author:Miao Yanliang, Zhang Xinyu, etc., Source: CICC Research Report “Stablecoins, Financial Markets and RMB Internationalization”

summary

Recently, the financial market and the whole society have held many discussions on topics related to stablecoins, but there are still many differences.For example, what exactly is the essence of a stablecoin, is it a revolutionary innovation or is it just a new vest for old things?Different groups have different perspectives on stablecoins. How should we dialectically view the impact of stablecoins on the financial market and the international monetary system and grasp the main contradictions?For China, should we consider participating in the development of stablecoins?We propose,Stablecoins have the potential to become a new type of infrastructure.And through analysisThe incentive compatibility mechanism of each participant in stablecoin,We will further look forward to the potential impact of stablecoins on the financial market and the international monetary system, and further explore China’s response strategies.We believe thatThe introductory period of infrastructure is an important development opportunity. The issuance of offshore RMB stablecoins may be a priority for China to participate in the development of stablecoins; however, it should be noted that stablecoins are only the “art” to promote the internationalization of the RMB. Whether the RMB can become a widely trusted international currency fundamentally depends on the “Tao”, that is, the “law anchor” and “functional anchor” of the RMB.

What is a stablecoin?Why has it attracted attention recently?

What is a stablecoin?Balance between “centralization” and “decentralization”

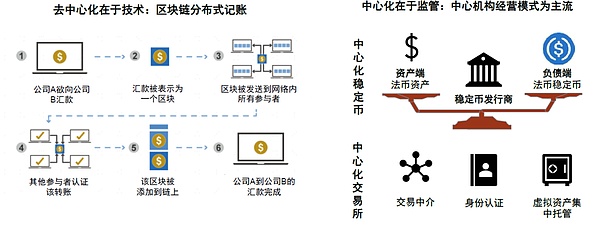

A general consensus is that stablecoins are the “on-chain cash” of the crypto world and are also the bridge connecting encryption and the real world.We summarize its essence in one sentence asStablecoins are the most decentralized in centralization and the most centralized in decentralization.”.Decentralization lies in technology, and centralization lies in operations and supervision.This dual feature not only gives the advantages of stablecoin blockchain technology, but also ensures its compliance in the real financial system.

From a technical level, stablecoins inherit the “decentralized” gene of blockchain technology.Relying on distributed ledger technology, we have realized peer-to-peer transactions and got rid of our dependence on traditional financial intermediaries.Multiple nodes in the network share ledgers, and each transaction node participates in ledger maintenance to ensure the transparency and immutability of transaction records.This technological architecture makes stablecoins the free circulation of “digital cash” in the crypto world.

At the same time, the other foot of the stablecoin is in traditional finance. The mainstream stablecoins adopt a centralized operation model and need to be regulated by the traditional financial system.In the issuance process, mainstream stablecoins such as USDT and USDC adopt a centralized operation model. Issuing institutions must hold sufficient fiat currency reserves on the asset side in order to mint the corresponding number of stablecoins on the liability side, thereby achieving stable currency value.In the trading process, users currently mainly exchange fiat currency and stablecoins through centralized exchanges (CEX). These exchanges assume the role of trading intermediary similar to traditional exchanges, perform KYC (know your client) certification like traditional financial institutions, and centrally custodialize users’ virtual assets.It is this centralized operational architecture that enables regulators to effectively regulate stablecoins, prevent risks such as insufficient asset reserves and hacker attacks, and ensure their compliant operation in the real financial system.This dual characteristics of technology and operation allow stablecoins to maintain the advantages of blockchain technology, but also gain recognition from the traditional financial system, becoming a bridge connecting the two worlds.

Figure 1: Stablecoins are “the most decentralized in centralization and the most centralized in decentralization”

Source: GAO, Binance, CICC Research Department

What is a stablecoin not?Not a currency, not a money market fund

Stable coins are not currency, they are tokens.The credit of fiat currency stablecoins comes from the national sovereignty represented by fiat currency, and on this basis, private enterprise credits that are self-proven with reserve assets are superimposed.Therefore, there must be a demand for fiat currency before a demand for stablecoins anchoring the fiat currency will be generated.The central bank digital currency (CBDC) is a currency issued by the central bank and its credit comes directly from national sovereignty.The similarity between the two is that they are both digital currencies, and some CBDCs explore the use of blockchain and distributed accounting technology in some links.

What is the difference between stablecoins and money market funds?Some views believe that stablecoins are no different from money market funds such as Yu’ebao. There is no need to develop stablecoins at a time when money market funds are developed.It is true that the two have similarities. Both allocate high-liquid assets such as cash and short-term bonds on the asset side, but they also have obvious differences: in terms of liquidity, stablecoins can be cashed almost at any time and can also be used for payment directly, but money market funds are usually subject to transaction and redemption rules, and the payment function of domestic Yu’ebao is supported by platform advance payment.In terms of income mechanism, stablecoin issuing institutions obtain investment gains and losses from reserve assets and do not directly pay interest to stablecoin holders. Holders can mortgage stablecoin to exchanges and other platforms to obtain income; money fund holders bear investment gains and losses, obtain cash dividends, and choose whether to reinvest dividends, and fund companies only earn management fees.

Stablecoins have been around for a long time, why has they attracted attention recently?

Recently, the market and the whole society have increased its attention to stablecoins, which is often regarded as a “new invention”, but stablecoins are not new in the cryptocurrency industry.The first stablecoin BitUSD has been issued more than ten years ago. Why has the stablecoin suddenly attracted great attention recently?

Recently, multiple event factors have catalyzed the increase in attention to stablecoins.1) The United States and Hong Kong, China, have made significant progress in stablecoin legislation.On May 20, the “Guiding and Establishing a Dollar Stable Coin National Innovation Act” (“Genius Act”, GENIUS Act) passed a key US Senate process to vote, gradually advancing until July 18, officially signed by US President Trump [2].On May 21, the Legislative Council of Hong Kong also passed the “Stablecoin Bill”, which will take effect on August 1 [3].2) Circle is launched.Circle is the second largest issuer of USDC, which accounts for about one-quarter of the total stablecoin scale. It has attracted much attention because it was the first IPO in the stablecoin field and rose sharply after its listing.3) Some Chinese securities companies have successively obtained relevant licenses for Hong Kong crypto asset business.

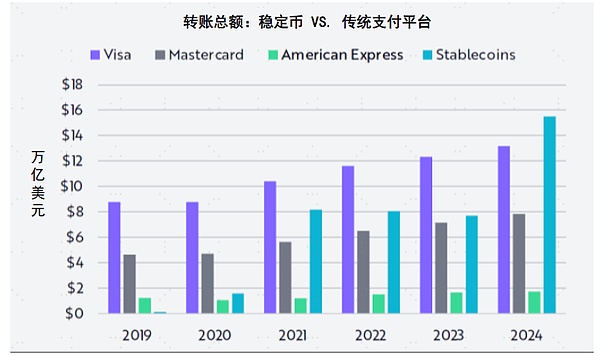

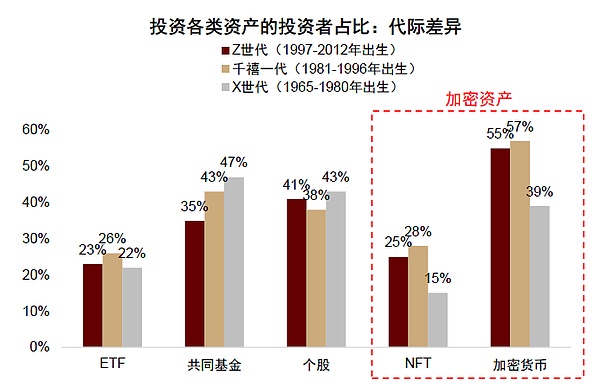

Events are just appearances, behind which are technical support and public opinion, quantitative change leads to qualitative change.At the technical level, the scale and application of stablecoins are gradually increasing.The current total scale of stablecoins has exceeded US$260 billion, and the transaction scale has gradually increased. According to ARK Invest, the total amount of stablecoins transferred in 2024 reached US$15.6 trillion, surpassing Visa for the first time in years (Figure 3).At the public opinion level, the increase in the US’s voice for younger generations with higher acceptance of cryptocurrencies has brought about a change in public opinion.FINRA and CFA survey research [4] shows that relatively young Gen Z and millennials in the United States generally account for a higher proportion of investment in cryptocurrencies and non-fungible tokens (NFTs) than older Gen Xs (Figure 4).As we grow older, the younger generation’s pricing power in the market and the discourse power in society have gradually increased; more and more Generation Z obtains voting rights after adulthood, and the political discourse power also increases, which directly affects the progress of stablecoin legislation.

From the perspective of narrative economics, the narrative of stablecoin conforms to the characteristics of “successful narrative”, has a high transmission rate, and forms a “circle-breaking effect”.In Narrative Economics, Robert Shiller believes that narratives transmitted through word of mouth or media can promote the formation of specific views or values, and narratives with certain elements are more likely to achieve high communication rates and low forgetting rates, becoming relatively successful narratives.In our previously released “Technology Narrative, Geographical Revaluation and Global Capital Relay”, combined with Schiller’s works and scholarly views [5], we summarized the four key elements of “successful narrative”, and the current stablecoin narrative is in line with these elements:

► 1) Repeatability: Through repeated publicity and continuous exposure of social media traffic, while increasing the spread rate, it also significantly reduces the forgetting rate.Since the end of May, many important events have occurred in the stablecoin field. Many well-known experts and scholars have expressed relevant opinions. In addition, the information is widely spread and fast and has many sources of communication in the era of self-media, which has prompted the public to repeatedly contact information related to stablecoin.

► 2) Concern for one’s own nature: When people feel that they are related to the interests of the story, the communication effect is best.Stablecoins can reduce the cost of cross-border payments. Cross-border e-commerce, overseas migrant workers, overseas student families and other groups have vital interests in cross-border payments, so pay attention to stablecoins.However, stablecoins can gain greater attention, which is closely related to the “global currency game” element in the stablecoin narrative.US Treasury Secretary Besent said that “stablecoins can stabilize the status of the US dollar” [6], and some narratives therefore lead to “global currency game”, thereby strengthening the focus of stablecoin narratives and arousing the attention of larger groups to stablecoins.

► 3) Narrative constellations: A system composed of multiple interrelated narratives is called narrative constellations, which is more influential and disseminated than a single narrative.This year, the topic of “global game” has been developing continuously, from scientific and technological issues triggered by AI, to cultural issues triggered by Labubu, to trade issues triggered by “reciprocal tariffs”, and then to monetary issues triggered by stablecoins, forming a multi-faceted “global game” narrative constellation.

► 4) Self-reinforcement: People tend to share content that can strengthen their self-concept. When narratives, actions and results form a cycle of self-reinforcement, the sense of identity will be further consolidated and the rate of forgetting will decrease.As the stablecoin narrative fermentes, some investors believe that stablecoins are an important development direction with potential, so they invest in related concept stocks and other assets, which triggers the price increase of related assets, and the rise in asset prices becomes a verification of their views, thus forming a self-reinforcement cycle.

Stablecoins meet the characteristics of “successful narrative”, have a high transmission rate and a wide range of dissemination. From the niche “currency circle” that already understands and pays attention to stablecoins, it has spread to the mass group that did not pay attention to cryptocurrencies in the past, forming a “circle-breaking effect”.

Chart 2: The total amount of stablecoin transfers in 2024 exceeds Visa and Mastercard

Source: ARK Invest Big Ideas 2025, CICC Research Department

Figure 3: Young people are more receptive to crypto assets

Source: FINRA, CFA, CICC Research Department,Note: The data comes from an online survey from November to December 2022, among which Generation Z only surveyed those who were over 18 years old at that time.

Stablecoins are new infrastructure supported by technology

Although the current market’s high attention to stablecoins and high expectations of their influence are affected to a certain extent by the “FOMO” mentality, we believe that stablecoins are worth paying attention to as a financial infrastructure.

Stablecoins are a new type of financial infrastructure with characteristics of economies of scale and network effects.In cross-border payment scenarios, compared with cross-border clearing systems such as SWIFT, stablecoins can simplify the process. After users have crypto wallets, they can use distributed accounting to realize point-to-point transactions, integrating information flow and capital flow, and realizing “payment is settled” when both parties recognize stablecoins. However, the current up and down chains still face some difficulties.Stablecoins also have infrastructure characteristics such as economies of scale and network effects. The market value scale is positively correlated with price stability and liquidity. If competition is liberalized, the market structure is likely to develop in the direction of dominance of several companies rather than blooming a hundred flowers.The scope of use of stablecoins is also being expanded and has exceeded the field of cryptocurrency trading. In addition to cross-border payments, stablecoins are also regarded as a value-preserving asset.In many countries and regions with underdeveloped financial infrastructure, due to the large fluctuations in the value of their local currency, local residents are more motivated to hold stablecoins anchored to the US dollar.At the same time, stablecoins are also used as collateral assets and liquidity media in the DeFi ecosystem.

In the genealogy of global value flow, stablecoins are like a “supersonic passenger plane” across the continent.If traditional bank transfers are still stuck in the era of roads and railways – queues, speed limits and frequent transfers – then this passenger plane will deliver “capital passengers” to all ends of the world in an instant with its programmable engine.However, every takeoff still requires passing the “customs” – KYC, AML (anti-money laundering) and other security checks; their routes and terminals are mapped to open public chains, cross-chain bridges and various exchanges, jointly building a backbone transportation network with digital value.

Figure 4: Stablecoin market value scale negatively correlates with volatility

Note: The size of the circle represents the operating time of the stablecoin.The median volatility of each stablecoin is calculated based on the daily volatility from January 1, 2019 to September 30, 2023.The daily volatility is the 30-day moving standard deviation (annualized) of the daily yield, and the closing price is based on the UTC zero-point closing price defined by CoinGecko.The PAX Gold overlaps the logo circles of Tether Gold, with the PAX Gold slightly smaller market capitalization and a high median volatility.Market value data as of September 30, 2023.

Source: BIS (2023). Will the real stablecoin pls stand up?, China Securities Research Department

Application and impact of stablecoins in financial markets

How does the stablecoin industry operate?Trust mechanism compatible with incentives

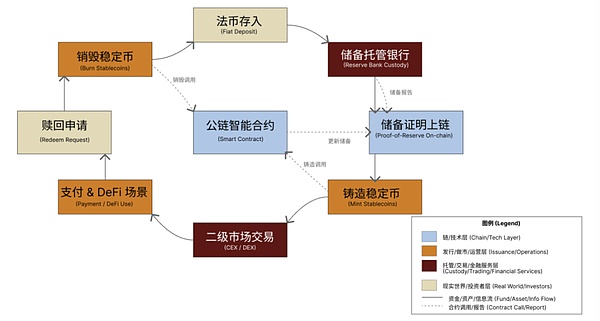

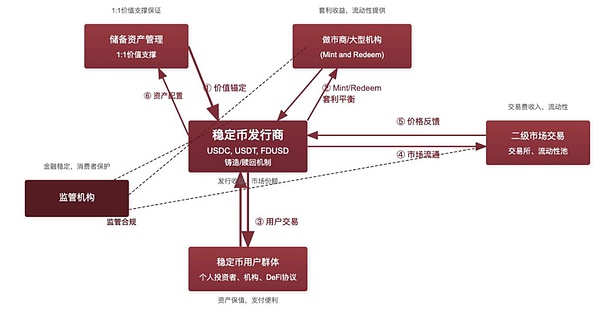

As a key hub connecting off-chain fiat currency and on-chain encryption ecosystem and laying the infrastructure for the next generation of cross-border digital finance, how does the stablecoin industry operate?Which core participants are there, how do they form mutual trust and how can they achieve long-term development?

We can understand the trust mechanism among participants through the life cycle of stablecoins.The trust of stablecoins begins with the close mapping of off-chain fiat currency reserves and on-chain smart contracts, which lays the foundation for the security and transparency of the subsequent life cycle.The trust mechanism of stablecoins begins when traditional fiat currencies are deposited into custodial banks.After the funds are deposited, the issuer mints an equally valued stablecoin on the chain through a public chain smart contract (i.e., programmable protocol code deployed on the open blockchain).The contract automatically performs issuance and redemption logic when the 1:1 guarantee and reserve disclosure conditions are met, and reserve proof is disclosed to any third party through a near-real-time on-chain data interface.The stablecoins held by users in payment or investment scenarios can be exchanged into fiat currency at any time according to the “minting-circulation-redemption-destruction” process.Compared with the traditional post-reconciliation model, open and automated contract verification enables on-chain assets and bank custody funds to maintain continuous mapping.

In order to promote the long-term development of the stablecoin ecosystem, it is crucial for the relevant parties in the industrial chain to achieve incentive compatibility.Among the main participants of stablecoins, users obtain payment efficiency and asset preservation, issuers obtain income from the interest rate spread of reserve assets as reserve funds, market makers and authorized institutions earn price spreads to provide liquidity, custodial banks charge storage fees, and regulators focus on consumer protection and financial risk prevention.Against the backdrop of rising global interest rates, the interest rate spread generated by reserve funds invested in short-term treasury bonds has expanded significantly, and the asset scale and liquidity risks managed by the issuer are gradually approaching large money market funds.The regulatory focus therefore needs to further evaluate the liquidity mismatch driven by interest rate spreads based on anti-money laundering and identity identification to ensure that the efficiency and security of the stable currency system are taken into account.

Figure 5: The Life Cycle of Stablecoins – Shaping the “Close Loop of Trust”

Source: Circle “USDC White Paper”, Tether “TransparencyReport”, Paxos “BUSDMonthlyReserveReport”, Etherscan on-chain data, CICC Research Department

Figure 6: How participants and value streams – How to achieve incentive compatibility in the stablecoin industry chain

Source: Circle, MakerDAO, DeFiLlama, Messari, CICC Research Department

The “impossible triangle” of stablecoins: price stability, decentralization, capital efficiency

Different stablecoins mechanisms are also different. What kind of stablecoins are more likely to develop in the long term?There is an “impossible triangle” for stablecoins: As a bridge connecting the crypto world and the real world, its primary goal is “price stability”, but from practical experience, it is often necessary to weigh “price stability”, “decentralization” and “capital efficiency”: 1) If you pursue price stability and capital efficiency, you need to rely on the credit of centralized institutions. For example, the fiat currency stablecoins USDC and USDT stablecoins rely on the credit of Circle and Tether companies, which violates the decentralization principle; 2) If you pursue price stability andDecentralization requires hedging risks through excessive collateral. For example, the over-collateralized stablecoin DAI in the early stage required ETH to be mortgaged at a 150% collateral rate, and the capital efficiency is relatively low; 3) If you pursue capital efficiency and decentralization, you need to rely on algorithms to adjust the supply chain and not anchor fiat currency or secure assets. For example, the algorithmic stablecoin UST maintains price stability through a dual token mechanism with LUNA, but in the extreme market, the failure of this regulation mechanism will bring about sharp price fluctuations (UST decoupling collapse in May 2022) and it is difficult to achieve security goals.Judging from the practical experience of the failure of the algorithmic stablecoin UST, the current successful stablecoins focus on achieving the goal of “price stability” and thus play the role of intermediary currencies.therefore,The development direction of stablecoins is to integrate with traditional finance and accept certain centralized supervision.This is also why most mainstream stablecoins are centralized stablecoins.

Figure 7: The “Impossible Triangle” of Stablecoins: Price Stable, Decentralized, Capital Efficiency

Source: “Decentralised Finance” EU Blockchain Observatory and Forum, CICC Research Department

What impact does stablecoins have on the financial market?Efficiency, universal, stable perspective

As a new infrastructure, if stablecoins can develop on a large scale, they will have a multi-faceted and deep-seated impact on the entire financial market, which includes both the optimization of traditional financial models and the new risks and hidden dangers brought by breaking through the traditional framework.Specifically:

First, as a payment tool, stablecoins have the characteristics of convenience, efficiency and low cost, and are especially suitable for cross-border payments.Global cross-border payments have long been relying on the traditional bank wire transfer system based on SWIFT. Under this model, commercial banks open clearing accounts at overseas agency banks, then send cross-border messages based on SWIFT channels, and then use the payment and clearing system of overseas agency banks to complete cross-border fund payment and clearing [8]. Among them, SWIFT is a financial information transmission system, mainly responsible for the transmission of information flows and does not process capital flows.However, the traditional cross-border payment system has long been trapped by problems such as relatively high costs and low efficiency. In contrast, we believe that stablecoins are fully reflected in cross-border payments based on their “integrated information flow and capital flow” characteristics: First, improve transaction speed, stablecoins are based on the “point-to-point” transaction characteristics of blockchain, which is different from the multiple agency banking links under the traditional system. Stablecoin payment can reduce the intermediate links, achieve near-instant arrivals, and support 7×24-hour transactions, which helps improve payment efficiency; Second, reduce payment costs. Traditional cross-border payments are relatively high due to their highly centralized infrastructure, such as monopoly, complex and lengthy processes, and layer-by-layer transfer of compliance costs. However, stablecoins have low handling fees due to their digital economy characteristics. At the same time, they are currently in the early stage of development and relatively sufficient competition in the stablecoin market, which is conducive to achieving low-cost cross-border payments.

It should be noted that the high efficiency of stablecoins in cross-border payments is more reflected in the transmission of funds in the on-chain channel, but the current upper and lower chains are still facing certain problems.If stablecoin payment is compared to a “stablecoin sandwich” architecture (Stablecoin Sandwich) [9], then stablecoin may make the middle part of its “sandwich” more efficient and valuable, that is, it has a stronger substitution effect on traditional fund transmission channels. However, both ends of the “sandwich” still face certain difficulties, that is, it still relies more on the traditional financial payment system.On the one hand, there are difficulties in managing cross-border capital liquidity, stablecoin payment can achieve free exchange of currencies with various countries, and faster and more efficient transfers can be achieved between different regions, which brings certain difficulties to capital flow control.On the other hand, there is still a cost to exchange between stablecoins and fiat currencies.(i.e. on-ramp and off-ramp), especially for cross-border payments between some developed countries, the exchange cost between stablecoins and fiat currencies is even higher than the cost of direct exchange of traditional banks in foreign exchange markets [10]. In this case, the speed advantages and cost efficiency advantages of stablecoins may be affected to a certain extent.

In addition, compared with cross-border payment scenarios, the advantages of stablecoins in local payment scenarios are not obvious.For example, domestic third-party payment platforms such as WeChat/Alipay have formed a strong network effect and economies of scale, with the advantage of being incumbent, and the convenience of Internet wallets and the perfection of infrastructure are difficult to replace; while overseas, in addition to third-party payment platforms such as Apple Pay/PayPal, traditional bank cards rely on their points/credit system and other advantages, and at the same time, card organization/clearing networks such as Visa/MasterCard are also more efficient.From the perspective of the convenience and security of payment, we believe that stablecoins may not have obvious advantages in the same currency zone, and their potential to reduce costs and improve efficiency is still more focused on cross-border payments.Just like a passenger who arrives at the airport on the stablecoin “supersonic passenger plane”, he still needs to take a taxi after landing and use an electronic wallet or bank card to complete the last mile.

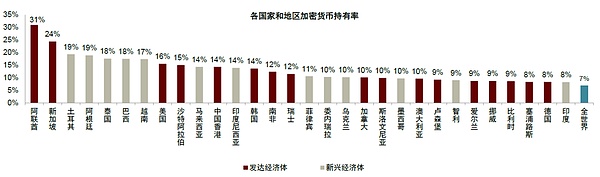

Second, stablecoins help expand service coverage and improve financial inclusion, especially in emerging markets, and are increasingly being used as a savings tool.Relying on technology empowerment, stablecoins are committed to improving financial accessibility, especially in retail financial scenarios, which are mainly reflected in: First, lowering the threshold for financial access and improving financial inclusion. According to World Bank statistics, there are still about 1.3 billion adults around the world who do not have bank accounts (Unbanked population) [11], especially in some developing countries and remote areas, where the traditional financial system is relatively underdeveloped, and stablecoins give them a more convenient channel to obtain financial services.Second, it serves to maintain residents’ wealth, especially asset hedging in high-inflation economies. For example, in high-inflation Turkey, Argentina and other countries, the proportion of their cryptocurrencies is close to 20%, far exceeding the global average of 7%, and its cryptocurrency transactions are mostly completed through stablecoins [12]; for some high-inflation regions such as Africa, Southeast Asia, and Latin America, due to the relatively stable characteristics of stablecoins’ currency value and can be used for value preservation and exchange, stablecoins are increasingly being used as means of savings and becoming an important tool to fight local inflation and currency depreciation.

Figure 8: Comparison of SWIFT vs. Web3.0 Trading Network

Source: BIS, SWIFT, McKinsey, Solana, Tether, CICC Research Department

Figure 9: The proportion of cryptocurrency holders in high-inflation areas such as Türkiye and Argentina is relatively high

Note: 2024 data Source: Triple-A, CICC Research Department

Third, we also need to pay attention to the impact on stability.Stable coins help improve payment efficiency and improve financial inclusiveness, but at the same time, they should also weigh the relationship between efficiency, inclusiveness and stability. Specifically: on the one hand, trade-off efficiency and stability.The relatively complete regulatory system under the traditional cross-border payment system brings relatively high payment costs, and banks face strict reviews on customer identity identification KYC, anti-money laundering AML, anti-terrorism financing CFT, etc.In contrast, the regulatory environment faced by stablecoins is relatively loose, and compliance review has not yet fully covered the above links, and there is a certain regulatory arbitrage space; and the issuing entity may move to offshore “regulatory depressions” (such as the Cayman Islands and the Marshall Islands) to evade supervision.On the other hand, weigh in inclusiveness and stability.For some developing countries with fragile fundamentals, financial coverage can be expanded through stablecoins and resist local inflation. However, considering that about 99% of stablecoins are still denominated in US dollars, if these countries gradually rely on US dollar stablecoins, this may cause stablecoins to have a substitution effect on local fiat currencies, threaten their monetary sovereignty, and even bring certain challenges to the effectiveness of their monetary policies and the stability of the financial system.

In addition, the potential risks of stablecoins themselves will also affect the stability of financial markets.First, runs and liquidity risks.Since stablecoins are issued by private institutions and stability depends on the quality and transparency of their reserve assets, if the reserve mechanism is insufficient or the asset quality is facing downward pressure, it may lead to a trust crisis, which may easily lead to a run, resulting in a sell-off of its held assets, which indirectly affects the stability of the traditional financial system and even triggers a wider liquidity risk.The second is the disintermediation of deposit moving and finance.Stable coins may divert bank deposits, loans, foreign exchange and other businesses. For example, residents in some high-inflation countries tend to hold stablecoins instead of bank deposits, and cross-border payment and settlement of stablecoins bypass the traditional remittance system of banks. If decentralized finance further develops, it will even aggravate the business loss of traditional financial institutions and cause financial disintermediation.The third is price fluctuations and the market are linked.Stablecoins and crypto asset markets have a high correlation. At the same time, the current boundaries between crypto assets and traditional stocks are gradually blurring, showing a “coin-share integration” trend, which is reflected in the fact that crypto assets have begun to appear in traditional financial markets (such as Circle and other currency stocks listed, stablecoins and crypto asset-related targets affect stock prices through fundamental changes), and traditional financial institutions have begun to lay out the crypto asset field (such as providing crypto asset trading services, issuing stock tokenized products, and directly holding coins to participate in crypto asset investment, etc.), which has led to the enhanced price transmission and linkage effect between the entire crypto assets and the traditional financial market.

From stablecoins to RWA: Can everything be chained?

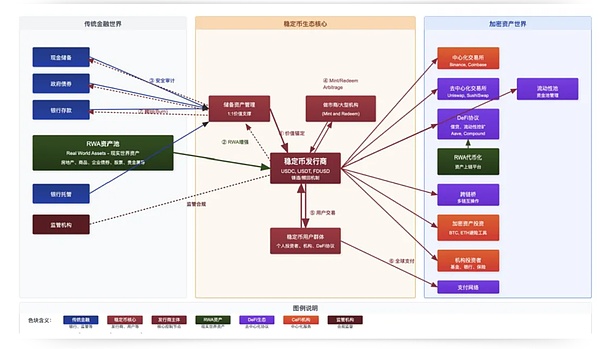

From a broader perspective, stablecoins are linked to the traditional financial and crypto assets world, focusing on the capital side, that is, the mapping of real-world funds on the chain.Corresponding to the asset side, the mapping of real-world assets on the chain, namely tokenized RWA.Looking forward, how do RWA and stablecoins jointly influence the on-chain ecosystem?Can all assets be listed on the chain?How will all things be rewrite traditional finance when they are on the chain?

Stablecoins and tokenized RWA are the mapping of real-world funds and assets on the chain, respectively, promoting each other and jointly improving the liquidity and activity of the on-chain ecosystem.Broadly speaking, stablecoins themselves are also a tokenized RWA, that is, the tokenized form of fiat currency. At the same time, stablecoins provide the funds and liquidity required for transactions for tokenized RWA.To summarize the characteristics of tokenized RWA, it is mainly reflected in:First, efficient,Execution of transactions based on blockchain smart contracts is more efficient and intermediary costs compared to the cumbersome processes under traditional IPO and ABS models and relying on a large number of intermediary institutions;The second is universal,Tokenized RWA can split assets into smaller units through tokenization, which helps to lower the threshold for investors to participate; at the same time, with the help of the cross-border characteristics of blockchain, tokenized RWA can achieve joint participation of global investors in the same asset, helping to expand market coverage.

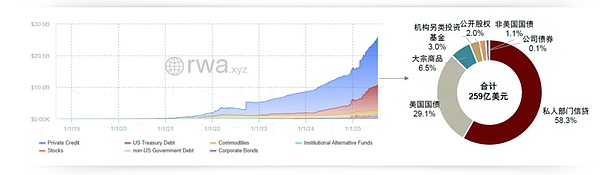

The difficulty of “all things are on the chain” does not lie in technology. Regulatory consideration of investor suitability and the size of capital demand may be the main constraints.Currently, the global tokenized RWA scale is nearly US$26 billion [13], which is still mainly financial assets including credit, treasury bonds, stocks, etc., while the proportion of tangible assets including commodities, real estate, etc. is relatively small.From the perspective of practical project cases, financial asset RWAs such as BlackRock BUIDL US bond rolling, Robinhood US stock tokenization, etc., tangible asset RWAs such as RealT’s real estate tokenization, charging piles of Ant Digital Technology and Langxin Technology, and photovoltaic power station rolling projects with GCL Energy Technology.However, looking forward, will stablecoins accelerate the integration with tokenized RWA and promote the “all things to be on the chain” process?We believe that the core issue is not the technology itself, but more in:On the one hand, based on the consideration of regulatory compliance,For example, in June, Robinhood launched the tokenized US stocks of US stocks to European customers, which lowered the threshold for investors to invest in US stocks, and launched OpenAI and SpaceX tokens, breaking the closure of traditional private equity. However, it should be noted that whether everyone is suitable for investing in tokenized US stocks, and whether everyone is suitable for investing in private equity shares?We believe that the so-called “financial democratization” may not meet the investor’s suitability requirements.On the other hand, for consideration of capital needs,For on-chain funds that are for speculation, tokenized RWA yield may not be attractive. At the same time, considering the scarcity of high-quality assets, not all over-chain assets have funding needs.Overall, there is still a long way to go to “all things on the chain”.

Chart 10: Stablecoins are becoming a key hub between traditional finance and crypto infrastructure

Source: Circle, Tether, MakerDAO, Binance, Coinbase, Uniswap, SushiSwap, Aave, Compound official websites and white papers, DeFiLlama, Messari, CICC

Figure 11: Global RWA scale is nearly US$26 billion, of which private equity credit/US bonds account for a high proportion

Note: As of July 19, 2025, institutional alternative investment funds include private equity, hedge funds, venture capital, etc.Source: rwa.xyz, CICC Research Department

How stablecoins affect the international monetary system

Among tokenization-related topics, its impact on the international monetary system has attracted much attention and constitutes an important part of the successful narrative of stablecoins.In “Asset Changes Under the Reconstruction of the Monetary Order”, we proposed that as the security of US dollar assets declines, the international monetary system is accelerating its diversification and fragmentation, promoting global capital to flow from the United States to other economies.In this process, the RMB has ushered in a critical period of opportunity to improve its international status with its advantages such as AI narrative transformation, resilience of China’s manufacturing industry, and structural quality of the balance sheet.However, the rise of stablecoins has introduced new complex factors to this process.Stablecoins are reshaping the global capital flow pattern by building a decentralized payment network parallel to the traditional dollar system.US Treasury Secretary Besent pointed out that stablecoins help consolidate the dollar’s global reserve currency status [14], and also triggered discussions on whether the dollar can re-expand on the “on-chain” with the help of stablecoins.How will stablecoins affect the international monetary system?The answer to this question will directly affect the strategic positioning of the RMB in the future monetary order.

How do stablecoins affect the international monetary system?

As mentioned above, from the essence, the credit of a stablecoin depends on the fiat currency it anchors (such as the US dollar) which is actually a digital token, not a separate currency.In its 2025 Annual Economic Report [15], BIS pointed out that stablecoins “maintain value commitments through the issuer’s reserve asset pool and their redemption capabilities.”This design makes it essentially a derivative of fiat currency rather than a separate currency.If measured by the three key standards of singleness, elasticity and integrity of the monetary system, stablecoins do not meet the requirements as the pillar of the monetary system.In terms of singularity, there is a price difference between different stablecoins due to the difference in credit of the issuer, which does not have a unified denomination like fiat currency; in terms of elasticity, their supply is strictly limited by the size of reserve assets, and it is impossible to create elastic currency through credit like the banking system; in terms of integrity, the anonymity of stablecoins leads to essential differences between stablecoins and regulated fiat currency.From this perspective, stablecoins rely on the existence of fiat currency credit and do not directly create new currency demand.There must be a demand for fiat currency before a stablecoin demand anchors the fiat currency.

However, the technical characteristics of stablecoins objectively create demands that traditional fiat currencies cannot meet, and may create new demand space in specific scenarios:First, stablecoins show unique alternative value in areas with weak financial infrastructure.Stablecoin is a new type of payment settlement tool. It uses blockchain technology to realize the integration of information flow and capital flow, shortening the traditional cross-border clearing time from 2-3 days to minute levels.This efficiency revolution may make stablecoins an important choice for underdeveloped financial infrastructure (such as Southeast Asia, Latin America, etc.) to replace the traditional proxy banking model, resulting in incremental demand for stablecoins.Secondly, the decentralized nature of stablecoins can meet the risk aversion demands of some countries, especially in areas where the political and economic situation is unstable, inflation is high, or where the market is large, stablecoins are particularly attractive.For example, Argentina has been suffering from inflation for a long time, with an average inflation rate of 189.97% from 1944 to 2024.The long-term persistent hyperinflation has made Argentina one of the countries with the highest demand for stablecoins in Latin America, with local residents holding large amounts of stablecoins such as USDT and USDC to cope with high inflation and currency depreciation.This phenomenon was particularly significant after the Argentine government abolished the monetary control measures “cepo cambiario” on April 14, 2025.The stablecoin market volume of Argentina’s cryptocurrency exchanges increased significantly after the country’s economic minister announced the measure [16].

In summary, in developed economies with sound financial systems, stablecoins mainly exist as derivatives of fiat currencies and do not create new monetary demand; but in areas with weak financial infrastructure or unstable macroeconomics, it may trigger deep currency substitution and create new demand for stablecoins.In the current global stablecoin market structure, US dollar stablecoins dominate, which essentially builds a global digital financial infrastructure for the US dollar system.By lowering the threshold for use and transaction costs of the US dollar, the US dollar stablecoin objectively expands the penetration range of the US dollar in global economic activities, which may further consolidate the US dollar’s reserve currency status.But this process is not without challenges.The dollar stablecoins are facing competitive pressure from two dimensions: on the one hand, the rise of non-US stablecoins anchored by major currencies such as the euro and the RMB; on the other hand, the accelerated development of digital currencies (CBDCs) of central banks in various countries.At present, the international monetary order is undergoing profound changes: factors such as the US debt problems and geopolitical conflicts have jointly promoted the continuous deepening of the “de-dollarization” process.This structural change has spawned the market’s incremental demand for non-U.S. currencies.Against this background, the emergence of stablecoins provides new opportunities for non-US economies to participate in currency competition.By building an alternative payment network based on blockchain, these countries have been able to establish new channels of currency circulation outside the SWIFT system.

Impact on China: Will stablecoins break through capital controls?

For China, stablecoins not only provide new tools for China to participate in global financial governance, but also pose new challenges to the existing regulatory system.

existCross-border trade, stablecoins may show two core advantages: First, as the world’s largest trade country, China has a natural scale advantage in the application of stablecoins.Stablecoins can bring about improved cross-border payment efficiency, avoid traditional high fees and cumbersome processes, and significantly improve capital turnover efficiency.Secondly, stablecoins have built a new decentralized payment network, breaking through the dilemma of having to use US dollars and agency banks for settlement, providing alternative payment channels for Chinese companies in a complex international financial environment, helping to enhance the resilience and flexibility of enterprises in global trade, and are of great strategic significance in the current geo-economic landscape.

existCapital MarketIn the field, stablecoins may improve financial popularity and strengthen the efficiency and liquidity of financial resource allocation.In some areas with backward financial infrastructure, stablecoins can provide low-threshold financial services portals.In addition, stablecoins provide new ideas for asset tokenization innovation, but their application requires careful evaluation of asset adaptability and investor suitability.Taking the case of Langxin Group in 2023 as an example, the group uses more than 9,000 charging piles as RWA anchor assets and issues digital assets representing part of the income rights based on Ant Chain technology.In the future, in charging payment, green energy settlement and other scenarios, stablecoins can play a payment settlement function, and smart contracts can also achieve automatic distribution of carbon emission reduction benefits.But it is necessary to be vigilant that not all assets are suitable for tokenization, and we must be vigilant about the risk of bubble formation caused by the introduction of everything on the chain.

However, as mentioned in Section 2, stablecoins themselves have many potential risks, and they also face the trade-offs of financial stability in addition to cost efficiency and inclusive expansion.In addition, two points should be paid special attention to China:

►Because stablecoins have strong anonymity, they can usually bypass traditional bank cross-border settlement systems without the need to accept strict foreign exchange or capital flow controls.May weaken the effectiveness of capital controls,There are even opinions that stablecoins may “break through” capital controls.From a technical perspective, there are indeed ways to regulate stablecoin accounts:At the technical level, capital control nodes can be set up on the public chain and transaction or performance specifications can be set on smart contracts; custodial wallets can also be monitored.But it is undeniable that stablecoin technology fundamentally solves the double coordination of wants, which may encourage cross-border “counterattack”.Compared with the traditional model, stablecoin pairs have faster turnover, lower costs and stronger anonymity.Traditional counter-knocking relies on underground money houses [17] as intermediaries, and capital flows are relatively easy to track; while stablecoin pairs reduce transaction thresholds and regulatory visibility.Specifically, under the traditional model, capital outflows need to be remitted to underground money houses through domestic accounts, and then the underground money houses remitted to overseas accounts in a complex chain, involving multiple exchanges of RMB and foreign currencies.In the stablecoin model, some intermediate links are omitted, which may improve transaction speed and concealment.

► Increased share of US dollar stablecoins may hinder the internationalization process of RMB.The global stablecoin market size has exceeded US$260 billion, of which more than 95% are eyeing US dollars.If the US dollar dominates the stablecoin field, it may squeeze the RMB’s cross-border payment share, which is not conducive to the internationalization process of the RMB.How should China respond to this situation?Do you want to participate in the development of stablecoins and how to participate?We will discuss it in detail in the next section.

Chart 12: Schematic diagram of the traditional mode vs stablecoin “tack” fund path

Source: CICC Research Department

How China participates in the development of stablecoins

Stablecoins have the potential to become infrastructure, and the germination period is an important development opportunity

Why should China participate in the development of stablecoins?Stablecoins connect fiat currencies and blockchain networks, with the potential to become a global financial infrastructure.The US dollar stablecoins represented by USDT and USDC dominate the market, and the total market value has increased by nearly ten times since the beginning of 2021.This digital currency has technical advantages such as 7×24-hour cross-border transactions, real-time settlements, and low-costs.It has the potential to become a replacement for traditional financial payment networks.History has proved that financial network technology innovation has profoundly influenced the international monetary pattern.In the 1970s, the SWIFT network replaced traditional telegram communications and built an interbank payment system dominated by the United States and other countries; credit card networks such as Visa formed a global network effect with electronic certification technology, supporting the global expansion of US dollar denomination.The global financial network established by the United States based on its technological advantages has laid the global monetary infrastructure status for the US dollar.

The current stablecoins are still far from the “mainstream financial infrastructure”. Institutions such as the Bank for International Settlements (BIS) pointed out that qualified stablecoins must meet the requirements of currency stability, supply flexibility, and compliance and credibility.The introductory period of infrastructure is an important development opportunity. If you can participate in the construction of new infrastructure at a reasonable cost, it may be conducive to the construction of a financial power.

Five paths of participation that are not suitable for China

If China wants to participate in the development of stablecoins, how should it participate?Before discussing how to participate in stablecoins, we believe that there are five more popular paths that have great limitations and are not suitable for actual implementation:

► Onshore RMB stablecoin.Stable coins issued by domestic institutions and supported by onshore RMB reserves conflict with the current financial management system.Anonymous transactions and decentralized settlements increase supervision difficulties.

► Stablecoin anchored to the central bank’s digital currency (CBDC).The digital RMB does not count interest payments, while existing stablecoins rely on reserve assets to cover costs.If the digital RMB is anchored, the issuer will either charge high fees to lose market competitiveness, or deviate from the 100% reserve requirement for venture capital, which violates the original intention of stablecoin design.

► Stablecoin anchored to gold.That is, the issuance of stablecoins supported by physical gold (such as “digital gold dollar”).Although gold is stable in value, it exists as a stablecoin anchor.Supply elasticity and cost benefits are two major problems.The total amount of gold reserves is limited and the incremental amount is scarce, which cannot meet the expansion needs of economic activities.A run during market panic may trigger a redemption crisis.Secondly, large-scale gold reservesHigh opportunity costs and holding costs,And no interest income is generated, and long-term holdings form negative interest spreads.

► Stablecoin anchoring the central bank’s reserve assets.Stable coins collateralized by national foreign exchange reserves or SDR,It may bind the country’s foreign exchange reserves to stablecoin liabilities, which implies huge risks.The core function of foreign exchange reserves is to maintain exchange rate stability and balance of payments security, and it is necessary to maintain high liquidity. The large-scale circulation of stablecoins will “lock” reserve assets, and the bank run may force the central government to use foreign reserves to repay.The central bank passively acts as the last guarantor of stablecoins and bears potential losses.

► Centralized asset tokenization (deposit token) stablecoins.First of all, low-risk asset stablecoins such as deposit tokens issued by commercial banks,Facing doubts about attractiveness and positioning.Domestic money market funds such as Yu’ebao have fully met residents’ demand for safe and convenient monetary assets, and then launched stablecoins with a lack of incremental value.Second,Stable coins issued by commercial banks are difficult to become a neutral public payment network.Financial institutions do not want to use stablecoins issued by competitors, which will damage the network effect of the stablecoins.In addition, banks convert deposits into low-interest stablecoin reserves, which is equivalent toDeposits are squeezed, If stablecoins cannot be used for lending, it will reduce bank profitability, conflict with traditional business models, and lack internal motivation.

Feasible path for China to participate in stablecoins: Offshore RMB stablecoins

Taking into account regulatory constraints and market demands in a comprehensive way,The issuance of “offshore RMB stablecoin” may be a priority for China to participate in the development of stablecoins.Its core idea is to issue digital stablecoins denominated in RMB and anchor the value of RMB by trusted institutions in overseas jurisdictions, but the restriction on its operation and circulation mainly occurs in overseas markets.With offshore RMB as reserves, circulation is limited to overseas markets and does not directly impact the domestic capital control system.The central bank can adjust offshore liquidity through tools such as currency swaps with the Hong Kong Monetary Authority to prevent overshooting in the exchange rate market.

at the same time,Offshore centers help to take advantage of Hong Kong’s institutional advantages as an international financial center.Hong Kong has a mature financial infrastructure, an independent rule of law environment and a large number of international players, and can flexibly design a stablecoin architecture to achieve compliance operations through local legislation and regulatory sandboxes.In short, “offshore issuance and offshore use” allows the RMB to participate in global digital currency competition while minimizing interference to the domestic financial system.

While issuing offshore RMB stablecoins, we must build real application scenarios in the fields of trade and investment and create a network for the use of RMB stablecoins..The success of the monetary network lies in the formation of network effects, and the basis of the network effect is rich use scenarios.Offshore RMB stablecoins should start with serving the real economy, focus on trade scenarios and investment scenarios, and create an ecological system that is “usable and inseparable”.In the field of trade settlement, chain owners with cross-border payment scenarios can be encouraged to issue stablecoins, including import and export entity enterprises that already have a certain cross-border trade volume, such as large home appliances and automobile manufacturers, as well as platform companies that operate cross-border trade, including JD.com, Alibaba, etc.In the field of financial investment, relying on Hong Kong, we develop stablecoin-denominated financial products.Chinese financial institutions are encouraged to issue stablecoin bonds, trade financing notes, etc. in the offshore market, and lower the threshold for international investors to participate.

The “Tao” and “Technique” of RMB internationalization: You cannot lose the roots and chase the end

Stablecoins are just the “art” to promote the internationalization of the RMB. Whether the RMB can become a widely trusted international currency fundamentally depends on the “Tao” – the “law anchor” and “function anchor” of the RMB.Only when the international community believes that the RMB has a solid sovereign credit and an expected policy environment can the RMB have the foundation to become a widely accepted international currency, which is the “legal anchor” of the RMB; only when the RMB is denominated in assets, smooth market flows, and complete risk management tools can international investors be more willing to hold and use the RMB, which is the “functional anchor” of the RMB.

On the road to participating in stablecoins, technological innovation should be steadily promoted to prevent losing the money and pursuing the end..Technological innovations such as stablecoins need to serve core goals and be wary of the risk of putting the cart before the horse.Technical means are important, but the willingness of investors and governments to the RMB depends on more macro factors such as China’s economic fundamentals, the stability of the financial system, and international political trust. It is possible to consider putting measures such as promoting RMB stablecoin under the overall framework of the national financial strategy, which complements the construction of the system and market. Only with the combination of strategic design and favorable opportunities can the internationalization of the RMB move forward steadily.