Author: danny Source: X, @agintender

Assuming that the early collapse of DAT of currency stocks is inevitable, how should we deal with it for investors?What strategies should be adopted?What are the algorithms and standards?Are there any successful cases in the market?What are their core competitive advantages?

Reading guide:

1. Friends who have not read the previous article have suggested to go first:Coin stock hidden story: The half-cutting method hidden in “equity dilution” and mNAV algorithm》

2. If you simply want to see the case analysis, you can read it down.

Part 4: The truth of the “Moat” and the future of the DAT model

After understanding the operating mechanism and risks of “coin stocks”, a core question surfaced: What is the long-term competitiveness of DAT companies and their “moat”?Where will their future go?

4.1. The truth of the moat: a “capital flywheel” that relies on market sentiment

The true “moat” of DATs does not originate from its business itself, but is a highly contextualized and fragileFinancing Advantages.Its core competitiveness is the cycle of liquidity-strong financing costs: “Financing capability → Buy more coins → Improve investor return expectations → Attract more liquidity → Reduce financing costs → Further enhance financing capabilities”. This mechanism, namely the “capital flywheel”, is to understand the essence of its business model.

Positive cycle (in a bull market):

This flywheel can produce a strong positive driving force in a bull market.

-

High premium is fuel: The company’s stock price is traded at a price higher than the digital net asset value (NAV) it holds, forming a “equity premium” (mNAV Premium).This premium is the key fuel for the entire flywheel start.

-

Financing capacity is activated: With high premiums, companies can raise “Accretive” financing by issuing new shares or low-interest convertible bonds, i.e. exchange high-valuation stocks for funds and purchase more digital assets, thereby expanding their balance sheet without diluting or even increasing the currency content per share.

-

Liquidity and low cost: When market sentiment is high and stock liquidity is excellent, companies can easily sell large amounts of new shares in the open market without causing too much impact on the price, which greatly reduces the frictional cost of financing.

-

“Buy, buy, buy” strengthens the narrative: The company will continue to buy more digital assets the funds raised, which not only increases the company’s net asset value, but also strengthens its market narrative as a “growth engine”, attracts more investors, further pushes up the stock price and premium, forming a strong positive feedback loop.

Reverse Destruction (in a bear market):

However, this powerful engine has a fatal weakness: it relies entirely on sustained bull sentiment and high stock premiums.Once the market turns, the flywheel will quickly rotate inversely, becoming a “death spiral”:

-

The premium disappears and the fuel runs out: When the underlying currency price falls, the stock price of “coin stocks” will fall even harder, causing its mNAV premium to shrink rapidly and even become a discount.

-

Financing capacity is frozen: Once the premium disappears, any financing through additional stock issuance will be “impairment” (Dilutive).At this time, the company could no longer provide value-added financing, and its core growth story went bankrupt.Financing capacity—this only moat—dried instantly.

-

Negative feedback loop: The exhaustion of financing channels and the destruction of growth narratives will trigger panic selling among investors, further suppress the stock price, and form a vicious cycle, which may eventually lead to the collapse of stock prices.

Therefore, the moat of DATs is extremely narrow and unstable because it relies entirely on fickle capital market sentiment.Once market sentiment reverses and the premium disappears, the moat will dry up instantly and the company will lose its only competitive advantage.

4.2. Comparative Case Study: Practice and Variation of Strategies

Despite similar basic models, different DATs show significant differences in specific strategies implementation, which reflect their different understandings of their own positioning, market environment, and regulatory constraints.

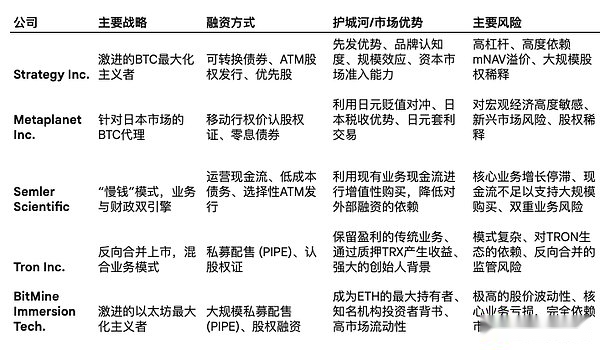

Strategy Inc. (MSTR) – A radical pioneer

As the pioneer of the model, MicroStrategy’s strategy is the most radical.Not only does it use a large number of debt instruments such as convertible bonds to maximize leverage, its founder Michael Saylor has also shaped a “soft moat” for the company through its strong personal brand and ongoing sermons.He successfully tied MicroStrategy to BTC in-depth, making it the most well-known BTC proxy stock in the hearts of global investors, and this brand awareness has consolidated its mNAV premium to a certain extent.

Metaplanet Inc. (3350.T) – Flexible International Adapter

Metaplanet’s case demonstrates how the DAT model innovates and adapts to the market environment in a specific country or region.Its strategy cleverly takes advantage of Japan’s unique macro and regulatory environment:

-

Yen Carry Trade: Against the backdrop of the Bank of Japan’s long-term ultra-low interest rates, Metaplanet borrowed the yen at a cost of nearly zero and converted it into BTC expected to appreciate in the long term, thus conducting macro arbitrage.

-

“Moving Strike Warrants” (Moving Strike Warrants): Since Japanese regulation does not allow the ATM issuance mechanism common in the US stock market, Metaplanet innovatively uses a warrant whose exercise price is linked to the closing price of the previous day.This design ensures that warrants are exercised only when the stock price rises, thus achieving the effect of dilution financing similar to ATMs at high stock prices.

-

Tax Advantages: Japan imposes high progressive taxes on the income from individuals who hold cryptocurrencies directly, while the capital gains tax rate for investing in stocks is much lower (about 20%).This tax difference makes Japanese investors holding BTC indirectly by buying Metaplanet stocks, which is more attractive in taxes than buying BTC directly, creating localized demand for their stocks.

Semler Scientific (SMLR) – a cautious business integrator

Semler Scientific represents another more conservative strategy—the “Slow Money” model.The company plans to use the stable cash flow generated by its core healthcare business to gradually and prudently purchase BTC, aiming to achieve a more “value-added” asset accumulation for shareholders.This model is theoretically more sustainable because it does not rely entirely on external financing.However, the challenge is that the company’s core business is facing growth bottlenecks and regulatory pressures, which complicates the narrative that it generates enough cash flow to support large-scale BTC purchases.

Tron Inc. (TRON) – Reverse Merge and Mixed Mode

The case of Tron Inc. demonstrates a non-traditional path to market and business structure.The company, formerly known as SRM Entertainment, entered the open market through a reverse merger with TRON DAO and was renamed Tron Inc.This strategy allows it to quickly become a Nasdaq listed company and focus on building fiscal reserves for TRX tokens.Its uniqueness is the hybrid business model: it retains the original business of designing and manufacturing customized goods for large entertainment venues such as Disney and Universal Studios, while also pioneering a blockchain fiscal strategy.In addition, the company actively uses its TRX reserves for pledge, generating annualized revenue of up to 10% through platforms such as JustLend, which provides non-dilutive cash flow for its operations.(From a bird’s eye view, $TRX token does not leave the Tron network, this is)

BitMine Immersion Technologies (BMNR) – The Radical Ethereum Whale

BitMine (BTMR) represents the aggressive expansion of the DAT model to assets outside BTC.The company has transformed from BTC mining business, focusing on becoming the world’s largest enterprise-level holder of Ethereum (ETH) and has set an ambitious goal of holding 5% of the total ETH in circulation.Its strategy is characterized by an astonishing financing speed, accumulating billions of dollars in ETH reserves in a short period of time through large-scale private placements (PIPEs) and equity financing.This radical accumulation strategy attracted high-spec investors including Peter Thiel’s Founders Fund and Stanley Druckenmiller, and was chaired by Fundstrat’s Tom Lee.However, BMNR’s stock price performance is extremely unstable, and after a surge of thousands of percentage points, it then pulls back sharply, highlighting its high-risk and high-return characteristics.Due to its meager revenue in its core business (mining) and its loss-making state, its valuation is almost entirely driven by market expectations of ETH prices and confidence in its financing capabilities.

4.3. Next evolution: “productive finance”

Faced with the inherent vulnerability of passive holding strategies, the DAT model is ushering in an important evolution, namely, from “passive finance” to “productive finance”.

The traditional BTC fiscal policy strategy is essentially a passive “digital gold” strategy, and the assets themselves do not generate any cash flow.The “productive finance” model focuses on holding digital assets that can generate returns through network native mechanisms, mainly public chain tokens that adopt POS consensus mechanisms, such as ETH and SOL.

By staking the ETH or SOL you hold, companies can receive token-denominated rewards directly from the agreement.This pledge income is an endogenous, crypto-native “interest” that does not rely on the traditional credit market and provides a stable, non-diluted source of cash flow for the company.The emergence of this model marks the possibility that DATs may transform from pure financial engineering carriers to operating companies with real crypto-native businesses.For example, companies such as DeFi Development Corp. (DFDV) are focusing on accumulating SOLs and generating staking income by operating verification nodes.(TRON Inc is also at the forefront of the times)

This evolution toward “productive finance” is a strategic response to the reality that the moat of passive holding model is too fragile.By creating endogenous cash flows that are decoupled from capital market sentiment, these companies are trying to build a wider, deeper economic moat, reducing their extreme reliance on financing capabilities in the bull market and providing a stronger foundation for their long-term survival and development.

Part 5: Summary – See the essence through the fog

For investors who wish to invest in such companies, they must abandon the view that they regard them as simple “crypto-asset stocks” and instead evaluate them as a highly speculative, actively managed leveraged fund.Its final investment performance depends on the complex interactions of the following four core variables:

-

Price performance of underlying crypto assets: This is the basis for determining the company’s net asset value (NAV).

-

Management’s financial engineering capabilities: That is, how fast, how low, and how small the company raises funds and converts them into assets.

-

Market sentiment in the stock market: This is the key to determining the premium level of a company’s mNAV, which directly affects its financing capabilities and the strength of the “flywheel effect”.

-

Net crypto asset holding content per share: This determines the level of crypto assets that are evenly distributed to each share.

Taking Strategy Inc BTC as an example, when evaluating “coin stocks”, the following key indicators should be focused on monitoring rather than just focusing on the company’s total BTC holdings announced:

-

Crypto Asset Content per Share (After Completely Diluted): This is the most important indicator to measure the true exposure of shareholders.Investors should closely follow their historical trends to judge whether the company’s financing activities are value-added or impaired in the long run.

-

mNAV premium trend: Is the premium expanding or shrinking?The continued contraction of premiums is a clear signal that market confidence is weakened and risks are intensified.Comparing it with similar companies and related ETFs can better evaluate whether its valuation is reasonable.

-

Financing/additional terms: Carefully study the specific terms of each company’s bond issuance or additional issuance, including the conversion price, interest rate of convertible bonds, as well as the execution scale and price of the ATM plan.These details reveal future dilution risks and financial stress for the company.

Know the truth and know the reason.

The “capital flywheel” that drives DAT’s stock price soaring in a bull market is precisely the fundamental reason for their accelerated decline in a bear market.Its core business model—by leveraging high stock price premiums to finance and buy more assets—is a double-edged sword in itself.This extreme dependence on capital market sentiment determines that their destiny must be closely linked to the cyclical fluctuations of the market.