Author: Christopher Bendiksen, Source: CoinShares, Compiled by: Shaw Bitchain Vision

TL;DR

-

Many blockchains are using permanent inflation (commonly called tail-issuance) to try to secure miners/verifiers’ income in the absence of a strong market for handling fees.

-

The problem is that all such inflation is denominated in the native tokens of the relevant blockchain, and its future purchasing power is unaware, let alone guaranteed.

-

Therefore, protocol security in censorship-resistant blockchains is the result of the market, not an engineering problem, so there is no guaranteed solution – the future demand for security will either exist or not exist, which is unpredictable.

-

Since the purchasing power of future tokens cannot be predicted, no matter how many modifications are made to monetary policy, the blockchain is not guaranteed to be fully secured – on the contrary, modifications will weaken the token’s monetary attributes and may fall into a death spiral of security, as tokens cannot compete for currency demand, and mining/verification rewards lack sufficient value to ensure the security of the blockchain.

-

In short, the final additional issuance is not and cannot be a guarantee of sustainable settlement guarantee.

-

Instead, I think the risk of continually modifying protocols poses much greater for long-term security than simply letting the market tell us whether it wants something.

A few weeks ago, on August 12, 2025, the blockchain Monero based on PoW algorithm underwent a 6-block reorganization.In the following days, it underwent several reorganizations of 9 blocks.

Although this represents only a 12 to 18 minutes of historical rewrite, considering Monero’s 2-minute block time target (approximately the time of 2 Bitcoin blocks), this still goes far beyond the scope of the occasional standard non-malicious reorganization on the PoW blockchain.Statistically speaking, natural reorganizations over 2 minutes are extremely unlikely to occur, and the probability of occurrence decays exponentially as each block increases.

Therefore, the 6-block restructuring is likely to be a deliberate behavior of Qubic – Qubic is a strange blockchain that actually acts as a Monero mining pool.They also publicly acknowledged this.The attack was widely described by the media as a 51% attack, however, more in-depth analysis found no compelling evidence to support this claim.

These restructurings are most likely to be an embodiment of the “selfish mining” strategy – a long-standing strategy that maximizes mining returns by miners who control about 33% of the computing power in the PoW blockchain.PoS blockchains are also vulnerable to such attacks, and usually the complexity of PoS makes it less simple to analyze even if the total equity holding is low.

However, this article does not explore selfish mining, nor does it explore Qubic’s unique incentive mechanism.The mechanism utilizes the token market (at least temporarily) to increase the profitability of Monero miners who point their computing power to Qubic, thereby rapidly increasing computing power.Instead, I want to discuss a less obvious but more important lesson in my opinion: the tail issuance is not a viable solution to the security of long-term protocols of blockchain, and we must resist the urge to adjust the attributes of Bitcoin currency in the name of long-term security.

Let’s first agree on some definitions

One reason why discussions on this topic (and most other debates are frankly the same) is that people cannot agree on the meaning of certain words and terms and end up saying their own words.To avoid this, I hope to express my meaning very clearly when referring to certain words and terms.

-

Protocol security——Seldom terms are used casually like this word.It is often reduced to “attack cost”, a vague and unspecified reference to restructuring costs.When we use this term, we will strictly follow the meaning of settlement guarantees elaborated by Nic Carter in 2019.

-

Resistance to censorship——Blockchain can expel malicious miners who have reached 51% or higher computing power contributions and leverage their ability to censor blocks.

-

Final additional issuance——Use infinite inflation as an incentive for block creation.

-

Safety budget——I try to avoid using this term because it cannot be meaningful quantified within the framework of the blockchain protocol.Therefore, it is purely conceptual illustration and has no specific meaning.

Bitcoin’s long-term security seems to be problematic

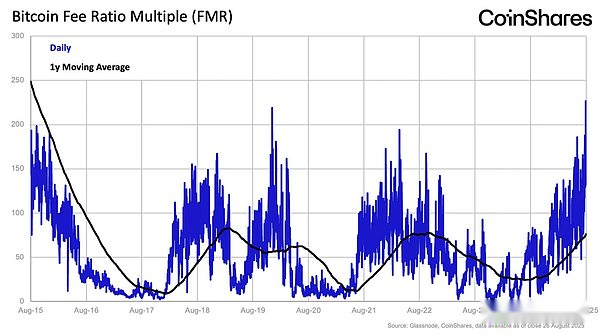

Let me try to briefly summarize the obvious problems behind all of this, and all of them are derived from Bitcoin.One of the main assumptions of Bitcoin is that once the supply of new coins is exhausted, transaction fees will become the main source of income for miners.

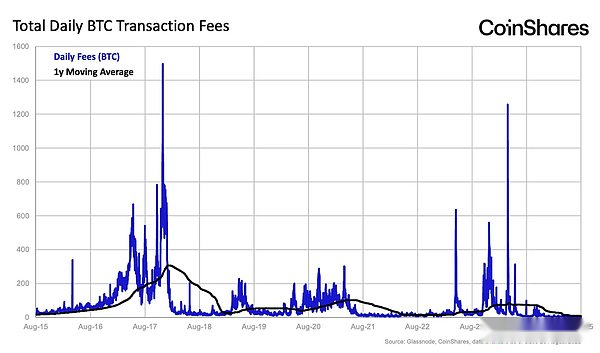

From a technical perspective, this is already the case.On average in the past year,If the current block reward of 3.125 BTC is removed, there will be about 0.06 BTC transaction fees left (if the average value is 30 days, this number will be even smaller).The problem is obvious: the current transaction fee is less than one percent of the block reward, which is really not too much.

In fact, ifFrom now on, the handling fees denominated in Bitcoin will no longer increase, so they will not match the size of the block reward until six halvings, which is about 23 years later.This means that to keep mining rewards at least at the current level,The product of Bitcoin purchasing power and the current total handling fee for each block (Bitcoin purchasing power *Bitcoin total fee) needs to grow 100 times within 23 years.

Many people think this is unlikely to happen, so there are a lot of suggestions on how to “solve” this problem.There is a problem with this idea.

Protocol security in censorship-resistant blockchain is a market result rather than an engineering problem

First, I need to clarify that when I talk about anti-censorship blockchain, I mean pure PoW blockchain.PoS blockchain is by definition unresisting censorship, and we have explored this topic in depth in previous articles.

I’ve said before that Bitcoin’s long-term security/settlement guarantee is based on one assumption, and that’s what I mean.It is impossible to prove that it is “sufficient” in the long run.The market either has the need to provide settlement guarantee through transaction fees or does not.This is almost exactly the same as whether there will be a demand for Bitcoin in the future.

If the answer to either of these two questions is “no”, Bitcoin will fail.I also can’t imagine that there will be a situation where “yes” answers to one of the questions and “no” answers to the other, so the conditions for failure will be almost the same.If people no longer need Bitcoin (currency) or Bitcoin protocol and network, it fails.This argument goes without saying.

This reality often makes engineers (I am one of them) feel unhappy.Therefore, many “solutions” have been proposed.These “solutions” can be roughly divided into two categories.Either aims to change the supply or demand side of the fee market, or aims to use the tail issuance as a permanent reward generated by blocks.

The problem is that neither method can prove effective.No matter how many adjustments are made to the supplier or demanding party of the expense market, there is no guarantee that there will be any demand, let alone “enough” demand, no matter what “enough” means here.This is obvious to most people.

Nevertheless, it is still believed that there is a better design theoretically than it is currently available just because it cannot be “guaranteed” or “prove”. This is why these solutions are proposed.This view itself is completely understandable, but I must emphasize that believing that these solutions will work, just as believing that the charging model will work, requires a lot of confidence.In fact, no one knows whether these two options are feasible.

The “safety budget” issued at the end can never prove its adequacy

Many people seem to be not sure that the tail issuance is the same as the solution to incentivize permanent settlement guarantee, and there are problems that cannot be proven.At what level is the “full” of the final issuance?Setting the final additional issuance to 1%, targeting a certain “safety budget” can never guarantee settlement guarantees at any specific level – this is purely speculation.

Since you cannot predict the future purchasing power of the token, you are always at risk of “too low” token issuance, which forces you to continuously adjust your monetary policy and even lead to hyperinflation in extreme cases.This further weakens the token’s monetary attributes and may cause token security to fall into a death spiral, as the token price plunge requires higher inflation rates to fund the “safety budget.”

Monero’s vulnerability should warn of the tail-issued blockchain

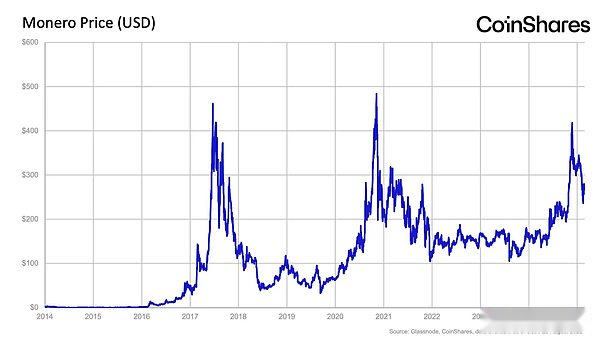

As mentioned above, the key point I want to emphasize is that the tail issuance cannot guarantee the long-term security of blockchain.Monero implemented a tail-issuance mechanism in 2022, and the community originally expected it to ensure the sustainability of block rewards.While this may be technically true, as we just saw, it makes no sense in providing viable settlement guarantees.

While Monero miners can get permanent block rewards, Monero cannot compete with Bitcoin in terms of currency attributes, so no one will use Monero to store value.The result is obvious that Monero’s purchasing power has been basically stagnant over the past decade.The situation is worse than its strongest rival Bitcoin, which has plunged over the years.

In other words, a tail issuance sounds good, but if your token has no value, no matter how much the tail issuance is not enough.

This should sound a wake-up call for blindly optimistic blockchain inflation theorists.At least in the Bitcoin circle, it is generally believed that inflation is harmful to fiat currency and the entire society.Therefore, I was very surprised that there were even Bitcoin supporters who believed that inflation was harmless to Bitcoin.

The main driving force for the long-term value of any type of currency comes from low-frequency users, They seek a tool that can maintain value for the long term.These users are strongly inclined to the currency units they believe have the strongest currency attributes.If your blockchain cannot provide this attribute, they may use it for high frequency transactions, but not to use it to store wealth when the economy is inactive.This is bad news for your token value.

We must resist the engineering temptation to modify the attributes of Bitcoin currency

As I mentioned earlier, in order to maintain Bitcoin’s current settlement guarantee for the next 25 years or so, it needs to increase the purchasing power of transaction fee rewards by about 100 times.Actually, I think this is entirely possible.

Given that Bitcoin prices have risen more than 100 times in the past 10 years, and at the same time, the handling fee levels have continued to be more than 20 times higher than the current BTC price on many occasions.In other words, in the next 25 years, the price will rise by 10 times and the handling fee will also rise by 10 times. In my opinion, it is not impossible.

That is, as long asBitcoin retains its outstanding monetary attributes, I don’t think this situation is impossible.If we destroy these attributes by changing the size of blocks, introducing infinite inflation, or falling into the universal mindset of Ethereum that constantly modify monetary policy, I think it is much more risky than just letting the market tell us whether there is demand for Bitcoin in the long run.

In fact, the fundamental reason why Bitcoin prices have not reached $10 million per coin is that we (as a huge society and market) simply cannot determine whether the assumption of sufficient future demand for Bitcoin is correct.Over time, figuring out the answer to this question and accurately assessing its possibilities is what the market exists.Let the market play its role.