Author: Gui Ruofei Lucius

“Polymarket’s story reveals a “capital-driven compliance” compliance path.In the early stage of platform operation, the project party first puts compliance and prioritizes making the project bigger and stronger, and gains scale effect and first-mover advantage.Afterwards, the project party took advantage of the initial accumulation of funds and used capital leverage to actively carry out compliance transformation through acquisitions and other methods, thereby achieving legalization and further expansion of the business.This is not only a compliance strategy, but also a business strategy.”

Traditional American polling agencies never thought that what replaced them was not advanced artificial intelligence, but actually a Web3 prediction platform.In the 2024 general election, survey data from a number of polling agencies showed that Harris had a clear advantage in approval rating compared to Trump.However, the prediction results of the Polymarket platform are very different from those of the polling agency, and Trump’s probability of winning has always been far ahead of Harris.In the end, as Trump swept Harris to win the 2024 presidential election with a crushing advantage, Polymarket became famous and began to enter the public eye.

However, behind the rapid development of Polymarket, compliance issues and regulatory pressure have always lingered, becoming the biggest obstacle to its further expansion and development.Faced with the aggressive regulatory authorities of various countries, Polymarket has embarked on a unique compliance path.This article will come from a professional perspective of the Web3 industry and cross-border compliance.In-depth analysis of the current regulatory status, compliance risks and compliance path of Polymarket, for reference by later Web3 entrepreneurs and project parties.

01What exactly is Polymarket?

As an emerging Web3 prediction market platform, since its establishment in 2020, Polymarket has quickly gained a foothold in the prediction market and became the leader in the track with its transparency and decentralization based on blockchain technology.Polymarket’s forecast market coverage is extremely wide, spanning political events, capital markets, economic indicators, sports events and even social and cultural events.The breadth of its predictable events is key to its appeal to a large number of users, but it also adds to the complexity of its classification and regulation in different jurisdictions.Users make event predictions on Polymarket mainly by purchasing event tokens with specific results, and the token price fluctuates between USD 0 and USD 1.Therefore, the event token price of Polymarket will also reflect in real-time the collective perception of the probability that this particular result will occur.

Polymarket’s core value proposition is thatWith blockchain technology innovation, transforms the original abstract prediction perspective into priceable and tradable digital assets, and allows users to benefit from it.For example, during the 2024 election, the token price of the bet on “Trump Win” event climbed from the initial $0.3 to $0.92, and was finally cashed at $1 when the election results were announced.This price change accurately captures the true turn of public opinion in the general election and creates a significant wealth effect for users who predict successful results.

Polymarket’s rapid rise in the Web3 forecasting market has also made it favored by the capital market.So far, Polymarket has successfully completed two rounds of financing, raising a total of more than US$70 million.Its investors include Vitalik Buterin, the famous co-founder of Ethereum, and Founders Fund, owned by Peter Thiel.

02A brief analysis of the global regulatory dilemma of Polymarket

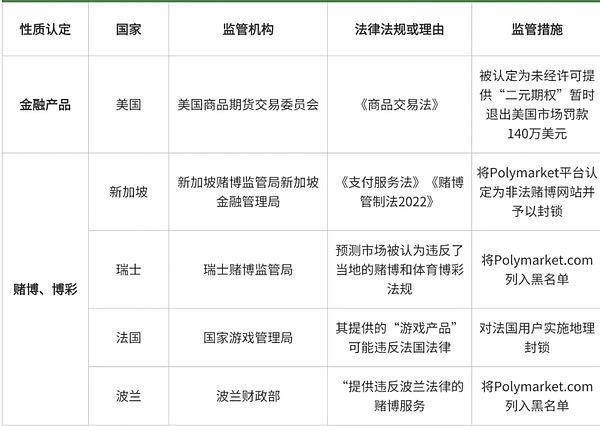

2.1 United States: Determined as binary options and finally settled with CFTC

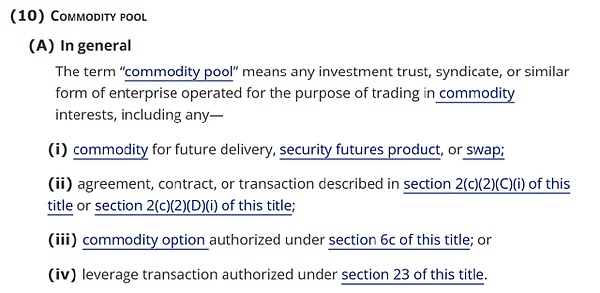

In the US market, Polymarket’s earliest compliance difficulties arose due to strict law enforcement by the U.S. Commodity Futures Trading Commission (CFTC).In January 2022, the CFTC imposed a civil fine of $1.4 million on Polymarket and issued a stop and termination order.According to relevant contents of the United States Commodity Exchange Act, the CFTC believes that the “Event Contracts” provided in the Polymarket forecast market fall within the jurisdiction specified in the Commodity Exchange Act.The Commodity Trading Act clearly stipulates that the CFTC has the power to regulate the “Future delivery, Security futures product, or Swap”.

Therefore, when the forecasting market allows users to bet on events such as election results, economic indicators, etc., the CFTC tends to view the product as a kind ofBinary options or swap contracts, thereby incorporating its exclusive jurisdiction over the derivatives market.That is, the CFTC believes that the nature of the “event contract” provided by Polymarket belongs to financial derivatives within its jurisdiction, rather than gambling or gambling.Therefore, the core of the CFTC’s allegation is that Polymarket operates an unregistered derivatives trading platform, andFailed to register as a swap execution agency (Swap Execution Facility) or a Designated Contract Market through the CFTC as required by the Commodity Exchange Act.

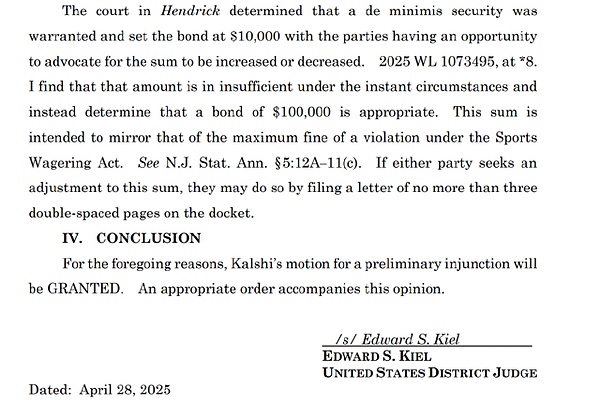

In addition, the forecast market where Polymarket is located is also facingA tug-of-war between federal and state regulators.The CFTC attempts to exercise exclusive jurisdiction over the forecast market through the Commodity Exchange Act, deeming it as an “event contract.”However, the US partState gambling regulators have viewed the forecast market as “illegal gambling” and filed a lawsuit.For example, on March 27, 2025, New Jersey Gambling Law Enforcement issued a cessation order to Polymarket’s direct competitor Kalshi, prohibiting it from providing sports betting services without permission.

In this regard, Kalshi has launched a protracted legal battle with gambling regulators in New Jersey and other places.Although New Jersey District Court Judge Edward Kiel found that the sports event contract provided by Kalshi belongs to the exclusive regulatory scope of the CFTC, he ruled that the New Jersey regulatory authorities stop interfering in Kalshi’s normal operations,But such disputes have not yet been concluded.This dispute over jurisdiction between the federal and state will further intensify the uncertainty of the U.S. forecast market regulatory environment.

Therefore, for platforms like Polymarket, even if they obtain federal licenses, they may face legal challenges and litigation risks from state-level levels.This situation of coexistence of “double supervision” and “regulatory vacuum” not only increases the platform’s compliance costs, but also hinders its comprehensive expansion in the US market.

2.2Europe: Determined as gambling, included in the blacklist

However, Polymarket’s compliance challenges are not limited to the United States.In other jurisdictions around the world, Polymarket is also facing severe regulatory pressure.In the EU,Crypto Asset Market Supervision Act (MiCA Act)The implementation of the company has established a unified regulatory framework for crypto asset service providers (CASPs) and covers asset reference tokens (ARTs), electronic currency tokens (EMTs) and other crypto assets that are not covered by existing financial services legislation.However, the MiCA Act does not explicitly include the forecast market in its regulatory scope, leaving room for discretion for countries to regulate independently in accordance with their gambling laws.Therefore, even if the MiCA Act provides a unified authorization framework for EU crypto asset services,Predicting market platforms still need to face fragmented supervision in European countries.

In Europe, from November 2024 to January 2025,Regulators in multiple countries have successively taken regulatory measures against Polymarket.The Swiss Gambling Authority blacklisted Polymarket.com on November 26, 2024, citing its forecast market as being considered to have violated local gambling and sports betting regulations.The French National Games Administration announced on November 29, 2024 that after investigation, Polymarket has agreed to impose a geographical blockade on French users because the “game products” it provides may violate French law.

The French regulator’s action was reportedly stemmed in part from the regulatory concerns mentioned above that French traders made huge US election bets on the Polymarket platform.Immediately afterwards, the Polish Ministry of Finance also blocked the visit of its residents to Polymarket.com on January 8, 2025 on the grounds of “providing gambling services that violate Polish laws.”

From this we can see that European countries generally adopt a conservative and prudent regulatory attitude towards the forecasting market led by Polymarket. Most regulators regard the forecasting market as gambling activities and strictly regulate and restrict them in accordance with their respective gambling laws.

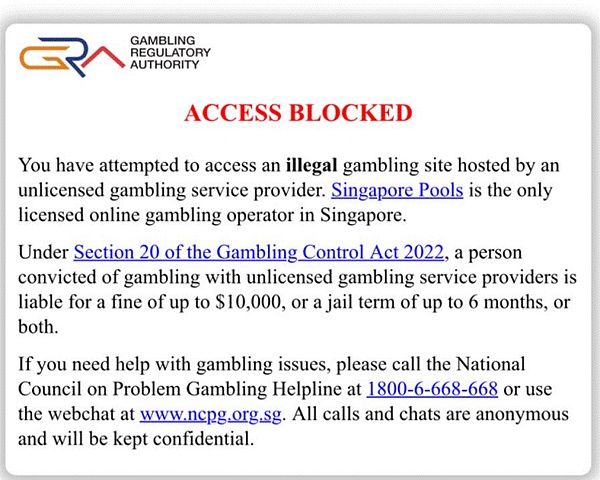

2.3 Singapore: Violation of two bills

Singapore’s regulatory framework for forecasting markets is combined withTwo bills, the Payment Services Act and the Gambling Control Act 2022, are two bills., “surround the Polymarket from different angles” respectively.First, the Monetary Authority of Singapore strictly licenses and regulates digital payment token service providers in accordance with relevant provisions of the Payment Services Act.The Monetary Authority of Singapore believes that the Polymarket platform operates digital payment token services without permission, and emphasizes that it has serious anti-money laundering/anti-terrorist financing (AML/CFT) risks, and lacks investor protection mechanisms and user dispute resolution mechanisms.

At the same time, the Singapore Gambling Regulatory Authority also identified the Polymarket platform as an illegal gambling website and blocked it in accordance with the Gambling Control Act 2022.The Gambling Control Act 2022 clearly states that only nationally licensed platforms (such as Singapore Pools) allow online gambling services to be provided in Singapore.therefore,Polymarket faces dual compliance challenges in Singapore, which must not only comply with the licensing and regulatory requirements for digital payment token services under the Payment Services Act, but also avoid violating the strict gambling industry access restrictions set by the Gambling Control Act 2022.

From the regulatory comparison of the above jurisdictions, it can be clearly observed that there is significant regulation of the forecast market by global regulators.“Financialization” and “gambling” are dichotomized.For example, the US CFTC tends to regard the forecast market as an “event contract” under the Commodity Exchange Act (CEA), trying to include it in the regulatory framework of financial derivatives such as options and swaps.This nature classification recognizes the potential value of the forecast market in terms of information discovery and risk hedging, but also requires it to assume strict regulatory responsibilities in the financial market, including CFTC registration, KYC/AML and reporting suspicious transactions.

However, in some European countries (such as Switzerland, France, Poland) and Singapore, regulators have clearly classified platforms like Polymarket as “illegal gambling” and have taken lockdown measures.This reflects that these countries focus more on controlling the speculative nature of the forecast market, potential social harm and moral hazard, and therefore put it under the usually stricter framework of gambling controls and consumer protection.

The challenge with Polymarket is that itA customized compliance strategy must be adopted in a global environment that lacks unified regulatory standards to address different requirements in different jurisdictions., which undoubtedly greatly increases the complexity of its operations and compliance costs.This difference in the recognition of the nature of the forecast market is not accidental, reflecting the delicate balance between financial innovation, consumer protection and public ethics of regulators across countries.

03Surviving in the cracks, how does Polymarket deal with compliance?

3.1United States: Actively compliant, return to the acquisition

Faced with the aggressive CFTC, Polymarket was sincere in the investigation process.And show a positive attitude of “substantive cooperation”.A good attitude and positive communication have also won a relatively low fine for Polymarket.In January 2022, Polymarket officially signed a settlement agreement with CFTC. Polymarket acknowledged that some of its trading activities are within the scope of CFTC’s supervision.Binary options trade and agreed to pay a fine of approximately $1.4 million.

As one of the key terms of the settlement agreement, PolymarketPromising to stop providing platform services to US users from 2022, and geo-block US IP addresses.Since then, Polymarket has moved its core forecasting business to operate offshore to circumvent domestic regulatory restrictions and compliance risks.It is worth noting that even though Polymarket claims to impose geographical restrictions on American users, there are still reports that some American users use VPN and other technical means to evade restrictions and continue to participate in platform transactions.On the one hand, this phenomenon reflects the limitations of geo-blocking technology based on IP addresses, and on the other hand, it also shows a solid user base for the prediction market.

To better adapt to the regulatory environment in the United States and prepare for a return to the United States,Polymarket appoints former CFTC member J. Christopher Giancarlo as chairman of its advisory committee in May 2022.Relevant reports pointed out that this move aims to help Polymarket better plan its compliance path and establish effective communication channels with regulators based on Giancarlo’s deep understanding of the CFTC operation model and regulatory logic.This“Hiring former staff of regulatory agencies to provide compliance consulting services”, it is not uncommon among companies in the fields of medicine, finance, etc. in the United States.

However, in November 2024, Polymarket’s compliance storm recurred.FBI raided Polymarket CEO Shayne Coplan’s New York residence and seized his cell phone and other electronic devices, but he was not arrested.The main purpose of the FBI’s operation is to investigate whether Polymarket violates a previous settlement agreement with the CFTC because Polymarket allegedly failed to prevent US users from continuing to trade on the platform through VPNs and other means.

However, just recently, with the Trump administration taking office and crypto-friendly policy regulatory orientation, Polymarket’s compliance prospects in the United States have seen a major turn.On July 15, 2025, official reports officially confirmed that the U.S. Department of Justice (DOJ) and CFTC have officially concluded the investigation into Polymarket and have not filed any new charges.This progress marks the finally basically resolved since the CFTC penalties in 2022 and the FBI’s enforcement actions against Shayne Coplan in 2024.

Polymarket also followed closely, officially announcing the acquisition of QCEX, a derivatives exchange and clearing house that has been licensed by CFTC on July 21, 2025.The strategic acquisition was hailed by Polymarket founder and CEO Shayne Coplan as the iconic move of “taking Polymarket home” to provide a “fully regulated and compliant framework” for Polymarket’s operations in the U.S. market.It happened that QCEX officially obtained the CFTC’s designated contract market (DCM) license on July 9, 2025, and Polymarket completed the acquisition of QCEX 12 days later.With QCEX’s ready-made DCM license, Polymarket has finally been able to re-legalize its users to US users and temporarily get rid of the worries of compliance risks.

On the surface, Polymarket solved the compliance problem by simply acquiring QCEX, which has a DCM license, and returned to the US market.But in fact, the changes and compromises made by Polymarket for compliance are much more than that.Among them, Polymarket’s change in attitude towards KYC/AML is the key to its compliance transformation.The early features of Polymarket were the “anonymity” of KYC and the “decentralization” of transactions.Polymarket also relies on the above characteristics to quickly gain a foothold in the highly competitive forecasting market and continue to expand.However, such operational strategies bring risks of “regulatory uncertainty” and “market manipulation” to the platform.As Polymarket returns to the United States through its acquisition of QCEX, it is likely that Polymarket will adopt the strict KYC/AML policy that must be followed by as a CFTC licensed entity.

Specifically, licensed entities under the CFTC regulation require customer identification procedures (CIP), customer due diligence (CDD) and enhanced due diligence (EDD), as well as ongoing transaction monitoring and reporting of suspicious activity.This also marks the need for a continuous trade-off between decentralization and regulatory compliance.Polymarket’s transformation is not just to meet regulatory requirements.It is also the inevitable result of its transformation from Web3’s “wild growth” model to regulated financial service institutions.

3.2Other countries and regions: Conservative strategy + active retreat

Compared with the United States, Polymarket’s compliance strategies in other countries and regions are relatively conservative.Faced with the “gambling” characterization and prohibitive requirements of the forecast market in Europe and Singapore, Polymarket did not raise any objections, but agreed to implement a geographical blockade of countries such as France and Singapore and withdraw from the local market.

04What are the important inspirations for Web3 entrepreneurs?

After analyzing Polymarket’s bumpy compliance path in detail, the author believes that other Web3 entrepreneurs should at least learn the following inspirations:

1.The Web3 industry has gradually escaped from the stage of “wild growth”More and more projects are beginning to enter the public eye and mainstream market.If Web3 projects want to truly become bigger and stronger and go mainstream, compliant operations are the general trend.

2. Whether Web3 projects can truly achieve compliance depends not only on the company’s compliance strategy.It will also be closely related to the country’s policy orientation and regulatory strength..Polymarket can ultimately achieve compliant operations, and the Trump administration’s coming to power and policy shifts are of great contribution.

3. Polymarket’s story reveals oneA “capital-driven compliance” compliance path.In the early stage of platform operation, the project party first puts compliance and prioritizes making the project bigger and stronger, and gains scale effect and first-mover advantage.The project party will use the advantages accumulated in the early stage to raise funds.Use capital leverage to actively carry out compliance transformation through acquisitions and other methods, thereby achieving legalization and further expansion of the business.This is not only a compliance strategy, but also a business strategy.

4.The regulatory arbitrage window for the Web3 industry around the world is narrowing rapidly, and the compliance costs of the entire Web3 industry are also increasing.As the crypto market matures, global regulators are strengthening cooperation and filling regulatory loopholes, making it increasingly difficult to achieve strategies to circumvent compliance by simply “regulatory arbitrage” or “offshore operations”.Polymarket’s “grow first and then compliant” route may no longer apply to the new regulatory environment.Both Web3 project parties and entrepreneurs need to have a deeper understanding and understanding of the importance of compliance.In the future, the competition in the Web3 industry will not only be limited to technology and products, but also a competition of compliance capabilities and capital strength.