Author: Thejaswini, Source: Token Dispatch, Compiled by: Shaw Bitchain Vision

Every financial advisor you meet will give you the preaching of compound interest at the beginning.

Invest $500 a month to buy an index fund with an annualized rate of return of 7%, and you will have $1.3 million in 30 years.This sounds great, but by year 15, a $500 investment per month seems insignificant, because rents have doubled and children have, and your definition of “enough money” has changed from “affordable avocado” to “affordable school district housing.”The traditional path assumes that your overhead remains the same and your money grows slowly, but real life is exactly the opposite.

So when you learn that someone can earn 15% to 20% a year through the cryptocurrency derivatives market, the first thing you think about is not the risk, but the timeline.Finally, there is a return that can exceed the rate of increase in cost of living.

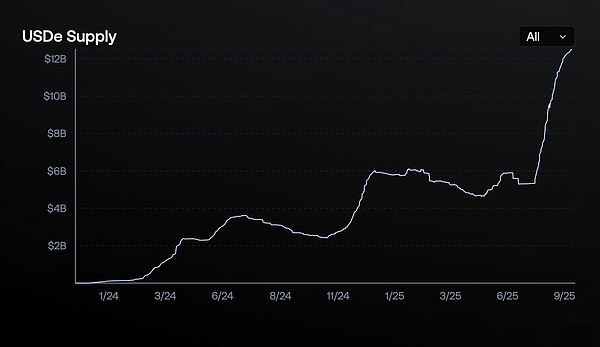

The following fact makes me want to explore in depth: an crypto protocol launched 18 months ago has exceeded US$12.4 billion in just a short period of time, which is faster than any digital dollar in history.Although USDT did not reach $12 billion until mid-2020 (experienced years of slow growth), and USDC did not exceed $10 billion until March 2021, Ethena’s USDe surpassed these two milestones in a short period of time, which can be regarded as a speed race in the financial field.

USDe is taking advantage of structural inefficiencies in the crypto derivatives market.

This brings to the core questions that every investor, regulator and competitor is asking.

How did they do this so quickly?What are the actual risks?Is this sustainable?Or is it just waiting for another high-yield experiment to collapse?

I’m trying to answer most of these questions.

The world’s largest arbitrage transaction

Ethena found a way to convert the ongoing demand for leverage in the cryptocurrency market into a money printing machine.Simply put, it works as follows.

Hold cryptocurrency as collateral and short the same amount of cryptocurrency futures contracts to earn the difference.This will result in a stable synthetic dollar while gaining benefits from the most reliable money printers in cryptocurrencies.

Let’s analyze it further.When someone wants to mint USDe, they deposit crypto assets like Ethereum or Bitcoin.But Ethena doesn’t just hold these assets and hope they stay stable (oh, by the way, they won’t), but will immediately open short positions of the same size on the perpetual contract exchange.

If ETH rises $100, their spot position will increase by $100, but their short contract position will lose $100.

If ETH falls $500, their spot position will lose $500, but their short contract will make a profit of $500.

Final result – perfect stability in US dollars.

This is called Delta neutral position.You won’t lose money because of price fluctuations, but you won’t make a profit either.

So where does the yield of 12%-20% come from?There are three sources.

first, they pledge ETH collateral and receive pledge rewards (currently about 3%-4%).

Second, They charge what are called “funding rates” from short contracts.

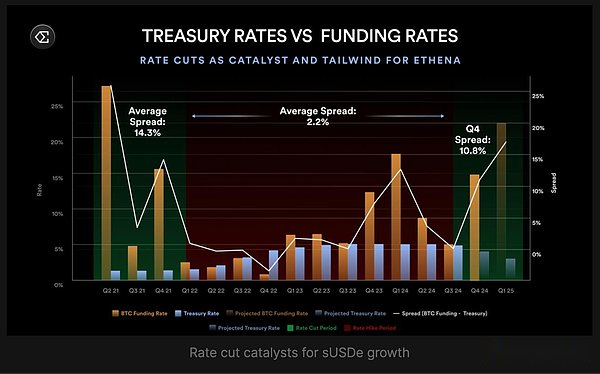

In a cryptocurrency perpetual contract, traders pay funds every eight hours to maintain positions.When there are more people who are long than those who are short (about 85% of this case), the longs will pay the shorts.Ethena is always on the short side and charges these fees.

In 2024, Bitcoin’s open weighted funding rate averaged 11%, while Ethereum averaged 12.6%.These are the actual cash flow that leveraged traders pay to anyone willing to bet with.

third, they can earn from cash equivalents and Treasury products they hold in their reserves.Ethena holds liquidity-stable assets with partners that pay additional revenue.USDC pays loyalty rewards, and holding USDtb can earn benefits from BlackRock’s BUIDL fund.

Overall, these funding sources have created an average annualized rate of return of 19% for sUSDe holders in 2024.

In the past few years, the cryptocurrency funding rate has remained at 8-11% annually.Add pledge rewards and other sources of income and you can get enough benefits to give you peace of mind.Isn’t this the key?

The Ethena ecosystem is powered by four tokens, each with different features:

USDe is a synthetic dollar unit, maintain a target price of $1 through Delta neutral hedging.Unless pledged, no reward is generated and USDe can only be minted or redeemed by whitelisted participants.

sUSDe is a revenue token obtained by pledging USDe to the ERC-4626 protocol vault.Currently, all revenue from the Ethena Agreement flows to sUSDe holders in the form of earnings rewards.As Ethena regularly deposits agreement revenue, its value (calculated in USDe) will also increase.Users can unsolicite and redeem USDe after the cooling period.

ENA as a governance token, allowing holders to vote on key agreement matters such as qualified mortgage assets and risk parameters.It also lays the foundation for future ecosystem security models.

sENA represents pledged ENA positions.The planned “fee conversion” mechanism will distribute part of the agreement revenue to sENA holders after a specific milestone is reached.Currently, sENA can obtain ecosystem allocations, such as Ethereal’s proposed 15% token allocation.

But there is a big trap here.This model works only if people are willing to spend money on cryptocurrencies.Once market sentiment reverses and the capital rate becomes negative, Ethena will start paying interest instead of gaining profits.

Why 2025 is Ethena’s breakthrough year

A combination of factors has made USDe the fastest growing digital dollar in history.

1. The perpetual futures contract market shows explosive growth, the open interest contracts of major altcoins hit a record high of about $47 billion in August 2025, and the open interest contracts of Bitcoin reached $81 billion.The increase in transaction volume means Ethena has more opportunities to obtain funding rate returns.

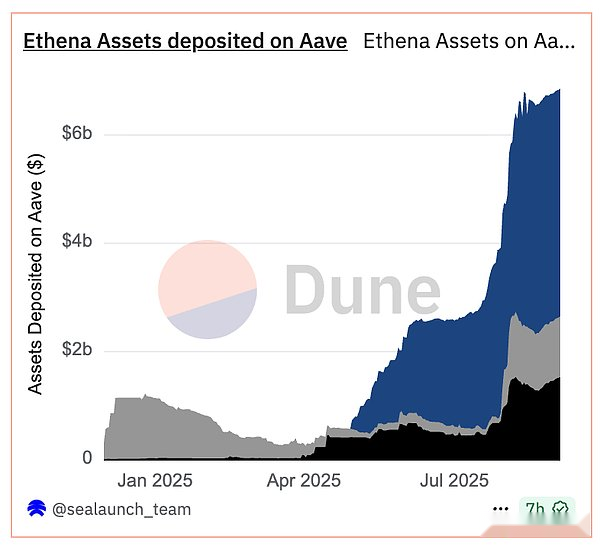

2. This accelerated development originated from a financial project that can be called a “strengthening version”.Users found that they can pledge USDe to obtain sUSDe (yield type), then tokenize sUSDe positions on Pendle (a income derivative platform), and then use these tokenized positions as collateral on Aave (a lending agreement) to borrow more USDe.This cycle goes on and on.

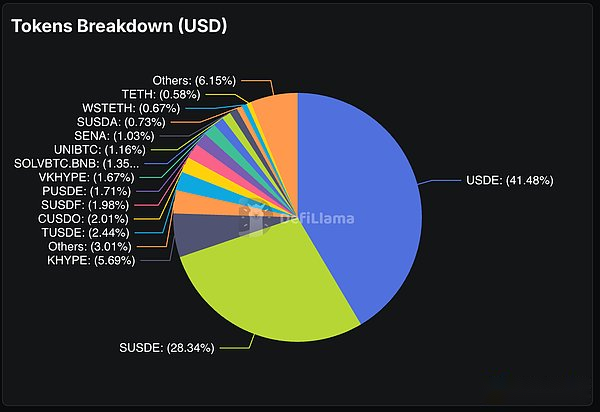

This creates a recursive benefit cycle where experienced players can amplify their exposure to potential USDe benefits.What is the result?70% of Pendle’s total deposit is Ethena assets.

Another $6.6 billion worth of Ethena assets is located on the Aave platform.

This layer of leverage is all chasing those double-digit yields.

3. The family name isStablecoinX’s Special Purpose Acquisition Company (SPAC) announces plans to raise $360 million specifically to accumulate ENA tokens.The entity will use the proceeds to accumulate ENA tokens under the Permanent Capital mandate, creating a structural buyer that eliminates selling pressure and supports governance decentralization.

4. Ethereal permanent decentralized exchange.Ethereal is built specifically on USDe, attracting $1 billion in total lock value (TVL) before the mainnet went online.Users deposit USDe to obtain points for the final token issuance, which creates another huge consumption for the USDe supply, and also stimulates people’s expectations for the first large-scale application built natively on the Ethena infrastructure.

5. The licensed L2 convergence chain built by Ethena and Securities aims to enable the introduction of traditional finance through infrastructure that complies with KYC standards..This chain uses USDe as a native fee token, while creating structural demand, it also opens up access to institutional capital that cannot interact with non-licensed DeFi.

6. The market expects the Federal Reserve to cut interest rates twice by the end of 2025, with the possibility of a rate cut in September being 80%..When interest rates fall, traders often increase risk-taking behavior, which drives up capital rates.USDe yields are negatively correlated with federal funds rates, which means a rate cut could significantly increase Ethena’s revenue.

7. Ethena’s fee conversion proposal.Ethena governance has approved a five-metric framework for activating revenue sharing with ENA holders.Among them, four of the following five conditions have been met:

USDe supply exceeds $6 billion (currently $12.4 billion), protocol revenue exceeds $250 million (has achieved over $500 million), Binance/OKX integration (has achieved), and sufficient reserve funds (has achieved).The last requirement – the rate-of-yield spread to maintain sUSDe by at least 5% higher than sUSDtb – is still the only obstacle for ENA holders to obtain a share of the agreed profits.

These conditions are safeguards for governance decisions designed to protect agreements and sENA holders from premature or risky benefits allocations.Milestones reflect the benchmarks for agreement maturity, financial status and market integration.Ethena wants to ensure its sustainability and value before fully unlocking its profit distribution.

Ethena has also been quietly building partnerships with traditional financial enterprises and cryptocurrency exchanges, allowing USDe to be used anywhere from Coinbase to Telegram wallets.

Institutional-level FOMO

Unlike previous stablecoin experiments that have developed purely through crypto-native use cases, USDe is attracting the attention of traditional financial institutions.

Coinbase’s institutional clients can now directly obtain USDe.CoinList provides USDe with a 12% annualized rate through its earnings program.Major custodians such as Copper and Cobo are managing Ethena’s reserves.

They are all related to institutional investors because they provide a platform, hosting or service designed specifically to support qualified investors and institutional clients in the crypto market.

This pattern is similar to the case with USDC and USDT, but the time span is much shorter.It took several years for major stablecoin providers to establish institutional relationships and compliance frameworks.Ethena was completed in just a few months, partly because the regulatory environment is mature, partly because its profit opportunities are too tempting and cannot be ignored.

Institutional adoption brings credibility, credibility brings more funds, and more funds means higher capital rates to capture, thereby supporting higher returns and ultimately attracting more institutions.As long as the underlying mechanism remains the same, it is like a flywheel that will continue to accelerate.

There are important prerequisites for this comparison of speed.USDe does not need to prove to the world the practicality, security or legitimacy of stablecoins.In the market it entered, USDT and USDC have already undertaken heavy responsibilities in institutional adoption, regulatory recognition and infrastructure construction.

Leverage Square

The high concentration of Pendle and Aave has caused what risk managers call a single point of failure scenario.If there is a problem with Ethena’s model, it will affect not only USDe holders, but also the entire DeFi ecosystem that relies on Ethena’s capital flow..

If there is a problem with Ethena, Pendle will lose 70% of its business.Aave will face a large-scale capital outflow.The profit strategy that relies on USDe will fail.We will face liquidity tightening throughout the DeFi system, not just the decoupling of stablecoins.

The most worrying aspect of Ethena’s development is how people use it.The recursive lending cycle on Aave and Pendle produces leverage multipliers, amplifying returns and risks.

Users pledge USDe as sUSDe, tokenize sUSDe on Pendle to obtain PT tokens, deposit PT tokens on Aave as collateral, and borrow more USDes, which goes on a cycle.Each cycle will amplify their exposure to USDe’s underlying returns, and will also amplify their exposure to any volatility or liquidity issues.

This reminds us of the CDO square structure that led to the 2008 financial crisis.A financial product (USDe) is used as collateral to borrow more funds, thus creating recursive leverage that is difficult to quickly remove.

Maybe I’m just thinking too much, but if the funding rate continues to be negative, USDe may face redemption pressure.Leveraged positions will face the requirement of additional margin.Protocols that rely on USDe Total Locked Value (TVL) will face large-scale capital outflows.Close positions may be faster than any single agreement can handle.

Every high-yield strategy ends up with a question: What happens when it fails?For Ethena, there are several situations that may trigger a closing position.

The most obvious situation is the continuous negative funding rate.If cryptocurrency market sentiment continues to bearish for weeks or months, Ethena will start paying for funds instead of collecting funds.Their reserves (currently around $60 million) provide some buffering, but not unlimited.

The more severe risk is the bankruptcy of the counterparty.While Ethena uses off-market custody of its spot assets, they still rely on large exchanges to maintain their short contracts.If the exchange goes bankrupt or is hacked, Ethena needs to quickly transfer contract positions, which could temporarily break its delta neutral hedge.

Aave and Pendle’s leverage cycle brings additional liquidation risk.If USDe’s yield suddenly drops, recursive lending positions may become unprofitable, triggering waves of deleveraging liquidation.This may put temporary selling pressure on USDe itself.

Regulatory risks are also increasing.European regulators have forced Ethena to move from Germany to the British Virgin Islands.As income stablecoins gain more attention, they may face more compliance requirements or restrictions.

Stablecoin Battle

Ethena represents a fundamental change in the stablecoin competition landscape.For years, the focus of this competition has been on stability, applicability and compliance.USDC competes with USDT in terms of transparency and regulation.Various algorithmic stablecoins compete with each other in decentralization.

USDe changes the rules of the game through rate of return.It is the first mainstream stablecoin to provide double-digit returns for holders while remaining pegged to the dollar.This puts pressure on traditional stablecoin issuers competing with it, who can only retain the full gains of the U.S. Treasury bonds they hold, but cannot provide any return to users.

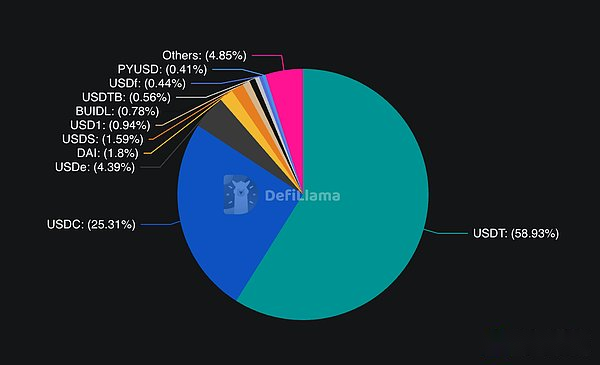

The market is reacting.USDe currently has more than 4% of the market share in stablecoins, second only to USDC (25%) and USDT (58%).More importantly, it grows faster than both.USDT has grown by 39.5% in the past 12 months, USDC has grown by 87%, but USDe has grown by more than 200%.

If this trend continues, we may see a fundamental reshaping of the stablecoin market.Users will move from zero-yield stablecoins to profitable alternatives.

Traditional publishers either have to share their earnings with their users or watch their market share be eaten up.

Despite the risks, Ethena’s momentum shows no sign of slowing down.The agreement has just approved BNB as qualified collateral, and XRP and HYPE tokens have also reached the threshold for future inclusion.This will expand its potential market beyond Ethereum and Bitcoin.

The ultimate test is whether Ethena can manage systemic risks while maintaining its profit advantage.If they can, they will create the first scalable, sustainable income dollar in cryptocurrency history.If it cannot be done, we will see again the dangerous story of chasing profits in a turbulent market.

Anyway, USDe reaches a rate of $12 billion,When real innovation is combined with market demand, the development speed of financial products can exceed anyone’s imagination.