Source: Grayscale; Compilation: Bitchain Vision

Quick look at the key points:

-

The US regulatory clarity on digital assets has been brewing for a long time — and while the road ahead is still unfolding, policy makers have made meaningful progress this year.

-

The market’s attention to good regulation may have contributed to the excellent performance of ETH.Ethereum is a leader in the blockchain financial market, so Ethereum may benefit from it if regulatory clarity can promote the popularity of stablecoins, tokenized assets and/or decentralized financial applications.

-

Digital Asset Treasury (DAT) — publicly traded companies holding cryptocurrencies on their balance sheets — have surged in recent months, but investor demand may have become saturated.The valuation premium of large projects is being compressed.

-

Bitcoin price once hit an all-time high of about $125,000, but closed down in August.Although Bitcoin prices in August are not as trending as other tokens,The pressure on Fed independence clearly reminds us why investors have such strong demand for Bitcoin.

In August 2025, the total market value of cryptocurrencies stabilized at around US$4 trillion, but there were obvious fluctuations in secret.Crypto asset classes cover a variety of software technologies, and their basic drivers vary, so token valuations do not always fluctuate synchronously.

althoughBitcoin price fell in August,butEthereum rose 16%.The second largest public chain, with market capitalization, appears to benefit from investors’ focus on regulatory changes, which may support the adoption of stablecoins, tokenized assets and decentralized finance (DeFi) applications – and Ethereum is currently leading the industry in these areas.

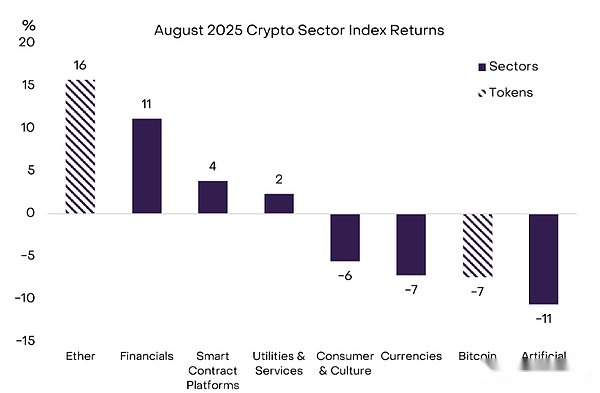

Figure 1 shows the changes in each segment of the track in August using Grayscale’s “crypto track” framework, a strict digital asset taxonomy and index portfolio developed in partnership with FTSE Russell Index.Currency, Consumption and Culture, and Artificial Intelligence (AI) crypto track indexes all fell slightly month-on-month.The weakness in the AI track reflects the poor performance of AI-related stocks in the public stock market.Meanwhile, the financial, smart contract platforms and utilities and services crypto track indexes all rose in the month.Despite the decline in Bitcoin’s price month-on-month, it hit an all-time high of about $125,000 in mid-August; ETH prices also hit an all-time high of just under $5,000.

Chart 1: August cryptocurrency track returns

GENIUS Act and the Future

We believe thatEthereum’s recent excellent performance is closely related to fundamentals: most importantly, the increased transparency of regulatory transparency in digital assets and blockchain technology in the United States.We believe that the most important policy change this year is undoubtedly the passage of the GENIUS Act in July.The bill provides a comprehensive regulatory framework for payment of stablecoins in the U.S. market (see “The future of stablecoins and payments”,). Ethereum is the leading stablecoin blockchain today (calculated in transaction volume and balance),The passage of the GENIUS Act drove ETH to rise by nearly 50% in July.The same factor seems to drive Ethereum higher in August.

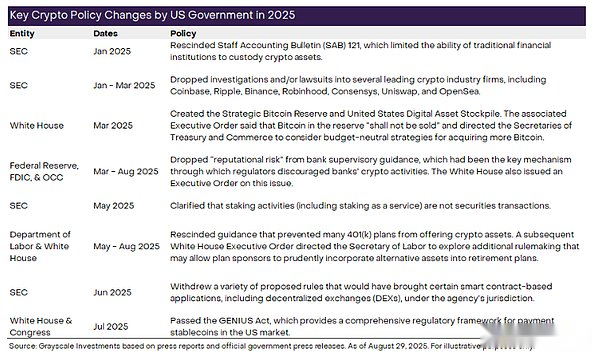

However, the U.S. policy changes this year are far more than stablecoins, covering a range of issues from crypto asset custody to bank regulatory guidelines.Chart 2 summarizes the specific policy actions we consider the most important in digital assets this year by the Trump administration and federal agencies.These policy changes—and more future policy changes—stimulate the wave of institutional investment across the crypto industry (see “Institutional chain reaction》).

Figure 2: Policy changes bring greater regulatory transparency to the crypto industry

In August this year, Fed governors Waller and Bowman both attended the blockchain conference in Jackson Hole, Wyoming, which was unimaginable a few years ago.The meeting was immediately followed by the Federal Reserve’s annual Jackson Hall Economic Policy Conference.In their speech, they emphasized that blockchain should be seen as an innovation in fintech and that regulators should strike a balance between maintaining financial stability and creating space for new technologies.

In August this year, Fed governors Waller and Bowman both attended the blockchain conference in Jackson Hole, Wyoming, which was unimaginable a few years ago.The meeting was immediately followed by the Federal Reserve’s annual Jackson Hall Economic Policy Conference.In their speech, they emphasized that blockchain should be seen as an innovation in fintech and that regulators should strike a balance between maintaining financial stability and creating space for new technologies.

In September, the Senate Banking Committee plans to review cryptocurrency market structure legislation—a regulation that will cover areas of cryptocurrency markets other than stablecoins.The Senate effort is based on the CLARITY Act, which was passed in the House in July by bipartisan support.Senate Banking Committee Chairman Scott said he expects market structure legislation to gain bipartisan support in the Senate.However, there are still some major problems to be solved.Industry groups pay particular attention to ensuring that market structure legislation is incorporated into protection for open source software developers and non-hosted service providers.Legislators may have ongoing debate on the issue in the coming months (it should be noted that Grayscale is the signatory of a recent letter of industry comment to members of the Senate Banking Committee and Agriculture Committee).

Is DAT oversupply?

BTC performed poorly in August, while ETH performed well, which was clearly reflected in the capital flows of a range of venues and products.

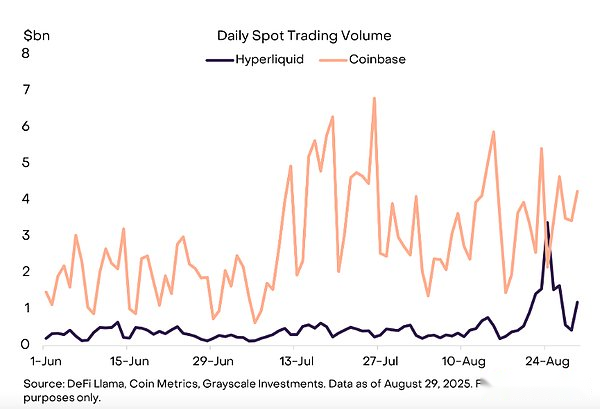

Part of this drama takes place on Hyperliquid, a decentralized exchange (DEX) that offers spot and perpetual contract trading (see “The Rise of DEX” https://www.jinse.cn/blockchain/3716302.html).Starting August 20, a Bitcoin “whale” (large holder) sold about $3.5 billion in BTC and immediately bought about $3.4 billion in ETH.While we cannot judge investors’ motivations, it is encouraging to see the risk transfer of this scale happen to DEX rather than centralized exchanges (CEX).In fact, on the day of the largest trading volume this month, Hyperliquid’s spot trading volume was once higher than Coinbase’s spot trading volume (Figure 3).

Figure 3: High liquidity spot trading volume surge

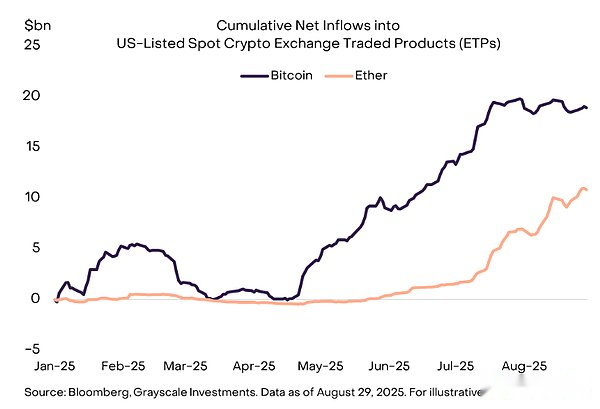

In August, net inflows from cryptocurrency exchange-traded products (ETPs) also reflected a similar preference for ETH.Spot BTC ETP listed in the U.S. saw a net outflow of $755 million, the first time since March.By comparison, spot ETH ETP listed in the U.S. has net inflows of $3.9 billion this month after a net inflow of $5.4 billion in July (Figure 4).Both BTC and ETH ETP hold more than 5% of their respective token circulation after a surge in net ETH inflows over the past two months.

Figure 4: ETP net inflow steering ETH

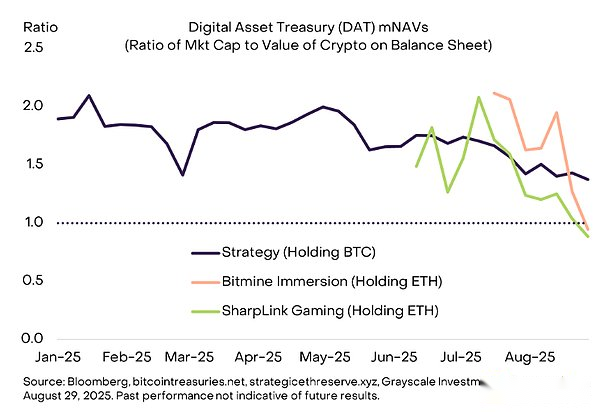

Bitcoin, Ether and many other crypto assets are also backed by digital asset treasury (DAT) purchases.DAT refers to a listed company that holds cryptocurrencies on its balance sheet and serves as an access tool for equity investors.Strategy (formerly MicroStrategy) is the largest Bitcoin DAT, which purchased an additional 3,666 BTC (about $400 million) in August.Meanwhile, the two largest Ethereum DATs have purchased a total of 1.7 million ETH (approximately $7.2 billion).

According to media reports, at least three new Solana DATs are in preparation, including more than $1 billion worth of investment vehicles sponsored by consortiums such as Pantera Capital and Galaxy Digital, Jump Crypto and Multicoin Capital.In addition, Trump Media and Technology Group announced plans to launch aDAT based on CRO tokens, the token is associated with Crypto.com and its Cronos blockchain.Other recent DAT announcements focused onEthena’s ENA token, Story Protocol’s IP token, and BNB tokens from Binance Smart Chain.

Although the promoters continue to provide these investment tools, price performance indicates that investor demand may have become saturated.To measure the supply and demand imbalance of DAT, analysts usually monitor their “mNAV,” the ratio of the company’s market value to the value of crypto assets on the balance sheet.If there is an oversupply of crypto assets in the form of public equity instruments (i.e., insufficient DAT), the transaction price of mNAV may exceed 1.0; if there is an oversupply of crypto assets in the form of public equity instruments (i.e., excess DAT), the transaction price of mNAV may fall below 1.0.At present, mNAVs of some large DATs appear to be converging to 1.0, indicating that supply and demand of DATs are tending to be balanced (Figure 5).

Figure 5: DAT’s valuation premium is falling

Return to the Origin: Reasons for Being Positive Bitcoin

Like all asset classes, public discussions about cryptocurrency markets have mostly focused on short-term issues such as regulatory changes, ETF capital flows, and DATs.However, it may be helpful to take a step back and think about its core investment philosophy.While the cryptocurrency space contains many different assets, Bitcoin exists in the rationale for providing a monetary asset and peer-to-peer payment system based on clear and transparent rules that are independent of any particular individual or institution.Recently, the independence of the Federal Reserve is under threat, which once again reminds us why many investors are so interested in these assets.

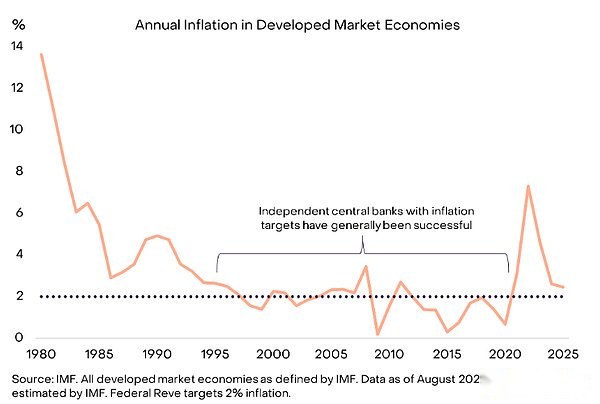

In terms of context, most modern economies adopt a “fiat” monetary system.This means that the currency has no clear support (i.e., it is not pegged to any commodity or other currency), and its value is entirely based on trust.Throughout history, governments have repeatedly used this feature to achieve their short-term goals (such as re-election).This could lead to inflation and reduce trust in the fiat currency system.

Therefore, to make fiat currencies effective, there needs to be a way to ensure that the government fulfills its commitment to not leverage the system.The approach adopted by the United States and most developed market economies is to give central banks clear goals (usually in the form of inflation targets) and operational independence.Elected officials usually provide some oversight on the central bank to ensure democratic accountability.In addition to the temporary surge in inflation after the COVID-19 pandemic, this clear goal, operational independence and democratic accountability system has achieved low and stable inflation in major economies since the mid-1990s (Figure 6).

Figure 6: Independent central banks achieve low and stable inflation

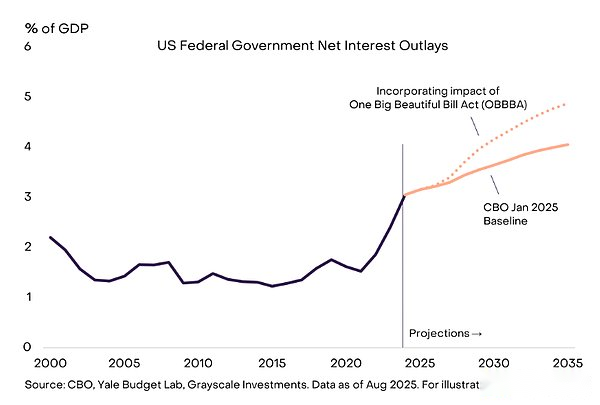

In the United States, this system is now under pressure.The fundamental drivers are not primarily from inflation, but from deficits and interest expenses.The U.S. federal government’s current total debt is about $30 trillion, equivalent to 100% of GDP. Although the U.S. economy is in peacetime and has a low unemployment rate, it still hits its highest level since World War II.As the Ministry of Finance refinances its debt at an interest rate of about 4%, debt interest expenditures continue to rise, occupying resources that could have been used for other purposes (Figure 7).

Figure 7: Interest expenses swallow more federal budgets

The Big Beautiful Act (OBBBA), passed in July this year, will lock in high deficits over the next 10 years.Unless interest rates fall, this will mean higher interest expenses and further squeeze other uses of government revenue.Therefore, the White House repeatedly pressured the Fed to lower interest rates and demanded that Fed Chairman Powell resign.These threats to Fed independence escalated in August as Lisa Cook, one of the six current members of the Fed’s seven-member board of directors, was removed from office.Although this may help elected officials in the short term,A weaker Fed independence will increase the risk of long-term high inflation and currency weakness.

Bitcoin is a monetary system based on transparent rules and predictable supply growth.When investors lose confidence in institutions that protect the fiat currency system, they turn to trustworthy alternative currencies.Unless policy makers take steps to strengthen institutions that support fiat currencies—to enable investors to believe in their long-term commitment to maintaining low and stable inflation—Demand for BTC may continue to rise.