Author: Tanay Ved, Source: Coin Metrics, Compiler: Shaw Bitcoin Vision

Summary of key points

-

Recently,Demand from major absorption channels such as ETFs and DATs has weakened, while October’s deleveraging and macro-level risk aversion continue to put pressure on the digital asset market.

-

Leverage in futures and DeFi lending markets has been reset, making positions clearer and reducing systemic risk.

-

The spot liquidity of mainstream coins and altcoins has not yet recovered, causing the market to remain fragile and more prone to large price fluctuations.

Introduction

“Uptober” got off to a strong start as Bitcoin climbed all the way to new all-time highs.But October’s flash crash quickly dampened market sentiment, and optimism faded.Since then, the price of Bitcoin has dropped by about $40,000 (more than 33%), while altcoins have also suffered heavy losses, causing the total market value of the crypto market to shrink to nearly $3 trillion.While fundamentals have developed well over the past year, price action has diverged significantly from market sentiment.

Digital assets appear to be at the intersection of multiple external and internal factors.Macroscopically,Uncertainty over a December rate cut and recent weakness in technology stocks have fueled risk aversion.In the field of cryptocurrency,Demand channels such as exchange-traded funds (ETFs) and digital asset treasuries (DATs) originally played a stable role in attracting funds, but now they are also experiencing capital outflows and pressure on the cost base..At the same time, the impact of the wave of liquidations caused by a round of violent deleveraging events triggered on October 10 is still continuing.Market liquidity remains insufficient.

In this article, we’ll take a closer look at the drivers behind the recent weakness in the digital asset market.We will focus on ETF capital flows, leverage conditions in perpetual futures and decentralized finance (DeFi) markets, and order book liquidity to explore the implications of these changes for the current market landscape.

The macro environment shifts to risk aversion

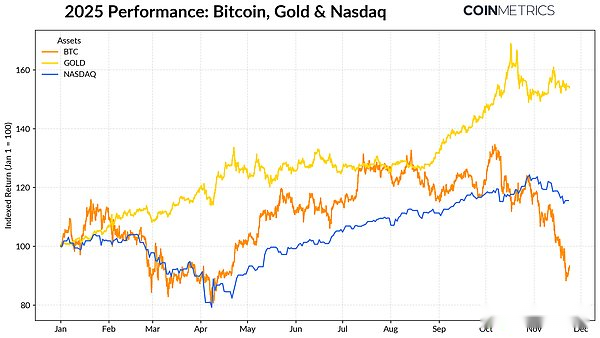

Bitcoin’s performance increasingly diverges from mainstream asset classes.Gold has soared, returning more than 50% year-to-date, on the back of record central bank buying and ongoing trade tensions, while tech stocks (Nasdaq) lost steam in the fourth quarter as the market reassessed the likelihood of imminent Fed rate cuts and the sustainability of AI-driven valuations.

As our previous research highlighted,Bitcoin typically has a volatile relationship with “risk-on” technology stocks and “risk-off” gold, which will change with the current macro environment.This makes Bitcoin particularly sensitive to market shocks or catalysts, such as October’s flash crash and the recent risk-off sentiment.

Source: Coin Metrics Reference Rates & Google Finance

As Bitcoin is a bellwether for the entire cryptocurrency market, its price decline has spread to other assets, which remain closely correlated with Bitcoin’s movements, although thematic sectors such as privacy briefly outperformed the market.

Absorption capacity of ETFs and DATs weakens

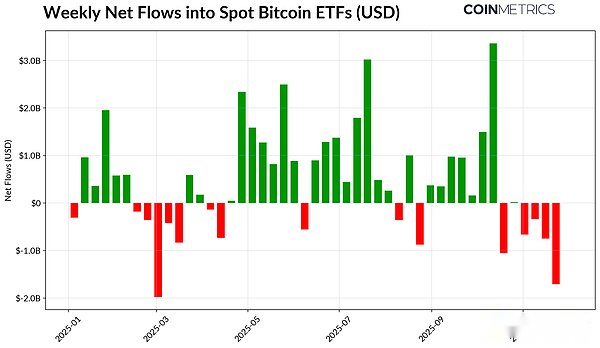

Part of Bitcoin’s recent weakness is due to reduced demand in the channels that supported its price strength through much of 2024 and 2025.Since mid-October, ETFs have experienced net outflows for several consecutive weeks, totaling $4.9 billion.This is the largest wave of redemptions since Bitcoin dropped to near $75,000 in April 2025 (before the “Liberation Day” tariff announcement).Despite short-term capital outflows, on-chain holdings continue to rise. BlackRock’s IBIT ETF alone holds 780,000 Bitcoins, accounting for approximately 60% of the current total supply of spot Bitcoin ETFs.

If funds continue to flow back, it would indicate a stabilization of the channel, as ETF demand has historically been a significant draw-in to supply when risk appetite improves.

Source: Coin Metrics Network Data Pro

DAT is also beginning to show stress.As prices retreated, the value of its shares and cryptocurrency holdings shrank, squeezing the NAV premium that underpinned its growth.This reduces their ability to raise capital through the issuance of equity or debt, limiting the growth of their per-share cryptocurrency holdings.Smaller, younger DATs are particularly vulnerable to this dynamic, as changes in market conditions can render cost bases and stock valuations unfavorable for further accumulation.

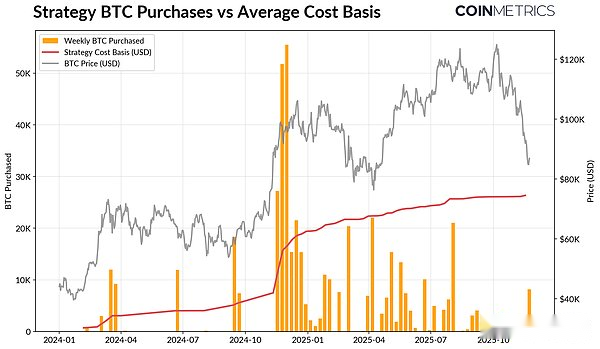

Strategy is currently the largest holder of Bitcoin DAT, with 649,870 Bitcoins (about 3.2% of the current Bitcoin supply), with an average purchase cost of $74,333.As shown in the chart below, when the price of Bitcoin rose and its asset valuation was strong, Strategy’s buying speed accelerated significantly, but it has slowed down recently and is not actively selling.Even so, Strategy is holding on to unrealized gains and its cost basis is below current market prices.

While Strategy could come under pressure if prices fall further or risk potential index delisting, a reversal in market conditions could bolster balance sheet strength and valuations, restoring an environment conducive to more aggressive DAT accumulation.

Source: Strategy & Bitbo Treasures

This seems to be in line with on-chain profitability trends.The realized profit-to-loss ratio (SOPR) for short-term holders (holding time less than 155 days) has fallen to a loss level of about 23%, a level that has historically reflected capitulation pressure from the most price-sensitive groups.Long-term holders are still in the black on average, but SOPR shows allocations picking up slightly, suggesting selective profit-taking.If the SOPR for short-term holders rises back above 1.0, while allocations to long-term holders slow, it would be a sign that the market is returning to stability.

Cryptocurrency Deleveraging: Perpetual Contracts, DeFi Lending and Liquidity

The wave of liquidation on October 10Marks the beginning of a multi-layered deleveraging cycle across futures contracts, DeFi and stablecoin-backed leverage, its impact is still continuing to ferment in the cryptocurrency market.

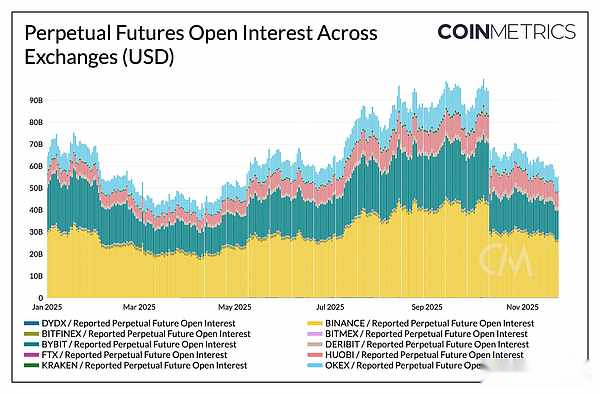

Continuous liquidation

In just a few hours, the perpetual contract suffered the largest forced liquidation in history, wiping out more than 30% of the open positions accumulated over several months.The drop in open interest was most pronounced on altcoin and retail trading venues such as Hyperliquid, Binance, and Bybit, where leverage surged, consistent with the steepest leverage growth before the event.As the chart below shows, open interest remains well below its pre-crash high of over $90 billion and has declined slightly since.This suggests that leverage in the system is coming back down as markets stabilize and readjust.

Funding rates also declined during this period, reflecting the adjustment in bulls’ risk appetite.Bitcoin funding rates have recently hovered around neutral or slightly negative values, consistent with the market not yet fully rebuilding directional confidence.

Source: Coin Metrics Market Data Pro

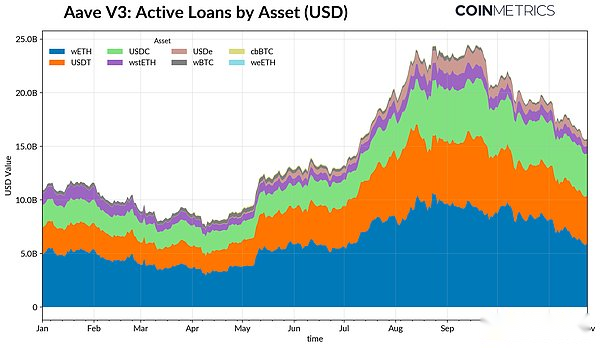

DeFi deleveraging

The DeFi credit market has also experienced a phase of gradual deleveraging.The number of active loans on the Aave V3 platform has trended downward since peaking in late September as borrowers reduce leverage and pay down debt amid weakening risk appetite and collateral repricing.Stablecoin-denominated borrowing has seen the most significant declines, a trend exacerbated by Ethena USDe’s dragging anchor, causing USDe borrowing volumes to drop by 65% and triggering wider leverage unwinding of synthetic USD.

Ethereum-based lending also shrank, with loans on Ethereum’s encapsulated token WETH and Liquidity Staking Tokens (LST) down around 35%-40%, suggesting less arbitrage activity and scaling back of yield staking strategies.

Source: Coin Metrics ATLAS

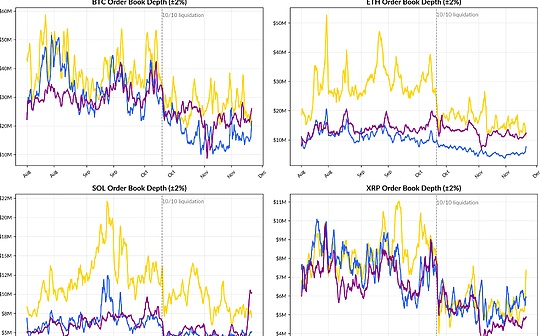

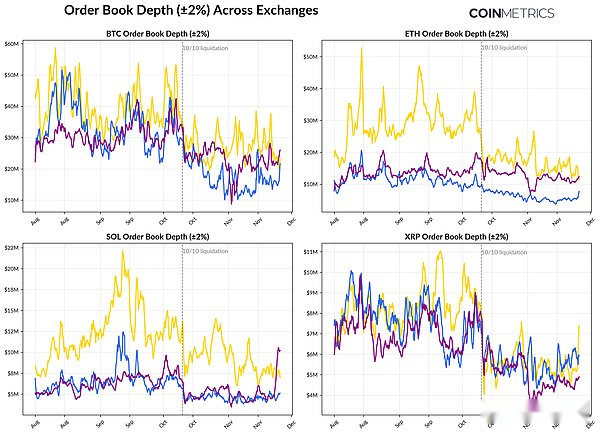

Shallow Spot Market Liquidity

After the liquidation wave on October 10, spot market liquidity remained weak.On major exchanges, the bid-ask spread (±2%) of Bitcoin, Ethereum and Solana is still 30%-40% lower than the level in early October, indicating that liquidity has not yet recovered along with the price.As a result of fewer pending orders, the market is more fragile, and a small amount of trading activity can cause large price fluctuations, thereby exacerbating market volatility and amplifying the impact of forced selling.

Liquidity conditions are even weaker for altcoins.In addition to mainstream coins, the order book depth of other coins has declined more sharply and for a longer period of time, reflecting the continued risk aversion of market participants and the reduction in market maker activity in mainstream coins and altcoins.An overall improvement in spot market liquidity would help reduce price shocks and stabilize market conditions, but for now, order book depth remains one of the clearest signs of continued stress in the system.

Source: Coin Metrics Market Data Pro

Conclusion

The digital asset market is undergoing a broad adjustment, which is mainly affected by factors such as weak demand for ETFs and DATs, reset of futures contracts and DeFi leverage, and continued insufficient spot liquidity.These factors put pressure on prices, but also make the overall system healthier, with lower leverage, more neutral positioning, and increasingly supported by fundamentals.

At the same time, the macroeconomic environment still poses unfavorable factors:Weakness in AI stocks, changing expectations for rate cuts and widespread risk aversion dampen demand.Continued recovery in key demand channels, e.g.ETF inflows, DAT accumulation, stablecoin supply growth, and a rebound in spot liquidity will lay the foundation for market stabilization and eventual reversal..Until then, markets will remain driven by tensions between risk aversion in the macro environment and the internal market structure of cryptocurrencies.