Source: Coinbase; Compilation: Bitchain Vision

Key points:

-

Our previous report, Stablecoins and the New Payment Landscape (August 2024), examines the role of stablecoins in the global payment system and explores why traditional banking systems, credit card and mobile providers must adapt to the changing needs of their customers.

-

In our follow-up report, we examine how the complexity of stablecoins integration into the existing financial system limits growth in the overall market size of stablecoins, such as the net impact on total U.S. Treasury demand.

-

Our random model predicts,By the end of 2028, the market value of stablecoins may reach around US$1.2 trillion.We believe this does not require unrealistic large or permanent rate misalignment; instead, it relies on gradual, policy-supported adoption and continues to grow compounded over time.

-

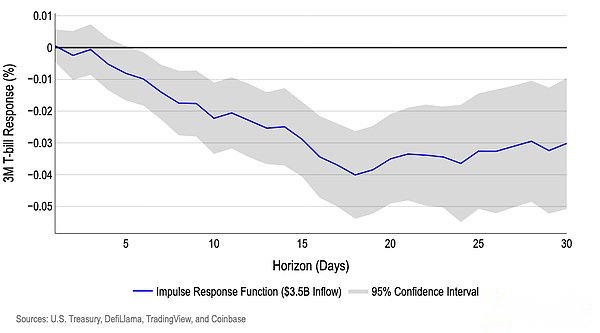

The continued growth of stablecoins will reduce marginal front-end financing costs, while large redemptions will tighten front-end financing costs.We estimate that the $3.5 billion inflow of stablecoins in 5 days may compress the 3-month Treasury yield by about 2 basis points within 10 days and up to 4 basis points within 20 days.The substitution effect may bring downside risks to this valuation.

-

Finally, we believe that regulatory developments such as the GENIUS Act are crucial to establishing clear reserve rules and liquidity buffers that can reduce the risk of large-scale redemptions becoming mandatory sale of Treasury bonds.

Random growth forecast

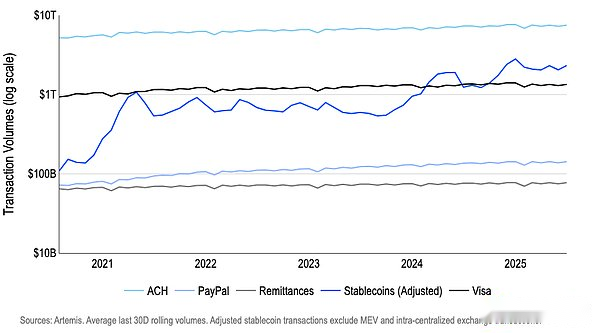

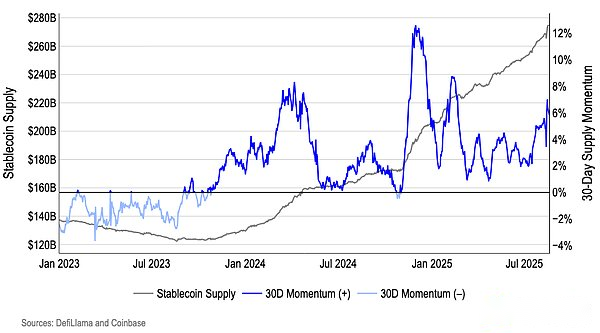

The stablecoin market is at a turning point, and its growth depends on key factors such as efficient channels, extensive distribution networks, and the evolution of market participants’ roles.According to Artemis data (see Charts 1 and 2), the global stablecoin market capitalization (from 2021) has grown at a compound annual growth rate of about 65%, exceeding $275 billion by mid-August 2025, with an average adjusted trading volume soaring from $10.3 trillion in the same period in 2024 to $15.8 trillion year-to-date.

Figure 1: Adjusted stablecoin transaction volume compared to existing systems

Figure 2: Stablecoin supply has now exceeded US$275 billion (as of mid-August)

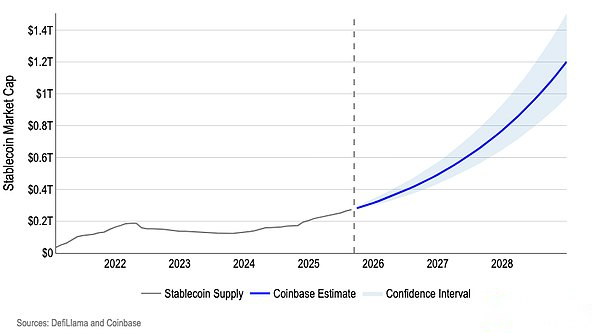

Future growth forecasts are often based on assumptions about the global share of money supply that stablecoins may eventually occupy.We took a different approach.Our random approach—running thousands of Monte Carlo-like simulations using autoregressive models—indicates that by the end of 2028, stablecoins may have a market capitalization of around $1.2 trillion (see chart 3).

Figure 3. Model-based stablecoin market capitalization growth forecast

It should be clear that since the utility of stablecoins will have a compound effect as more and more consumers and businesses use it, it cannot perfectly simulate the growth dynamics of stablecoins.This leaves a lot of room for volatility in analysts’ valuations.That is, there is still a data gap in real-world adoption patterns, which makes it challenging to predict the final stablecoin market size.Our weighted autoregressive AR(1) model focuses more on certain historical observations to capture long-term and local temporal patterns:

-

We used a simple AR(1) model to estimate log supply, but we gave greater weight to the period beyond 2024 to reflect (1) better structural policy context and (2) accelerated adoption trends.

-

We then perform Monte Carlo simulations on thousands of forward paths through resampling of the recent growth shock, which preserves the fatter “crypto-style” noise at the tail we actually see, rather than assuming neat bell curves.

How to simulate the growth of stablecoins

We think this approach works in today’s markets because it captures the right economic factors with minimal assumptions.The supply growth of stablecoins is path-dependent and sustainable.Good policy and distribution means growth may lead to growth.Logarithmic autoregressive AR(1) can capture this persistence without overfitting dozens of covariates that are themselves institutionally sensitive.Weights after 2024 enable models to “learn” from the environment we care most.

That is, our model focuses on historical observations, including: (1) recent U.S. policy momentum (e.g., the adoption of the GENIUS Act, state/federal frameworks, etc.); (2) stablecoin integration into institutional tracks; and (3) significant improvements in fiat currency entry and exit channels.We believe this is more relevant than diluted data with earlier and lower correlation periods.The residual bootstrap method step respects the observed growth volatility, so our prediction interval remains statistically honest about uncertainty while still centering on the new mechanism.

also,We believe the $1.2 trillion path is both realistic and consistent with our front-end interest rate model.From the current $275 billion to $1.2 trillion, it means a net issuance of approximately $925 billion in U.S. Treasury bonds in about 175 weeks, or about $5.3 billion per week(See next section).Our model shows that such weekly issuances will only cause short-term interest rates (3-month yields) to temporarily drop by about 4.5 basis points in two to four weeks.Since this reaction gradually decays, the effects do not overlap infinitely.We believe that trillions of dollars in money market funds can be reconfigured between Treasuries, repurchase agreements and Fed overnight reverse repurchase (O/N RRP) tools, which sets an effective lower limit for overnight interest rates and limits the pricing of Treasuries.

On the supply side, when demand is strong, the Ministry of Finance can tend to issue notes; on the demand side, stablecoin issuers can moderately diversify the period in about 3 months, both of which can further dilute the continued downward pressure on yields.In short, we believe that this prediction does not require unrealistic large-scale or permanent interest rate misalignment (interest rate misalignment, meaning serious pricing errors in the U.S. Treasury market or a substantial deviation from fair value); instead, it relies on incremental, policy-backed, compound adoption over time.

In-depth study of the “constraints” of treasury bonds

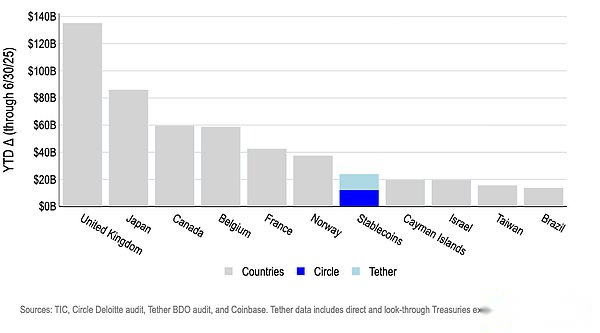

Stablecoins have become an important new source of demand for US Treasury bonds and are expected to fundamentally change the pattern of Treasury bond supply management.In fact, stablecoin issuers have ranked among the top ten holders of all sovereign entities holding U.S. Treasury bonds.In fact, the first two stablecoin issuers alone have become the seventh largest buyer of US Treasury bonds as of June 30 in 2025 (see Figure 4).

Figure 4. The largest buyer of US Treasury bonds so far in 2025 (as of June 30)

However,The support mechanism of stablecoins has raised questions about whether these tools will exhaust the U.S. government’s ability to issue short-term T-bills, and to what extent capital flows may affect these yields.

Obviously, the issuance and redemption of stablecoins will drive the front end of the U.S. yield curve, as issuers buy short-term Treasury bonds when stablecoins are issued and sell them when redeemed.However, modeling its effects can be complex, especially when examining inflows and outflows.For example, we estimate that (over 5 days) of USD 3.5 billion stablecoin inflows could compress 3-month yield by about 2 basis points in 10 days and up to 4 basis points in 20 days.This is roughly consistent with a recent study by the Bank for International Settlements (BIS) (see Figure 5).

For inflows, our benchmark estimates show that its impact on 3-month Treasury yields is smaller in the first week and gradually increases in the second-3 weeks and eventually weakens.Our model removes common front-end drivers before estimating the “stablecoin effect.”We controlled for the forward changes in adjacent periods (1 month and 6 month yields), as well as the last 5-day changes in 1 month/3 month/6 month yields, outstanding notes (supply), Fed RRP balance (front-end cash pressure), and VIX (risk sentiment).This can avoid mistakenly considering the Fed’s interest rate day, curve changes or liquidity fluctuations as catalysts for stablecoins.

Figure 5. Effect of 5-day inflow of US$3.5 billion stablecoins on 3-month Treasury yields

That is, we use predictors that drive capital flows but do not directly affect Treasury yields to separate causal relationships.Our inputs include lagged cumulative residuals in the cryptocurrency market (i.e., the portion of cryptocurrency earnings that are not explained by macro/curve factors) and a lagged anchor bias of USDT/USDC to $1.00 (outliers have been removed and split by symbol).We then confirmed that our approach to identifying the direct impact of stablecoin fund flows on Treasury yields is statistically robust.

Risk and uncertainty

It turns out that simulating the impact of stablecoin outflows on Treasury yields is much more difficult, because the impact of outflows is highly asymmetric compared to inflows.Such models need to have some unique features that often affect their accuracy.For example, the Bank for International Settlements believes that the outflow of US$3.5 billion of stablecoins of similar scale may lead to a tightening of yields by about 6-8 basis points, as a tight market environment may hinder stablecoin issuers from grasping the timing of the issuance of Treasury bonds.However, limited tail event data makes such model estimates less reliable, and regulatory changes may offer the possibility for issuers to open up other sources of financing.

This is not to reduce the risk of stable currency outflows.Their asymmetric effects are directly related to negative decoupling, which may have a nonlinear chain effect on Treasury bonds.One of the biggest such events in recent history (among major stablecoin issuers) occurred in March 2023, when USDC fell below 87 cents at one point because 8% of its reserves were disclosed to be deposited in Silicon Valley Bank (SVB).This centralized risk itself is caused by a regulatory environment that makes it difficult for cryptocurrency-related entities to establish the necessary extensive banking relationships to reduce redemption risks.

For example, the bank’s bankruptcy of Silicon Valley (SVB) is mainly due to its poor asset-liability management, as the bank invests heavily in long-term U.S. Treasury and mortgage-backed securities using short-term, uninsured deposits.The key for stablecoin issuers is that Operation Chatter 2.0 has forced many cryptocurrency companies to work with only a few crypto-friendly banks willing to do business with them.Federal regulators subsequently urged these banks to limit deposits from cryptocurrency-related entities, which directly led to deposit instability and ultimately led to SVB runs.(Evidence is based on obtained from the Freedom of Information Act litigationFederal Deposit Insurance Company FDIC Document)

While this does not negate the decoupling event, it does suggest that this may be an isolated case, with limited explanatory power for testing the stability of stablecoins or the elasticity of Treasury markets during stressful times.

Furthermore, our analysis to date only assumes that stablecoin issuance represents a new demand for Treasury bonds, but we believe thatFunds may be reconfigured from commercial bank deposits, offshore foreign exchange and money market funds to stablecoins, creating an alternative effect.That is, if USD 1 is transferred from the bank to the stablecoin issuer, this may only constitute a marginal net new demand for additional treasury bond supply.This not only poses a downside risk to our initial estimate of stablecoin inflows that will compress Treasury yields by 2-4 basis points, but also poses a downside risk to estimates that stablecoin outflows will compress yields.

A new regulatory landscape

Another challenge in modeling stablecoin liquidity effects stems from the ever-changing regulatory environment since the approval of the GENIUS Act in July.The GENIUS Act will come into effect in January 2027, which ensures consumer rights through the following ways:

-

Implement strict 1:1 reserve requirement (monthly audit) for 100% of the outstanding stablecoins,

-

The bankruptcy priority claims of stablecoin holders, and

-

Regulatory oversight at the state or federal level.

However, there are still some unanswered questions about the future of stablecoin operations that may be resolved within the next 18 months.For example, many stablecoins are currently issued directly through intermediaries rather than issuers.This led to a double-layer redemption system in which only institutions (rather than retail investors) have a direct contractual relationship with the issuer, which was a concern for the Securities and Exchange Commission (SEC) commissioner Caroline Crenshaw in April this year.Resolving this may remain a point of debate, although the GENIUS Act strengthens legal protections for stablecoin holders, meaning stablecoin issuers need to publicly disclose their redemption policies.

Another key question in dealing with the “risk run” of potential capital outflows is whether stablecoin issuers can gain access to the Fed’s balance sheet (such as credit lines, main accounts), just as the access enjoyed by banks and money market funds.The GENIUS Act does not explicitly grant stablecoin issuers access to the main account or discount window, but rather hand it over to the Fed’s sole discretion.However, the bill may allow these entities to operate as subsidiaries of insured banks, which indirectly gives the Fed access if the parent company qualifies.Similarly, implementation remains the key.

in conclusion

Our analysis shows that stablecoins are expected to achieve substantial growth.Our random model predicts that by the end of 2028, the market value of stablecoins will reach around $1.2 trillion.This growth will be supported by a continuous improvement in policy environment and accelerated adoption trends.

Ultimately, as stablecoins continue to grow, we believeClear reserve rules, high-frequency information disclosure and liquidity buffering are crucial to reducing the risk of large-scale redemptions turning into a series of forced treasury bond sell-offs.

That is, we thinkDevelopments like the GENIUS Act are crucial to reduce run risks and build a more resilient stablecoin ecosystem.