2. Increase in domestic policy interest rates; 3. Increase in gold prices.

Obviously, fiat currency debt is the most expensive, requiring the country’s government, enterprises and residents to shoulder long-term debt; domestic policy interest rate hikes are second, because the overall debt maturity is relatively short; gold price increases are the cheapest, which is a pure form of stimulus that only requires the central banks of various countries to unite.

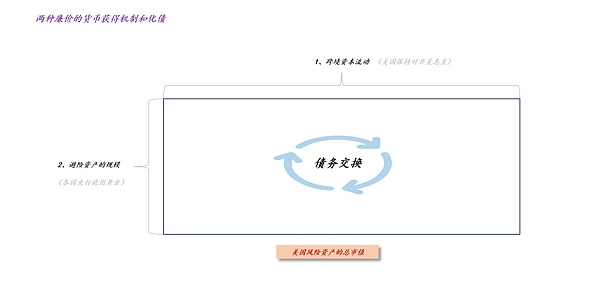

As shown in the figure above, through the cost difference of the three instruments – “fiat currency debt > interest rate increase > gold price increase”, we can get aDebt-resolving magic——Promote the rise of risk assets through interest rate increases and the expansion of safe-haven assets. In the process of rising risk assets, we have completed the process with overseas investors.debt exchange.

When the tide recedes, some overseas investors are locked in expensive legal currency debt. The tragic experiences of these unlucky people will serve as a warning to other investors.Let them re-examine the value of long-term U.S. debt.

Conclusion

Finally, we will draw the following basic conclusions, which are not so much counter-intuitive as they are counter to the “classical monetary and banking model”:

1. The Federal Reserve’s interest rate cuts are detrimental to U.S. stocks. As the federal funds rate continues to decrease, funds will eventually flow back to Africa on a large scale;

2. The rising price of gold is beneficial to U.S. stocks. It is expanding the coefficient of safe-haven assets and hedging against the negative impact of the Federal Reserve’s interest rate cuts;

3. When the ten-year U.S. bond interest rate and the price of gold fall together, it is the most dangerous time for the U.S. stock market. At this time, the original flow of funds is reversed, and the entire system faces huge chaos;

4. The end result of everything is that the ten-year U.S. bond interest rate and the federal funds rate fall together, and finally, the U.S. debt crisis is resolved;

5. When the tide goes out, we will know who is swimming naked, but we need to study the tide thoroughly;

6. On the surface, Powell is a hawk, but in fact he is a dove. On the surface, Trump is a dove, but in fact he is a hawk;

7. The biggest expected difference in 2026 will be the new FOMC, which can no longer be dovetailed. In the name of a dove, an eagle does what it does;

8. Powell will be missed.