Author: YQ; Source: X, @yq_acc; Compiler: Shaw Bitcoin Vision

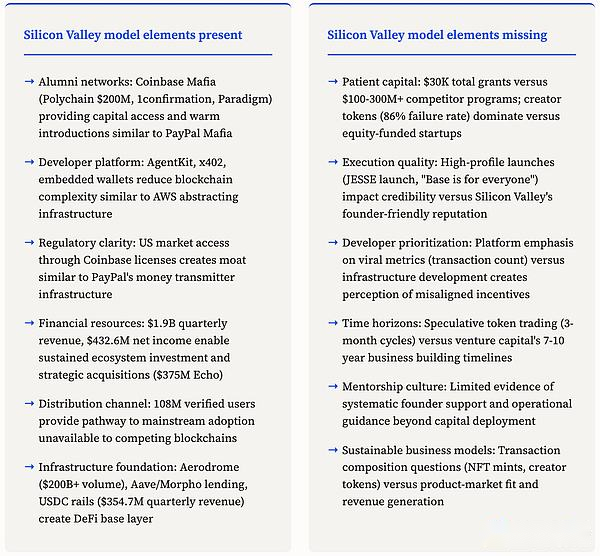

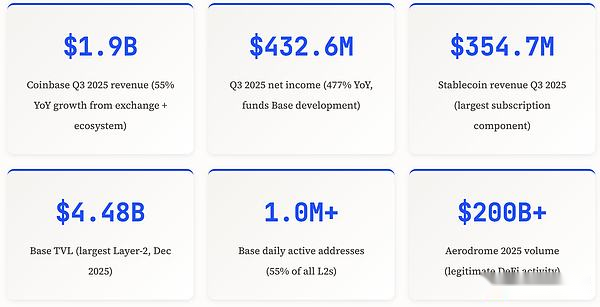

Coinbase has transformed from a mere centralized exchange to an ecosystem orchestrator, the core of which is Base, the Ethereum Layer-2 platform launched in August 2023.This shift leverages three Silicon Valley advantages that no other blockchain can match:Regulatory infrastructure facilitates entry into U.S. market(Has 108 million verified users and quarterly stablecoin revenue of $354.7 million);Alumni network connects projects to venture capital(Polychain, 1confirmation and Paradigm founded by Coinbase alumni); andA developer platform that reduces blockchain complexity(AgentKit, x402 payment protocol, embedded wallet).Base achieves market leadership with $4.48 billion in TVL (the largest Layer-2 network), over 1 million daily active addresses (55% of all Layer-2), and the Aerodrome platform’s projected cumulative transaction volume of over $200 billion by 2025.However, the composition of transactions shows a tension between creator token speculation (peak daily issuance volume reached 38,254 times and a three-month failure rate of 86%) and institutional DeFi infrastructure.Coinbase’s third quarter 2025 results ($1.9 billion in revenue, $432.6 million in net profit) demonstrate the financial ability to continue investing in the ecosystem, while the partnership with Circle ($740 million in revenue per quarter, $74 billion in USDC circulation) provides it with a stablecoin foundation.

1. From exchange operations to ecosystem architecture

Coinbase’s strategic evolution from a centralized exchange to a comprehensive blockchain ecosystem developer reflects a thoughtful transformation similar to Amazon’s transformation from an online bookstore to a cloud infrastructure provider through AWS.Base, launched in August 2023, will become Coinbase’s infrastructure layout in the blockchain field, providing building foundations and developer tools for other applications, rather than directly competing with every cryptocurrency use case.This structural shift from a service provider to a platform operator has also changed Coinbase’s revenue model, shifting it from pure transaction fees to multi-level value capture, including sequencer revenue, stablecoin issuance, token listing fees, and equity in ecosystem projects.

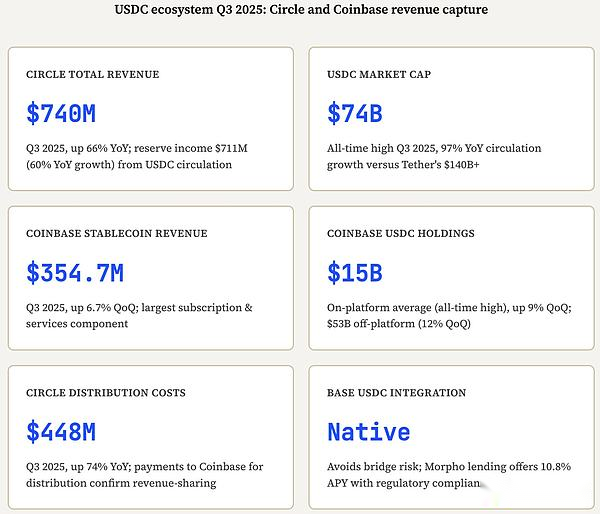

This transformation was quantified in Coinbase’s Q3 2025 financial performance, which demonstrates both the company’s health with continued ecosystem investments and Base’s contribution to revenue diversification.Coinbase reported quarterly revenue of $1.9 billion (a year-on-year increase of 55%) and a net profit of $432.6 million (a year-on-year increase of 477%).Subscription and service revenue (including Base-related activities and stablecoin issuance) has now diversified revenue beyond transaction fees.In the third quarter of 2025, stablecoin revenue reached $354.7 million (a 6.7% quarter-on-quarter increase), becoming the largest component of the subscription and services segment.Subscription and service revenue is expected to reach $710 million to $790 million in the fourth quarter of 2025, driven by USDC’s continued popularity and ecosystem growth.

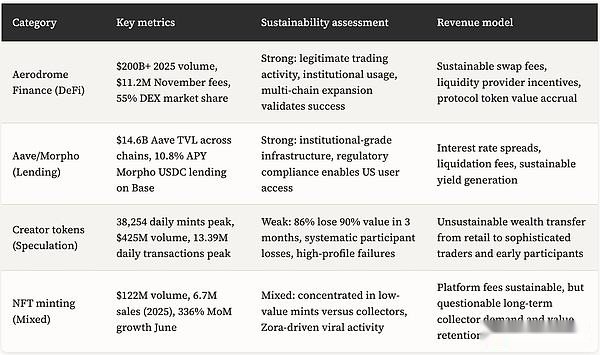

Base achieved market leadership with $4.48 billion in total value locked (TVL) as of December 2025, surpassing Arbitrum and other mature Layer-2 networks, and has only been in operation for 28 months.There are over 1 million daily active addresses, accounting for 55% of all Layer-2 addresses by the end of 2025 (growing from 63% in January to 82% of the top Layer-2 networks in April).On January 1, 2025, the daily transaction volume peaked at 13.39 million transactions, demonstrating its strong transaction throughput processing capabilities.Aerodrome Finance, the main decentralized exchange (DEX) on Base, has a cumulative trading volume of more than 200 billion US dollars in 2025 (a 3-fold year-on-year increase), and generated US$11.2 million in handling fees in November 2025, with annualized revenue of approximately US$136 million.These metrics validate Base’s technical execution and market acceptance, but questions remain about the makeup of transactions and the sustainability of growth driven by creator tokens.

2. Coinbase Alumni Network: Silicon Valley Capital Network on the Chain

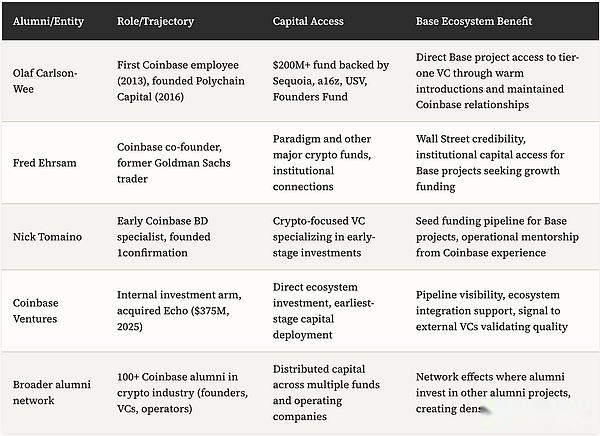

Coinbase’s alumni network provides a structural advantage to the Base ecosystem, similar to how PayPal Mafia (Peter Thiel, Elon Musk, and Reid Hoffman) shaped the structural advantages of subsequent entrepreneurial generations through access to capital, operational expertise, and introductions..Olaf Carlson-Wee was the first employee hired by Coinbase in 2013. He left in 2016 to found Polychain Capital, which is now among the world’s largest cryptocurrency hedge funds and has raised $200 million from the likes of Sequoia Capital, Union Square Ventures, Andreessen Horowitz and Founders Fund.Polychain’s portfolio includes projects in the Base ecosystem that benefit from capital investment and the relationship Carlson-Wee maintains with Coinbase executives, building a project pipeline that allows Base projects to receive faster due diligence and more favorable terms than similar projects on other competing chains.

Fred Ehrsam is a former Goldman Sachs trader who co-founded Coinbase with Brian Armstrong.He is the second important alumni node connecting the Coinbase ecosystem with Wall Street capital and institutional relationships.Ehrsam’s subsequent entrepreneurship and investments have opened up additional avenues for capital formation, while his background at Goldman Sachs has given him credibility when evaluating investments in cryptocurrency infrastructure with traditional financial institutions.Nick Tomaino’s experience illustrates this pattern on a smaller scale: he served as an early-stage business development specialist at Coinbase, then joined Runa Capital to improve his venture capital skills, and then founded 1confirmation, a cryptocurrency-focused venture capital fund.As successful alumni invest in subsequent Coinbase projects, the network effect continues to grow, forming a tightly interconnected financing ecosystem.In this ecosystem, Coinbase projects receive preferential access to financing through personal connections, an advantage that other blockchain ecosystems cannot replicate without similar alumni networks.

Coinbase Ventures, Coinbase’s internal capital deployment arm, invests in outstanding founders who are driving the growth of the crypto ecosystem and builds partnerships with early-stage teams.At the end of 2025, Coinbase acquired Echo, founded by well-known cryptocurrency trader Cobie, for $375 million. This move added a complete on-chain financing and transaction execution platform to Coinbase Ventures, allowing it to gain earlier insight into potential projects and provide a standardized process for cryptocurrency private financing.This acquisition exemplifies how Coinbase identifies emerging infrastructure needs (on-chain capital formation) and acquires solutions while integrating them into the broader Base ecosystem strategy.Judging from actual performance, the financing speed and valuation premium of the Base project have increased.Communication between founders shows that Base-focused projects can achieve faster venture capital responses, higher initial valuations, and more favorable terms than similar projects on other Layer-2 networks.

Coinbase Alumni Network and Silicon Valley Capital Advantage

3. Developer Platform: Reduce Blockchain Complexity

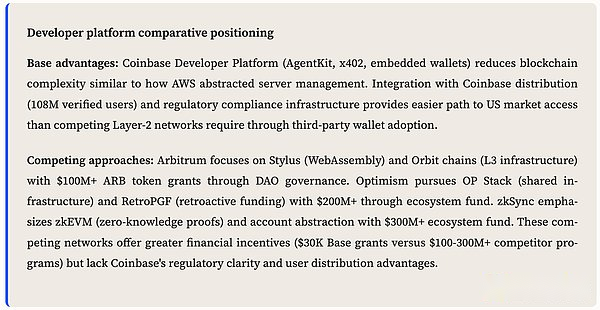

Coinbase’s developer platform strategy is similar to that of Amazon AWS, which simplifies the complexity of server management so that application developers can focus on business logic rather than infrastructure operations.The Coinbase Developer Platform (CDP) provides a toolkit, simplifies the complexity of blockchain and enables developers to build applications using familiar web development patterns without the need for deep cryptography expertise or knowledge of blockchain protocols.Launched in 2024 and further expanded in Q1 2025, AgentKit enables AI agents to interact with blockchain networks through secure wallet management and comprehensive on-chain functionality.The core value of the platform is to reduce time to market, allowing developers to release blockchain-enabled applications in just a few weeks, instead of spending months on infrastructure development.

The x402 payment protocol re-enables the HTTP 402 “Payment Required” status code, enabling APIs, applications and AI agents to make instant stablecoin payments directly over HTTP.The protocol solves the long-standing pain point of Internet micropayments by embedding payment requests into standard HTTP interactions, eliminating the need for a separate payment processing system and its associated integration complexities.For application developers who need to make money based on usage-based billing, subscription services or APIs, x402 provides seamless integration compared to traditional payment methods involving bank integrations, payment processor accounts and complex fee structures.Released in January 2025, in sync with AgentKit updates, the protocol creates a unified technology stack for autonomous payment applications capable of automating financial transactions without human intervention.

Embedded wallet infrastructure (CDP wallet)This lowers the barrier to entry for end users by enabling applications to create and manage user wallets behind a familiar web interface, without requiring users to understand mnemonics, fees or blockchain transaction mechanisms.This simplification is critical for mainstream adoption, as the technical complexity of cryptocurrencies can hinder non-technical users who lack an understanding of concepts such as “fees,” “nonce,” or “transaction confirmation time.”Coinbase’s Builder Grant program, launched in the summer of 2025, awarded $30,000 to 13 projects using CDP wallets, AgentKit, and Onramp, demonstrating that Coinbase is actively cultivating the developer ecosystem by providing financial incentives beyond tools.The program received a total of 55 applications, indicating that there is still demand for these developer tools despite broader concerns about the makeup of the creator token ecosystem and the dominance of speculation in trading indicators.

4. Regulatory moat: U.S. market access as a competitive advantage

Base’s regulatory positioning established through Coinbase’s compliance infrastructure creates an asymmetric advantage similar to PayPal’s remittance license in building a moat in the online payment field..Coinbase holds licenses in all 50 U.S. states and has applied to register as a national securities exchange with the U.S. Securities and Exchange Commission (SEC), has also received derivatives registration from the U.S. Commodity Futures Trading Commission (CFTC), and is registered as a broker-dealer with the U.S. Financial Industry Regulatory Authority (FINRA).When this compliance framework is extended to the Base ecosystem, it transforms from a pure cost center (hundreds of millions of dollars in legal and operational expenses annually) to a strategic asset.Applications built on Base are able to gain regulatory clarity for U.S. market access that other Layer-2 networks cannot provide without making similar compliance investments.Given the massive regulatory costs, such compliance investments remain economically unfeasible for most blockchain infrastructure providers.

The speed of user acquisition and user composition are concrete manifestations of its advantages.By the third quarter of 2025, Base’s daily active addresses will reach 1 million. As of April 2025, it has occupied 82% of the top Layer-2 addresses, and will grow to 55% of all Layer-2 addresses by the end of the year.Consumer trading activity on the Coinbase platform jumped to $59 billion in the third quarter of 2025 (up 37% quarter-on-quarter), institutional trading volume reached $236 billion (up 22% quarter-on-quarter), and institutional trading revenue reached $135 million (up 122% quarter-on-quarter).These verified and KYC-compliant users provide Base applications with distribution channels not available on offshore exchanges or anonymous DeFi protocols, creating a shortcut to mainstream adoption.Other blockchains must achieve this through more circuitous routes involving third-party wallets and decentralized exchange interfaces.

Exchange listing support provides a second dimension of regulatory advantage.Base ecosystem tokens receive priority when listing on Coinbase through internal advocacy and a streamlined due diligence process, while tokens on other chains face an external application process, and the timing and outcome of the process are uncertain.The advantages of liquidity, price discovery, and investor access brought by Coinbase’s listing are difficult for other trading platforms to match, and its economic impact has therefore become significant.The launch of the Base-Solana cross-chain bridge in December 2025 reflects this dynamic: Coinbase announced the acquisition of Vector (Solana’s native decentralized exchange), and at the same time vigorously promoted the Base-centered cross-chain bridge infrastructure, allowing SOL and SPL tokens to flow into Base applications and generate Base transaction fees, but the Solana ecosystem was unable to obtain corresponding value from it.This prompted Solana developers to describe it as a “vampire attack disguised as interoperability,” noting that this asymmetric interest structure favors Coinbase-controlled infrastructure.

5. USDC Infrastructure: Stablecoin as Ecosystem Track

Coinbase’s partnership with Circle and the distribution of USDC create infrastructure advantages similar to those used by Visa and Mastercard payment networks to empower commerce by providing trusted settlement channels..The economics of the collaboration were reflected in Q3 2025 results, when Coinbase’s stablecoin revenue reached $354.7 million (up 6.7% quarter-on-quarter), becoming the largest component of its subscription and services segment.In the third quarter of 2025, the average balance of USDC held in Coinbase products reached an all-time high of $15 billion (up 9% quarter-on-quarter), while balances outside the platform increased to $53 billion (up 12% quarter-on-quarter).This distribution capability transcends competing platforms and directly benefits Base through native USDC integration, avoiding issues such as cross-chain bridging risks or liquidity fragmentation that other Layer-2 networks may face.

Circle’s financial results for the third quarter of 2025 confirm the overall growth of the USDC ecosystem.Circle reported that its total revenue and reserve income reached $740 million (a 66% year-on-year increase), with reserve income reaching $711 million (a 60% year-over-year increase), mainly due to a 97% increase in the average USDC circulation.USDC’s market value reached an all-time high of US$74 billion in the third quarter of 2025, up from the previous US$61.3 billion, making it the second largest stablecoin after Tether (with a market value of more than US$140 billion).It is worth noting that Circle’s distribution costs increased 74% year-on-year to $448 million, with the increase “primarily coming from an increase in distribution payments, which reflects an increase in USDC circulating balances and an increase in the average USDC holdings on the Coinbase platform.”This disclosure confirms that Coinbase has received a significant share of revenue from USDC’s growth, prompting Coinbase to use it as a USDC distribution channel and establish a financial foundation for ecosystem development independent of speculative token trading.

For Base applications, native USDC integration has many advantages over other Layer-2 networks.Developers do not need to implement a bridge interface to ensure the availability of USDC and price it in a US dollar pricing method familiar to mainstream users, while avoiding the risk of bridge failure or liquidity fragmentation caused by the existence of multiple bridge versions of assets with different liquidity depths.Coinbase launched USDC lending services on Base in November 2025 through integration with Morpho (providing annualized returns of up to 10.8% through automatic yield optimization), fully demonstrating how Coinbase builds financial products on top of USDC infrastructure while maintaining regulatory compliance, which is something offshore platforms cannot provide to US users.JPMorgan analysts previously estimated that Coinbase could gain an additional $60 billion in value from its core position in the USDC ecosystem, and third-quarter 2025 results are starting to bear out this prediction, as is the growth trajectory of stablecoin revenue.

6. Ecosystem composition: DeFi infrastructure and speculation

The Base ecosystem exhibits a fundamental contradiction between compliant DeFi infrastructure and speculative creator token activity, similar to the coexistence of sustainable business models (Amazon, Google) and speculative enterprises (Pets.com, Webvan) during the dot-com bubble.Aerodrome Finance represents the infrastructure category, with cumulative trading volume exceeding $200 billion by 2025 (a 3x year-on-year increase), and accounting for 55% of all decentralized exchange (DEX) trading volume on the Base platform.Results in November 2025 show that its transaction volume reached US$16 billion, the handling fees incurred reached US$11.2 million, and the annualized revenue was approximately US$136 million.Aerodrome’s capital pool contributed $260 million in “on-chain GDP” in 2025, accounting for 44% of the Base platform’s total economic activity, indicating that its liquidity is focused on compliant transactions rather than speculative minting.

In November 2025, Aerodrome announced that it would merge with Velodrome to form the cross-chain platform “Aero”, which will be launched on Ethereum and Circle’s Arc blockchain in 2026.This news not only verifies the success of the Base protocol, but also reduces Base’s exclusive value acquisition.This strategic evolution shows that Base’s most advantageous applications adopt a multi-chain strategy rather than relying on a single ecosystem, which creates tension between protocol growth and Base ecosystem lock-in.Aave’s deployment on Base and integration with Morpho further demonstrates its institutional-grade infrastructure, providing a regulated access point for U.S. users seeking decentralized lending without the need for offshore exchanges or regulatory uncertainty.

Creator token activity shows a very different pattern, with impressive trading metrics but questionable economic sustainability.Base reached a peak daily transaction volume of 13.39 million on January 1, 2025, and continued to maintain high activity in the spring and summer of 2025, with the number of daily active addresses reaching 1.2 million in April and 1.6 million in May.However, much of this activity stems from token issuance rather than actual applications of DeFi.The surge in creator tokens in the summer of 2025 drove the daily minting of about 38,254 tokens, with a total value of $425 million, but industry data shows that 86% of influencer-promoted tokens will lose 90% of their value within three months.High-profile issuances including the JESSE token offering in November 2025 (application delays led to snipers withdrawing $1.3 million, while retail investors faced a 17-20 minute lock-up) and the April 2025 “Base is for”everyone” issuance (official promotion pushed the token market cap to $17 million before plunging 90%), affected the credibility of the ecosystem and may have prompted users to realize that creator tokens represent negative expected value to ordinary participants.

Base ecosystem composition: compliance infrastructure and speculative activities

7. Silicon Valley on the chain: reality and ideals

The vision of “Silicon Valley on the Chain” requires Base to replicate Silicon Valley’s entrepreneurial ecosystem dynamics:High-quality founders build sustainable businesses, venture capital provides patient capital and operational expertise, successful entrepreneurs mentor subsequent entrepreneurs through network effects, and infrastructure supports rapid experimentation and lowers barriers to entry..Base has several necessary ingredients, such as the Coinbase Mafia alumni network (Polychain, 1confirmation, Paradigm), a developer platform that reduces technical complexity (AgentKit, x402, embedded wallets), regulatory clarity that allows it to enter the US market (108 million Coinbase verified users), and financial resources for ecosystem investments (Coinbase’s quarterly revenue of $1.9 billion, net profit of $432.6 million supports funding and acquisitions, e.g.$375 million Echo acquisition).

However, there remains a gap between vision and realistic execution.Silicon Valley venture capital deploys patient capital over a 7- to 10-year time horizon, willing to accept early losses in the hope of achieving potentially exponential returns by taking equity stakes in sustainable businesses.Financial activities in the Base ecosystem are mainly focused on creator tokens, and the three-month failure rate of tokens is as high as 86%. This is mainly reflected in NFT speculation, rather than equity-financed startups aiming to create long-term value.Coinbase’s Summer 2025 Builder Grant program only awarded a total of $30,000 to 13 projects, a pittance compared to Arbitrum (over $100 million in ARB funding), Optimism (over $200 million in ecosystem funding), or zkSync (over $300 million announced).This indicates that Coinbase relies more on regulatory advantages and distribution channels rather than direct financial incentives to attract developers, which may lead to adverse selection, where projects choose Base more for user access considerations than financial availability or technical advantages.

Developer sentiment analysis shows continued concerns that Base prioritizes viral growth metrics (trading volume of creator tokens) over sustainable infrastructure construction (DeFi protocols, institutional collaborations, developer tool improvements).When ecosystem leadership engages in questionable creator token issuances, or approves official account promotions that result in speculative price spikes followed by 90% crashes (e.g. “Base is for everyone”), it creates the impression that the platform values web craze over serious app development.This perceived risk is reflected in discussions on developer forums, with infrastructure builders preferring alternative Layer-2 networks with “less speculative interference,” suggesting the presence of adverse selection: Base attracts token speculators, while serious developers choose platforms with stronger DeFi ecosystems and less emphasis on creator tokens.

The fundamental question is whether Base can transition from relying on creator tokens to a Silicon Valley-style startup ecosystem before speculation dies down.Financial results for the third quarter of 2025 demonstrate Coinbase’s ability to continue investing (revenue of $1.9 billion, net profit of $432.6 million).The proportion of active addresses (accounting for 55% of all Layer-2 addresses) and TVL leadership ($4.48 billion, the largest Layer-2 network) verify its market appeal.Aerodrome’s legitimate DeFi activity (over $200 billion in transaction volume, $11.2 million in fees) and USDC base ($354.7 million in quarterly stablecoin revenue, $74 billion in circulation) provide the infrastructure for sustainable economic activity.However, deal composition issues, high-profile execution issues, and Aerodrome’s multi-chain expansion have reduced reliance on Base for exclusivity, suggesting that current metrics may partly reflect temporary advantage (speculative boom, protocol exclusivity) rather than a lasting competitive position.The next 12-24 months will reveal whether Base can successfully transform into on-chain Silicon Valley, or whether it will still rely on speculative cycles to produce impressive statistics that mask its underlying economic vulnerability.

Coinbase has the necessary ingredients to build an on-chain Silicon Valley.Coinbase’s deep pockets (quarterly revenue of $1.9 billion, net profit of $432.6 million) provide it with sustainable investment capabilities.The Coinbase Mafia alumni network (Polychain, Paradigm, 1confirmation) mirrors the capital formation benefits of PayPal Mafia.The regulatory infrastructure and 108 million authenticated users create a distribution moat that rival Layer-2 networks cannot replicate.Aerodrome’s trading volume of over $200 billion and quarterly stablecoin revenue of $354.7 million demonstrate that its economic activity is not speculative but compliant.The challenge is execution: transitioning from creator token cycles to patient capital, from viral metrics to institutional adoption, from regulatory advantage to true developer loyalty.Silicon Valley’s success comes from a 7-10 year time horizon and a sustainable business model.Coinbase has the resources, distribution channels, and infrastructure base required.The next 12-24 months will reveal whether Coinbase can realize the vision it envisions.