Author: Pillage Capital; Source: X, @PillageCapital; Compiler: Shaw Bitcoin Vision

Bitcoin was never the future of money.It is just a battering ram in the regulatory wars.Now that this war is coming to an end, the funds supporting the development of Bitcoin are also quietly withdrawing.

For 17 years, we have firmly believed that magical Internet currency is the ultimate form of finance.This is not the case.Bitcoin is a regulatory battering ram, a battering ram built specifically to destroy a specific barrier: a state’s refusal to tolerate digital holdings of assets.

The work is basically complete.Tokenized U.S. stocks are already being issued.Tokenized gold is legal and growing.The market capitalization of tokenized U.S. dollars has reached hundreds of billions of dollars.

In wartime, a battering ram is a priceless treasure; in peacetime, it is just a bulky and expensive antique.

As the financial system upgrades and legitimizes, the Bitcoin “Gold 2.0” narrative is collapsing, returning to what we really wanted in the 1990s: tokenized claims to real assets.

1. Bitcoin’s past life: E-gold

To understand why Bitcoin is becoming obsolete, you must understand why it was created.It has not been smooth sailing, but was born in the shadow of repeated failures of digital currencies.

In 1996, E-gold was launched.By the mid-2000s, it had about 5 million accounts with billions of dollars in trading volume.This proves something important: the world needs digital assets backed by physical value.However, the state killed it.

In December 2005, the FBI raided E-gold.In July 2008, its founder pleaded guilty.The message is clear: destroying a centralized digital gold currency is easy.Just knock on a door, seize a server, prosecute a person, and it’s over.

Three months later, in October 2008, Satoshi Nakamoto published the Bitcoin white paper.He had been thinking about these issues for many years before that.He once pointed out in his article that the fundamental flaw of traditional currencies and early digital currencies is that they place too much trust in central banks and commercial banks.And experiments like E-gold show how easy it is to attack these trust points.

Satoshi Nakamoto saw a real innovation in digital currency stifled.If you want digital assets to survive, you can’t let them be killed easily.

Bitcoin was designed to eliminate the attack vectors that led to the collapse of E-gold.It does not aim at efficiency but at survivability.

2. The Regulatory War: The Necessary Illusion

In the early days, getting users into Bitcoin was almost like magic.We just tell them to download a wallet to their phone.When the first batch of Bitcoins arrived, you could see their aha moment.It’s as if they open a financial account and receive value instantly, without any permissions, without any documentation, and without any regulatory agencies.

It was a slap in the face.The banking system suddenly looked archaic.Only then do you realize that you have been suppressed before, but you didn’t know it.

At the Money 20/20 conference in Las Vegas, a speaker displayed a QR code on a big screen and a Bitcoin raffle was held live.Viewers send Bitcoin and the prize pool is built up in real time.A guy next to me who was in traditional finance came up to me and told me that this speaker had just broken about fifteen laws.He may be right.But no one cares.That’s exactly the point.

This is not just a financial issue, it is a rebellion.One of the #1 posts on Reddit in the early days of Bitcoin captured the sentiment perfectly: Buy Bitcoin because “it’s a slap in the face to the scammers and thieves who are trying to steal my hard-earned money.”

This self-financing mechanism is perfect.By fighting for the cause, posting, promoting, debating, and recruiting new members, you directly increase the value of the tokens in your own wallet and the wallets of your friends.This revolution has many benefits for you.

Because the network cannot be shut down, it continues to grow after every crackdown and negative publicity.Over time, everyone started acting as if Magic Internet Money was the real goal and not a stopgap measure.

The delusion has grown so strong that mainstream institutions are playing along.BlackRock applies to issue Bitcoin ETF.The President of the United States discusses Bitcoin as a reserve asset.Pension funds and universities are investing in Bitcoin.Michael Thaler convinced convertible bond buyers and shareholders to fund the company’s multibillion-dollar Bitcoin purchase.The scale of mining continues to expand, and its power consumption is even comparable to that of medium-sized countries.

Finally, with more than half of campaign funding coming from cryptocurrencies, the calls for cryptocurrency legalization are finally being heard.Ironically, the government’s crackdown on banks and payment processors has instead spawned a three-trillion-dollar behemoth that has forced the government to its knees.

3. The Road to Success: Profits Ruin the Deal

Infrastructure upgrades, monopoly breaks

Bitcoin’s advantage has never been just censorship resistance, but monopoly status.

For years, Bitcoin was the only option if you wanted tokenized holding value.Accounts were closed and fintech companies feared regulators.If you want the benefits of instant, programmable money, you have to accept Bitcoin’s full terms.

So we just accepted it.We loved it and supported it because there was no other option.

That era is over.

You can see what happens when there are multiple trading channels available by looking at Tether (USDT).USDT was originally issued on Bitcoin trading channels, and later most of the circulation moved to Ethereum because Ethereum had lower fees and was easier to use.When Ethereum’s fees skyrocketed, retail investors and emerging markets turned to Tron for issuance.Same dollar, same issuer, different trading channels.

Stablecoins are not loyal to any blockchain.They view blockchain as a disposable channel.Assets and issuance are the key; channels are simply a combination of cost, reliability, and connectivity to the rest of the system.In this sense, the “Blockchain not Bitcoin” camp actually wins.

In its early days, horse-drawn carriages were widely used to ridicule banks’ reports on blockchain technology.

Once you understand this, Bitcoin is in a very different position.When there is only one channel, and all assets are forced to depend on it, you can confuse the value of the asset with the value of the channel.And when there are many channels, value will flow to those channels with the lowest cost and the most convenient connection.

This is where we are now.With the exception of the United States, most of the world’s population can now hold tokenized interests in U.S. stocks.Perpetual futures, once the killer application of cryptocurrencies, are being copied domestically by physical exchanges such as the Chicago Mercantile Exchange (CME).Banks have also begun to open USDT deposit and withdrawal services.Coinbase is moving toward a hybrid bank and brokerage account where users can send money, write checks, and buy stocks while holding cryptocurrencies.The network effects that once protected Bitcoin’s monopoly are slowly breaking down, replaced by a universal network infrastructure.

Once the monopoly is broken, Bitcoin is no longer the only way to earn profits.It will be reduced to one product among many, competing against regulated, high-quality goods and services that are closer to what people really want in the first place.

Technology reality check

During the war, we ignored a simple fact: Bitcoin is a terrible payment system.

We still move money by scanning QR codes and pasting long strings of meaningless character information.There is no standardized username.Transferring funds across levels and chains is as difficult as breaking through a barrier.Once you can’t figure out which address corresponds to which account, your money will be wasted forever.

“Future Currency”

By 2017, Bitcoin transfer fees soared to nearly $100.A Bitcoin cafe in Prague had to accept Litecoin in order to stay afloat.When I had dinner in Las Vegas, it took half an hour to check out with Bitcoin because people were scrambling with their mobile wallets and the transaction kept getting stuck.

Even today, wallets often suffer from some basic glitches.Balances didn’t show up, transactions got stuck, and people sent money to the wrong addresses, resulting in lost funds.In the early days, nearly everyone who received gifted Bitcoin lost it.I personally have lost more than a thousand Bitcoins.This is the norm in the cryptocurrency space.

Pure on-chain finance is very scary to apply on a large scale.People click the “Sign” button in their browsers and they simply can’t read and understand the code.An operation as complex as Bybit can still be hacked and lose billions of dollars with no effective recourse.

We told ourselves that these user experience issues were temporary pain.Ten years later, the real improvement in user experience comes not from some elegant protocol, but from a centralized custodian.They provide people with access to passwords, account recovery, and fiat currencies.

From a technical perspective, this is the crux of the matter.Bitcoin never learned how to actually work without recreating the very middlemen it purported to replace.

Trading is no longer worth the risk.

Once infrastructure improves elsewhere, all that’s left is trading.

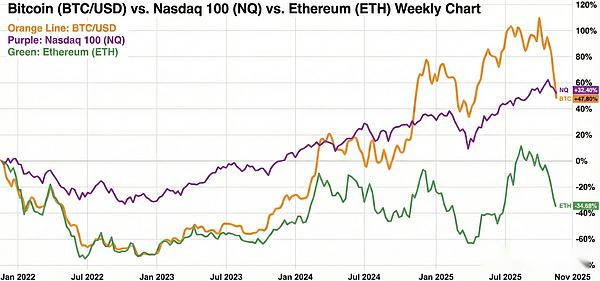

Look at the returns over the past four years (one full cryptocurrency cycle).The Nasdaq outperformed Bitcoin.You take on existential regulatory risk, accept heavy drawdowns, endure constant hacks and exchange failures, and your returns are worse than a common tech index.The risk premium has disappeared.

Ethereum’s situation is even worse.The part that was supposed to give you the most bang for your buck now becomes a direct drag on performance, while the boring index only slowly rises.

Part of the problem is structural.There is a large group of early holders whose entire net worth is in cryptocurrencies.Now they are older, have families, real expenses, and a normal desire to reduce risk.They sell some coins every month to maintain a wealthy and normal life.Thousands of holders sell off every month, which adds up to billions in “living expenses” sales.

New inflows are a different story.ETF buyers and wealth managers mostly make 1% or 2% allocations just for compliance checking purposes.While these funds are stable, they are not aggressive.These modest allocations not only have to contend with ongoing sell-offs from early holders, but also exchange fees, new coins issued by miners, scam tokens, and hacker attacks in order to barely keep the price from falling.

Gone are the days when huge gains could be made by taking on regulatory risks.

Developers smell stagnation

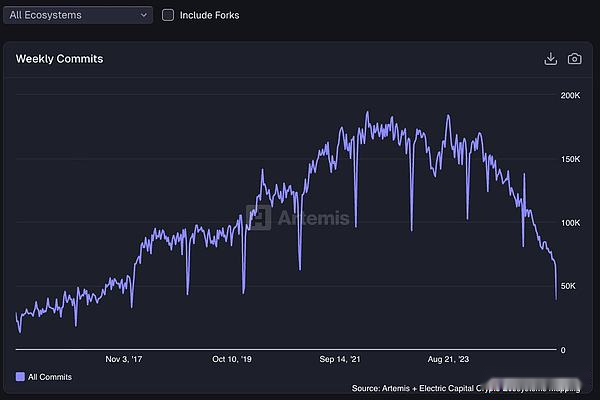

Developers are not stupid.They can detect signs that technology is losing its edge.Developer activity has plummeted to 2017 levels.

Weekly developer commit records across all ecosystems

Meanwhile, the codebase has effectively ossified.Decentralized systems are designed to be difficult to change.Ambitious engineers who once viewed cryptocurrency as a cutting-edge field have now moved on to robotics, aerospace, artificial intelligence and other fields where they can do more exciting things than just tinker with numbers.

If deals are bad, user experience is worse, and talent is being lost, the path ahead is not hard to foresee.

4. Error correction mechanism is better than pure decentralization

Decentralization believers tell a simple story: code is law, currency is uncensorable, and no one can block or reverse transactions.

Most people don’t actually want that.What they want is infrastructure that works well, and they want someone to fix it when something goes wrong.

This can be seen in the way people treat Tether.When funds were stolen by North Korean hackers, Tether froze those balances.If someone mistakenly sends a large amount of USDT to a contract address or a burn address, Tether will blacklist the frozen tokens and mint new tokens to the correct address, as long as they can still sign from the original wallet, complete KYC verification, and pay fees.While there is some paperwork and time delays involved, at least there is a process and there is management who can admit the mistake and fix it.

That’s counterparty risk, but it’s also the risk that people value.If you suffer losses due to technical glitches or hacker attacks, there is at least hope of recovery.This is not the case with on-chain Bitcoin.If you enter the wrong address or sign the wrong transaction, the losses are permanent.No appeals, no customer service, and no second chances.

Our entire legal system is built on diametrically opposed intuitions.The courts have an appeals process.The judge can overturn the verdict.Governors and presidents can pardon criminals.The bankruptcy system exists to prevent one wrong decision from completely ruining a person’s life.We like to live in a world where obvious wrongs can be corrected.No one really wants a system flaw like the Parity multi-signature flaw, which resulted in $150 million in Polkadot funds being frozen, and everyone to just shrug and say “code is law.”

We also have much more trust in issuers now than in the early days.Back then, “regulation” meant early cryptocurrency businesses losing their bank accounts because banks feared regulators would revoke their banking licenses.We’ve watched as some crypto-friendly banks collapsed in just one weekend.The government feels more like executioner than referee.Today, the same regulatory mechanisms serve as safety nets.It forces disclosure, brings issuers into the audit framework, and gives politicians and courts the power to punish outright theft.Cryptocurrency and political power are now so closely intertwined that regulators can’t just destroy the entire space; they have to regulate it.This makes coexisting with the risks of issuers and regulators much more sensible than living in a world where a lost mnemonic phrase or a malicious signature hint could leave you bankrupt and unable to recover.

No one really wants a completely unregulated financial system.A decade ago, a broken regulatory system made unregulated chaos look attractive.But as regulatory systems modernized and became more powerful, this trade-off reversed.People’s preferences are clear.People want strong infrastructure, but they also want referees on the field.

5. From “magical Internet currency” to tokenized real assets

Bitcoin has accomplished its mission.It was like a hammer blow that broke down the barriers that had held back E-gold and all similar attempts.It makes a permanent ban on tokenized assets politically and socially impossible.But this victory also brought with it a paradox: When the system finally agreed to upgrade, the high value of this hammer disappeared.

Cryptocurrencies still have their place, but we no longer need a three-trillion-dollar rebel army.Hyperliquid only needed 11 employees to develop prototype functionality and force regulators to respond.Once a feature works well in a test environment, Traditional Finance (TradFi) replicates it with a regulatory-compliant shell.

Today, the main strategy is no longer to put the majority of your net worth into a “magic internet currency” for a decade and hope it appreciates in value.This approach only makes sense if the financial system collapses and the prospects for gains are extremely promising.“Magic Internet money” has always been a strange compromise: a flawless financial system wrapped around an asset backed only by a story.In subsequent articles, we will explore what happens when these financial systems carry claims to assets that are truly scarce in the real world.

Capital is already adjusting.Even cryptocurrencies’ unofficial central banks are shifting.Tether already has more gold holdings on its balance sheet than Bitcoin.Tokenized gold and other real-world assets are growing rapidly.

The era of “magic internet money” is coming to an end.The era of tokenized real assets is beginning.Now that the door is open, we can stop worshiping Bitcoin and start looking at the assets and transactions that really matter on the other side.