War. War Never Change.

The direct triggers of the 10·11 and 11·3 events were not income-generating stablecoins, but they hit USDe and xUSD one after another in a dramatic manner. Aave’s hard-coded USDe anchored to USDT prevented the Binance on-site crisis from spreading to the chain, and Ethena’s own minting/redemption mechanism was not affected.

However, the same hard coding caused xUSD to fail to die directly and fell into a long garbage time. The bad debts of the issuer Stream could not be cleared in time. The related party Elixir and its YBS (yield stable currency) product deUSD were also questioned.

In addition, multiple Curators (I translate it as managers) on Euler and Morpho accept xUSD assets, and user assets are randomly exploded in various Vaults. Without the emergency response role of the Federal Reserve in SVB, there is a possible liquidity crisis.

Let the single-point crisis amplify into industry shocks, when xUSD crosses over the sinking managers and goes to war for eternity.

Manager + leverage, the source of crisis?

It is not a crisis caused by leverage. Private exchanges between protocols lead to opaque information and lower the psychological defense threshold of users.

When a crisis breaks out, the following two points of understanding form the basis for the division of responsible subjects:

-

1. The management teams of Stream and Elixir are the main culprits in the insufficient issuance of xUSD from the leverage cycle;

-

2. Curated Markets (selected markets) of lending platforms such as Euler/Morpho accept the “toxic asset” xUSD, and the platform and the manager should bear joint and several liability;

Let’s reserve our opinions first and look at the operating mechanism of YBS. Compared with the operating logic of USDT/USDC, that is, U.S. dollars (including U.S. debt) are deposited in banks, Tether/Circle mints stable coins of equal amounts, Tether/Circle earns deposit interest or treasury bonds, and the usage of stable coins reversely supports Tether/Circle’s profit margin.

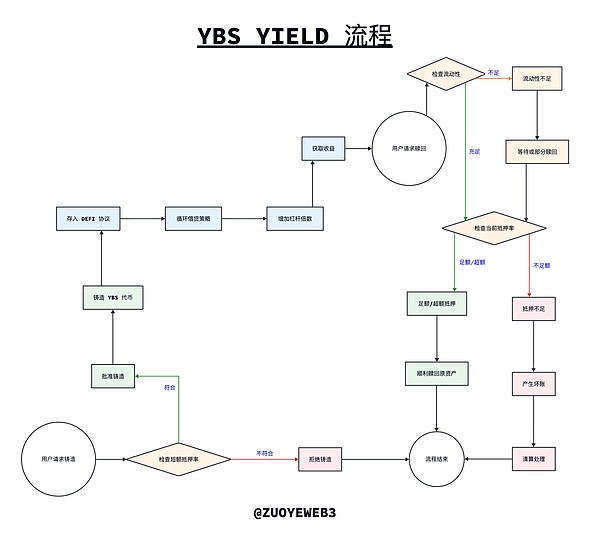

The operating logic of YBS is slightly different. In theory, it will adopt an over-collateralization mechanism, that is, it will issue 1 US dollar of stable currency for more than 1 US dollar of collateral, and then put it into the DeFi protocol. After the income is distributed to the holders, what is left is its own profit, which is the essence of its income.

Image Caption: YBS Minting, Yield and Redemption Process

Image source: @zuoyeweb3

Theory is not reality. Under the pressure of high interest rates, the YBS project side developed three “cheating” methods to improve its profitability:

1. Converting the over-collateralization mechanism to under-collateralization and directly reducing the value of the collateral is stupid and basically ineffective, but the corresponding strategies are also evolving:

-

“Expensive” and “cheap” assets are mixed to support it. US dollar cash (including US debt) is the safest, and BTC/ETH is also relatively safe. However, TRX is also supporting USDD, and its value will be discounted;

-

On-chain/off-chain asset mixed support is not a bug, it is a kind of time arbitrage. Just ensure that the assets are in the corresponding position during the audit. Most YBS will adopt such a mechanism, so I will not give a separate example.

2. Enhance leverage capabilities. After YBS is minted, it will be put into DeFi protocols, mainly various lending platforms, and it is best to mix it with mainstream assets such as USDC/ETH:

-

If you magnify the leverage to the extreme, and use 1 US dollar as 100 US dollars, the greater the profit you can obtain, such as the revolving loan combined by Ethena and Aave/Pendle. The most conservative cycle of 5 times can achieve almost 4.6x Supply leverage, and 3.6x Borrow leverage.

-

Use fewer assets to leverage. For example, Curve’s Yield Basis once planned to directly issue additional crvUSD, which actually reduced the amount of capital used for leverage.

So, xUSD performed a set of combos,Leverage in front, cyclical issuance, which is the version mechanism of xUSD. As you can see from the picture above, YBS will enter the income “strategy” after minting, which is essentially a process of increasing leverage. However, xUSD and deUSD cooperate with each other to migrate it to the issuance process, so users can see both the over-collateralization rate and the income strategy. However, this is completely a cover-up of Stream. Stream acts as both a referee and an athlete, making xUSD an under-capitalized YBS.

xUSD uses the leverage of the second step to issue additional shares in the first step, relying on Elixir’s deUSD to leverage about 4 times the leverage, which is not a big deal at all. The problem is that 60% of the circulation is controlled by Stream itself. When making money, the profit will be kept for itself, and when there is a thunderstorm, the bad debts will also be for itself.The most important part of the liquidation mechanism, the socialization of losses, cannot be achieved.

The question is why do Stream and Elixir do this?

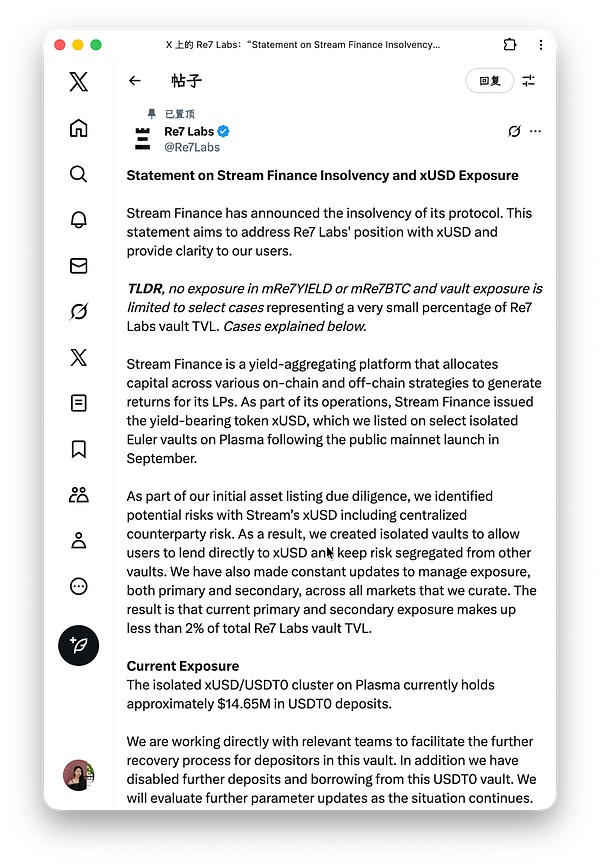

In fact, direct blending between protocols is no longer news. When Ethena introduces CEX capital, it also has partial immunity from ADL liquidation. Returning to xUSD, among the responses from many vault managers, Re7 is the most interesting.“We recognized the risk, but due to strong user requests, we still put it on the shelves.”

Image caption: Re7 response

Image source: @Re7Labs

In fact, treasury managers on platforms such as Euler/Morpho can definitely identify the problems of YBS, but under the demand for APY and profit, some people will actively or passively accept it. Stream does not need to convince all managers and is not rejected by everyone.

These managers who accept xUSD must have a responsibility, but this is a process of survival of the fittest. Aave is not developed in a day, but continues to grow into Aave in crises. If only Aave is used, will the market be safer?

Actually not,If Aave existed as a lending platform in the market, then Aave would become the only source of systemic crisis.

Platforms such as Euler/Morpho are a decentralized market or “New Third Board” mechanism, with more flexible allocation strategies and lower entry barriers, which are of great significance to the popularization of DeFi.

But the problem is still opaque. The Curator of Euler/Morpho essentially allows third-party sellers to exist, while Aave/Fluid is completely self-operated by JD.com, so when interacting with Aave, Aave is responsible for security. However, part of Euler’s treasury is the responsibility of the Curator, and the platform intentionally or unintentionally blurs this point.

In other words, platforms such as Euler/Morpho reduce users’ defense and due diligence expectations. If the platform adopts a friendly fork similar to Aave or HL’s liquidity backend aggregation, while maintaining absolute separation between the front end and the brand, it will suffer much less criticism.

How should retail investors protect themselves?

The end point of every DeFi dream is to press the doorbell of retail investors.

As the main public chain of DeFi, Vitalik is not that fond of DeFi and has long called for non-financial innovation to occur on Ethereum. However, he sincerely benefits retail investors. Since DeFi cannot be eliminated, he has begun to call for Low Risk DeFi to empower the poor around the world.

Image caption: DeFi and the real world through Vitalik’s eyes

Image source: @zuoyeweb3

Unfortunately, what he fantasized about has never been true, and people have long believed that DeFi is a high-risk and high-yield product. This is indeed the case in the 2020 DeFi Summer, with returns of more than 100% at every turn, but now 10% is suspected of being Ponzi.

The bad news is that there are no high returns, and the good news is that there are no high risks.

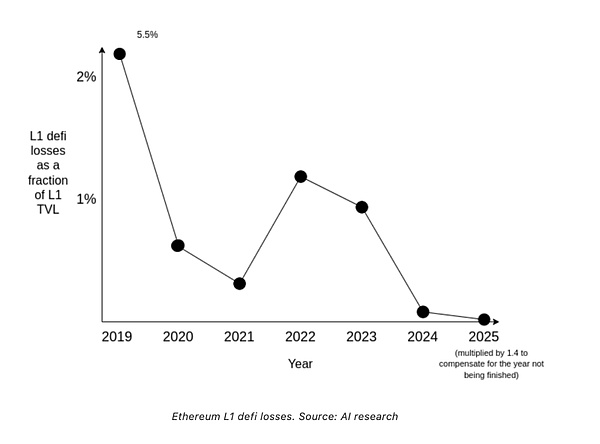

Image caption: Ethereum loss rate

Photo credit: @VitalikButerin

Whether it is the data given by Vitalik or the data of more professional research institutions, the security level of DeFi is indeed increasing. Compared with the 1011 Binance liquidation data and the huge theft of Bybit, the thunderstorms and losses of DeFi, especially YBS, are not worth mentioning.

But!I want to say again, but this does not mean that we should safely invest in DeFi.CEX is increasingly transparent, but DeFi is increasingly opaque.

The era of regulatory arbitrage on CEX has ended, but the era of relaxed regulation of DeFi has returned. This is of course beneficial, but in the name of DeFi, the centralization situation is becoming increasingly serious. There are too many clauses hidden between protocols and between managers that cannot be known to outsiders.

What we think of on-chain cooperation is code, but it is actually TG’s rebate ratio. This time, many xUSD managers released screenshots of TG, and their decisions will directly affect the future of retail investors.

It doesn’t make much sense to require supervision on them. The core is to combine the available modules from the chain. Don’t forget over-collateralization, PSM,x*y=kand Health Factor are enough to support DeFi’s macro activities.

In 2025, the Yield supported by the entire YBS is nothing more than the following:YBS assets, leveraged Yield strategy, lending agreement, not too numerous to count, such as Aave/Morpho/Euler/Fluid and Pendle meet 80% of interaction needs.

Opaque management leads to strategy failure. The manager does not demonstrate better strategy setting capabilities. The elimination process must occur after every problem.

Outside of this, what retail investors can do is penetrate everything, but frankly, this is not easy. Both xUSD and deUSD casting are theoretically over-collateralized, but the two are mixed together to advance the leverage process after casting to the casting stage, resulting in xUSD actually not being over-collateralized.

When YBS is minted based on another YBS, the mortgage rate after iteration is difficult to distinguish.

Before the advent of products that penetrate everything, retail investors can only rely on the following beliefs to protect themselves:

1. Systemic crisis is not a crisis (socialization). Participating in mainstream DeFi products is safe by default. Unsafe moments are unpredictable and unavoidable. If Aave has problems, it will see the decline or restart of DeFi;

2. Don’t rely on KOL/media. Participating in projects is a subjective choice (all judgments are our thoughts). News only reminds us that “this product is available”. Regardless of KOL reminders, warnings, orders, or DYOR exemptions, in the end, you need to make your own judgment. Professional traders should not even read the news, but only rely on data to make decisions;

3.The pursuit of high-yield products is not more dangerous than low-yield products. This is a counter-intuitive judgment. It can be viewed with Bayesian thinking. High-yield products are not explosive, and high-risk products are very small. Low-yield products are not explosive, but low-risk products are very high. However, we cannot quantify the ratio between the two, that is, the odds of winning (Odds). More generally speaking, the two are independent events.

Revise our beliefs with external data rather than seeking data to support our beliefs.

In addition, there is no need to worry too much about the market’s self-healing ability. It is not retail investors who will pursue volatility returns, but funds will seek liquidity. When all funds return to the Bitcoin standard or USDT/USDC standard, the market will automatically induce them to pursue volatility.That is, stability creates new volatility, and volatility crises trigger the pursuit of stability.

You can look at the history of the development of negative interest rates. Liquidity is the eternal beep of finance, and volatility and stability are two sides of the same coin.

Conclusion

Retail investors need to do two things in the next YBS market:

1. Seek data, penetrate all data, penetrate leverage ratios and reserves, transparent data will not deceive people, do not rely on opinions to evaluate facts;

2. Embrace the strategy, and the cycle of increasing leverage/deleveraging is endless. Simply reducing leverage cannot ensure safety. Always ensure that your strategy includes exit costs;

3. Control losses. You cannot control the loss ratio, but you can set your own psychological position based on points 1 and 2, and then take responsibility for your own cognition.