原标题:Ethena – Synthetic USD Challenges Stablecoin Duopoly

Source: Multicoin Capital; Compiled by: Bitcoin Vision

We are proud to announce that Multicoin Capital’s liquid fund has invested in the ENA token – ENA is the native token of the Ethena protocol, the issuer of USDe, the leading synthetic U.S. dollar stablecoin.

In our article “The Endgame of Stablecoins,” we pointed out that stablecoins are the largest potential market in crypto, and that revenue is their ultimate competitive frontier.While we were right about the direction yield stablecoins were heading, we underestimated the size of the market for synthetic dollars.

We divide the stablecoin category into two categories:

– Stablecoin to share revenue

– Stablecoin that does not share revenue

Among them, revenue-sharing stablecoins can be further subdivided into:

– A stable currency fully backed by government bond assets at a ratio of 1:1

– Stablecoin that is not fully backed by Treasury bonds, i.e. synthetic USD

The synthetic U.S. dollar is not fully supported by government-backed treasury bond assets, but achieves income generation and price stability by executing a delta-neutral trading strategy in the financial market.

Ethena is a decentralized protocol and the largest operator of the synthetic U.S. dollar USDe.

Ethena aims to provide an alternative stablecoin option to traditional stablecoins such as USDC and USDT – the reserve assets of these traditional stablecoins can only obtain the income of short-term US Treasury bonds.Ethena’s USDe reserve achieves income generation and target stability through basis trading, one of the largest and most proven strategies in traditional finance.

Basis trading in U.S. Treasury futures alone amounts to hundreds of billions (and possibly trillions) of dollars.Today, only accredited investors and institutional buyers have access to hedge funds with large-scale infrastructure for executing basis trades.Cryptocurrencies are completely restructuring the financial system and making such investment opportunities available to everyone through tokenization.

Our team has been looking at synthetic dollar projects based on basis trading for several years.Back in 2021, we published an article explaining this market opportunity and announced an investment in the UXD protocol – the first token fully backed by basis trading.

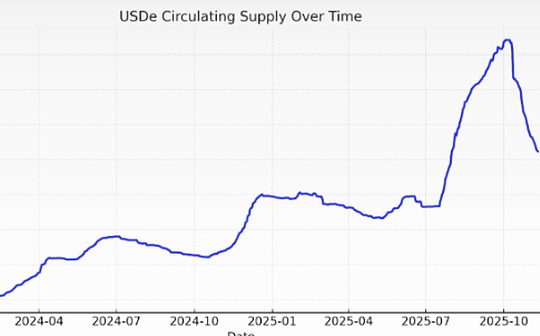

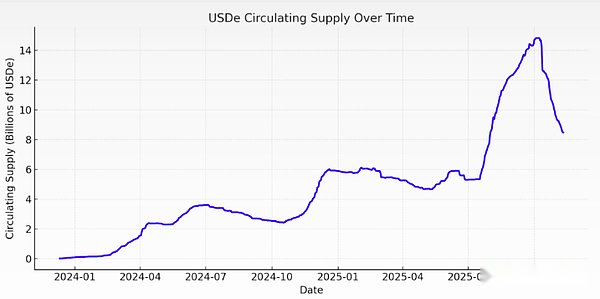

While the idea of the UXD Protocol was ahead of its time, in our opinion Guy Young, founder and CEO of Ethena Labs, has done an excellent job of realizing this vision.Today, Ethena has become the largest issuer of synthetic U.S. dollars: within two years of its launch, the circulation volume increased to 15 billion U.S. dollars, and after the market crash on October 11, it fell back to approximately 8 billion U.S. dollars. It is still the third largest digital U.S. dollar stablecoin after USDC and USDT.

Changes in USDe circulation (data source: DefiLlama)

Systemic benefits of synthetic dollars

Ethena sits at the intersection of three powerful trends that are reshaping modern finance: stablecoins, perpification, and asset tokenization.

稳定币

The total stablecoin circulation currently exceeds US$300 billion and is expected to grow to trillions of US dollars by the end of this decade.USDT and USDC have dominated the stablecoin market for nearly a decade, accounting for more than 80% of the total supply.Neither stablecoin shares revenue directly with holders, but we believe that over time, sharing revenue with users will become the industry norm rather than the exception.

In our view, the competition and differentiation of stablecoins are mainly reflected in three core dimensions: distribution capabilities, liquidity and income levels.

Tether has built a superior liquidity and global distribution network for USDT, which is the primary denominated asset in cryptocurrency trading and the most widespread way for users in emerging markets to obtain digital dollars.

Circle expands distribution channels by sharing economic benefits with partners such as Coinbase. This strategy has effectively promoted growth, but it has also put pressure on Circle’s profit margins.As cryptocurrency adaptation accelerates, we expect more companies with extensive distribution networks in the financial and technology fields to issue their own stablecoins, further intensifying the homogeneous competition in the government bond-backed stablecoin market.

For new entrants to the digital dollar space, the primary way to stand out is by offering higher yields.The interest-bearing stablecoin narrative has been heating up over the past few years, but those backed by U.S. Treasuries have not offered high enough yields to drive mass adaptation in the crypto space.The reason is that the opportunity cost of capital for crypto-native users has historically been higher than U.S. Treasury yields.

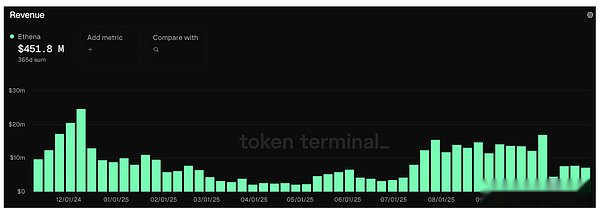

Of all the new entrants, Ethena is the only project to achieve significant distribution scale and liquidity, thanks in large part to its higher yield levels.Based on the price changes of sUSDe since its launch, we estimate that its annualized return is slightly more than 10%, which is more than twice that of Treasury-backed stablecoins.This achievement is due to its basis trading strategy – which achieves profits by taking advantage of the market’s demand for leverage.Since its launch, the protocol has generated nearly $600 million in revenue, over $450 million of which came from the past 12 months.

Data source: Token Terminal

We believe that the real test for the adaptation of synthetic dollars is whether they can be accepted as collateral assets by mainstream exchanges.Ethena has performed outstandingly in this regard and has successfully integrated USDe as one of the core mortgage assets of large centralized exchanges such as Binance and Bybit. This is also a key driver of its rapid growth.

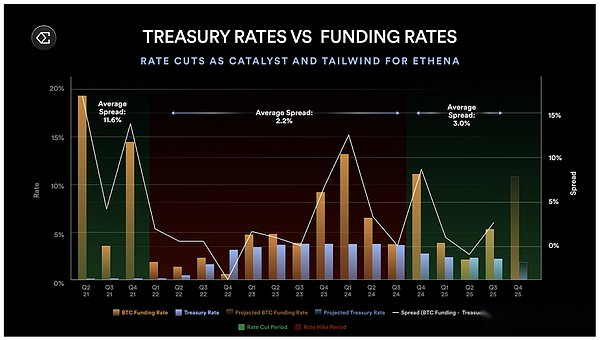

Another unique aspect of the Ethena strategy is its mild negative correlation with the federal funds rate.Unlike Treasury-backed stablecoins, Ethena is expected to benefit from falling interest rates – because low interest rates stimulate economic activity, increase demand for leverage, drive up funding rates, and strengthen the basis trade that supports Ethena’s earnings.A similar situation occurred in 2021, when the spread between the funding rate and the government bond interest rate widened to more than 10%.

Although as cryptocurrencies integrate with traditional financial markets, more money will flow into the same basis trade, causing the spread between the basis trade and the federal funds rate to narrow, but this integration process will take several years.

Data source: Bitcoin funding rate, Treasury bond interest rate

Finally, J.P. Morgan predicts that interest-bearing stablecoins may account for up to 50% of the stablecoin market in the next few years.With the total stablecoin market expected to soar into the trillions of dollars, we believe Ethena is well-positioned to become a major player in this transformation.

永续合约化

Perpetual futures have achieved strong product-market fit in the crypto space.In the crypto asset class with a scale of approximately US$4 trillion, the average daily trading volume of perpetual contracts exceeds US$100 billion, and the total open interest of centralized exchanges (CEX) and decentralized exchanges (DEX) exceeds US$100 billion.They provide investors with a simple way to gain leveraged exposure to the price movements of an underlying asset.We believe that more asset classes will adopt the form of perpetual contracts in the future, which is what we call “perpetualization”.

A common question regarding Ethena is its addressable market size – as the size of its strategy is limited by the open interest in the perpetual contracts market.We agree that this is a reasonable constraint in the short term, but believe it underestimates the market opportunity in the medium to long term.

Perpetual Contracts for Tokenized Stocks

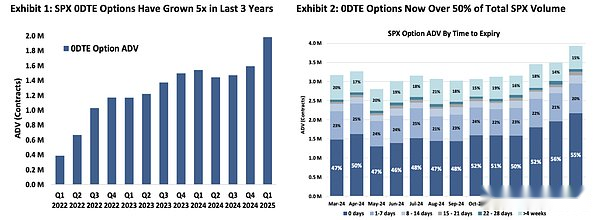

The global stock market is approximately US$100 trillion, almost 25 times the size of the entire crypto market, and the US stock market alone is US$60 trillion.Like the crypto market, there is a strong demand for leverage among stock market participants.This is evidenced by the explosive growth of zero-date-to-expiration (0DTE) options—which are primarily traded by retail investors and account for more than 50% of S&P 500 Index (SPX) options trading volume.Retail investors clearly want leveraged exposure to the price movements of underlying assets, and perpetual contracts on tokenized stocks can directly address this need.

Data source: Chicago Board Options Exchange/Cboe

For most investors, perpetual contracts are easier to understand than options.A product that provides 5x exposure to the underlying asset is far simpler than understanding the time value (theta), volatility value (vega) and delta value of options – the latter requires an in-depth understanding of option pricing models.We do not believe that perpetual contracts will replace the zero-expiry date option market, but they are expected to capture a significant market share.

As stock assets are tokenized, stock perpetual contracts are expected to unlock massive new opportunities for Ethena.We believe this will make Ethena an important source of liquidity in the launch phase of new markets, which will benefit both centralized and decentralized exchanges; alternatively, Ethena can internalize this opportunity by launching its own brand of decentralized exchanges for stock perpetual contracts.Given the size of equity markets relative to crypto markets, these developments could expand the capacity of basis trading by orders of magnitude.

Fintech companies integrate new distribution channels brought by decentralized perpetual contract exchanges

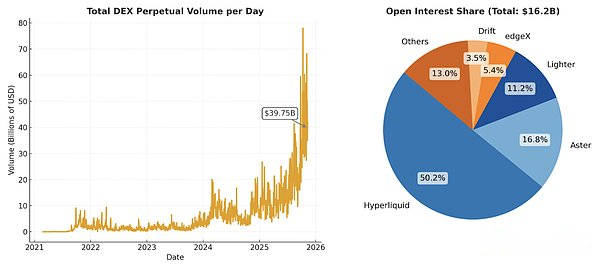

When we first proposed the idea of a decentralized digital dollar based on basis trading, decentralized derivatives exchanges were still in their early stages – illiquid and not yet ready for mainstream users.Since then, stablecoins have become mainstream and low-fee, high-throughput blockchains have been battle-tested.Today, the average daily trading volume of decentralized perpetual contracts on platforms such as Hyperliquid is approximately US$40 billion, with total open interest reaching US$15 billion.

数据来源:DefiLlama

As the regulatory environment for cryptocurrencies becomes more favorable, global fintech companies should increasingly embrace cryptocurrencies.Industry leaders such as Robinhood and Coinbase have gradually transformed into “universal exchanges.”Many of these companies have integrated decentralized finance (DeFi) middleware to support spot trading of long-tail assets on their platforms.

Today, most non-crypto native users only have access to limited crypto assets, and only in spot form.We believe this group represents a significant unmet need for leverage.As decentralized perpetual contract exchanges become mainstream, it is only natural that fintech companies will integrate these products directly.

For example, Phantom recently integrated with the decentralized perpetual contract exchange Hyperliquid, allowing users to trade perpetual contracts directly through the Phantom wallet. This integration has brought about US$30 million in annualized revenue.If you are the founder of a financial technology company, it is difficult not to want to follow up after seeing such results.For example, Robinhood recently announced its investment in decentralized perpetual contract exchange Lighter.

We believe that as fintech companies adopt crypto perpetual contracts, they will create new distribution channels for these products, driving trading volume and open interest growth, thereby expanding the capacity and scalability of basis trading underpinning Ethena.

Tokenization

The core advantage of cryptocurrencies is that anyone can issue and trade tokens seamlessly.Tokens can represent any valuable asset, from stablecoins and Layer 1 assets to memecoins and even tokenization strategies.

In traditional finance, the closest product to tokenization is exchange-traded funds (ETFs).Today, the number of ETFs on the U.S. market exceeds the number of publicly listed stocks.ETFs package complex strategies into a single tradable ticker that investors can easily buy, sell, or hold without having to worry about execution or rebalancing—all of this complexity is handled behind the scenes by the ETF issuer.Not surprisingly, the CEO of BlackRock, the world’s largest ETF issuer, appears to be all-in on tokenization.

Tokenization goes far beyond ETFs—it makes holding and trading assets faster, cheaper, and more convenient (regardless of size), while also improving distribution and capital efficiency.Anyone with an internet connection can buy, sell, send or receive tokens instantly, and can even use them as collateral to unlock additional liquidity.We envision a future where global fintech companies become major distributors of tokenization strategies, bringing institutional-grade products directly to consumers around the world.

Ethena initially entered the market through tokenized basis trading, but it is well-positioned to diversify its revenue streams over time.In fact, it is already doing so today.When basis trading returns are low or negative, Ethena can transfer some of the collateral assets to another product in its ecosystem, USDtb, a stablecoin backed by BlackRock’s tokenized Treasury bond fund BUIDL, to maintain stability and optimize returns.

Be optimistic about the core logic of ENA

While we have laid out the long-term bullish logic for Ethena’s addressable market size, it is equally important to understand its team and protocol characteristics, especially in terms of risk management, value capture, and future growth opportunities.

team

“I quit my job to start Ethena just days after Luna collapsed, and built the team a few months after FTX went bankrupt.” – Guy Young, founder of Ethena

Based on our contacts, Guy has proven to be one of the sharpest and most strategically thinking practitioners in the decentralized finance (DeFi) space.He brings his experience investing across capital structures at Cerberus Capital Management to the crypto market, which is undergoing a phase of rapid financialization.

Guy’s success is supported by a lean but experienced team of approximately 25 operational staff.Just to name a few core members of the Ethena team: CTO Alex Nimmo is one of the early employees of BitMEX and has witnessed the company’s entire process of building perpetual futures into the most important financial instrument in the crypto field; COO Elliot Parker has worked for Paradigm Markets and Deribit, and his network resources in the field of market makers and exchanges have laid the foundation for Ethena’s current integration and cooperation with these counterparties.

The results speak for themselves.Ethena became the largest issuer of synthetic dollars in less than two years.During this time, the team moved quickly, achieving integrations with top centralized exchanges and establishing hedging channels that would take most projects years to acquire.Today, USDe has been accepted as a collateral asset by major platforms such as Binance and Bybit.Many of these exchanges are also investors in Ethena, indicating clear strategic synergies between the protocol and key players in the global crypto market.

risk management capabilities

My partners Spencer and Kyle published an article in 2021 titled “DeFi Protocols Don’t Capture Value, DAOs Manage Risk.”The core argument is simple: DeFi protocols that try to charge fees without managing risk will be forked because there will always be a forked version with zero fees.Agreements that essentially need to manage risk must charge fees, otherwise no one will provide risk coverage for the system.

Ethena is the perfect example of this principle.The protocol has demonstrated strong risk management capabilities and has successfully navigated two major stress events this year alone, each reinforcing its credibility, resilience and brand trust within the crypto ecosystem.

Bybit Hack: The Largest Hack in Crypto History

On February 21, 2025, Bybit suffered a $1.4 billion hot wallet hack, which became a real-world stress test for the Ethena exchange’s counterparty model.The incident triggered a massive wave of user withdrawals from Bybit, but Ethena’s strategy was not affected in any way.

With hedging positions and collateral assets dispersed across multiple platforms and secured by off-chain custodians, Ethena maintained normal operations throughout the incident.Importantly, Ethena did not lose any collateral assets and the minting and redemption processes associated with Bybit were not disrupted.

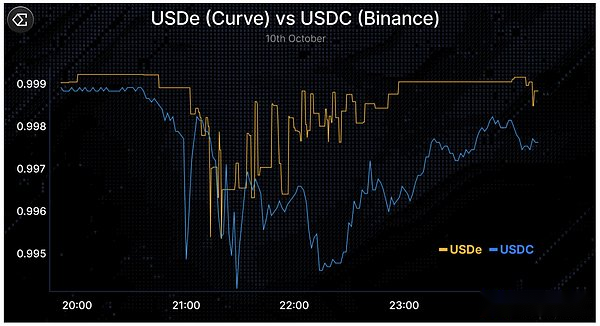

The October 11 Selloff: The Biggest Single-Day Liquidation Event in Crypto History

On October 11, 2025, the crypto market experienced an extreme deleveraging event—approximately $20 billion in positions were liquidated within a few hours, and the open interest volume of major centralized exchanges and decentralized exchanges shrank significantly.In the process, the trading price of USDe on Binance fell to about $0.65 due to the design of Binance’s oracle machine (which was later criticized).However, on more liquid on-chain platforms such as Curve, the price of USDe remains close to parity (see chart below) and the redemption function is functioning normally – suggesting that this is a price dislocation on a specific platform rather than a systemic de-anchoring.Guy’s tweet on the X platform explains the events of October 11 in detail and is worth reading.

Data source: X platform

In both incidents, the Ethena team communicated transparently and no user funds were lost.Meanwhile, the protocol continued to operate normally, processing billions of dollars in redemption requests within hours, with all transactions verifiable on-chain.Moments like this test the risk discipline of any agreement.Successfully responding to such stressful events at scale not only strengthens trust and credibility, but also builds brand equity and competitive barriers – building a strong moat for DeFi protocols like Ethena.

To be clear, there is reason to expect that the Ethena protocol will face more stress tests in the coming years.We are not arguing that the risk does not exist or has been completely eliminated, but we would like to emphasize that Ethena has demonstrated strong performance and resilience during some of the most significant market stress events in recent times.

value capture potential

We believe that Ethena has the ability to charge higher rates compared to stablecoins such as USDC.Unlike USDC, Ethena actively manages market risk, provides users with higher yields in most cases, and is likely to be negatively correlated with interest rates in the near to medium term—all factors that enhance its ability to capture and sustain long-term value.

Although the ENA token currently functions primarily as a governance token, we believe there is a clear path for it to accumulate value.Ethena generated approximately $450 million in revenue over the past year, none of which is currently distributed to ENA token holders.

A rate switching proposal put forward in November 2024 outlines several milestones that need to be achieved before ENA holders can receive distributions of value.All of these conditions were met before the crash on October 11.The only indicator that is currently not up to standard is the circulating supply of USDe – we estimate that the circulating supply of USDe will exceed $10 billion before the rate switch is initiated.Implementation details of the rate switch are currently being reviewed by the Risk Committee and the community.

Our assessment is that these developments will likely be viewed positively by the public market, as they will enhance Ethena’s governance synergy, expand the long-term holder base, and reduce selling pressure on the token.

long term growth potential

Based on its existing business alone, Ethena is already one of the highest-grossing protocols in the crypto space.

Ethena is leveraging its leading position to launch multiple new product lines based on its core strengths of stablecoin issuance and crypto perpetual contract exchange expertise.These product lines include:

-

Ethena Whitelabel: A “stablecoin-as-a-service” solution, Ethena customizes stablecoins for large blockchains and applications.Currently, Ethena has reached white label cooperation with megaETH, Jupiter, Sui (through SUIG), etc.

-

HyENA and Ethereal: Two third-party perpetual contract decentralized exchanges built on USDe mortgage assets, which not only promote the expansion of USDe’s application scenarios, but also bring transaction fee income to the Ethena ecosystem.Both projects are developed by external teams but directly create value for Ethena.

These potential product lines will further solidify Ethena’s leading position in the field of synthetic dollars.

With all new product lines built on Ethena, Ethena is expected to reap financial benefits from these initiatives, complementing its already strong revenue.

Why we like Ethena long-term

In a stablecoin market long dominated by USDT and Circle, Ethena has carved out a unique niche and become the clear market leader in the synthetic USD category.

As the number of stablecoins proliferates, traditional assets tokenize, and perpetual contract decentralized exchanges rise, we believe Ethena is uniquely positioned to fully capitalize on these trends – transforming global demand for leverage into attractive and accessible yields for users and global fintech companies.

The protocol’s strong risk management culture has withstood real-world stress testing and continues to succeed, helping Ethena build deep trust and credibility among its users and partners.

Over the long term, Ethena can leverage its scale, brand and infrastructure to expand into other product areas, diversify revenue and increase its ability to withstand market shocks.

As the issuer of the fastest-growing synthetic USD in the fastest-growing stablecoin category (Yield Stablecoins), Ethena is perfectly positioned to incubate new lines of business that will bring additional growth to the most profitable businesses in cryptocurrencies, exchanges, and deposit and withdrawal lanes, while increasing the supply of USDe.

The opportunities ahead are huge, and as long-term ENA token holders, we are very excited.