Source: insights4.vc, compiled by: Shaw Bitcoin Vision

Introduction

Fintech 1.0Moving existing banking products online – think of early online banking and payment apps.The user experience has moved to web and mobile devices, but fund flows still rely on traditional channels such as ACH, SWIFT and card processing networks.Value creation comes from convenience and user interface optimization, not changes in the way funds flow.2010sFintech 2.0giving rise to new mobile-first banks and specialist fintech companies.Emerging challengers like neobanks target specific groups (students, gig economy workers, underbanked populations) with simple and smooth apps, but still rely on partner banks and card networks for their core functionality.Differentiation is in brand and functionality, while legacy payment systems and regulations limit innovation and keep it at the “top of the technology stack.”

High fixed costs and licensing hurdles mean that only chartered banks or their partners can handle custody and transfers, so fintech startups are mostly just repackaging the same old system.

By the late 2010s, “embedded finance” and Banking as a Service (BaaS) were being heralded as the next stage of development – might as well call itThe traditional view of FinTech 3.0.Any application can access the banking system through API to provide account, payment or loan services.This did expand distribution channels, but actual financial flows remained limited to closed, bank-controlled networks.Overreliance on a few originating banks has led to homogenization of services and concentration of risk.Compliance burdens on these banks are increasing, costs are rising, and the pace of innovative experimentation is slowing.For two decades, fintech innovation has remained superficial—delivering a better user experience on aging infrastructure—because building new infrastructure outside of the banking oligopoly has been nearly impossible.

Stablecoins mark turning point, cryptocurrencies take opposite approach

It does not start with a beautiful interface, but builds a new financial infrastructure from scratch (such as automated market makers, on-chain lending, etc.).In this series of experiments, stablecoins backed by legal currency stood out and became a breakthrough product with practical application value.Unlike previous fintech stages, stablecoins are not just new packaging of old systems, they are entirely new systems themselves.They perform critical banking functions directly on the open network.In other words, we are moving from fintech companies relying on other people’s infrastructure to fintech companies owning and building entirely new infrastructure.This research report believes that the hallmark of FinTech 3.0 is the native infrastructure of stablecoins—programmable digital dollars based on blockchain rails—which will unleash a series of specialized fintech opportunities that were previously unattainable.

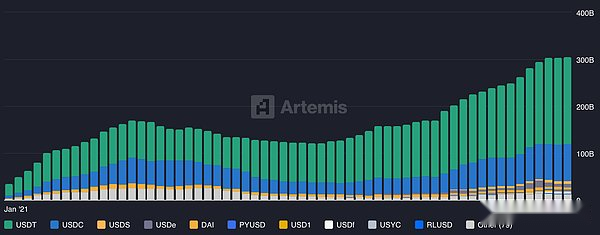

Stablecoin supply by token.Source: Artemis

What is Fintech 3.0: Stablecoin native infrastructure

Fintech 3.0 refers to financial products and services based on stablecoins and tokenized asset payment rails, rather than traditional banking networks.Its distinguishing feature is that funds flow on an open, interoperable blockchain.This is in stark contrast to today’s closed, permissioned payment rails (such as FedWire, SWIFT, Visa/Mastercard), which are limited by bank opening hours, geographical barriers and multiple layers of intermediaries.The stablecoin payment track operates 24/7, year-round, with global coverage, enabling fast and direct transfers without the need for multiple agent banks to reconcile.For example, anyone can send U.S. dollar-pegged stablecoins like USDC or USDT across borders in seconds with extremely low network fees, whereas international wire transfers can take days and incur high fees.Stablecoin transactions settle in near real-time, often with just a few block confirmations, enabling near-instant peer-to-peer settlement and avoiding the delays of batch processing.

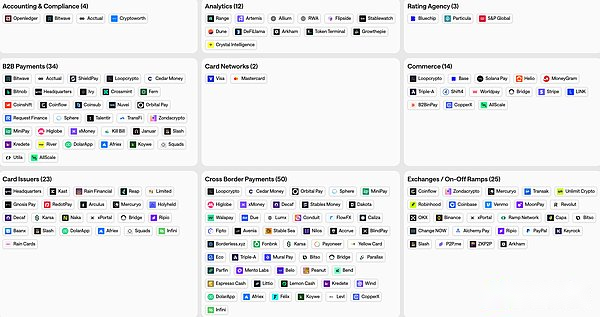

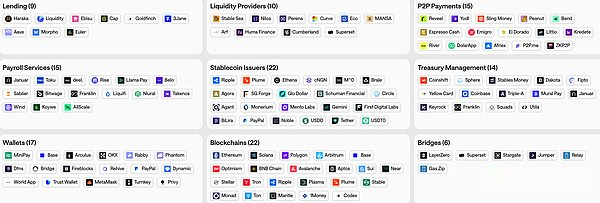

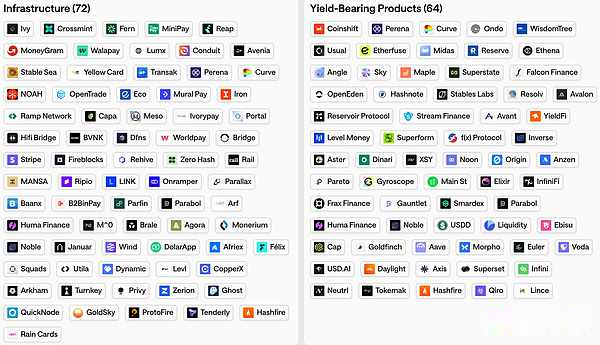

Stablecoin Ecosystem Map

Stablecoin Ecosystem Map

Stablecoin Ecosystem Map

Programmability and composability are equally important

Stablecoins are digital bearer certificates that exist on a public blockchain ledger, meaning they can interact with smart contracts and other cryptoassets.Dollars turned into software.Enterprises and developers can program the flow of funds—for example, streaming payments billed by the second, escrow services for cash on delivery, or complex multi-party transactions—that are difficult to implement on traditional infrastructure.Stablecoins can be seamlessly integrated with on-chain lending, exchanges or tokenized assets, enabling composable finance where various modules are interconnected.This opens the door to entirely new product structures not possible in traditional systems.As a risk analysis report points out, stablecoins represent a fundamental architectural shift from batch processing to real-time processing, from agent banking to peer-to-peer, and from physical finance to programmable finance.

For institutions and regulated businesses, stablecoin rails also offer advantages such as transparent auditability (transactions can be traced on-chain), more efficient liquidity management, and the ability to do business across jurisdictions without opening a local bank account in each country.Of course, to achieve mainstream application, stablecoins must be connected to existing systems—bank account deposit and withdrawal channels, compliance inspections, and regulatory oversight are all constantly developing and improving.But its core idea is that Fintech 3.0 subverts the traditional model: Fintech companies are no longer customers of banks and networks, and the stablecoin era allows them (even non-financial companies) to become providers of basic financial infrastructure.Global stablecoin transfers could occur entirely outside the traditional banking system, yet achieve the same results faster and more cost-effectively.It’s no wonder that the value of stablecoins in circulation has soared to over $230 billion (a 45x increase from 2019 as of early 2025), and monthly on-chain payment volumes have reached hundreds of billions of dollars or more.Fintech 3.0 means these digital dollars are no longer a cryptocurrency novelty, but an important new way to move money at scale.

Stablecoin Technology System: Hierarchy and Value Capture

Finance based on stable currency is forming its unique technology and service system.We can think of it as several key layers, each performing a different function and capturing a different share of value in the ecosystem.Fintech companies often focus on one tier, but as companies expand across multiple tiers, the lines between tiers can become blurred.A simplified technical system might include:

Settlement layer (basic blockchain)

This underlying layer consists of a public blockchain network that records stablecoin transactions.For example, general blockchains such as Ethereum, Solana, and Tron, as well as Layer-2 networks optimized for payments.This layer provides the infrastructure for the clearing and settlement of stablecoin transfers.Just as ACH or VisaNet underpin bank payments, blockchain plays a fundamental role in the stablecoin space.Value capture comes primarily from transaction fees, but may also come from the value of network tokens.Despite the multitude of blockchains, competitive pressures for speed, capacity and low cost remain.We are seeing the rise of dedicated payment-focused blockchains and aggregation chains to support large stablecoin transactions at minimal cost (e.g., Coinbase’s Base L2 enables sub-1 cent, sub-1 second USDC transfers).The settlement layer tends to develop slowly and prioritize security and stability because it is the foundation for all others.

Issuing layer (stable currency issuer)

It is at this level that trust enters the system, as stablecoins are created and managed by the entities themselves.Currently, major issuers such as Circle (USDC) and Tether (USDT) dominate, and together they hold huge reserves (currently among the top 20 global U.S. Treasury holdings).Issuers are responsible for providing asset backing for each token at a 1:1 ratio, managing liquidity, and complying with emerging “payment stablecoin” regulations.We are also seeing some new issuers emerging: large fintech companies (such as PayPal’s PYUSD), regional institutions launching local currency stablecoins on multiple blockchains (such as EURC, etc.), and even corporate or bank-led projects.Opportunities also exist for specialized stablecoin issuers targeting specific regions, industries or application scenarios – for example, stablecoins linked to commodity prices for trade settlement, or fully compliant stablecoins serving Islamic regional markets.Issuers have the potential to build network effects (widely used tokens become more valuable) and regulatory moats (licenses, trust), allowing winners at this level to be highly profitable.However, this is capital intensive (reserves and compliance costs) and only a few issuers will get the most value from it.

Infrastructure and Orchestration Layer

This middle layer encompasses the technical and compliance infrastructure used by fintech companies and enterprises to integrate stablecoin infrastructure.It includes wallet platforms, hosting providers, API services, deposit and withdrawal service providers, blockchain node infrastructure, compliance and analytics tools, payment processing gateways, and more.Essentially, these are B2B services that simplify the complexity of blockchain and provide the building blocks for stablecoin applications.For example, a fintech company might use a custodial API to securely handle private keys, KYC/AML tools to screen addresses, or an “orchestration” API to route payments across multiple blockchains to achieve the best speed/cost ratio.This layer also covers stablecoin liquidity management and foreign exchange (conversion between stablecoins and fiat currencies or other currencies).Many startups are rushing into this space because there is an immediate need – every stablecoin project needs some infrastructure.However, infrastructure and middleware may become homogeneous; if many companies offer similar APIs and wallet services, profit margins will be compressed.We’re already seeing intense competition and price pressure here.Some infrastructure providers try to differentiate themselves by bundling multiple features (for example, an all-in-one platform that integrates regulation, custody and deposits and withdrawals) or by supporting specific niche needs that other providers do not offer.However, investors generally believe that middle-tier service providers will face margin compression over time.While many middle-tier service providers will still exist, their value capture may be limited unless they achieve scale or transition to proprietary services.

Distribution and application layer

At the top are user-facing fintech applications and services, which truly provide stablecoin-based solutions to end users or businesses.This includes wallets and payment apps, remittance platforms, merchant payment solutions, lending and savings apps using stablecoins, payroll and money management services, and more.Essentially, any traditional fintech product can be “reimagined” based on stablecoins—from new bank accounts that hold stablecoins, to cross-border payment applications, to decentralized financial interfaces that integrate stablecoins with other assets.At this level, professional processes and customer relationships create differentiation.For example, a stablecoin fintech serving Latin American export businesses or the diaspora community could tailor its product and acquire customers that larger platforms might overlook.Although the underlying technology is open, distribution strategy and market segment positioning can form a moat.Companies at this tier typically achieve scale through superior user experience, trust, and integration with the community.

We’ve seen stablecoin usage grow most rapidly in areas where traditional payment methods fail – for example, users in emerging markets with volatile currencies, or freelancers who need fast global payments.Because of this, the distribution layer can create huge value by solving real pain points in specific markets.However, this requires consideration of both the cryptocurrency and fiat worlds (e.g., integration with local payment methods, compliance with local laws and regulations, user education).Many successful participants may start with the distribution layer and then gradually integrate it into their own infrastructure or distribution links to obtain higher profits.Conversely, some issuers or infrastructure providers will also launch user applications to drive user adoption.The entire technology architecture is dynamic, but generally speaking, the greatest long-term value may exist at the “edge”—the issuance and distribution layers—where companies either have strong network effects or have established direct connections with users.

Fintech companies focusing on stablecoins: Who can become a profitable market?

The core argument is that significantly lower infrastructure costs and open access allow fintech companies that specialize in specific areas to thrive on stablecoin platforms.If launching a financial app no longer requires partnering with a bank or spending millions of dollars on licensing and integrations, a small team can profitably serve a specific user base.Many customer segments that were historically underserved or unprofitable by large banks can now rely on specialized fintech solutions to stay afloat.The following lists several such customer groups (from individual users to small and medium-sized enterprises) and explains why stablecoin platforms can bring new opportunities to them:

Professional athletes and individual sports practitioners

Top athletes’ income often comes from an international level – from prize money, sponsorships or cross-border club transfer fees.The traditional banking system makes managing these funds cumbersome (opening multi-currency accounts, delays in wire transfers, high foreign exchange fees).For example, a tennis player might have to wait weeks to receive international tournament winnings and incur substantial currency conversion fees.The stablecoin-based solution allows sports professionals to receive USD-denominated stablecoins immediately after the game and can use or redeem them at any time.This reduces their dependence on high-cost intermediaries.Additionally, athletes from countries with weak currencies or capital controls may be more inclined to hold stablecoins (digital dollars) to preserve value.A fintech company focused on a specific niche could provide athletes with a stablecoin wallet linked to a debit card, as well as the tools to automatically convert a portion of their funds into local currency when needed.They can achieve profitability by charging management fees or arranging earnings from stablecoin reserves.The speed and global nature of stablecoin payment systems is particularly suitable for those who frequently travel and earn money in different markets.Athletes are no longer beholden to slow banking networks and have greater control over their money.

Illiquid equity stakes for startup employees

Imagine that employees of a high-growth unicorn company are rich on paper (with stock options) but strapped for day-to-day cash.Traditional banks typically don’t lend easily to private stocks, and selling shares is often restricted.Cryptocurrency payment infrastructure can provide some innovative solutions: for example, fintech platforms can tokenize employees’ vested options or use them as collateral for stablecoin loans.In this way, employees actually borrow USDC as collateral and can obtain liquidity without selling shares.In traditional payment channels, this particular collateral would be too complex for bank lending, but in stablecoin payment channels, a combination of smart contracts and market-driven lenders (even through DeFi) can provide support.A dedicated fintech company could work with businesses to offer “options liquidity in the form of stablecoins” as an employee benefit.They can charge interest or fees on these loans.The advantages of a stablecoin are crucial as it enables instant programmatic settlement of loans, and collateral can even be managed through blockchain escrow.While this is still an emerging concept, it exemplifies how programmable money can unlock financing use cases for communities (entrepreneurs) that are underserved by traditional finance.

On-chain developers and crypto-native teams

Ironically, many crypto project teams have difficulty accessing traditional banking services (due to regulatory uncertainty or bank policy restrictions on crypto businesses).These teams operate on stablecoins – using USDC/USDT to pay contractors, cloud services, and even salaries.This is an opportunity for fintech companies focused on serving these crypto-native companies to provide enhanced payroll, accounting and financial services built on stablecoins.For example, one service could manage multi-currency stablecoin payroll and handle tax filings in different jurisdictions, streamlining the process of paying contributors for a globally distributed DAO or startup.The service could also provide secure custody of funds and control of spending (very useful for multi-signature treasury), and perhaps automatically convert funds into fiat currency for things like office rent.The revenue source can be SaaS service fees or a certain percentage of the payment amount.Traditional banks are not interested in serving a DAO treasury or development team that is paid in tokens.Stablecoin fintech companies can fill this gap by combining the trustless nature of cryptocurrencies (no one can freeze your funds) with a multi-layered compliance reporting mechanism that satisfies audit requirements.Essentially, it could turn stablecoins into a commercial banking system for the cryptocurrency space.Given that there are hundreds of blockchain teams around the world, this segment is growing.

Digital nomads and cross-border freelancers

The boom in remote working has given rise to millions of freelancers and “digital nomads” who earn income from overseas clients.Traditional freelance payment methods (international bank transfer, PayPal, Western Union) are often slow and have high fees.Freelancers in Latin America or Africa may have to pay 8% to 10% in fees and foreign exchange transactions, and have to wait a week for the money to arrive.The emergence of stablecoins has changed this situation and enabled near-instant, low-cost global payments.At present, nearly one-third of freelancers on a global platform have applied to use stablecoins for payment. For example, they prefer to receive USDC and then exchange it for local currency or spend through cryptocurrency debit cards.A number of fintech companies are emerging specifically to serve this group: a wallet, for example, would allow freelancers in Nigeria or Argentina to receive USDC, convert a portion into local currency or airtime, and deposit the remainder into an account balance pegged to the U.S. dollar and unaffected by local inflation.They can receive their money as late as midnight on Sunday — no need to wait for a bank wire on Monday.Such platforms can make money through subscription services such as FX spreads (when users exchange stablecoins for other currencies) or faster withdrawals.The value proposition is simple: allow freelancers to earn money faster and have higher take-home wages.By removing the barriers posed by time zones and bank fees, stablecoin payment systems make it possible to build financial services for the world’s vast gig worker population.

Islamic compliant finance

Finance in Islamic areas follows religious principles, one of the important principles being the prohibition of interest.This makes it difficult for Muslim customers to use traditional banking products that pay interest or involve some uncertainty.Stablecoins open up a new avenue for Sharia-compliant digital finance.For example, a startup could offer stablecoin-based savings and payment accounts that pay no interest, but profits may be distributed in a Sharia-compliant manner (such as through fee-based services or profit-sharing contracts).In fact, we are witnessing the rise of Islamic cryptocurrency businesses – one recently licensed Islamic digital bank plans to operate entirely on stablecoin infrastructure to avoid offering interest-based products.By using stablecoins as a medium, they can ensure that customers’ funds are not commingled with interest-bearing instruments, while still providing modern payment services around the clock.For example, a stablecoin fintech company targeting Muslim SMEs in Southeast Asia could provide Sharia-compliant trade financing (without paying interest, possibly in an equity-like arrangement) and ensure profit sharing through on-chain transparency and smart contracts.The source of income is not interest, but service fees or profits from trade transactions.Traditional banks have been slow to introduce customized Islamic products in many markets; stablecoin platforms enable new entrants to serve these customers with built-in programmable compliance capabilities (e.g., automated screening of non-halal business transactions).In this segment, trust and religious beliefs are as important as technology, and stablecoins provide the flexibility to enable financial services to meet these needs in a natively digital way.

Cross-border SMEs and exporters

Small and medium-sized enterprises engaged in international trade often face the problem of slow B2B payment speed and high cost.Exporters may have to wait weeks to receive payment from overseas buyers, which not only ties up their working capital but also results in losses of 4% to 6% in bank fees and foreign exchange spreads.The reason these pain points persist is that agent banking and trade finance services for SMEs have not improved significantly – large banks prioritize serving large enterprises, while fintechs like Wise or Payoneer have improved but still rely on intermediary banks.The stablecoin payment system can realize instant and secure settlement of B2B transactions at extremely low cost.Imagine a platform built specifically for exporters that can generate invoices denominated in U.S. dollar stablecoins; buyers pay the invoices by transferring USDC, and within minutes, sellers receive confirmed payments on the chain.

The platform can automatically convert portions of funds into local currencies or treasury management products.Since payments are made in near real-time, exporters can immediately put money back into the business (significantly improving cash flow).For businesses in areas with capital controls, such as Africa or parts of Asia, a stablecoin channel that is more reliable than the volatile local banking system could also bring benefits.Fintech companies serving this area can make money by converting foreign exchange or providing trade finance (for example, using on-chain invoices as collateral and prepaying stablecoin funds to offset outstanding accounts).The key advantages are speed and cost-effectiveness: stablecoin trading can reduce cross-border payment costs by 40% to 70% and shorten settlement times from days to seconds.By focusing on specific trade corridors or industries, startups can build workflows (such as integration with accounting software, etc.) that large banks have never offered to smaller customers.

Luxury goods resellers and high-value peer-to-peer marketplaces

In the world of high-end watches, jewelry, art and collectibles, transactions are often large and sometimes urgent or require confidentiality.Traditional payment methods can become bottlenecks—wire transfers that are too large may be flagged for manual review, and international buyers face challenges sending money on short notice, especially on weekends or holidays.Stablecoins serve as digital cash for large transactions, allowing buyers in Hong Kong to instantly send $100,000 USDC to London sellers at 2 a.m. via cryptographic proof of funds.We have already seen some luxury goods dealers start accepting stablecoin payments.For example, a British luxury watch retailer partnered with a payment service provider to begin accepting USDC and other cryptocurrencies to provide customers with a faster and more flexible payment method.

A fintech company could build an escrow service specifically for luxury goods transactions: it stores the buyer’s stablecoin payment in a smart contract and transfers it to the seller when the buyer receives the item (a kind of automated escrow).For high-ticket items, this enhances trust and eliminates the need for costly letters of credit or escrow agents.The service can charge a low percentage fee that is much lower than traditional escrow or auction house commissions.Using stablecoins avoids the risk of chargebacks (unlike credit cards) and eliminates the need to rely on the normal operations of a bank.Such a platform can also help businesses with compliance (only one KYC verification is required for both parties) and potentially provide shipping insurance.In summary, stablecoin payment channels can energize markets that currently rely on archaic cash or bank wire transfer processes, and startups focused on this can create value by solving specific pain points in these market segments (speed, trust, global reach).

Rotating Savings Clubs and Expatriate Families

In many cultures, community savings circles (such as mutual aid societies, savings mutuals, etc.) are popular – members send money into a pool and take turns receiving the proceeds.Expatriates abroad also often send remittances home to support their loved ones.Traditional methods of sending money are inefficient: remittance fees are high and cross-border savings are difficult to coordinate using cash or bank transfers.Stablecoins provide an opportunity to standardize and simplify community finance.For example, a financial technology application allows friends from different countries to use US dollar stable coins to form a savings circle.Each member’s monthly deposit is a stablecoin transfer (almost free and instant), and the fund pool is transparently saved in the smart contract, which will transfer one-time income to each member’s wallet in turn as planned.This both reduces losses due to fees (more funds flow to members) and increases transparency (all deposits and expenditures are openly and transparently recorded on-chain).

Likewise, diaspora users can pool funds to support community projects back home, knowing that stablecoins are more resistant to inflation than local currencies.Such applications can make money by charging a small management fee or by holding a pool of funds in a yield-generating stablecoin account during the cycle.Key improvements are in convenience and trust – people without formal bank accounts can participate with just a mobile wallet, and they don’t need to rely on a certain “cashkeeper” in the group to manage their money.Additionally, stablecoins can bypass some country restrictions: for example, if a family in country A wants to send money to relatives in country B, which is subject to sanctions or is economically unstable, traditional remittance channels may be blocked, but a well-designed stablecoin solution (that complies with the regulations of the country of origin) can still get aid directly to those in need.We have seen NGOs use USDC to deliver humanitarian aid to recipients in areas of economic collapse precisely because it is faster and more reliable than correspondent banking.Consumer-focused fintech companies can apply the same concept to ordinary people, providing a faster, more affordable, and more transparent way to get things done that communities have long done informally.

What areas should stablecoin entrepreneurs and investors pay attention to currently?

In view of the above, what types of companies and products should founders and investors pay attention to in the stablecoin era?This does not promote any specific company, but can highlight some promising areas of opportunity in the FinTech 3.0 era.

Vertical neobank based on stablecoins

Essentially, this kind of digital banking or financial application is tailored for a specific group of people but operates on stablecoins.For example, it could be a wallet + bank card for remote freelancers, foreign gig workers or regional expats, with all internal transfers using stablecoins for speed.This new type of bank could offer multi-currency accounts (based on stablecoins), allowing users to hold and send U.S. dollars without requiring a U.S. bank account.The advantage over traditional neobanks is that cross-border transaction costs are significantly reduced, as stablecoins can provide near-free foreign exchange and instant transfers.This business model can be profitable through transaction fees (by linking bank cards), subscription fees for premium services, or loans (for example, by providing small advances or lines of credit after trust is established).

B2B cross-border payment tools for small and medium-sized enterprises

This includes building software for businesses that uses stablecoins under the hood to enable cheaper and faster cross-border payments.Imagine an accounts payable tool for import and export businesses that could automatically convert invoices into stablecoin payments, handle money management (such as converting part of the receivable into local currency and hedging if necessary), and even provide financing services.By combining on-chain settlement with a user-familiar interface, these tools can significantly reduce payment times and foreign exchange costs for SMEs engaged in global trade.Another direction is on-chain invoice factoring or trade finance, where the platform provides liquidity by paying a business’s invoices in stablecoins up front and then leverages smart contracts to collect payments from counterparties, thereby ensuring the execution of transactions.With stablecoin payment channels, even short-term credit can be issued more easily across borders because the collateral can be on-chain and payments are instant.Such fintech solutions can make money through invoice discounts, subscription fees or foreign exchange spreads, and they solve an obvious pain point: small businesses often face cash flow shortages due to slow international payments.

Infrastructure connecting stablecoins and banks

Although FinTech 3.0 is all about building new payment rails, in reality the world will remain a hybrid model for some time – stablecoins need to be connected to the banking system and vice versa.This creates opportunities for companies that provide “stablecoins as a service” to banks, payment service providers (PSPs), payroll processors and markets.For example, an API platform could allow any fintech company or bank to easily pay via stablecoin or receive stablecoin deposits, and present all the complex blockchain technology under a simple interface.We are already seeing some initial progress: some banks, such as Cross River, are launching services to unify fiat and stablecoin funding flows for their fintech clients.A startup could also become the Stripe of stablecoin payments, taking care of compliance, chain selection, and conversion.Its revenue source can be API usage fees or a percentage of transaction volume.This type of infrastructure development can accelerate the adoption of stablecoins by making it easy for traditional institutions to use stablecoins.They effectively solve interoperability challenges, ensuring that stablecoin rails can connect with existing ledgers and payment methods (ACH, SWIFT, etc.) without each institution having to build it from scratch.

Stable currency issuance platform for enterprises and specific industries

As stablecoins gain popularity, we may see large businesses, brands, and even governments looking to have their own stablecoins or tokenized deposits for specific purposes.Fintech companies can develop toolkits to help other institutions issue and manage digital tokens with stable value.For example, a platform could help retail brands issue USD-backed loyalty tokens that also serve as a method of payment for their stores (similar to a fully reserved private stablecoin).Alternatively, commodity producers could issue tokens (an asset-backed stablecoin used for settlement of transactions) that are redeemable for a certain amount of the commodity.These issuers require technical support (smart contract issuance, reserve management dashboards, compliance controls) and may require ongoing management services.Fintech companies in this space can charge setup fees, advisory fees, and transaction fees for the token’s continued circulation.Essentially, this is a “stablecoin white label” service – lowering the barrier to entry for specific issuers.Not every company will need its own token, but those with large ecosystems (such as Amazon gift card balances or airline miles) may find value in branded stablecoins in improving customer engagement or financial efficiency.Helping businesses create such stablecoins safely and compliantly is a niche worth exploring, especially as regulations clarify the rules for new entrants.

Stablecoin financial compliance and identity verification solutions

One of the risks hindering institutional adoption of stablecoins is complying with anti-money laundering (AML), know-your-customer (KYC), tax laws and similar regulations when using open blockchain systems.Tools need to be developed that allow businesses and regulators to “see clearly” the flow of stablecoins while ensuring their security without unduly infringing on user privacy.Possible options include on-chain identity frameworks (enabling wallets to host certified identity information or risk scores), advanced analytics tools for detecting illicit activity in stablecoin transactions, and reporting tools that integrate companies’ on-chain transactions into their regular compliance and accounting systems.For example, a fintech company focused on this could provide compliance officers with a dashboard showing every stablecoin payment, counterparty (perhaps with identity verification via NFT-based credentials), and flags for any risk patterns.Alternatively, a travel rule compliance solution could be considered where required, transmitting the necessary sender/receiver information along with the blockchain transaction.As stablecoins go mainstream, regulators will demand standards, so building middleware that meets regulatory requirements while retaining the openness that makes stablecoins attractive is critical and potentially lucrative.The source of revenue can be a software as a service (SaaS) model or transaction fees for compliance processing.Essentially, these are key elements to ensure that FinTech 3.0 can operate within the legal framework.Those who can overcome the challenges of integrating on-chain privacy and off-chain compliance will be highly sought after.

Constraints, risks and why this transformation is still in its early stages

The legal status of stablecoins and digital assets varies by jurisdiction.Some countries have clear frameworks (such as the EU’s Crypto Market Structure Act MiCA, which treats certain stablecoins as electronic currencies), while others (such as the United States, as of mid-2025) are still debating federal stablecoin legislation.This uncertainty may prevent institutions from fully adopting stablecoin payment systems until the relevant rules are finalized.Additionally, a startup operating globally must navigate a labyrinth of regulations: What is permitted in one country (such as offering USD stablecoin accounts) may be restricted in another.There are risks with regulatory crackdowns; sudden bans or new requirements could upend business models.Builders of FinTech 3.0 will need strong compliance strategies, and until the laws are perfected, they will likely operate in a hybrid model (stablecoins in a permissive environment, fiat by default when necessary).The good news is that the current trend is generally toward clearer regulation, not the other way around.For example, in the United States, the GENIUS Act and others aim to provide regulatory and reserve standards for payment stablecoins.However, navigating the complex legal environment remains a huge challenge.

Stablecoin trust and technical risks

Stablecoins carry inherent risks, and fintech companies must properly manage these risks.Users and businesses must trust that stablecoins are indeed backed by fiat currency and can be converted into fiat currency.Any crisis of confidence (e.g., a de-anchoring event or issuer bankruptcy) could destroy its value proposition.Although the largest stablecoins have always maintained their peg to fiat currencies, there have been some failed stablecoin cases in history.Fintech companies should probably diversify their support for multiple reputable stablecoins and develop contingency plans (for example, if there is a problem with one stablecoin, users can quickly switch to other stablecoins).From a technical perspective, building systems based on blockchain infrastructure introduces smart contracts and cybersecurity risks.If not properly guarded against, hacker attacks or vulnerabilities can result in the loss of funds.Additionally, there is the issue of scalability: If a fintech company scales to millions of users, can its chosen blockchain handle such massive transaction volumes without incurring high fees or slowdowns?Emerging solutions (e.g. L2 networks, new protocols) are working to solve this problem, but this is still an evolving area.In essence, stablecoin fintech companies must be both financiers and technologists, dealing with issues that were once handled abstractly by banks (such as settlement finality, fraud prevention, and funding guarantees) but are now being addressed at the protocol level.

User experience gap

Although technology continues to advance, for the average user, using stablecoins and crypto wallets is still not as convenient as using banking apps.Managing private keys, dealing with wallet addresses, and understanding network fees can all be daunting.The success of FinTech 3.0 depends on the ability to integrate the complexity of blockchain into a familiar and user-friendly interface.This means huge investments in design, education, and customer support.In addition, the conversion of stablecoins (fiat currency into and out of accounts) must also be seamless.If target users had to figure out how to buy USDC on an exchange before they could use the app, they would lose a lot of potential customers.Many startups are working on building better access (for example, integrating local payment methods), but this is still a pain point, especially in emerging markets.Trust is another important aspect of user experience: emerging fintech companies must establish trust that customer funds are safe and easily accessible.Ironically, despite the transparency provided by blockchain, the average user may still worry about where their money is going if they don’t understand it is self-custody.We may see more regulated custodial wallets or insurance products to increase user peace of mind.In short, the work of building a bridge between crypto and the expectations of ordinary users is still a work in progress, and until this issue is resolved, stablecoin fintech companies may face slower adoption outside of early tech-savvy groups.

Existing players vs. hybrid model

Banks and card networks are not standing still, they are actively adapting (for example, Visa is piloting the use of USDC for payments, and JP Morgan has launched its own deposit token) and integrating the many advantages of stablecoins into their own products and services.In the short term, we will see hybrid payment systems.For example, a user might pay with a card, but backend settlement between merchant acquirers is done via stablecoins.If traditional financial institutions can successfully modernize their payment systems (even with blockchain technology underneath), they may offset the cost advantages of some emerging fintech companies.Additionally, they have brand credibility and a large user base.Fintech 3.0 startups must be prepared not only to face competition from other startups in the industry, but also to deal with the challenges of collaboration between large banks and large technology companies.The most likely scenario is coexistence: stablecoin payment systems will develop in parallel with ever-improving traditional payment systems such as fast payment networks and central bank digital currencies.This is not an overnight replacement.Therefore, emerging fintech companies must integrate with existing systems where necessary (to expand coverage) and focus on those market segments that are truly ignored by traditional institutions.The transition to a new payment system is a gradual process; if the front-end product meets user needs, many users may not even know or care that stablecoins are involved.We need patience and adaptability; the infrastructure revolution is underway, but it will go through a hybrid innovation phase.

Conclusion

Fintech 1.0 and 2.0 mainly rent space in banking infrastructure and are constrained by the rules and costs of banks and card networks.Fintech 3.0 based on stablecoins enables fintech companies to become part owners and rebuilders of infrastructure.Stablecoins and open blockchains create a more level playing field, allowing small teams to build cross-border value transfers that once required global banks, often faster and cheaper.

The most compelling opportunities are not universal wallets or payment apps, but products designed to fill specific gaps in legacy systems.Use cases such as freelance income, Islamic finance or SME trade show that digital dollar payment channels can provide convenience and efficiency that were previously unattainable.For investors, the key will be to watch how stablecoins evolve from trading tools into a broader payment and banking services layer.For developers, the challenge is to design products that are only possible based on a programmable, always-running currency, rather than simply porting old banking products to APIs.

Fintech 3.0 will coexist with traditional finance for many years, but the direction of development is already clear.Stablecoin infrastructure is expected to become a core component of global finance.The ultimate winners will be those who can combine the efficiencies of new rails with tangible solutions to real-world problems, and who are willing to take on the responsibility of operating critical financial infrastructure.