Source: Coinbase Research; Compilation: Bitchain Vision

Key points:

-

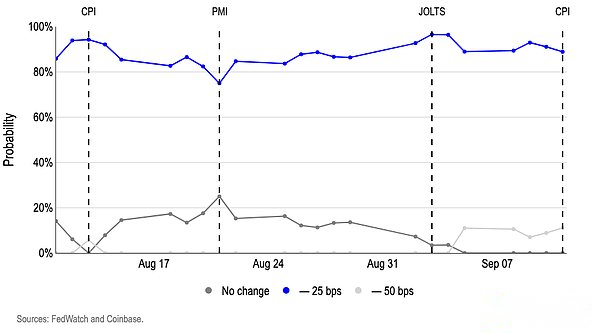

We think the Fed will cut interest rates by 25 basis points on September 17: The weak labor and real estate markets increase the likelihood of a rate cut, but inflation trends make it more likely to take a conservative path.

-

DATs in the PvP stage: Many DATs have mNAV compressed to about 1 and trading volumes declined; however, NAV and supply share continue to rise.

Fed: Current urgency

We think the Fed will cut interest rates by 25 basis points (instead of 50 basis points) next week (September 17) on the Federal Open Market Committee, the reasons are as follows:

-

Inflation trend remained unchanged – driven by continued rise in core services/housing and energy, the overall CPI in August was slightly higher than expected (0.4% month-on-month growth and the median expected growth was 0.3% month-on-month).This data is not enough to reverse the trend of annualized inflation. More importantly, the core CPI remains controllable.(Super Core Services rose only 0.33%, compared to 0.48% in July).But we believe that the data is enough to prevent conservative board members from taking more radical cuts this month.

-

Employment is crucial – Still, expectations for job cuts continue as the U.S. Bureau of Labor Statistics lowered its preliminary estimate of non-farm employment by 911,000 this week, suggesting that labor market weakness may have begun as early as the spring of 2024.If so, then that means the business cycle actually peaked early in the second quarter of 2024, and recent data suggests that we may have extended this downturn.

-

Housing – We believe housing is the biggest risk factor for the U.S. economy at present, as despite median U.S. housing prices rose 2.9% year-on-year, the number of home starts and permits has dropped to its lowest levels in years.Coupled with weak labor market data, the outlook for the real economy is bleak from the perspective of long-term high interest rates.

-

Trustworthiness – Nevertheless, the 50-bp rate cut will be interpreted as suggesting that policy is too tight for a long time, contradicting the guidance of months of “data-dependent”.Progressive policies allow the commission to update more labor and inflation data without locking in radical paths.From the perspective of the policy loss function, the risk of the Fed is asymmetric: the cost of over-easing and re-inducing price pressure is greater than the cost of over-easing and re-examining at the next meeting.

Figure 1: Futures prices currently reflect 100% certainty of the rate cut in September, with a very small possibility of a 50 basis point cut

Deeply explore DAT

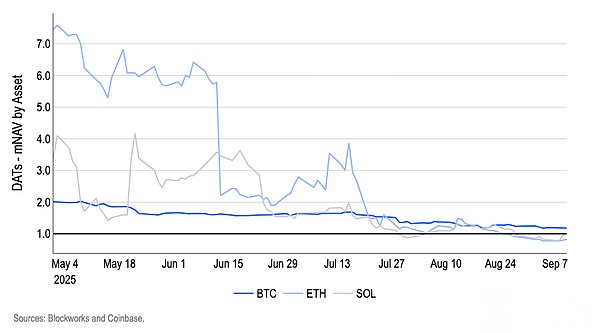

Most digital treasury (DAT) mNAVs have basically tended to be parity, with the compression of ETH DATs being the most significant since May.We believe that this indicates that the “DAT premium” is disappearing, and has entered a PvP stage bound by valuation.The weighted average mNAV of ETH DAT fell from a high of more than 5 times in early summer to less than 1 times in early September(Figure 2).We believe that this model shows that: 1) investors are now pricing ETH DAT stocks as a transfer primarily as a base reserve asset rather than speculative “operation” of cryptocurrency fanaticism; 2) competition among issuers has offset most of the “DAT premium.”

Figure 2. Weighted average mNAV for digital asset treasury by asset class

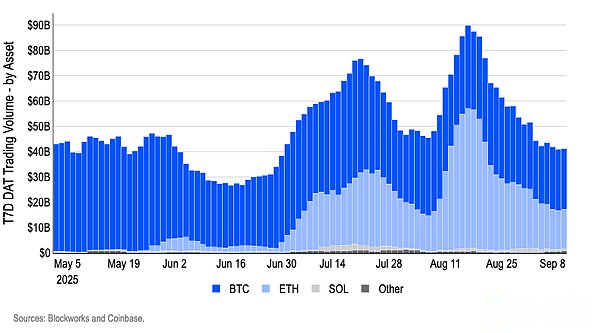

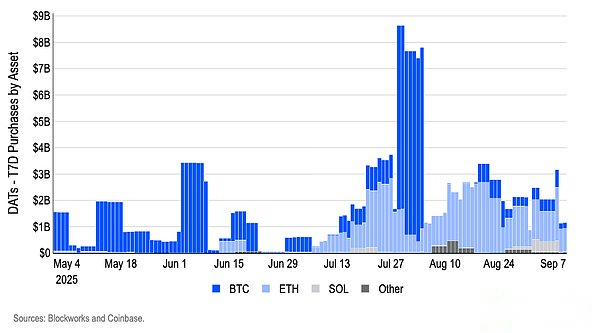

DAT trading volume peaked in mid-August and fell back in September, suggesting that the DAT narrative has faded, while valuations are also re-anchored to the net asset value (NAV).During this period, DAT’s trading volume fell by about 55% over the past 7 days, and the share of ETH DAT narrowed along with the share of BTC DAT (Figure 3).Using volume as an indicator of attention, we believe that the narrative of DAT is weakening marginally, which may reduce market participants’ willingness to pay speculative premiums.Treasury purchases surged in late July/August, trading volumes surged, followed by cryptocurrency price consolidation, highlighting the liquidity-driven nature of trading: when major purchase momentum slows down and macro uncertainty suppresses market sentiment, enthusiasm weakens and mNAV falls back to about 1 (Figure 4).

Figure 3. T7D DAT Trading Volume – Classified by Asset

Figure 4. T7D DAT Purchase – Classified by Asset

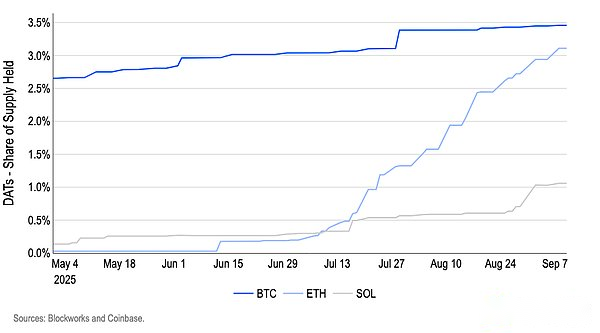

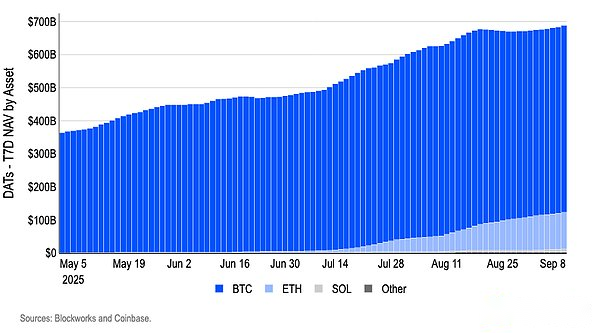

However, despite the decline in trading volume and the compression of premiums, balance sheet absorption continues – most obviously, ETH – which leads to a shift in the center of gravity from mispricing toward liquidity and structure.DAT’s net asset value (NAV) and the total supply share held by DAT continued to rise in September (Charts 5, 6), which meansEven if DAT’s equity pricing is close to net asset value (NAV), they are structural demand absorbers for circulating supply.We believe that the combination of rising ownership share with mNAV ≈ 1 defines the PvP stage.Cross-sectional results depend on execution and policy choices (financing portfolio, fund purchase rhythm, treatment of pledged ETH), and at the overall level, the binding variable is simply the rhythm and breadth of net fund purchases, not any lasting equity premium.

However, we note that if the cryptocurrency market regains momentum, the PvP phase may reverse because we believe that under the risk appetite mechanism, when the focus exceeds the main issuance, the speculative premium may reappear, forming a brief wedge.We believe thatThe key factor that determines whether such mechanisms can return may be macro liquidity—especially the trend of policy interest rates——We believe thatMacro liquidity plays a greater role in shaping risk appetite than the fundamentals of a specific agreement.

Figure 5. T7D DAT Net Asset Value – By Asset

Figure 6. The proportion of assets held by DAT as total supply