Author: Michael Zhao & Zach Pandl, Grayscale; Translation: Bitchain Vision xiaozou

-

Just like the traditional financial field, exchanges are the core infrastructure of the digital asset industry.Although currently decentralized exchanges (DEXs) focus mainly on crypto asset trading, the share of transaction volume of stablecoins and tokenized assets is expected to continue to grow over time.

-

Cryptocurrency trading is still dominated by centralized exchanges (CEXs), which adopt traditional enterprise architecture.But the industry is increasingly “reaping its own fruits”: more and more trading volumes are turning to decentralized exchanges (DEXs), and this year’s explosive growth of decentralized futures exchange Hyperliquid is proof of this year.

-

Decentralized exchanges (DEXs) settle transactions through on-chain without the need for centralized operators—in their form include smart contract applications deployed on blockchains such as Ethereum or Solana, or exchange logic directly embedded in Layer1 protocols such as Hyperliquid.In the first five months of 2025, DEX accounted for 7.6% of the total cryptocurrency transaction volume.

-

Although cryptocurrency exchanges can benefit from the growth in trading volume, they also face competitive pressure on transaction fees.Grayscale Research expects CEX to continue to dominate the transactions of large-cap assets such as Bitcoin, but DEX will become the first choice for long-tail asset trading and the first choice for users who value the transparency and accessibility of licenseless global platforms.

Public chains provide digital business solutions without centralized intermediaries.However, to attract users, decentralized technology must provide functionality that is at least as attractive as centralized solutions.If decentralized applications are inferior to centralized solutions in terms of speed, cost and historical data, then blockchain activity is likely to remain only a small part of the online business landscape.

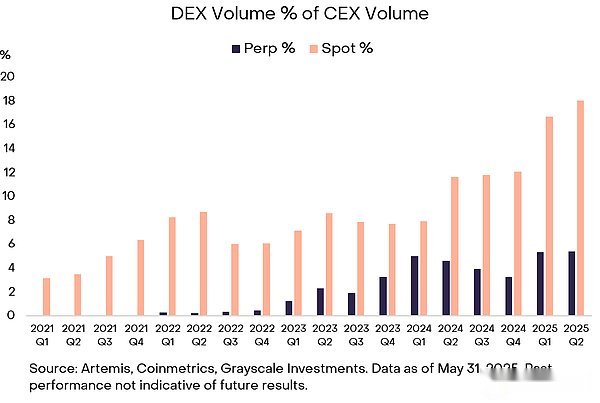

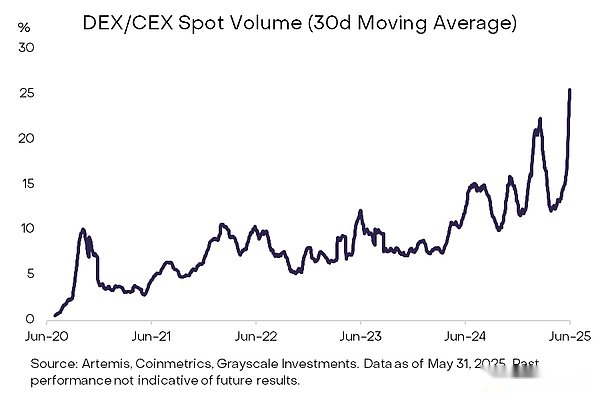

Fortunately, after years of exploration, we have seen with our own eyes that decentralized applications compete head-on with traditional institutions in the core field of token trading, the cryptocurrency.Grayscale Research estimates that DEX currently accounts for 7.6% of the total global cryptocurrency trading volume (only 3% in 2023), and its share of transaction volume compared to CEX has also increased significantly (Figure 1).Nowadays, DEX is evenly matched with CEX in terms of price, and often has higher transparency, and often becomes the main trading place for newly issued assets on the chain.

Figure 1: DEX trading volume has increased by more than double compared to CEX since 2021

This year is likely to be a turning point for the industry, with technological advancements and clear regulatory efforts to drive users to adopt DEX and other decentralized finance (DeFi) applications.This article will provide a comprehensive overview of the DEX industry, including industry structure, competitive trends and development prospects.Grayscale Research believes that market leadership will eventually be concentrated on a few top platforms—in each segment (CEX and DEX, spot and perpetual contracts) may only remain one or two exchanges—that combines deep liquidity, capital-efficient infrastructure with attractive token or equity economic models.

1. How to trade tokens

In traditional finance (TradFi), transactions are executed through exchanges or over-the-counter markets (OTCs) after both parties reach a price consensus.These transactions are matched through the Central Limit Order Book (CLOB) or the broker network.After the transaction is executed, the transaction details and risk exposure of the diverted participants will be confirmed by clearing houses such as the Custody Trust Company (DTC), and the settlement will be completed the next day (electronic record of transferring funds and securities ownership).Stock Securities was changed from T+2 settlement to T+1 settlement in May 2024.

Cryptocurrency trading adopts a completely different market structure and can be divided into three categories: trading venues, exchange structures and trading products.

Cryptocurrency trading venues are mainly divided into two categories:

Centralized exchange (CEX):Traditional commercial institutions that adopt off-chain custody and transaction matching provide a nearly instant settlement experience through internal ledgers.However, users will still experience settlement delays when transferring assets to traditional bank accounts.

Decentralized Exchange (DEX):Smart contract applications directly deployed on blockchains (such as Ethereum) support users to directly trade from self-hosted wallets.When trading on DEX, execution and settlement are completed within a single block confirmation cycle, usually only in a few seconds.

DEX mainly adopts two transaction structures:

Automatic Market Maker (AMM):Passively provide quotes through liquidity pools, centralized liquidity models based on preset mathematical curves (such as the constant product formula x*y=k) or Uniswap v3.AMM is particularly good at efficiently handling long-tail asset exchange and stablecoin transactions, and has performed outstandingly on blockchains with limited throughput.

Central Limit Order Book (CLOB):Highly restore the traditional exchange model and match the limit orders dynamically managed by liquidity providers.This approach usually enables narrower spreads and higher capital efficiency, especially suitable for high-volume assets and perpetual contracts.But maintaining this efficiency requires frequent order updates and relying on complex infrastructure such as professional blockchain application chains or Roll-ups.

Both CEX and DEX support two types of product transactions:

Spot trading:The target tokens are delivered instantly at the agreed price – no leverage, only involving on-chain transfers (or CEX internal ledger updates).

Perpetual contract (Perps):Derivative contracts without maturity track the price of the underlying asset, settled through margin adjustments and fund rate payments, and support leveraged trading.

2. The business model of the exchange

The exchange makes profits by charging transaction fees.In the crypto space, CEX charges directly, while DEX usually distributes handling fees to liquidity providers, token holders and/or protocol vaults through smart contract mechanisms or governance decisions.

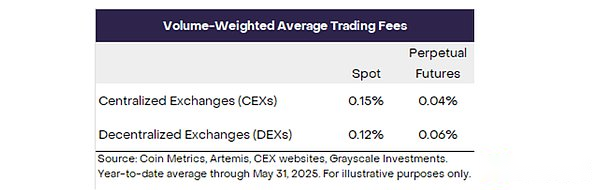

Currently, DEX has fully realized its price competitiveness for CEX.According to data from the first five months of 2025, Grayscale Research estimates that the weighted average handling fee of CEX spot trading volume is about 15 bps, and the DEX is 12 bps; the average handling fee of CEX perpetual contracts is 4 bps, and the DEX is 6 bps (Figure 2).Although these data do not reflect the rate differences between platforms and tokens, they indicate that the average handling fee of the two types of platforms has tended to be flat.

Figure 2: DEX now has price competitiveness comparable to CEX

As the cryptocurrency industry develops, all exchanges may benefit from the growth of trading volume, but will also face pressure from the compression of handling fees.Although the handling fees of CEX and DEX are approaching, compared with the most efficient market in traditional finance,Cryptocurrency transaction fees are still high.For example, academic research found that the average handling fee on U.S. stock exchanges is only 0.0001% (i.e. one-tenth of a basis point).It will take some time for cryptocurrency trading to reach such a low level, but fierce competition on traditional exchanges does indicate that as market competition intensifies, cryptocurrency trading fees will inevitably decline.

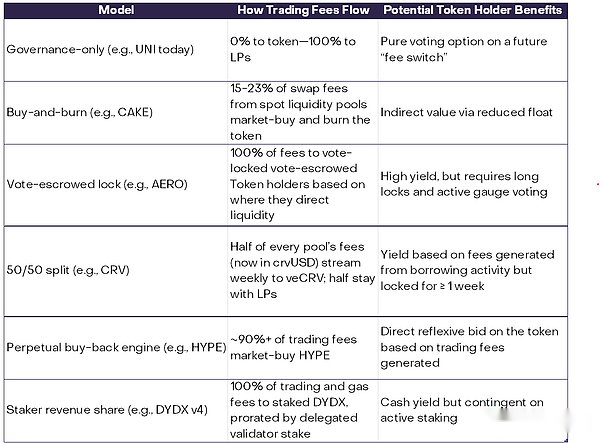

In the long run, we expect the capital structure of cryptocurrency exchanges to be consistent.As a traditional enterprise, CEX usually raises equity funds (such as Coinbase), but may also issue associated tokens (such as BNB).DEX is a smart contract based on open source software, and its operations do not rely on any controller.But the development team behind it may receive financial support through equity, tokens, or a combination of both.Tokens may bring various benefits to holders, but there is no unified model among different projects: DEX tokens may capture cash flow, provide governance rights, or have only marketing and brand value (Figure 3).It should be noted that the token model may indeed change through governance; Uniswap’s UNI token has explored proposals such as turning on the fee switch (a fee allocation switch controlled by governance) for stakeholders, which may reshape the token’s value proposition overnight.Therefore, investing in DEX tokens requires a deep understanding of the project’s economic model, governance proposals, and token supply and value accumulation mechanisms.

Figure 3: The economic model of DEX tokens is significant.

3. DEX evolution process

The development of decentralized exchanges has shown obvious phased breakthroughs, and each generation has overcome the limitations of the previous generation.Early attempts (2017-2018)—such as EtherDelta’s order book model, off-chain relay scheme of 0x protocol, and Bancor’s first AMM fund pool—although verifying the feasibility of decentralized transactions, it faces serious user experience and liquidity challenges.The launch of Uniswap in 2018 was a turning point, with its simplified AMM model and intuitive interface greatly improving accessibility, paving the way for the explosive growth of trading volume and total locked value during the “DeFi Summer” period in 2020.

Further optimizations from 2021 to 2023 – especially the centralized liquidity design of Uniswap v3, and innovations in the perpetual contracts by Perpetual Protocol and GMX – significantly improve capital efficiency and enable finer on-chain derivatives trading.In the recent stage (2023-2025), on-chain CLOBs such as dYdX Layer1 based on Cosmos and Hyperliquid’s ultra-high-speed customized blockchain have emerged one after another, combining the speed accuracy of centralized exchanges with the transparent decentralized characteristics of DeFi.

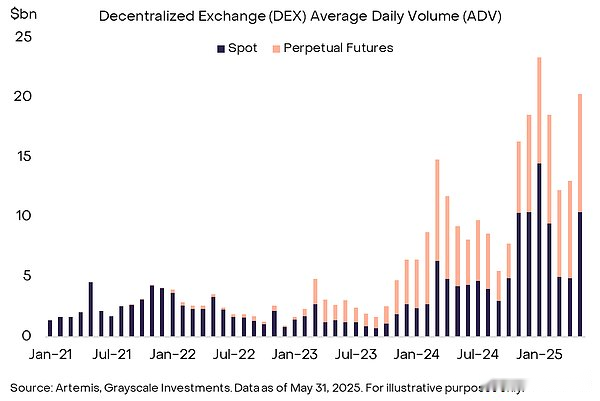

The current average daily trading volume (ADV) of spot and perpetual contracts for cryptocurrency DEX is close to $10 billion (Figure 4), while the average daily trading volume of the platform under the New York Stock Exchange Group is about $150 billion.The growth in the transaction volume of DEX perpetual contracts mainly comes from Hyperliquid, which accounts for about 80% of the total daily trading volume of perpetual contracts.

Figure 4: The average daily trading volume of DEX spot and perpetual contracts has exceeded 10 billion US dollars

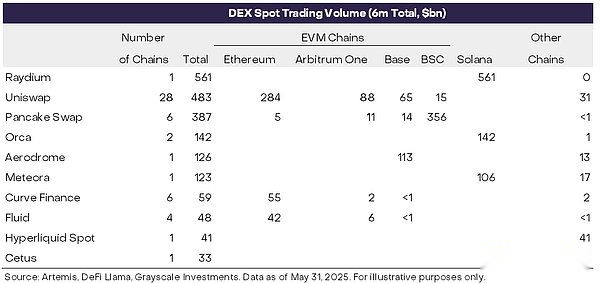

A unique feature of cryptocurrency trading is that some spot DEXs are deeply tied to specific blockchain ecosystems such as Ethereum or Solana.For example, Figure 5 shows the distribution of DEX spot trading volume on various blockchains in the past six months – industry leader Raydium is only deployed on the Solana chain, while Uniswap’s AMM model has been expanded to 28 different chains.Therefore, for crypto spot DEX, changes in transaction volume are often closely related to the fluctuations in the economic activity of the blockchain ecosystem to which it belongs.

Figure 5: Spot DEX can achieve multi-protocol deployment

4. DEX’s market share expansion

Currently DEX accounts for about 25% of the trading volume in the cryptocurrency spot market.Decentralized exchanges can continue to gain market share, mainly due to the rapid innovation on the supply side of their products.DEX is often the first to launch new tokens, attracting early liquidity and speculative trading volume.For example, during the on-chain ecological outbreak period at the end of 2024, many popular crypto narratives – such as tokens on Solana and Base chains with AI agents as the theme, and viral tokens such as TRUMP meme coins on Meteora – were originally born only in the decentralized liquidity pool of chains such as Solana and Base.These new tokens did not log on to centralized exchanges in the early stages, prompting traders to directly interact with the decentralized platform.

Figure 6: The ratio of spot trading volume between DEX and CEX continues to rise

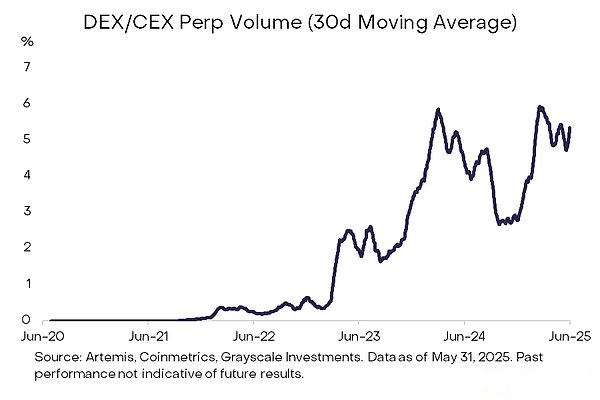

Decentralized exchanges have also made significant progress in the perpetual contract trading field – mainly due to the explosive success of the decentralized perpetual contract exchange Hyperliquid.Grayscale Research estimates that in the past 30 days ended May 31, 2025, the DEX perpetual contract trading volume accounted for approximately 5.4% of the CEX perpetual contract trading volume (Figure 7).Even so, centralized perpetual contract exchanges still have many advantages, including: deep liquidity and network effects, high-speed execution capabilities and integrated user experience.

Figure 7: DEX perpetual contract trading volume is small but continues to grow

Since CEX has these advantages, why can Hyperliquid capture such a large transaction volume?We believe that the reasons why traders are increasingly inclined to decentralized perpetual contracts are as follows:

Self-management and auditability:The deposited funds are always controlled by the user, and every operation from transaction to liquidation is transparently recorded on the chain, reducing the risk of opponents similar to the FTX crash and recent hacking incidents of centralized exchanges [16].

Global accessibility:Decentralized platforms achieve global threshold participation.

Composability and seamless integration:Complex financial products such as third-party robots, trading vaults, analysis panels, and delta neutral strategies on the entire chain can be directly integrated bypassing regulatory frictions.

Release new:The community-driven governance model allows decentralized platforms to first launch perpetual contracts for emerging tokens, far faster than centralized competitors.

Although centralized exchanges still have significant advantages in risk management, user interface and institutional liquidity, the rapid progress of decentralized exchanges and the increasingly mature technical architecture indicate that major changes in the competitive landscape in the next few years.

5. DEX Battle

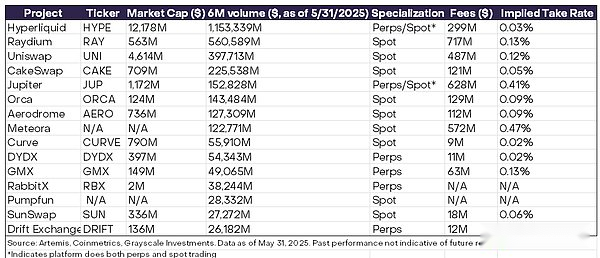

The top ten DEXs in cryptocurrencies account for 6.7% of the total transaction volume, with a total market value of US$22 billion, of which the top five platforms account for about 80% of the transaction share (Figure 8).These platforms may benefit from strong network effects: at the spot trading end, centralized liquidity AMM minimizes slippage; in the field of perpetual contracts, highly competitive rate hierarchies attract high-frequency traders.In both scenarios, deeper liquidity pools will attract more order flows—traders naturally tend to choose exchanges with narrower spreads, lower execution risks, and large active communities.

Figure 8: Despite the large number of DEXs, only a few have the advantage of volume dominance

We believe that no single exchange can monopolize every corner of the cryptocurrency market.In contrast, one or two dominant platforms may appear in each exchange type (CEX vs. DEX) and product type (spot vs. perpetual contract) field.

In the field of spot products, transactions of large-cap assets (such as Bitcoin, Ethereum and mainstream stablecoins) are still biased towards CEX.With fiat currency deposit channels, deep inventory of market makers and VIP transaction rates below 10 basis points, CEX usually allows users to trade mainstream tokens at lower costs than the most efficient AMM fund pool.But for small market capitalization and newly issued tokens, early trading activity is still concentrated on DEX.Since DEX supports unlicensed coins, when the market narrative focuses on a newly created niche token, traders pursuing first-day exposure often follow the platform where liquidity first appears.

The perpetual contract field also presents the same pattern.CEX accounts for more than 90% of the nominal value of Bitcoin and Ethereum perpetual contracts because it provides millisecond delays, market-making rebates and a mature clearing engine.But if you observe the contract varieties that rank ten, market share begins to reverse: in multiple mid-cap trading pairs, Hyperliquid contributes most of the global trading volume and open contracts.For traders chasing new assets, advantages such as self-custody, borderless access and governance-driven contract creation may overwhelm the convenience of centralized exchanges.

6. Conclusion

DEX has evolved from an experimental concept to a core infrastructure for on-chain asset expansion.With the growth of stablecoins, accelerated migration of real-world assets to public chains, and decreased block space costs, DEX’s share in daily transactions will continue to expand—especially new tokens or niche markets that have never touched the centralized order book.CEX will still maintain its advantage in high nominal value, low latency sensitive transaction flows.But the long-term competitive landscape is even more grand: cryptocurrency exchanges are accumulating the overall momentum to challenge traditional exchanges, and launching impacts on asset custody, liquidity provision and price discovery mechanisms in the fields of tokenized stocks and bonds.In short, the question is no longer “whether DEX is important”, but rather how fast its transparent and programmable infrastructure will redefine the “exchange” in the next decade.