Note: Everyone has always said that they are stablecoins recently. Bitchain Vision has previously summarized the discussions on stablecoins from government leaders, entrepreneurs, economists, national think tanks, securities firms and other Chinese people, see “How will China deal with the shock wave of US dollar stablecoin”.

On May 19, Morgan Stanley China chief economist Xing Ziqiang also led the research report “Stablecoins and RMB internationalization?”.Let’s take a look at how foreign securities firms view stablecoins and their impact on the internationalization of RMB.

The full text is as follows:

We believe China’s recent new interest in stablecoins is due to concerns that U.S. stablecoin legislation could expand the dominance of the dollar.The People’s Bank of China is using Hong Kong as a test site for future payment alternatives.But tokenization alone cannot make the RMB international, the real work lies in domestic reform.

Why is Beijing paying attention to stablecoins now?

The U.S. Senate passed the GENIUS bill, which requires that the dollar stablecoins must be fully supported, marking a turning point.If the bill passes in the House, it will essentially transform the stablecoins anchored by the dollar (currently 99% of the stablecoin market) into synthetic dollars and deeply embed them into the global payment system, thereby increasing demand for U.S. Treasury bonds.

In our opinion, this is not a challenge to the dominance of the US dollar—but a further strengthening of the dominance of the US dollar.Stable coins are not new currencies, but new distribution channels for existing currencies.They expand the dollar’s influence to cryptocurrencies, Web3 and emerging markets through low-cost, almost instant settlement.

For China, ignoring this trend is likely to lag behind the competition for digital infrastructure, especially as stablecoins increasingly serve as bypassing traditional banking network mechanisms.

The turn of the People’s Bank of China – from ban to blueprint

Cryptocurrency trading has been deemed illegal in mainland China since September 2021 due to regulators’ concerns about financial stability risks.But the speech of the central bank governor Pan Gongsheng at the Lujiazui Forum this week sent a signal of a policy shift: he called for the construction of a multipolar global monetary system and promised to ensure the security of international transactions.With the improvement of efficiency and the maturity of technology, digital RMB and stablecoins have been proposed as feasible alternatives to cross-border settlement.President Pan specifically pointed out that digital technology exposes the weaknesses of traditional cross-border payment systems, which are inefficient and vulnerable to geopolitical risks.

RMB stablecoin—Prospects and constraints

At present, the settlement of cross-border digital RMB mainly relies on the M Bridge project, a multi-central bank digital currency platform developed by the Bank for International Settlements (BIS).However, the project is still small, with only five central banks participating, and the Bank for International Settlements withdrew in October 2024, which may slow down the expansion in the future.In theory, the RMB stablecoin has the characteristics of decentralization, easy access and high efficiency, and is a good supplement to cross-border transactions.However, domestic bans, capital controls remain, and lack of global recognition under the dominance of the US dollar stablecoin, all these factors limit the development of the RMB stablecoin.

Hong Kong – Strategic “sandbox”

Hong Kong is the first jurisdiction in the world to pass stablecoin legislation, and the law will take effect from August 1.The Stable Coin Act requires stablecoins to be supported by 100% high-quality reserves and are pegged to the corresponding currencies (whether it is the US dollar, Hong Kong dollar or offshore RMB) – which actually paves the first legal path for offshore RMB stablecoins.Under the legislation, Hong Kong will first promote stablecoins pegged to the US dollar and Hong Kong dollars to build technology and market trust, and then promote stablecoins pegged to the offshore RMB.Relying on Hong Kong’s deep offshore RMB liquidity pool (about 1 trillion yuan), offshore RMB stablecoins will provide verification for the practical application scenarios of cross-border settlement without violating mainland capital controls or affecting onshore financial stability.The increase in offshore RMB use will also drive demand for RMB assets (such as offshore RMB treasury bonds and central bills).

Stablecoins are tools, not strategies

It should be clear that the rise of stablecoins does not mean the establishment of a new “super sovereign” international monetary system.In fact, stablecoins are just an extension of fiat currencies under existing regulations to promote cross-border transactions.In this sense, we believe that the development of RMB stablecoin should be regarded as a potential component of China’s cross-border RMB settlement infrastructure, which also includes the RMB swap protocol, the RMB cross-border payment system (CIPS), and the global RMB clearing service network.

Infrastructure construction is not all, the internationalization of the RMB is still a protracted war

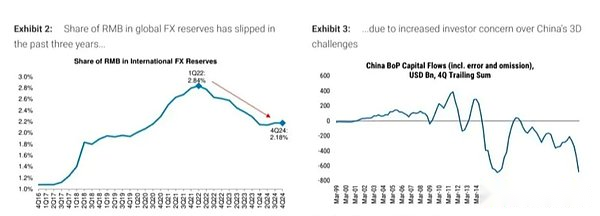

Although Beijing is accelerating the construction of cross-border settlement infrastructure, the internationalization of the RMB has regressed in the past three years. By the end of 2024, the RMB’s share in global reserve currencies has dropped from 2.8% at the beginning of 2022 to 2.2%.This is mainly because the market is concerned that China’s “three-D challenges” (debt, deflation, and demographics) have caused weakening capital flows, offsetting the growth in the use of the RMB in trade.

This means that the key to enhancing the global use of the RMB lies in global confidence in China’s economic growth potential.To this end, we believe decisive structural measures are needed to achieve economic rebalancing and break the deflation cycle through consumption pull, including social welfare reform, debt restructuring, tax reform and a regulatory environment that promotes growth.All of these are difficult reforms and can only be promoted step by step (see “Is China Rebalancing?” on May 28, 2025), which means that the road to internationalization of the RMB may be long and full of twists and turns.